Authored by Georgina Tzanetos, Director of Content

In one of our recent pieces, we established that private credit’s current stress is three separate conversations – redemptions, credit quality, and systemic risk – that media coverage has collapsed into one crisis narrative.

The framing holds, but the looming issue of AI concentration risk warrants its own treatment.

What is happening at the intersection of private credit and artificial intelligence is a structural story about how a decade of concentrated underwriting theses- the SaaS loan as the ideal private credit asset – is being stress-tested simultaneously across an entire market, and where pricing has not yet caught up with reality.

How the Thesis Was Built – and Why It Made Sense

SaaS companies were not a reckless bet. They were, for much of the last decade, arguably the ideal private credit borrower. Predictable recurring revenue, high customer retention, scalable margins, low capital intensity – the favorable characteristics a direct lender should want to underwrite against. The math was clean, the covenant packages were tight (at first), and capital flowed accordingly.

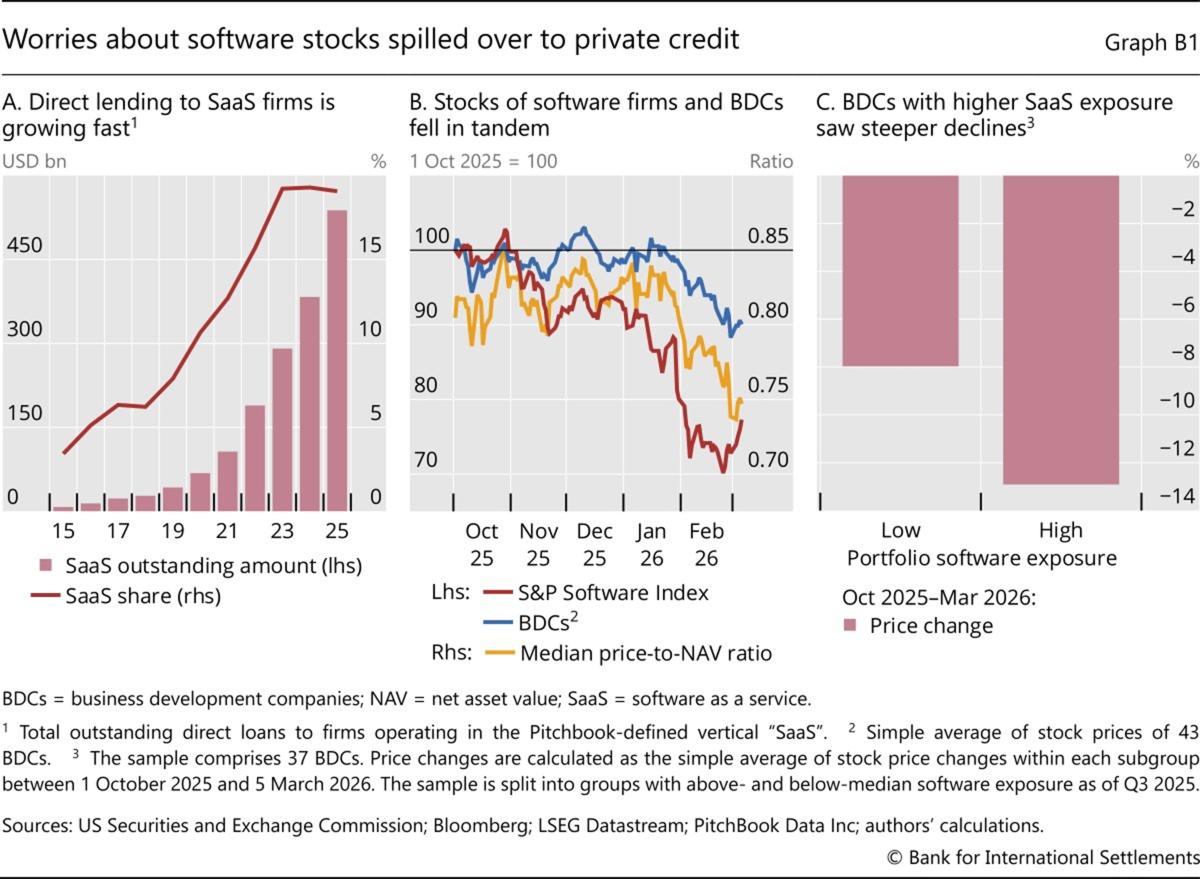

Outstanding loans to SaaS firms grew from approximately $8 billion in 2015 to over $500 billion, representing 19% of total direct loans, by end-20251. By that point, a third of all private credit funds had extended loans to the sector. BDCs – the most transparent segment of the private credit ecosystems by virtue of quarterly SEC disclosure requirements – extended over 15% of their loans to SaaS firms in 2025.

The structural problem is not that the thesis was wrong in 2019. It is that it became so dominant throughout the inflow cycle of 2021-2024 that underwriting discipline eroded in proportion to competitive pressure.

Within the SaaS sector specifically, the deterioration was more acute than the overall private credit markets. As previously stated, outstanding loans to SaaS firms grew from $8 billion in 2015 to over $500 billion – 19% of all direct loans – by end-2025, with a third of all private credit funds carrying SaaS exposure2. As capital flooded in, spread compression accelerated: average spreads on US LBOs financed by direct lending contracted 161 basis points between 2022 and 2024, falling to levels that left lenders with diminishing cushion against deterioration3.

At the same time, covenant packages softened, as competitive pressure from the broadly syndicated loan markets pushed covenant-lite terms into private credit documentation – structure that, in software specifically, was further weakened by ARR-based underwriting rather than traditional EBITDA4, effectively removing the earnings test that would otherwise have served as an early warning mechanism.

