Authored by Georgina Tzanetos, Director of Content

The Paradox – and Pricing – of Capital Flows in a Conflict Zone

Back in February, we underscored the Gulf’s financial firepower, including its ability to underwrite Venezuela’s enormous oil redevelopment. Today that same region is entangled in a conflict with Iran, navigating sustained attacks and a rapid exodus of residents. Against this backdrop, investors must reassess whether the GCC—and our valuation frameworks—are truly ready for the next phase.

Oil prices have surged as tanker disruptions in the Strait of Hormuz threaten global supply on the heels of attacks on Iran and surrounding GCC states. On any given day, approximately 21 million barrels of oil pass through the tiny strait sandwiched by Iran and the United Arab Emirates – roughly 20% of global supply. This 21-mile-wide chokepoint is crucial for investors, but it also affects the families filling their truck in Ohio, the truck driver hauling goods across Europe, and the factory worker in Mumbai whose employer depends on affordable energy. When risk materializes in the Gulf, it cascades far beyond IRR.

Yet as geopolitical tensions simmer across the Middle East—from the Gaza conflict to Iran-Israel hostilities to decentralized cyber warfare operating from Telegram chat rooms—private capital continues flowing into the Gulf Cooperation Council at record pace.

The disconnect has potential to disrupt private markets but is perhaps understated. While ordinary citizens across the world carry latent exposure to Middle East instability every time they buy groceries or fill a gas tank, the professional investors making concentrated bets on the region appear remarkably sanguine about systemic risk.

Deal structures include long lock-up periods with no early exit provisions tied to geopolitical events. Due diligence questionnaires continue to treat “political risk” as a checkbox item rather than a core underwriting criterion. Fund marketing materials lead with Vision 2030 upside while relegating regional instability to brief risk factor disclosures written in passive voice. LP meetings feature presentations on Saudi infrastructure pipelines and UAE fintech opportunities, with geopolitical scenario planning—if discussed at all—confined to the final Q&A slide.

Perhaps most telling: pricing. War risk premiums in GCC markets appear inadequate relative to the tail risk scenarios they face.

The Pricing Problem

Valuation multiples and required returns on GCC deals haven’t meaningfully adjusted despite escalating regional tensions. Given deal volume and a mismatch between pullback and wartime conflict, investors are likely paying 2023 prices for 2026 risk.

Global private equity multiples actually increased from 11.3x EBITDA in 2024 to 11.8x in 20251 – a 4.4% rise – even as Middle East conflicts intensified. Deal activity and capital deployment patterns suggest investors continue underwriting Middle East opportunities at pricing levels that don’t reflect heightened war risk. GCC markets attracted $4.2 billion2 in foreign inflows in Q2 2025, a 50% quarterly increase, while 271 M&A transactions3 closed in H1 2025 – 108 private equity deals4 in 2024 alone, with five exceeding $1 billion.

Large-scale transactions ($500 million to $1 billion) now represent 29% of deals but 42% of capital deployed5, indicating investors are committing larger tickets rather than reducing exposure. This behavioral evidence – accelerating capital flows, increasing deal sizes, and absence of structural geopolitical protections in deal terms – suggests pricing hasn’t adjusted for war-regime risk. In contrast, when the Russia-Ukraine conflict erupted in 2022, secondary market discounts widened 25-35% within weeks and capital withdrew entirely.

This raises an uncomfortable question that extends beyond fiduciary duty into “Is anyone driving this thing?”: Are allocators and general partners amply prepared for what happens when the Gulf’s maturation is tested? Not just to their portfolios—but to the interconnected global systems those portfolios depend on?

The answer, based on current portfolio construction and risk management practices, is troubling, and at this point, unavoidable for both investors and the broader systems that support them. While GPs rush to capitalize on Vision 2030 opportunities and economic diversification narratives, few appear to have stress-tested their portfolios against scenarios that would simultaneously crater their returns and spike energy costs for billions of people worldwide.

Further, technological warfare is accelerating at a pace that perhaps outruns the ability to properly price it. The investment industry might be underprepared for the pricing in of these new and rapidly changing systemic risks.

