Authored by Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP, Managing Director, Content & Community Strategy

“Human beings have a remarkable ability to accept the abnormal and make it normal.”

Andy Weir’s Project Hail Mary is a fantastic book, which was just made into an equally compelling film. Read it or go see it (in a theater!) if you can. In the book, a lone astronaut wakes up with no memory aboard a spaceship, gradually recalling that he was given an impossible choice: volunteer for a one-way suicide mission to save humanity, or stay home and die with everyone else when Earth’s sun slowly fails from an unknown sun-eating organism.

While not as existential, our industry is running two very different experiments at the same time, and at some point, we’re going to find out which one wins out.

On one track, you have semi-liquid vehicles: interval funds, tender offer funds, non-traded REITs, and BDCs. Products designed to give wealth channel investors something in between the 10-year lockup and the daily redemption window. On the other track, you have tokenization. Blockchain-enabled fractional ownership, real-time settlement, 24/7 trading, and programmable transactions. The technology isn’t new, but the use case is: rebuilding market infrastructure from the ground up on digital rails.

In our recent report, The World Rewired, we asked the CAIA community about the future of product development. 29.2% of respondents identified tokenized private markets with 24/7 digital exchanges as the innovation most likely to alter how investors allocate capital. Evergreen and semi-liquid fund structures came in second at 27.7%. [2] Which one wins?

Two parallel tracks, both chasing the same goals. Or are they?

What the Data Actually Shows

Before going further, it is worth pausing to take stock of the current universe and to be honest about AUM comparisons, which are more complicated than they first appear. I’ve caught myself mixing numbers before, so putting it all down on paper was a useful reset.

