By Georgina Tzanetos, Director, Content, CAIA Association

The headlines have been breathless. The $2.02 trillion private credit market, we are told, is in freefall, and depending on which outlet you read, we are either on the precipice of systemic collapse or watching the first act of a slow-motion replay of 2008.

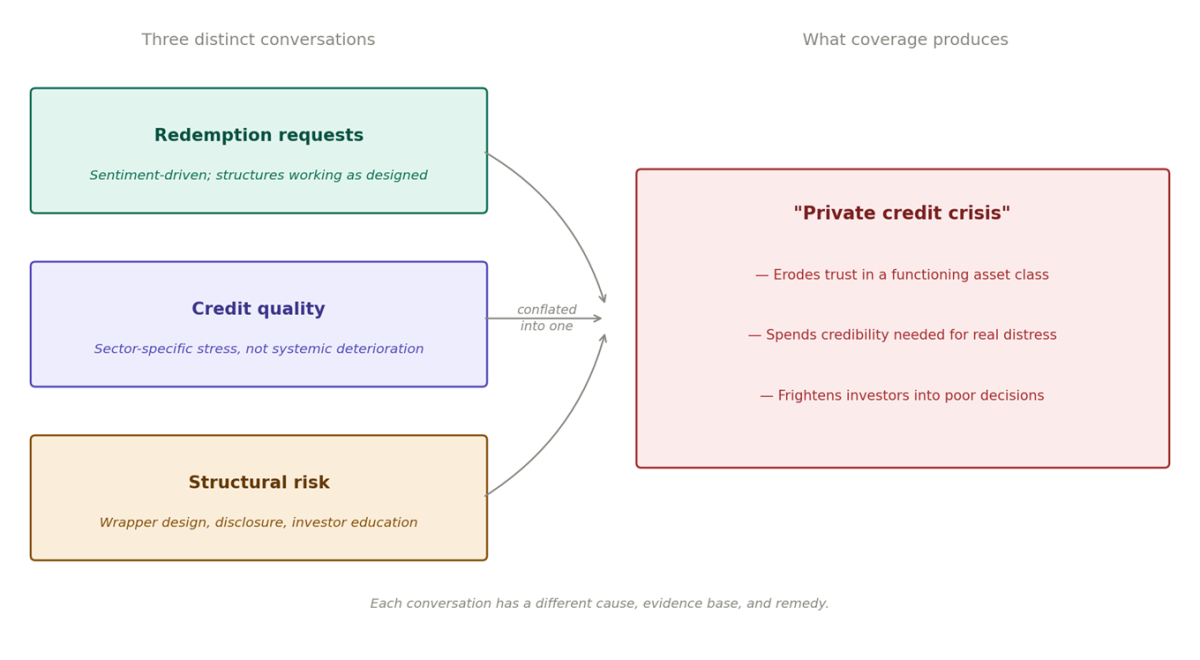

Neither is entirely true, and the gap between what the data shows and what the coverages suggests is worth examining – not to dismiss legitimate concerns, but because conflating three separate and distinct conversations (redemptions, defaults, and structural issues) into one crisis narrative has potential to do real damage.

Three conversations. One misleading narrative.

Conflating redemption requests, credit quality, and structural risk into a single crisis story does real damage to market understanding.

It erodes trust in an asset class that, by most credible measures, is doing what it was designed to do. And it spends the analytical credibility the industry will need when a real problem eventually arrives.

So, let’s separate the arguments.

What’s Actually Happening with Redemptions

Retail investors in non-traded BDCs and semi-liquid vehicles are redeeming at rates that are triggering quarterly caps. Gates have gone up, capital has been locked, and the coverage has treated this as “evidence” of a collapsing asset class. It is worth pausing on the language here. Actual redemptions – capital returned to investors – are fixed and capped at 5% of NAV by design. What is surging is redemption requests: the volume of investors seeking to exit. The distinction is important. A spike in redemption requests is a signal of investor sentiment. It is not, on its own, evidence of credit deterioration, and treating it as such conflates two very different problems.