The concentration that resulted is structurally difficult to measure. Private credit loans are held at par, borrowers do not publicly disclose earnings, and – critically- at least 250 loans to software firms worth more than $9 billion were classified as other industries by one or more BDCs at the time of disclosure5. Investors looking at sector-level allocations were therefore seeing a number that did not accurately represent their actual SaaS exposure. The consequence of that opacity became visible only after the fact: BDCs with above-median SaaS exposure underperformed those with below-median exposure by approximately five percentage points according to the BIS Quarterly Review.

Valuation Lag and the Disclosure Problem

Private credit’s lack of frequent disclosure is a structural feature of the asset class that does provide some benefits in allowing GPs to strategically think long-term, but the downside is these trends don’t show up in real time. In a disruption scenario these features can create a dangerous lag.

Loans are held at par and borrowers do not publicly disclose their earnings, which means there is no mechanism by which deterioration in a borrower’s business model surfaces in stated valuations until a hard event – a covenant breach, missed payment, or maturity wall – forces recognition. The problem is not that marks are dishonest, but by the time they move, the remediation options available to lenders have already narrowed.

The amendment that would have been straightforward eighteen months earlier now requires a more expensive restructuring, and the refinancing window that existed at origination may have closed entirely.

This dynamic is now interacting with a sector-level disruption whose pace outstrips the normal pace of private credit portfolio monitoring. Software companies’ stocks collapsed by approximately 30% between October 2025 and February 2026, while BDC stock prices fell by approximately 10% on average over the same period. As previously mentioned, BDCs with above median SaaS exposure underperformed those with below-median exposure by approximately five percentage points. NAV discounts deepened during this period- the public BDC index (CWBDC) reached a price-to-NAV discount of approximately 17% in line with the prior low in June 2022 - , signaling market skepticism about stated loan book valuations – but those valuations have yet to move commensurately.

Source: BIS Quarterly Review

The valuation gap is visible in secondary market pricing. Secondary buyers of interests in gated private credit funds are pricing discounts to stated NAV, with the discount widening as each new gate announcement has been made – reflecting the market’s independent assessment that stated marks do not fully capture the probability of future credit deterioration6.