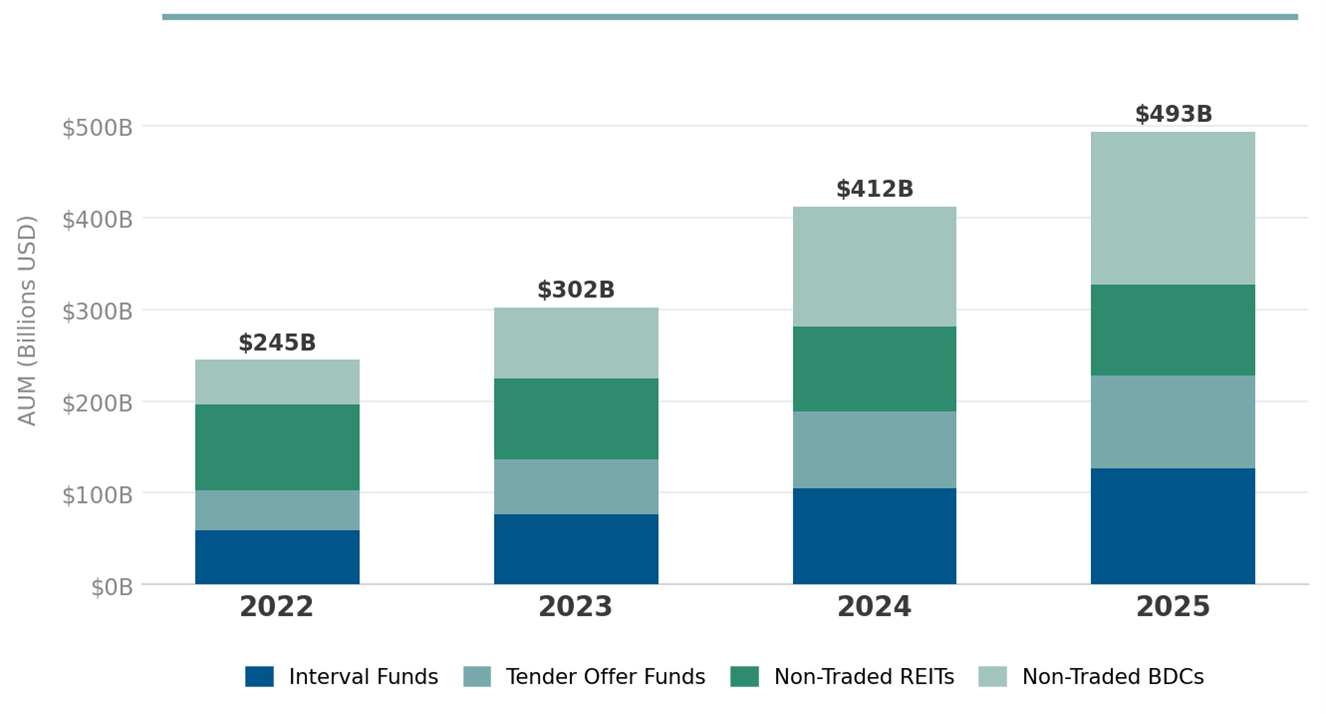

According to data from Pitchbook, semi-liquid AUM doubled from almost $250 billion in 2022 to $500 billion by the end of 2025. [1] This is a pretty defensible number because these figures are required to be shared and we have very good data providers who can verify them.