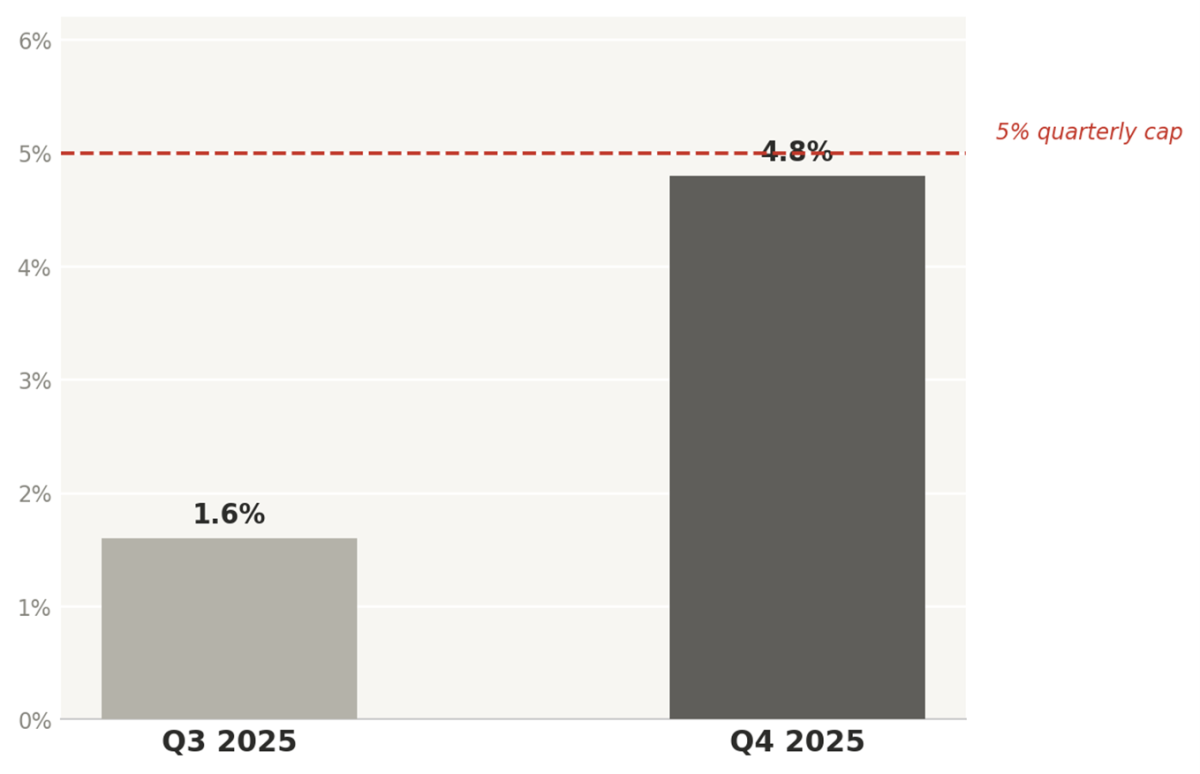

In Q4 2025, average redemptions for the perpetually non-traded BDCs rose to 4.8%1 of NAV, up from 1.6% in Q3 2025, with five BDCs funding tenders above the standard 5% quarterly cap. Headlines took off, and what ensued can only be likened to hysteria.

What is driving those requests, Fitch argues, is sentiment rather than credit deterioration, with concern largely stemming from investor concerns about AI disruption risk for software companies. This has led to elevated redemption requests and slower inflows, alarming from a narrative perspective, but not yet broad-based judgment on private credit portfolio quality.

The structures, it should be noted, are doing precisely what they were designed to do. The quarterly cap is not a gate imposed in a moment of crisis. These gates are there from the beginning as a function of the product. It exists to protect the integrity of the loan book, the underwriting discipline, and the return profile for investors who remain. A manager honoring the 5% cap is not a story, but a massive oversubscription to redemption requests, however, is. This is not because the assets are necessarily failing, but because it reveals the elephant in the room: was the long-term nature of these vehicles properly understood by the investors who bought them to begin with?

Liquidity and asset coverage cushions are sufficient to absorb a spike of elevated redemptions. Sustained tenders above 5% could pressure credit profiles, but that is not Fitch’s base case. The average debt-to-equity ratio for the seven rate perpetually non-traded BDCs stood at 0.71x, compared with 1.13x2 from the other 25 rated BDCs, and asset coverage cushions averaged 38.6% - well above the 22% average for Fitch-rated public and private BDCs. These are hardly the balance sheet metrics of a sector in crisis.

