By Mila Sherman, PhD, Professor of Finance, Shhreya Anand, Jonathan Fula, Hurditya Lohia (students), and Alternatives Class Advisor: Kristen Walters (alumni)

Isenberg School of Management, UMASS Amherst and Center for International Securities and Derivatives Markets (CISDM)

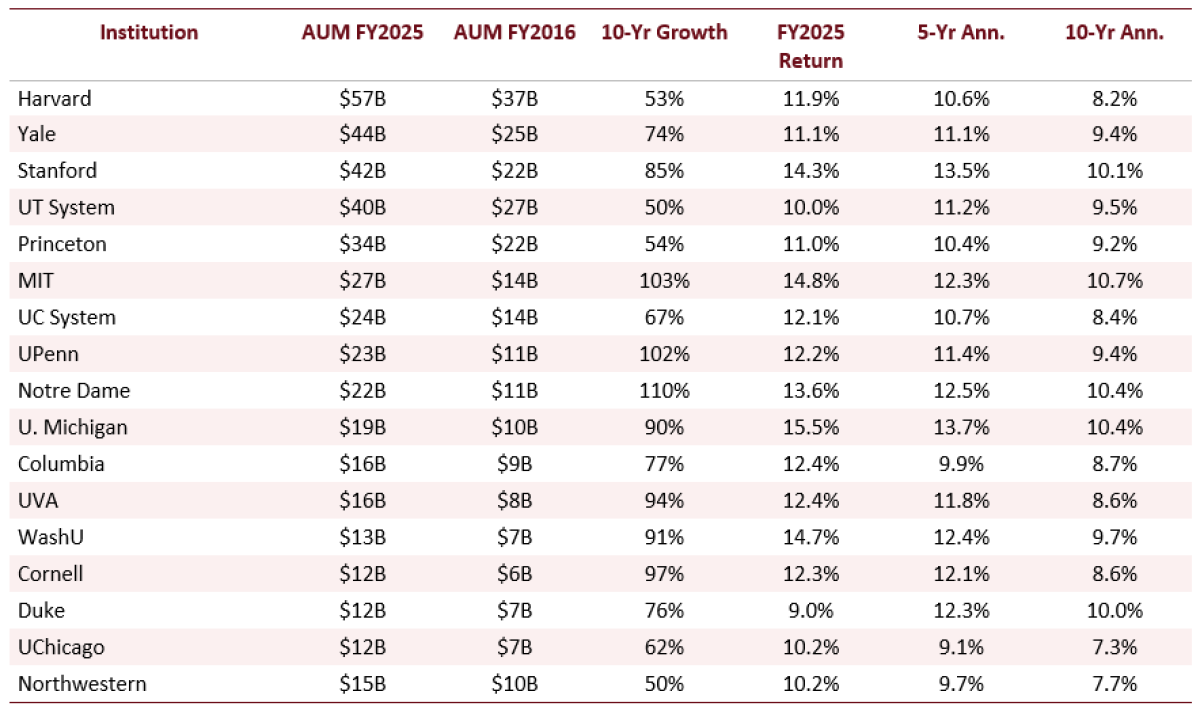

The 17 largest U.S. university endowments collectively grew from roughly $249 billion in FY2016 to $426 billion by FY2025, an increase of approximately 70-73% depending on rounding, driven by both investment performance and new gifts. Behind that aggregate figure is a more instructive story: three distinct allocation philosophies, meaningfully different risk profiles, and a structural gap that only becomes visible when these endowments are benchmarked against global institutional peers. This article draws on the 2025 NACUBO-Commonfund Study of Endowments, individual fund annual reports, and FIS-APT multi-factor statistical risk model output to examine what the top 17 endowments reveal about allocation, risk, and efficiency.

A Decade of Growth: Returns Are Strong, But Long-Term Leaders Differ

Combined AUM grew from roughly $247 billion in FY2016 to approximately $426 billion by FY2025, a gain of about 70-73% through investment returns and new gifts. Table 1 presents the full picture by institution. Michigan led in FY2025 with a 15.5% net return, followed by MIT at 14.8%, WashU at 14.7%, and Stanford at 14.3%. Over five years, Michigan, Stanford, Notre Dame, WashU, and MIT all exceed 12% annualized returns. Over ten years, MIT, Michigan, Stanford, Notre Dame, and Duke lead. Harvard, despite holding the largest AUM at $57 billion, posts an 8.2% ten-year return, the lowest among the top five by assets. The best one-year performers are not always the strongest long-term compounders.