Source: Pitchbook, CAIA Association

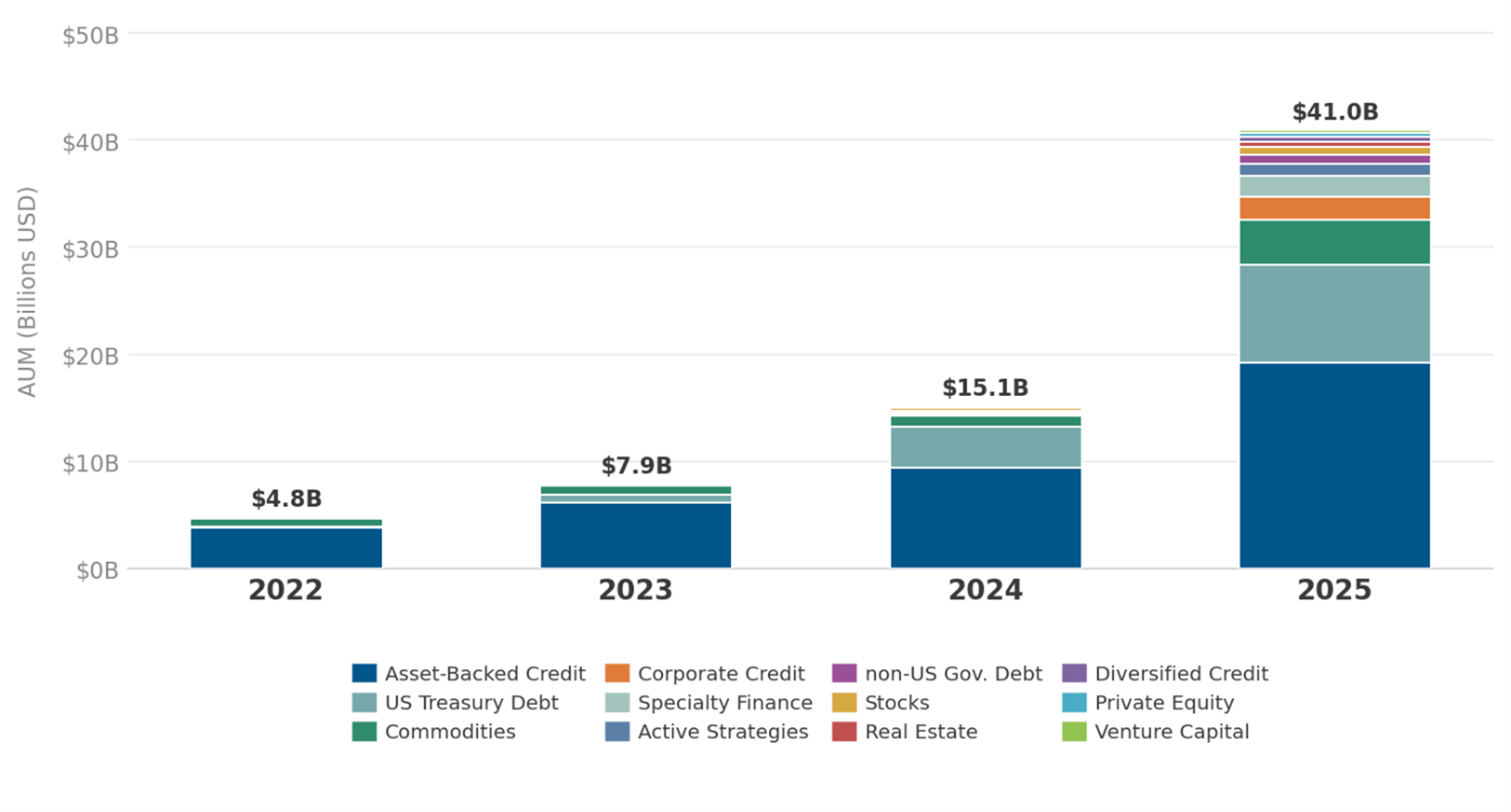

Tokenization is trickier to measure because it depends a lot on what you count in the mix. According to RWA.xyz, a tokenized analytics data platform, tokenized assets have grown from near zero to $415 billion over that same time period. [3] So it might be easy to think that these two worlds are at parity with one another. However, most of this AUM sits on permissioned networks and is not available to the broader investment community. Instead, these assets operate as repurchase agreements on private networks that large institutions use for greater operational efficiency, primarily to settle overnight loans.

When you strip out those figures and isolate what’s broadly available (like most semiliquid funds are now), the numbers drop significantly, but it’s worth noting that they have grown very quickly. In 2022, tokenized assets represented $5 billion, and today that number is over $40 billion. Again, impressive growth, but still nowhere near the size and scale of semi-liquid structures.

Source: RWA.xyz, CAIA Association

In other words, the largest segment of the tokenization market today is not the open, borderless, 24/7 trading vision that most people picture when they hear the word. Rather, it is a set of private institutional platforms where assets move more efficiently — which, if you squint, looks a lot like what semi-liquid funds were trying to do on a different layer.

The Evolving Case and Critiques for Semi-Liquid

“I am scary space monster. You are leaky space blob.”

The bull case for semi-liquid funds is straightforward: they work within a regulatory and operational infrastructure that already exists. The mechanics are understood, the reporting is familiar, and distribution platforms have figured out how to sell them. [4] As I mentioned earlier, the flows have followed, though how durable (leaky?) that adoption turns out to be is an open question.

Defenders of this approach would also argue that semi-liquid structures are the only realistic bridge between where we are and wherever private markets are going next. The wealth management channel, the largest adopters by far, needs products advisors can explain, and clients need structures they can understand. Further, the regulatory environment, while evolving, still provides more legal certainty for a registered fund than for a tokenized fund on a public blockchain.

The tension is that many of these structures have been run in ways that undermine their own design. As I wrote recently in Institutional Investor, most of the fund structures in this ecosystem were built with a discretion lever built in. Managers were supposed to have flexibility over redemption timing. Instead, the industry standardized quarterly windows it was not required to offer. Every time redemption windows have overwhelmed the system, the asset of regular liquidity became a liability. The structure itself was not a problem, but how we use it might be.

The Newer Case and Critiques for Tokenization

“We’re as smart as evolution made us. So, we’re the minimum intelligence needed to ensure we can dominate our planets.”

Despite its size in the open market, the bull case for tokenization should be taken seriously as well. It wasn’t that long ago that the semi-liquid fund market was niche, and look at us now.

The most credible case for tokenization is simply the observed institutional adoption.