Fitch even identifies a structural silver lining: if fundraising stays weak, the competitive pressure that has compressed spreads and weighed on BDC earnings in recent years could ease – which is more akin to a rebalancing than a crisis.

For these perpetually non-traded BDCs, Moody’s3 noted that inflows shifted to the first-ever outflow in Q1 2026 and that publicly traded BDCs have maximized leverage, leaving less room for error.

A significant underlying contributor to this “mess” is the concentration of software in BDC portfolios. Moody’s found it represents roughly 25% of BDC portfolios on a median basis and flagged AI as a developing credit risk, but their own language offers a welcome balance: “Asset quality metrics have so far remained largely benign, and software loan maturities do not increase more meaningfully until 2028-2029, suggesting AI risk will be a sentiment and monitoring issue in the near term rather than an immediate ratings driver.”

Non-traded BDC redemptions surge in Q4 2025

Redemptions as % of NAV

Source: Cliffwater; Robert A. Stanger & Co. Five BDCs funded tenders above the standard 5% quarterly cap in Q4 2025.

How did private credit get so deep into software?

SaaS has long been one of private credit’s darlings. Outstanding loans to SaaS firms increased from almost $8 billion4 in 2015 to over $500 billion, or 19% of total direct loans, by end-2025. By that point, a third of private credit funds had extended loans to the Saas sector. The logic was pretty straightforward, and at the time, sound: SaaS companies offered exactly what private credit lenders want - predictable recurring revenue, sticky customer bases, high margins, and scalability. Direct lenders captured 34% of large LBO financing in 2022, rising to a record 54% in 2023, according to PitchBook LCD5 – a sharp reversal from the pre-pandemic period when roughly 80% of buyouts were financed through the syndicated loan markets, with software dominant throughout.

Enter AI.

The proximate trigger to the redemption request waterfall was Anthropic’s unveiling of new agentic AI tools designed to perform complex professional tasks that many SaaS companies currently charge for, sparking a sell-off in software data provider shares and raising fresh concerns that AI could weaken traditional SaaS business models.6

Within weeks of those AI product launches, investors sought to pull over $10 billion from private credit funds driven by fears of over-exposure to software companies perceived as vulnerable.

The deeper problem is not the software exposure itself but the opacity that surrounds it – private credit loans are held at par, and borrowers don’t publicly disclose earnings. Deteriorations in a borrower’s business model may not surface in stated valuations until a covenant breach or maturity event forces it- and by then, the options have narrowed considerably.

The stress indicators that do exist are worth examining carefully. As of Q4 2025, 6.4% of private credit loans carried “bad PIK” – interest deferred mid-loan due to liquidity strain rather than structured in at origination – nearly triple 2021 levels. Lincoln International7 treats this as a shadow default rate, putting implied distress closer to 6% against a headline rate of around 2%. Meanwhile, approximately 70% of private credit issuance is not covenant-lite, meaning the early warning systems that once flagged borrower stress before a missed payment are largely gone. The result is a market where investors know the loans haven’t been marked down, don’t know whether they should have been, and in the absence of transparency, the rational move for a retail investor with a quarterly redemption window is to leave before the answer becomes clear.

Blue Owl: A Headline Casualty with Others in Tow

Blue Owl became the most visible casualty of the redemption request wave when investors sought to withdraw 40.7%8 of shares from its technology-focused vehicles and 21.9% from its credit income funds. These requests were largely driven by sentiment and software sector fear, not by any meaningful deterioration in the underlying loan portfolios, which had actually delivered returns in line with the Cliffwater Direct Lending Index since inception with non-accruals at just .6%. The company attempted to resolve the liquidity mismatch by merging OBDC II into its publicly traded BDC at terms that would have imposed a roughly 20% haircut on investors due to OBDC’s discount to NAV triggering a class action lawsuit (and media drama) alleging the firm had repeatedly told investors there was no “meaningful pressure” on redemptions while withdrawals were accelerating.

The timing proved deeply unlucky: the merger was terminated, redemption mechanics were restructured to eliminate quarterly tender offers entirely, and Moody’s revised its outlook to negative- while simultaneously noting that asset quality remained solid, confirming that what failed was the wrapper and the disclosure, not the credit itself.