Table 1. AUM Growth and Net Returns: Top 17 Endowments (FY2016-FY2025)

Note. Source: 2025 NACUBO-Commonfund Study of Endowments; individual endowment annual reports. Returns are net of investment management fees and exclude distributions and operating expenses. AUM growth reflects investment returns and net new gifts. Some figures estimated where not publicly disclosed.

Three Philosophies: How the Largest Endowments Actually Differ

Table 2 highlights three institutions that best illustrate the philosophical range within the top 17: Harvard as the largest endowment at $57 billion and the clearest example of private-equity concentration; Yale as the originator of the diversified-alternatives model that shaped how the industry thinks about endowment portfolio construction; and Michigan as the top FY2025 performer at 15.5%, driven by a venture-capital-heavy posture that has compounded into a 13.7% five-year and 10.4% ten-year annualized return. Together these three institutions show that there is no single path to long-term outperformance.

Table 2. Three Endowment Case Studies: Harvard, Yale, and Michigan (FY2025 Standardized Allocation Categories)

Note. Source: FY2025 institutional reports and APT/UMass standardized allocation mapping. Categories are presented in comparable asset-class buckets and may differ from each institution's exact public-report labels. Rows may not sum to 100% due to rounding and category mapping.

Harvard -- Concentration Model: 41% in private equity and 31% in hedge funds, with no venture capital sleeve. Harvard accepts significant illiquidity and manager concentration in exchange for private-market return premia. Its 8.2% ten-year return reflects the cost of its earlier transition period despite strong recent one-year performance at 11.9%.

Yale -- Diversified Alternatives Model: 24% in venture capital, 20% in private equity, and 22% in hedge funds reflect the broad alternatives diversification that David Swensen pioneered and that has since become the benchmark others are measured against. Yale's 11.1% one-year and 9.4% ten-year returns demonstrate that disciplined diversification compounds consistently over long horizons.

Michigan -- Growth-Concentrated Model: 33% in venture capital and 11% in private equity, with 13% each in hedge funds and real assets. Michigan led the peer group in FY2025 at 15.5%, and its 13.7% five-year and 10.4% ten-year annualized returns confirm that this is a durable strategic posture built across multiple market cycles, not a single-year outcome driven by AI-related public market valuations.

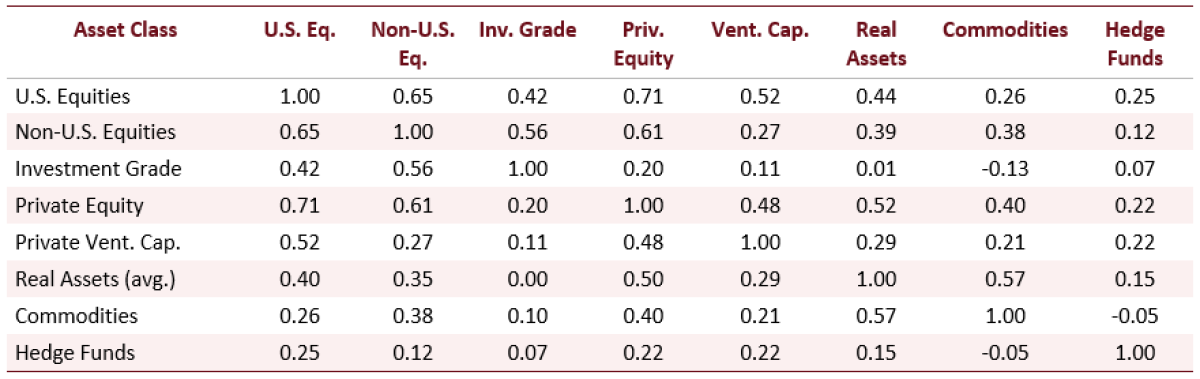

Diversification: Real Assets and Hedge Funds Stand Apart

Despite broad diversification into alternatives, not all alternatives reduce risk equally. Table 3 presents selected ex-ante correlation estimates from the APT model. Because Real Assets is presented as an approximate composite category, Table 3 should be read as a selected correlation summary rather than a complete symmetric matrix. The contrast between private equity and hedge funds is the most decision-relevant finding for practitioners.