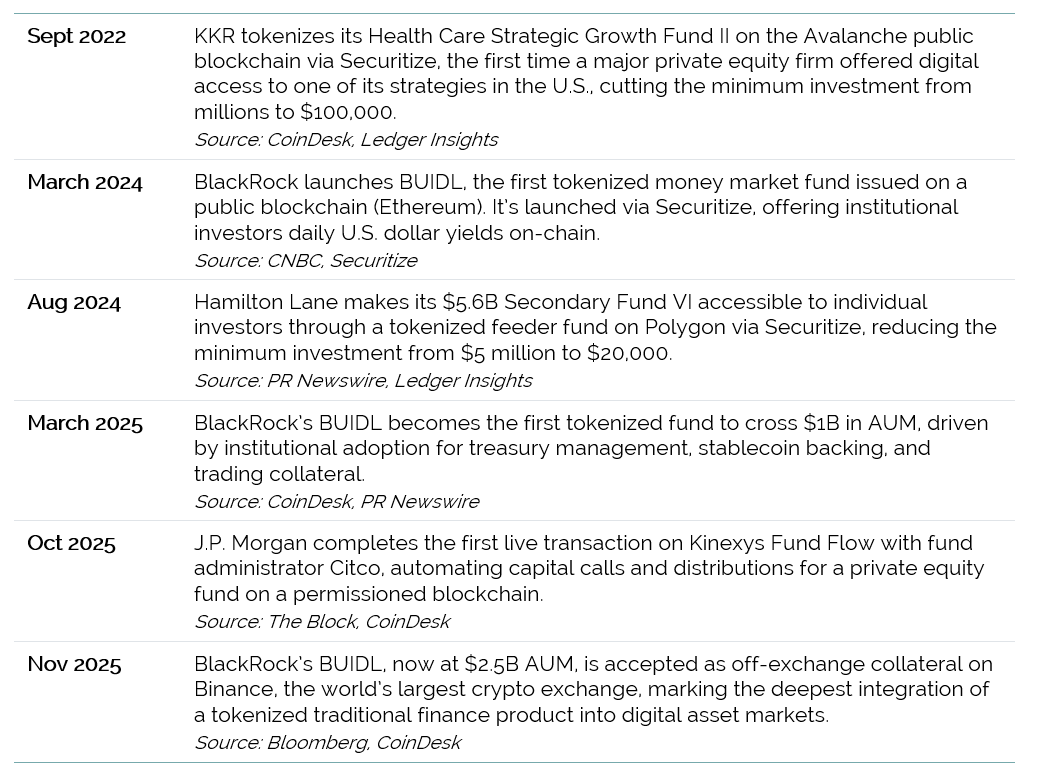

Worth pausing on who these firms actually are: KKR, Hamilton Lane, BlackRock, J.P. Morgan. None of them make speculative bets. Like most large organizations, they move more slowly, deliberately, and under enormous scrutiny. However, they all moved in the same direction within three years.

But let’s look more carefully at what they are using it for:

- Distribution: KKR and Hamilton Lane started at the access layer: can we get more investors into these funds with smaller minimums?

- Efficiency: BlackRock started at the yield and collateral layer: can we give institutional clients a more efficient way to hold short-duration assets and post margin?

- Infrastructure: J.P. Morgan started at the operational layer: can we automate the back office of private fund administration?

Three firms, three different problems, same technology. That pattern of independent convergence is probably the most credible signal in this whole debate.

That said, the current version of tokenization has two real problems that don’t get talked about enough.

- Trustless networks: Blockchain was invented to enable two parties who do not know or trust each other to transact without an intermediary. However, in private markets, you already know your counterparties. Hamilton Lane knows its LPs. KKR ran a full KYC process before anyone could touch its tokenized fund. When verified counterparties, custodians, and legal agreements are already in place, the trustless mechanism is solving a problem that does not really exist, which is why BUIDL still uses Securitize as a transfer agent and BNY Mellon as a custodian. Blockchain has been placed on top of the intermediary stack, not instead of it.

- Interoperability: None of these firms use the same network. KKR is on Avalanche. Hamilton Lane is on Polygon. BlackRock started on Ethereum. J.P. Morgan runs on its own permissioned network. If the promise of tokenization is unified, frictionless market infrastructure, the current reality is a fragmented set of platforms that cannot talk to each other. An allocator with positions across multiple tokenized funds may need separate platforms, wallets, and compliance processes for each. Until that gets sorted out, tokenization risks rebuilding the same siloed market it was supposed to replace, just with different walls.

Where the Two Paths Diverge

“Evolution can be insanely effective when you leave it alone for a few billion years.”

This brings us back to the key question: are both solutions tackling the same problem? I don’t think they are.

Semi-liquid funds are solving an investor access and behavior problem: how do you bring a broader set of investors into private markets while giving them enough flexibility to stay invested? The answer the industry landed on was periodic redemption windows, lower minimums, and familiar tax reporting. The catch is that solving for investor comfort required bending the product design in ways that put the structure under stress during bad times. When the liquidity promise outran the liquidity reality, the product took the blame for a problem that was really about a weak social contract.