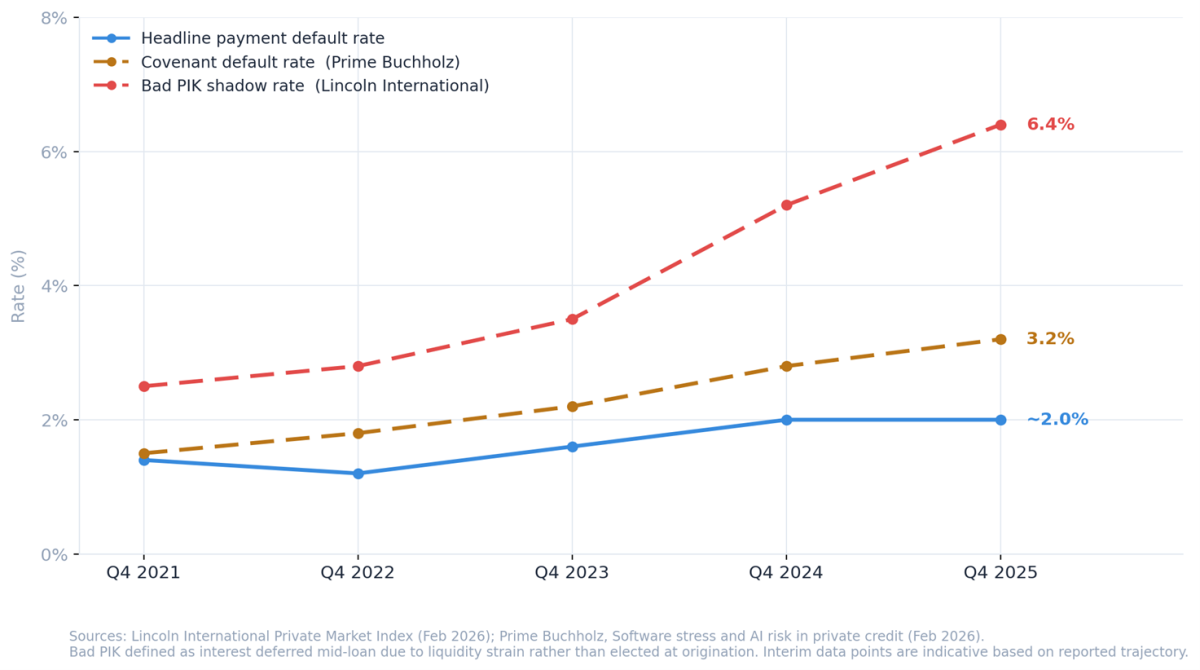

The shadow default indicators are more instructive. The headline payment default rate in private credit sits at around 2% - a figure that captures only outright missed payments.7 As of Q4 2025, 6.4% of loans in Lincoln International’s8 proprietary database carried “bad PIK” – interest deferred mid-loan due to liquidity strain rather than elected at origination – up from 2.5% in Q4 2021. Lincoln treats this figure as a shadow default rate, characterizing it as a proxy for situations in which a default may have occurred absent a PIK election. This implies distress closer to 6% of loans, against the headline payment default rate of approximately 2%9. Covenant defaults, a distinct and earlier-stage stress indicator, reached 3.2% as of September 30, 2025.10 The secondary market is pricing for something closer to the shadow figures, but the stated marks are not.

Sectoral Heterogeneity and the Disclosure Gap

AI disruption risk is not uniformly distributed across the software sector, and – importantly - the current disclosure framework does not allow investors to differentiate meaningfully between exposed and non-exposed segments. Infrastructure software, mission-critical vertical SaaS with deep regulatory or workflow integration, and data-layer companies face materially different displacement risk profiles than horizontal application software – productivity suites, CRM platforms, document automation tools, project management software – where AI disruption risk is highest and switching costs are lowest.

No major fund currently discloses the composition of its software exposure at this level of granularity. Software appears as a category total, typically 20-35% of AUM at the funds most active in 2022-2024 direct lending. The AI displacement risk metric does not exist as a disclosed portfolio category.

This absence is operationally significant: when LPs cannot quantify their exposure to a specific risk factor and that factor is material and uncertain in its timelines, the rational institutional response – especially for those operating under risk mandates – is to reduce the allocation. The observed correlation between redemption queue volumes and the absence of subcategory disclosure is not coincidental.