Table 3. Selected APT Correlation Estimates Across Asset Classes (APT Model)

Note. Source: APT model, UMass Amherst Endowment Research Project (2026). Real Assets is an approximate composite based on several real asset sub-categories, so pairwise values should be interpreted as selected model estimates rather than a mathematically complete symmetric correlation matrix. Full model correlation output is available in the underlying workbook.

Private equity shows 0.71 correlation with U.S. equities and venture capital 0.52 -- both retain meaningful equity beta. Real estate and private energy carry similar exposures. Hedge funds (as model by the Global HFR Index), by contrast, show only 0.25 with U.S. equities and 0.12 with non-U.S. equities; commodities show -0.05 with hedge funds. This is why 86% of ex-ante volatility across large endowments still emanates from the equity factor, even in portfolios with 60%+ in alternatives. Endowments did not eliminate equity risk; they shifted it toward manager selection, valuation timing, and illiquidity.

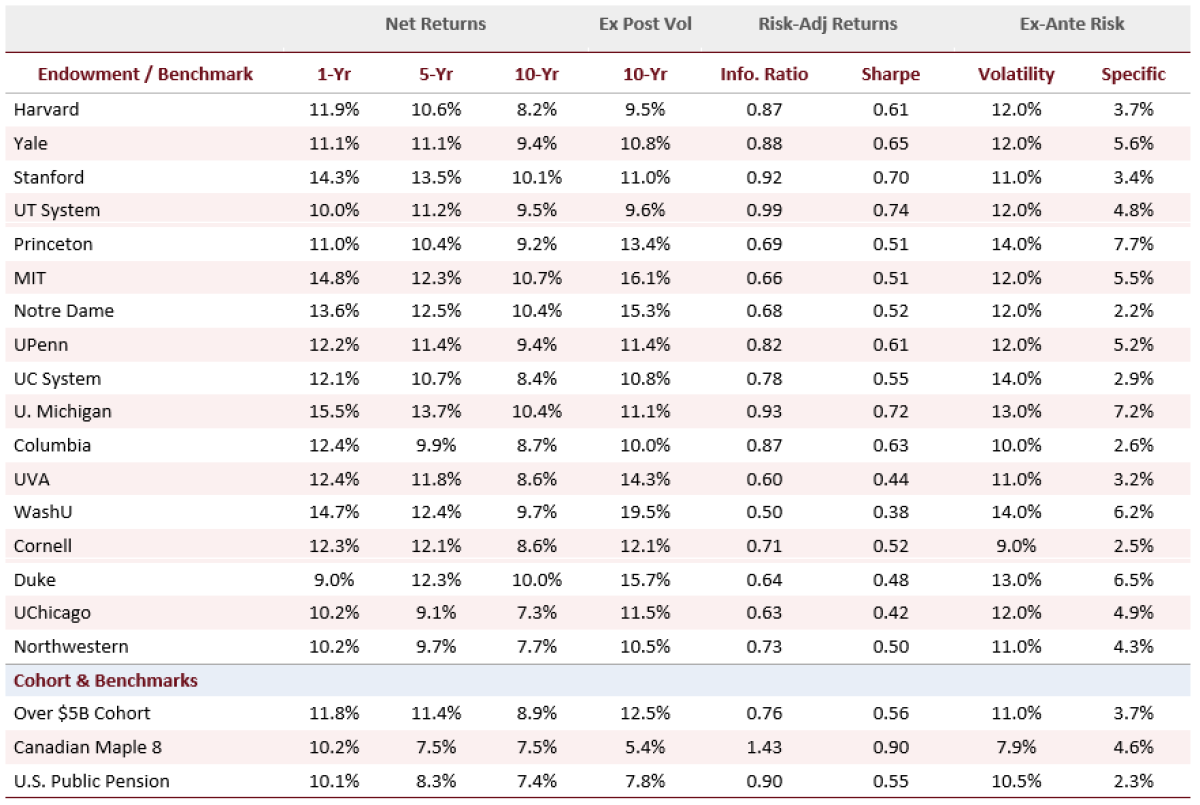

Risk Profile: Higher Returns, But Lower Risk-Adjusted Efficiency

Table 4 presents the full APT risk model output for each institution and the three benchmark portfolios. The largest 17 endowments outperform U.S. and Canadian pension peers over 1-year, 5-year, and 10-year horizons at 12%, 11%, and 9% respectively for the Over $5B cohort, but with higher ex-ante risk (~11%), higher potential losses (approximately 20% in a 1-in-20-year event), and lower risk-adjusted returns. Sharpe and Information Ratios for the Over $5B cohort are 0.56 and 0.76 versus the Canadian Maple 8 at 0.90 and 1.43