Investors were not redeeming because the assets were falling, but because they were frightened – by the same negative coverage now citing their redemption requests as proof of crisis – and because “semi-liquid” had been sold to them as something meaningfully more accessible than the quarterly cap mechanics permit.

Which raises a harder question.

Investor psychology does not exist in a vacuum. It is a product of conversations between investors and the layers of agents who serve them – GPs, advisors, intermediaries – and what those conversations did or did not adequately convey. When redemption requests massively oversubscribe a 5% quarterly cap in a vehicle designed for long-term illiquidity, it is worth asking whether the vehicle’s fundamental nature was mis-sold, misunderstood, or simple ignored as animal spirits took over.

It even challenges whether our language is adequate. “Semi-liquid” implies a degree of accessibility that the mechanics may not support. And more fundamentally: are structures that tease periodic withdrawal capability from inherently illiquid assets feasible at the scale the industry has pursued? Retail investors deserve access to private market premia- this is where the bulk of capital formation and new economy innovation is happening, and excluding them from that entirely is its own problem. But until the messaging, the structures, and the investor education are genuinely fit for purpose, it is difficult to argue that these products are serving investors or the broader system well. The industry may need to go back to the drawing board on wrapper design before it earns the right to expand further into the retail channel.

This is a distribution problem, an education problem, and a wrapper problem, but a credit problem it is not – yet.

What’s Actually Happening With Credit Quality

Credit quality is a separate conversation, and it deserves honest treatment on its own terms. There are meaningful pockets of stress. Software and tech exposure – estimates are around 26% of direct lending portfolios - is under pressure as AI disruption raises real questions about SaaS business models underwritten for a world of predictable recurring revenue.

Highly leveraged healthcare roll-ups and smaller middle-market borrowers, priced for an era of cheap money, are showing strain. Covenant-lite structures that became standard during the inflow frenzy of 2021-2024 are offering less protection than lenders assumed.

Morgan Stanley9 has warned that direct lending default rates (currently running at around 5.6%) could reach 8% - well above the 2-2.5% historical average. That is worth watching. But Morgan Stanley’s own analysts called an 8% spike “significant but not systemic.” KBRA’s10 rated BDC universe showed no rating changes or negative outlook revisions thought Q3 2025, though selective downgrades followed in Q4. The stress is real and concentrated, but it’s also sector-specific. It is not broad-based deterioration across a $2 trillion market.

That distinction matters enormously. Concentrated credit stress in software and leveraged healthcare is a manager selection and underwriting discipline problem. It is not a private credit problem.

While AI disruption risk is real, it does not apply to all of private loans any more than it would in any other sector. That said, it certainly does operate in a system that is interrelated.

What’s Actually Happening With Systemic Risk

The GFC comparison seems to be invoked every time a complex financial structure shows stress.

It is almost always wrong, and it seems to be misleading here as well – but not for the reasons the industry’s defenders usually cite. Investors, understandably, are primed to recall the worst episodes and the pain associated with them, and such narratives exploit that reflex.

Private credit is structurally different from 2008. There are no depositors to run, no repo lines to pull, no overnight funding markets to freeze. The feedback loop that made subprime systemic – mortgage losses embedded in bank balance sheets backstopped by government-insured deposits – does not exist in the same form.

But that does not mean systemic risk is zero. The contagion channels are different, but they are still present. Mark-to-model valuation means deterioration builds invisibly until it doesn’t. Insurance company entanglement (a growing share of private credit is now funded through insurance vehicles) means losses could ultimately sit against the retirement savings of policyholders with no awareness of their exposure. These are real risks. They are just not exactly 2008 risks.