Regionalization, but Systems-Level Nuance

The Gulf Cooperation Council (GCC) is undergoing one of history’s most ambitious economic transformations. The sovereign wealth funds driving Saudi’s Vision 2030 are attempting to create entirely new capitals—new financial centers, new innovation hubs, and new economic engines independent of hydrocarbon dependency. Saudi Arabia’s entertainment sector, the UAE’s fintech ecosystem, and Qatar’s logistics infrastructure all represent sovereign-scale efforts to fundamentally rewire regional economies.

But it’s important to remember: this is not done in isolation. These transformations and the investments that enable them are very interconnected, and risk exposures are still raw from even last year’s conflicts.

The GCC has revitalized itself so quickly that there is still legacy thinking and tensions embedded within the system. New Dubai Marina towers rise alongside memories of 2014-2016 real estate crashes. Riyadh’s NEOM blueprints compete for capital with debt service from previous mega-projects. The very speed of transformation has left institutional memory fragmented— investors with five-year track records in the region may lack experience of what happens when the system is stressed.

A lot of the activity right now is in the GCC, but connection points exist across the system at large—reminding investors:

Investment in the Gulf is not into an Asset Class or Region, but a System.

Regionalization is happening—but within a deeply interconnected global architecture that we cannot quite yet unmoor ourselves from regardless of the urgency.

The Key Transmission Channels

1. Oil as the Perfect Conduit

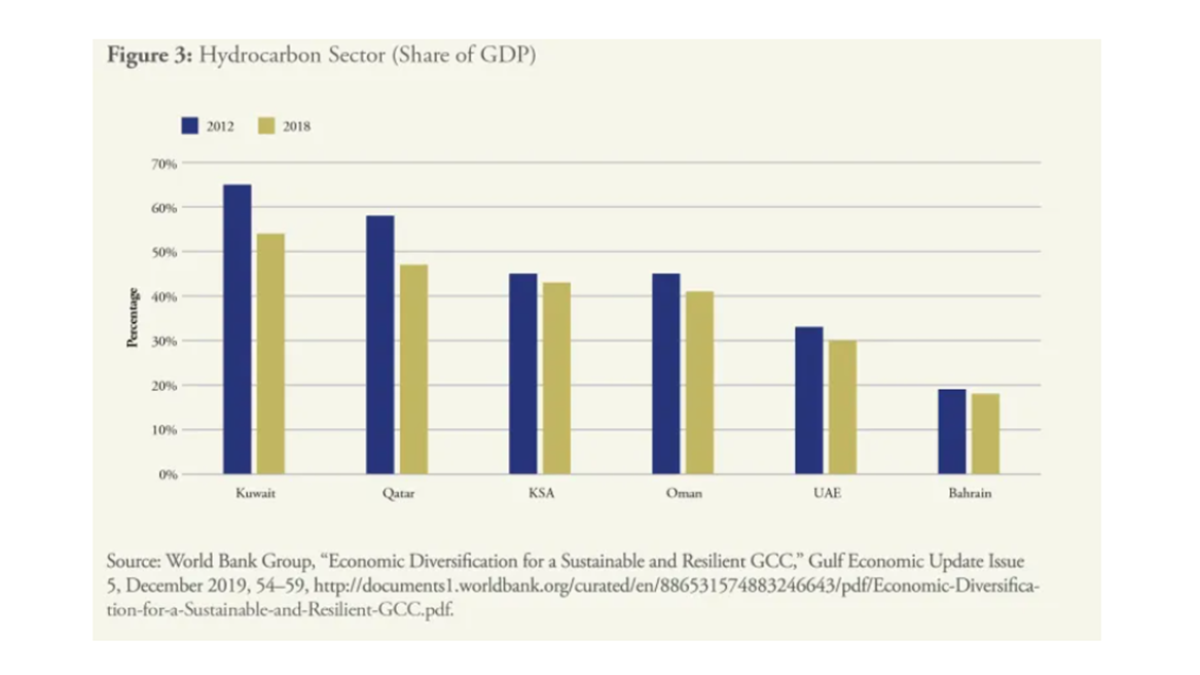

Oil remains the interconnected thread that both compounds regional conflicts yet tethers almost everyone and every investor to common realities. The Gulf is in the process of attempting to disconnect from hydrocarbon dependency, but the current reality is that even after diversification reforms in the region, hydrocarbons still accounted for around 70% or more of government revenues in several Gulf states in 2021 according to the Brookings Institute6, though the share varies by country. Although the Gulf has posted non-oil-related growth in more recent years, the World Bank7 reports hydrocarbons still dominate fiscal positions in the region, maintaining their role as central to economic plans and development strategies.