Table 4. Ex-Ante Risk, Net Returns, and Risk-Adjusted Performance by Endowment Plan (APT Model Output)

Note. Source: APT model output, UMass Amherst Endowment Research Project (2026). Net returns are from 2025 NACUBO-Commonfund Study and individual annual reports. Ex post volatility is 10-year realized. Sharpe Ratio uses the workbook's 3.1% risk-free rate. Information Ratio is reported directly from the APT workbook. Ex-ante volatility and systematic/specific risk from the TLA_ST tab.

The Sharpe ratio range across the 17 endowments runs from 0.38 (WashU) to 0.74 (UT System), while the Canadian Maple 8 achieves 0.90. WashU's 19.5% ex-post volatility over ten years is the highest in the group and explains how a 9.7% ten-year return produces only a 0.38 Sharpe despite competitive raw performance. Cornell and Columbia, by contrast, show the lowest ex-ante volatility in the individual endowment group at 9.1% and 9.6% respectively, and above-average Sharpe ratios relative to peers with higher headline returns. The Maple 8's 1.43 Information Ratio versus the Over $5B cohort's 0.76 represents the clearest single-number expression of the efficiency gap.

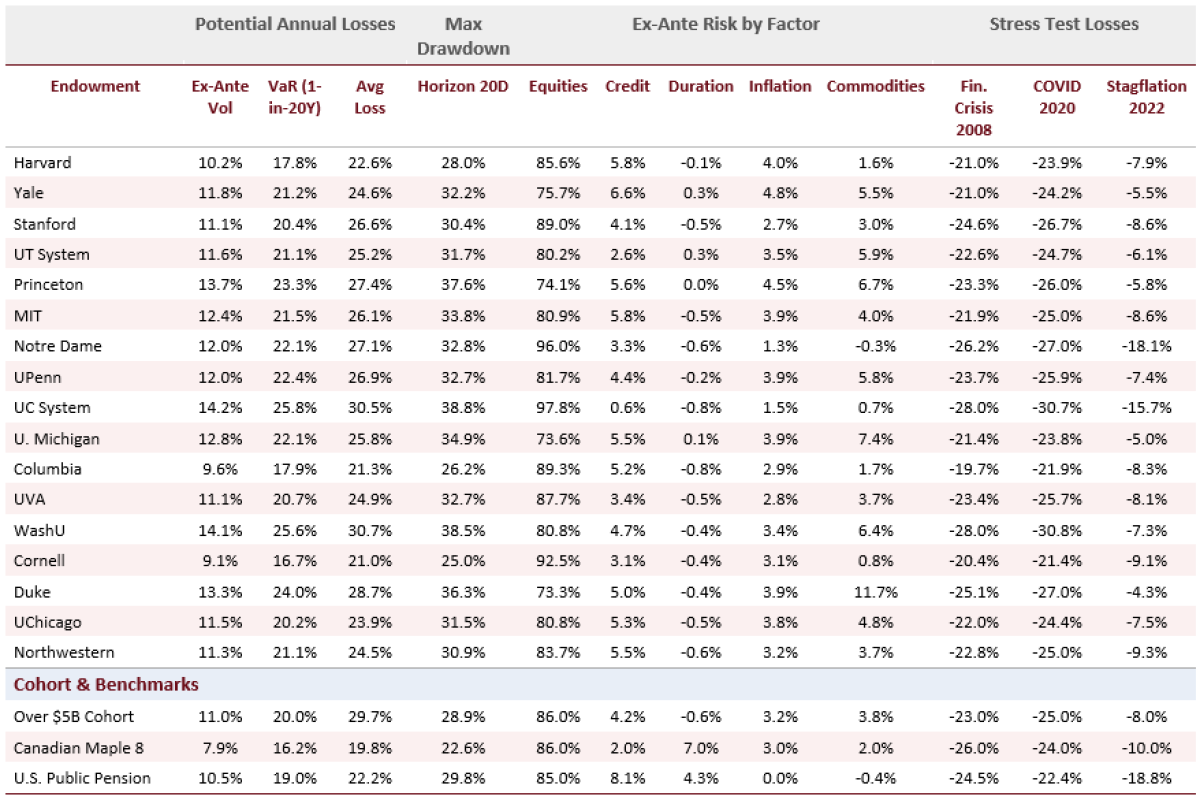

Stress Tests: When Equity Risk Dominates

Table 5 presents stress-test losses and factor attribution for each institution and benchmark. Despite diversification into alternatives, 86% of ex-ante volatility across large endowments emanates from equity factor risk, which produces significant losses in stress scenarios. The COVID scenario (March-April 2020) sees most endowments lose 21-27%. In a repeat of the early 2022 inflationary environment, however, endowments fare better than pension peers, with the Over $5B cohort losing approximately 8% compared to 22-25% for the benchmark portfolios, as real assets and hedge fund exposures provide a partial inflation hedge.

Table 5. Potential Losses and Factor Risk Attribution by Endowment Plan (APT Model Output)

Note. Source: APT model output, UMass Amherst Endowment Research Project (2026). VaR and Average Loss are 1-in-20-year annual loss estimates. Max Drawdown Horizon is 20 days. Factor attribution percentages are selected model factors and may not sum to 100% because Currencies and Other factor exposures are omitted for space. Stress test losses are scenario-based estimates: Financial Crisis (June-December 2008), COVID (March-April 2020), Stagflation (January-October 2022).