Morgan Stanley estimates software exposure among direct lenders at around 26%11 based on BDC holdings, and at 19% based on private credit CLO holdings. S&P Global puts software and technology at about 25% of the private credit market through year-end 2025. These aggregate figures mask the differentiation that matters analytically.

Differentiated Exposure by Manager

The practical consequence of this lack of subcategory disclosure is that LP-level risk assessment depends heavily on manager-specific diligence rather than industry-level data. What limited information is available – drawn from BDC quarterly filings, dividend announcements, and redemption disclosures – suggests significant dispersion in actual exposure quality across different managers.

Apollo planned to reduce its software allocation from approximately 20% to roughly 10% during 202512, a deliberate de-risking move made in advance of the broader deterioration in software sentiment. Golub Capital, with approximately 26% of its portfolio invested in software cut its dividend by 15%, with analysts forecasting further reductions of 10-20%. Blackstone’s BCRED posted its first monthly loss in three years in February 2026, driven in part by meltdowns on SaaS loans including debt linked to Medallia. Blue Owl’s technology-focused vehicles saw redemption requests representing 40.7% of shares – driven largely by sector sentiment rather than credit deterioration, as non-accruals within the portfolio stood at 0.6%.

The divergence between Blue Owl’s stated credit quality and its redemption pressure illustrates the core analytical problem: in the absence of subcategory disclosure, investors are unable to distinguish between funds with material horizontal SaaS concentration at actual disruption risk and those with more defensible portfolios. The result is sector-level sentiment driving fund-level redemption behavior, regardless of underlying credit quality.

Default Rate Trajectory and Maturity Wall

Morgan Stanley’s credit strategy team has projected that direct lending default rates, currently running at approximately 5.6%, could reach 8% - approaching COVID-era peak levels - as AI disruption compounds existing leverage pressure in software and related sectors. The firm’s analysts characterized an 8% default spike as “significant but not systemic”, citing lower leverage ratios at private credit funds and BDCs relative to 2008 bank balance sheets.

The maturity wall constrains the timeline available for orderly resolution. As of early 2026, 23 out of 32 rated BDCs have unsecured debt maturing in 2026, totaling $12.7 billion – a 73% increase over the prior year13. The risk is not uniform across all 23 BDCs, but the concentration of maturities in 2026 still constrains the timeline for orderly resolution across the sector, especially for those with higher SaaS exposure.

Loans originated at peak valuations in 2021–2022, when SaaS companies traded at multiples approaching 60 times earnings, will face refinancing decisions in a market where comparable companies now transact at average multiples of approximately 18 times14. The gap between origination valuation and current enterprise value will be forced into view at maturity events, regardless of how stated NAV has evolved in the interim.