Source: Brookings Institute

Moreover, Vision 2030 projects are largely financed by oil revenues and “new economy” sectors like tech, tourism, and entertainment are built with old economy capital. GCC infrastructure investments also likely incorporate oil price assumptions in the $70-80/barrel range based on recent historical averages and government fiscal planning, though specific private market underwriting assumptions are not publicly disclosed.

Should oil prices spike to $150+ during conflict (as modeled in stress scenarios), it might seem positive for GCC revenues – but high prices associated with war indeed create fiscal uncertainty and operational disruption that undermines the stability assumptions used to justify crucial infrastructure investments (not to mention the reputation of perceived stability the GCC has worked so hard to maintain).

When governments face war-related fiscal pressures, they delay payments, renegotiate contracts, or redirect capital to defense spending, ironically causing the infrastructure investment financed by oil revenues to underperform precisely when oil prices are highest.

Norway spent 30 years successfully transforming away from oil dependency. The Gulf is attempting it in 10-15 years, and during escalating regional instability. The transformation is real—but incomplete. Portfolio construction must account for this incomplete transition.

The transmission mechanism:

- Strait disruption → oil spike → global inflation → monetary tightening → private market discount rates reprice → portfolio NAVs compress

- Simultaneously: sovereign fiscal stress → government spending cuts → portfolio company contracts delayed → cash flow deterioration → refinancing challenges

The “diversified away from energy” Saudi entertainment company traces back to oil revenue through three steps: company receives government contract → paid by PIF → PIF funded by Aramco dividends → Aramco dependent on $70+ oil and Strait access.

2. The Sovereign Capital Network

GCC sovereign wealth funds now function as a global capital backbone, with more than $3 trillion influencing infrastructure, real estate, and technology markets across North America, Europe, and Asia. Because their capital is embedded through LP commitments, co‑investments, and portfolio‑level commercial ties, a manager with modest direct exposure may still have significant indirect dependence on Gulf sovereign flows. When regional tensions rise, this interconnected network can tighten simultaneously, creating outsized liquidity and exit risk across global private markets.

3. The Banking System Interconnection

Regional banks appear robust—but stress mapping reveals vulnerabilities:

- Deposit bases from oil-economy participants

- Loan books concentrated in real estate and government-linked entities

- Cross-border exposures to each other

- Legacy NPLs from 2014-2016, 2020 crises still on books

Global banks with significant GCC operations (HSBC, Standard Chartered, BNP) create contagion pathways.

The typical cascade: Conflict → Sovereign finances stressed → Government payments delayed → Corporate defaults rise → Bank NPLs increase → Lending tightens → Portfolio companies can’t refinance → Valuations compress → Secondary markets seize.

This scenario happened in 2015-2016. When oil crashed from $100 to $30, the cascade activated as above. The difference between now and then is crucial: 2016 was an oil shock without war, triggered by a supply glut and demand weakness. Recovery took 18-24 months as oil stabilized and governments adjusted.

This time there is a potential oil shock WITH war, meaning longer duration, no clear recovery timeline, and compounding factors the 2016 crisis didn’t have; decentralized cyber warfare, fragmented Iranian command creating unpredictable escalation, and a banking system that hasn’t fully healed from the last stress test.