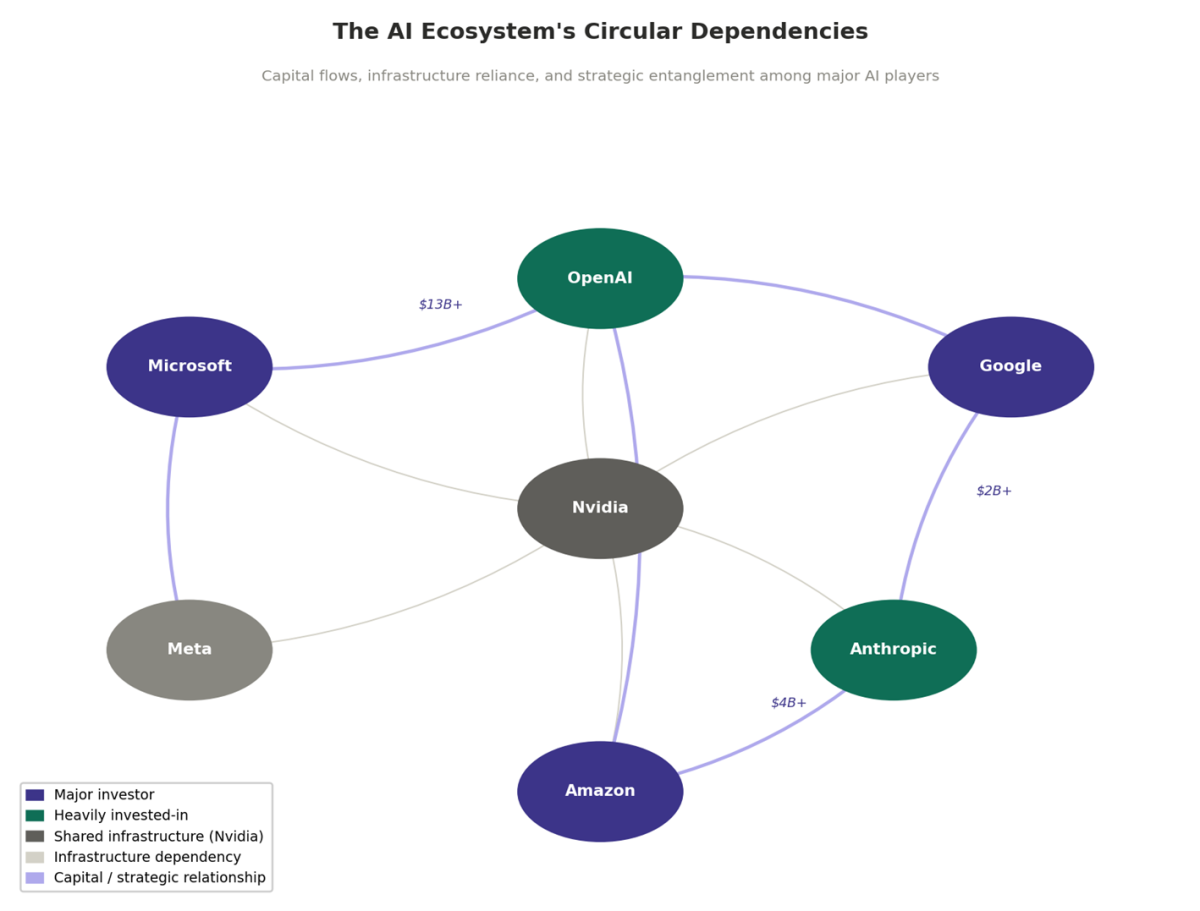

That said, there is a wrinkle that has received very little attention: the AI ecosystem disrupting SaaS is itself built on circular dependencies that should feel familiar to anyone who studied the pre-2008 financial system. Microsoft is embedded in OpenAI. Google and Amazon are in Anthropic. Nvidia underpins virtually every model in production. Map the relationships and you get something that looks less like a competitive technology sector and more like a single organism with multiple faces – which is precisely what counterparty exposure diagrams looked like in 2007, right before the question shifted from “who has the risk” to “who doesn’t”. If one significant node stumbles, the private credit portfolios exposed to SaaS companies whose revenue depends on that ecosystem sitting intact would feel it. The diversification many investors believe they have may be more theoretical than real. Again, the goal is to inform rather than cause a new version of hysteria, but it’s also important to learn from the past rather than repeat the same mistakes.

The AI Ecosystem's Circular Dependencies

Capital flows, infrastructure reliance, and strategic entanglement among major AI players.

Note: Arrow thickness indicates relative capital or strategic significance. Infrastructure dependencies reflect GPU/compute reliance on Nvidia across all major AI developers.

Why The Conflation Is Itself the Problem

Redemptions requests do not directly cause defaults. A company does not fail on its loan because retail investors in a non-traded BDC wanted liquidity.

The ecosystem is connected. Persistent outflows tighten lending conditions at the margins > companies that have to rely on private credit for financing feel that tightening over time. But the chain of causation is long and indirect rather than immediate.