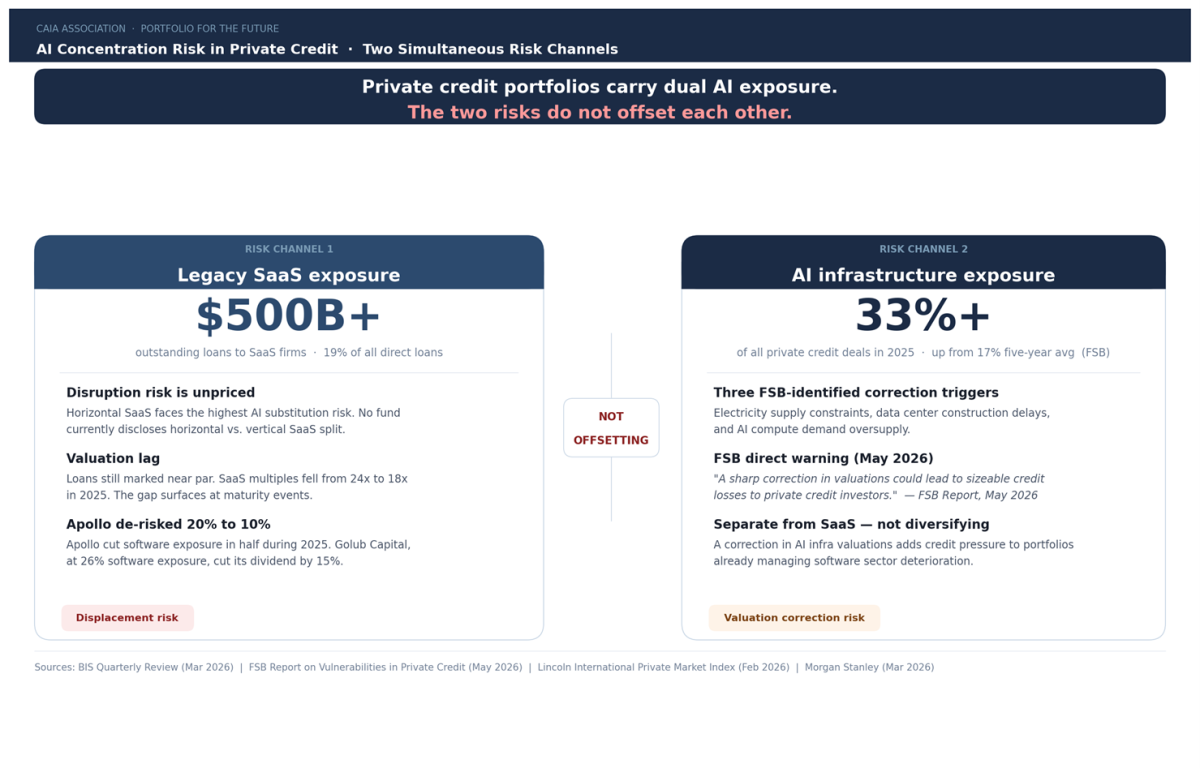

The AI Infrastructure Concentration: A Separate Risk Channel

The concentration risk in private credit is not confined to legacy SaaS lending. A second and distinct exposure has accumulated in AI infrastructure financing – data centers, GPU compute capacity, and model infrastructure. The Financial Stability Board, in its May 2026 report on private credit vulnerabilities, noted that AI accounted for more than a third of private credit deals in 2025, up from 17% over the prior five years. The FSB warned explicitly that a sharp correction in AI asset valuations – exposed to electricity supply constraints, data center construction delays, and the possibility of AI compute oversupply – could produce sizeable credit losses for private credit investors.

This creates a structural asymmetry in portfolio risk. Private credit managers face simultaneous exposure to companies disrupted by AI adoption — legacy SaaS borrowers — and to the infrastructure buildout enabling that disruption. These two exposures are not offsetting. A correction in AI infrastructure valuations would add credit pressure to portfolios already managing software sector deterioration, without providing a diversification benefit.

The FSB's broader vulnerability assessment flags concentration in technology, healthcare, and services alongside opaque multi-layered leverage structures and data gaps that impede effective regulatory oversight of exposures and transmission channels. At the fund level, the chain of capital — from institutional or retail investor through wrapper vehicle through fund to borrower — insulates the ultimate risk bearer from information about the risk it carries. This structural information asymmetry applies most acutely to the insurance channel: PE firms have, over the prior seven years, acquired life insurance and annuity businesses and redirected policyholder reserves into proprietary private credit funds operating with limited disclosure and infrequent marks, with significant concentration in mid-market software borrowers during the peak valuation period.

Portfolio Construction Hurdles and Manager Selection

The immediate analytical requirement is disclosure and granularity that the current framework does not provide. Aggregate software exposure as a percentage of AUM is not enough for LPs to assess AI displacement risk. Meaningful evaluation requires transparency of this subcategory – horizontal versus vertical SaaS, application versus infrastructure, covenant-lite versus covenant-heavy documentations – alongside vintage disclosure that allows assessment of which loan cohorts were originated at the most vulnerable valuation multiples. What this ultimately demands is more rigorous GP underwriting on the part of the LPs. Disclosure in private markets is limited and unlikely to improve materially outside of regulated vehicles – but the investment due diligence process is where these questions must be asked. GPs may be considerably less diversified across SaaS sub-segments than their sector-level allocations suggest, and that assumption should not be granted without a certain level of scrutiny.