Tokenization is solving an infrastructure and transaction problem: how do you make the operational mechanics of private markets faster, cheaper, and more transparent? The answer being built right now is programmable settlement, automated capital calls, and on-chain record-keeping. The risk is that the infrastructure story gets oversold into a liquidity story. Every example in the timeline above confirms that tokenization makes illiquid assets easier to access and administer. Not one of them makes those assets actually liquid.

The two paths are not racing toward the same finish line. One is trying to make investors comfortable enough to stay in illiquid markets. The other is trying to make the markets themselves run better. Those are compatible goals, and understanding the difference is what determines whether you build the right product for the right problem.

Where Are We Going?

“Another day, another staff meeting. Who would have thought saving the world could be so boring?”

I think tokenization eventually wins. But I think it wins on efficiency, not on liquidity.

The analogy I keep coming back to is the ETF. When ETFs showed up, they didn’t make equities more liquid…because equities were already liquid. What they did was make equities cheaper and easier to access, trade, and hold. They separated the trading mechanism from the underlying asset and improved one without pretending to change the other. Further, ETFs didn’t kill the mutual fund. Mutual funds still exist, still manage trillions, still serve a large segment of the market. ETFs just grew up alongside them as a better vehicle for a lot of use cases, and flows have followed accordingly.

If that’s right, tokenization eventually transforms how investors access these strategies, how capital calls get processed, how reporting works, how secondary transactions happen. What it won’t do, and shouldn’t be expected to do, is manufacture liquidity in assets that don’t have it.

Which brings me back to the semi-liquid question. My intuition is that the future does not look like a permanent middle ground between liquid and illiquid. It looks more like the prior world: liquid and illiquid as distinct categories, but with dramatically better infrastructure sitting underneath the illiquid side. Semi-liquid structures, in their current form, may turn out to be a transitional product: a necessary bridge for a period when the technology and regulatory framework needed to support real tokenization were not yet in place.

That does not mean semi-liquid funds disappear. But as tokenization matures, the operational benefits that made semi-liquid structures attractive in the first place (lower minimums, simpler reporting, broader distribution) should become available through tokenized vehicles without the structural tension of trying to make illiquid assets feel liquid.

The place I could be wrong is on semi-liquid’s staying power. ETFs didn’t get rid of mutual funds, but they have eaten into its market share and captured a different kind of investor. The same thing could happen here. If the wealth management channel’s structural constraints (i.e., suitability frameworks, tax reporting, advisor familiarity) turn out to be sticky enough that tokenized products can’t fully replace the registered wrapper, then semi-liquid doesn’t go away. It just becomes its own permanent category serving one segment of the market while tokenization serves another. I think that’s more likely near-term outcome.

The industry isn’t choosing between two solutions, yet. It’s still figuring out what the question is.

“Sometimes, the stuff we all hate ends up being the only way to do things”

Works Cited

[1] PitchBook: Semi-liquid fund AUM growth 2022–2025: https://pitchbook.com/news/reports/q1-2026-us-evergreen-fund-landscape

[2] CAIA Association, The World Rewired: Member Survey on Product Innovation

[3] The Defiant: RWAs Became Wall Street’s Gateway to Crypto in 2025 (RWA.xyz data, on-chain and represented AUM): https://thedefiant.io/news/defi/rwas-became-wall-street-s-gateway-to-crypto-in-2025

[4] Institutional Investor (Aaron Filbeck): We Built Discretion into These Funds. Then We Gave It Away: https://www.institutionalinvestor.com/article/opinion-we-built-discretion-these-funds-then-we-gave-it-away

[5] The Block: JPMorgan executes first fund-servicing transaction on its Kinexys blockchain: https://www.jpmorgan.com/payments/newsroom/kinexys-fund-flow-aum-citco-transaction

[6] CoinDesk / Ledger Insights / Bloomberg: KKR (Avalanche), Hamilton Lane (Securitize), BlackRock BUIDL tokenization coverage: https://www.zoniqx.com/resources/market-trends-shaping-asset-tokenization-in-2025

Photo Credit | iStockphoto: dima_zel