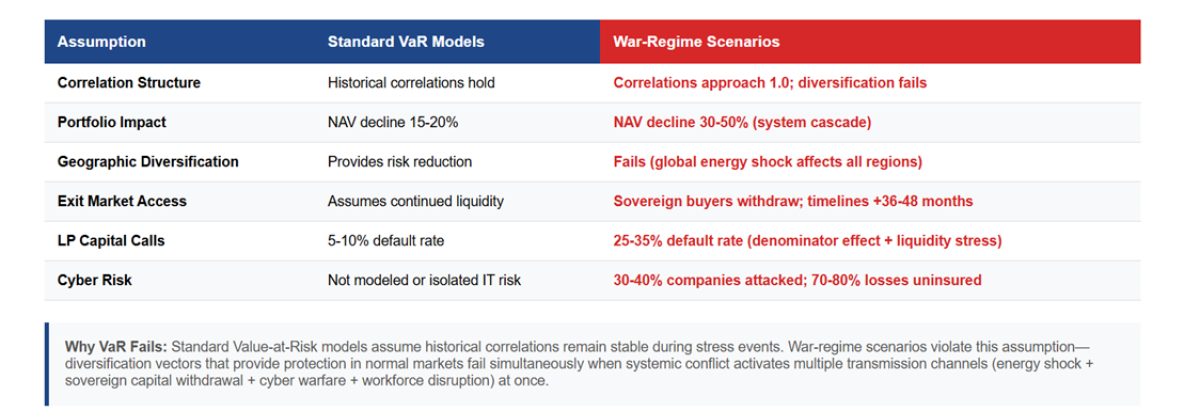

Private‑market investors operating in the GCC can no longer rely on traditional VaR assumptions, as conflict‑driven shocks radically alter correlations, liquidity, and capital‑call dynamics. This framework illustrates how wartime conditions reshape every pillar of portfolio construction—from diversification and exit timelines to cyber exposure and sovereign market behavior. The chart below gives an example of how to recalibrate pricing, underwriting, and liquidity expectations for a region where geopolitical risk is now a core part of the investment equation.

Conclusion

Wartime dynamics in the Gulf are not reflected in today’s valuations, leaving investors exposed to risks that are neither modeled nor priced. The managers best positioned for what lies ahead will be those who treat geopolitics as a core portfolio variable, stress‑test systemwide interconnections, embed a meaningful risk premium into underwriting, and maintain liquidity and exit flexibility even in the absence of sovereign buyers. The opportunity set in GCC private markets is real—transformational, in fact—but returns only matter if portfolios are built to withstand shocks as well as capture upside. That requires acknowledging the region’s structural dependencies, from energy transmission channels to workforce mobility, cyber vulnerability, and the speed with which sovereign capital can reorient. Successful practitioners won’t be betting against the Gulf’s trajectory but will design portfolios that recognize they are investing in both assets and a complex, interconnected system where conflict risk remains materially underpriced.

- McKinsey & Company. (2025, May 20). Global private markets report 2025: Braced for shifting weather. https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report

- Arab News. (2025, July 15). Foreign investors buy $4.2bn GCC stocks in Q2, up 50%: Kamco Invest.

https://www.arabnews.com/node/2608160/business-economyMiddle East Briefing. (2025, September 8). Middle East M&A activity grows in H1 2025. - Middle East Briefing. (2025, September 8). Middle East M&A activity grows in H1 2025.

https://www.middleeastbriefing.com/news/middle-east-ma-activity-grows-in-h1-2025/Middle East Briefing. (2025, September 8). Middle East M&A activity grows in H1 2025.

https://www.middleeastbriefing.com/news/middle-east-ma-activity-grows-in-h1-2025/ - Bain & Company. (2025). Global private equity report 2025. https://www.bain.com/insights/global-private-equity-report-2025/

- McKinsey & Company. (2026). Global private markets report 2026: Clearer view, tougher terrain.

https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report - Kabbani, N., & Ben Mimoune, N. (2021, January 31). Economic diversification in the Gulf: Time to redouble efforts. Brookings Institution. https://www.brookings.edu/articles/economic-diversification-in-the-gulf-time-to-redouble-efforts/

- World Bank. (2025, December 4). GCC economies demonstrate resilience, advance diversification, and accelerate digital transformation. https://www.worldbank.org/en/news/press-release/2025/12/04/gcc-economies-demonstrate-resilience-advance-diversification-and-accelerate-digital-transformation.

Photo Credit | iStockphoto: davincidig