The media narrative has compressed that chain into a single alarming story, and that compression has consequences. When every instance of a redemption gate becomes a systemic crisis, and every gated fund becomes evidence of a collapsing asset class, the coverage loses its ability to signal true distress when it actually occurs.

Private credit might not be in a crisis, but it would be fair to say recalibration – one that involves real stress in specific sectors, real structural questions about semi-liquid wrapper design, and real risks that deserve rigorous oversight and honest analysis. What it does not deserve is the kind of breathless conflation that makes it impossible to tell the difference between a wrapper problem, a sector problem, and a systemic one.

The distinction is analytically important but also marks the difference between informed markets and frightened ones.

This connects to the broader shifts we’re tracking in CAIA's latest report: The World Rewired Report—watch this video for a closer look at the key ideas and how it all came together.

Cliffwater (4.8% figure): https://icapital.com/insights/investment-market-strategy/bdc-redemptions-looking-beyond-the-gates/(iCapital piece citing Cliffwater's index data directly)

Robert A. Stanger & Co. (4.6% figure): https://www.wealthmanagement.com/alternative-investments/private-placement-bdcs-met-three-fourths-of-redemption-requests-in-first-quarter

- Fitch Ratings. "Perpetually Non-Traded US BDCs See Higher Redemptions, Slower Fundraising." February 17, 2026. https://www.fitchratings.com/research/corporate-finance/perpetually-non-traded-bdcs-see-higher-redemptions-slower-fundraising-17-02-2026

- Moody's Ratings. "BDC Sector Outlook Revised to Negative." April 7, 2026. Reported by Reuters: https://www.investing.com/news/stock-market-news/moodys-cuts-outlook-on-us-bdcs-to-negative-on-redemption-pressure-rising-leverage-4600566.

- Bank for International Settlements. "Private credit's software lending meets AI disruption." BIS Quarterly Review, March 16, 2026. https://www.bis.org/publ/qtrpdf/r_qt2603v.htm

- PitchBook LCD. "Private credit steps up competition with BSL market for large buyout funding." June 12, 2025. https://pitchbook.com/news/articles/private-credit-steps-up-competition-with-bsl-market-for-large-buyout-funding. Note: figures reflect large LBO financing (deals of $1 billion or more). Across all deal sizes, PitchBook LCD tracked 84% of 2024 leveraged buyouts funded via private credit, up from 65% in 2021.

- https://www.cnbc.com/2026/02/09/private-credit-software-firms-fall-ai-fears.html

- Lincoln International, Q4 2025 private credit valuation data, as cited in Omnigence Asset Management, February 25, 2026: https://omnigenceam.com/insights/are-the-private-credit-markets-under-stress-pik-usage-covenant-erosion-may-tell-the-tale. Shadow default rate methodology per TCW, "The Big PIK-ture," August 18, 2025: https://www.tcw.com/Insights/2025/2025-08-18-The-Big-PIK-ture. KBRA headline rate per KBRA Q3 2025 Middle Market Borrower Surveillance Compendium: https://www.kbra.com/publications/nDFtjDwL.

- Blue Owl Capital shareholder letters, Q1 2026, as reported by Bloomberg, April 2, 2026: https://www.bloomberg.com/news/articles/2026-04-02/blue-owl-bdcs-impose-caps-after-facing-41-22-requests-to-exit. Corroborated by CNBC, April 2, 2026: https://www.cnbc.com/2026/04/02/blue-owl-private-credit-funds-redemptions-requests.html. Note: figures reflect Q1 2026 (three months ended March 31, 2026). Both funds capped redemptions at the standard 5% quarterly limit.

- Morgan Stanley, research note by strategist Joyce Jiang, March 16, 2026, as reported by Bloomberg: https://www.bloomberg.com/news/articles/2026-03-16/private-credit-default-rates-to-reach-8-morgan-stanley-says. See also CNBC, "A 'significant' private credit shakeout on par with Covid losses is coming, predicts Morgan Stanley," March 17, 2026

- KBRA. "Private Credit: Business Development Company (BDC) Ratings Compendium: Third-Quarter 2025 and 2026 Outlook." December 5, 2025. https://www.kbra.com/publications/tmPgxxsR.

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/