Several findings stand out. Notre Dame's 96% equity factor attribution and -18.1% stagflation loss is the starkest in the group, reflecting its public-equity-heavy posture. Duke's 11.7% commodities factor share -- the highest in the peer group -- contributed to its smaller -4.3% stagflation loss, with real assets and natural resources exposure providing meaningful inflation hedging. The Maple 8's 7.0% duration factor attribution versus -0.1% to 0.3% for most endowments reflects its higher fixed income exposure (achieved partly via leverage); this explains both its lower ex-ante volatility and its -10.0% stagflation loss, worse than most endowments despite a lower overall volatility profile.

The UC System and Notre Dame show the two largest stagflation losses at -15.7% and -18.1%, driven by their high equity factor concentrations at 97.8% and 96.0%. The U.S. Public Pension shows the largest stagflation loss of the benchmarks at -18.8%, consistent with its mandatory fixed income allocation creating mark-to-market losses when rates rise sharply. The COVID scenario shows less dispersion across institutions, as most portfolios lost 21-27%, reflecting widespread equity beta that alternatives could not fully offset during a rapid global liquidity event.

Key Insights for Investment Professionals

1. Raw returns require a volatility adjustment before comparison. WashU's 9.7% ten-year return and Cornell's 8.6% ten-year return look similar in isolation, but WashU carries 14.1% ex-ante volatility versus Cornell's 9.1%. On a Sharpe basis, Cornell's disciplined approach produces a more efficient outcome for the risk accepted. Table 4 makes this comparison explicit across all 17 institutions.

2. Factor attribution explains stress-test outcomes better than allocation labels. Institutions with similar alternatives percentages can have very different equity factor shares, and that equity share is the dominant driver of both the Financial Crisis and COVID losses. Real assets and commodities exposure, specifically in energy, natural resources, and infrastructure, is what drove differentiated stagflation outcomes in 2022.

3. The Maple 8 approach is structurally different, not just strategically different. U.S. endowments use real assets and hedge funds to diversify away from equity markets. The Maple 8 uses leverage -- from debt, repo, and derivatives markets -- to diversify exposure (e.g., via Fixed Income). Both approaches improve risk-adjusted returns relative to a traditional portfolio but do so through different mechanisms with different risk profiles. The Maple 8 achieves a Sharpe ratio of 0.90 and Information Ratio of 1.43 versus 0.56 and 0.76 for the largest U.S. endowment cohort. Closing that gap would require U.S. endowments to adopt balance sheet leverage and direct-investment infrastructure that current governance structures do not support.