In the interim, manager selection criteria should weight demonstrated underwriting discipline during the 2021-2024 inflow cycle- specifically, the degree to which managers maintained covenant protections and leverage discipline when competitive pressure ran against doing so- alongside restructuring capability and borrower relationship depth that allow for proactive covenant renegotiation ahead of maturity.

The funds best positioned to manage through the maturity wall are those that built structural protections into loan documentation when doing so was commercially harder, and that have the operational infrastructure to work through distress on a loan-by-loan basis rather than relying on market conditions for exit.

The credit stress accumulating in direct lending SaaS portfolios is real, sector-specific, and not yet fully reflected in stated valuations. It is also not uniform across managers or across the SaaS universe. The analytical work required — and the disclosure framework that would support it — is not yet in place, but at the very least, the warning signs are there.

- https://www.bis.org/publ/qtrpdf/r_qt2603v.htm

- Avalos, F., Doerr, S., & Todorov, K. (2026, March). Private credit's software lending meets AI disruption. BIS Quarterly Review. https://www.bis.org/publ/qtrpdf/r_qt2603v.htm

- PitchBook LCD. (2024, November). Q4 Global Private Credit Survey. PitchBook. https://pitchbook.com/news/articles/q4-global-private-credit-survey-spreads-expected-to-tighten-in-chase-for-assets

- PitchBook. (2026, February 27). For private credit, software connection, see pandemic era. https://pitchbook.com/news/articles/private-credit-101-for-private-credit-software-connection-see-pandemic-era

- Bloomberg News. (2026, February). Private credit: AI disruption may trigger a singularity in software debt. Bloomberg. https://www.bloomberg.com/opinion/articles/2026-02-18/private-credit-ai-disruption-may-trigger-a-singularity-in-software-debt (https://www.privatedebtnews.org/p/private-credit-news-weekly-issue-a7f)

- A sector under pressure: How AI-exposed software loans are reshaping private credit. (2026, April 30). The NYC Times. https://www.thenyctimes.com/ai-exposed-software-loans-reshaping-private-credit/

- Proskauer / J.P. Morgan Global Alternative Investment Solutions. (2026, April). Private credit still earns its place in portfolios. https://privatebank.jpmorgan.com/nam/en/insights/markets-and-investing/ideas-and-insights/private-credit-still-earns-its-place-in-portfolios-with-the-right-approach

- Lincoln International. (2026, February 11). The Lincoln Private Market Index ends the year with its slowest quarter of growth in 2025. https://www.lincolninternational.com/news/the-lincoln-private-market-index-ends-the-year-with-its-slowest-quarter-of-growth-in-2025/

- Lincoln International. (2026, February 11). The Lincoln Private Market Index ends the year with its slowest quarter of growth in 2025. https://www.lincolninternational.com/news/the-lincoln-private-market-index-ends-the-year-with-its-slowest-quarter-of-growth-in-2025/

- Prime Buchholz. (2026, February 24). Software stress & AI risk in private credit. https://www.primebuchholz.com/2026/02/24/software-stress-ai-risk-in-private-credit/

- Fontevecchia, A. (2026, March 25). Private credit's 'zero-loss fantasy' is coming to an end as defaults and fund exits rise. CNBC. https://www.cnbc.com/2026/03/25/private-credit-defaults-loan-quality-debt-risk-systemic-ai-disruption.html

- https://www.ft.com/content/137bfe82-3e52-418b-9d4f-930978b2532e?syn-25a6b1a6=1

- Fitch Ratings. (2026, February 5). Recent US BDC debt issuance lowers refinancing risk of 2026 maturities. https://www.fitchratings.com/research/corporate-finance/recent-us-bdc-debt-issuance-lowers-refinancing-risk-of-2026-maturities-05-02-2026

BIS Quarterly Review