By Charles Skorina In our last letter we took a hard look at recent investment performance among the eight Ivy League endowments. [See NL44 at http://www.charlesskorina.com/775/] As a bonus we added four "Alt-Ivys" to round it up to an even dozen. These are all, of course, privately-funded institutions. Now, we turn to the cream of our state-supported schools, the twelve Public Ivys. The traditional Private Ivy endowments, including Harvard and Yale, get lots of scrutiny for obvious reasons. They control a lot of money; they're regarded as leaders in the art and science of investing; they have lots of Big Foot alumni; and they're located in the media-saturated Northeast corridor. Endowments at the big state schools, many of which are tucked away in flyover country, draw much less media attention. So, we would like to provide some, welcome or not.

A list of "Public Ivys" was composed by Richard Moll in 1985, and expanded by Howard and Matthew Greene in 2001. Dr. Moll was a Princeton man and, as he visited schools around the country 30 years ago, he was especially charmed when he encountered traditional neoclassical architecture on the historic flagship campuses of our older public colleges. Today, of course, these schools have expanded into multi-campus behemoths, but we will generously apply the Public Ivy tag to the complete university systems. Admissions offices at these schools, as one might expect, were very receptive to the Public Ivy phrase, and the term stuck. We ranked these schools by endowment size; then cut the list down to a manageable twelve to correspond to our original dozen Private Ivys. This omitted some worthy runners-up (with slightly smaller endowments); so, apologies to Michigan State, University of Florida, University of Iowa, and several other good schools which would have been included in a longer list. These 12 Public Ivys, as one might expect, also ranked among the top 100schools on either or both of the U.S. News and Times Higher Education lists, which include both public and private institutions. Many people mock these rankings as manipulated beauty contests, and many people are probably right to do so. But, in education as elsewhere, perception is reality, and we are bound to take some notice of it. In the Great American Pecking Order, a degree from Cornell or Columbia might slightly outrank one from Berkeley or Michigan, but not by much. And, on a prestige-per-tuition-dollar basis, the ranking almost certainly tips back the other way. Investment performance, however, is objective, as most boards of trustees would agree; and we shall see how our state schools have done in that sphere. We'll also consider the relationship between pay and performance among their respective chief investment officers, and how they stack up against their colleagues at the private colleges. These are not small pots of money, either, even compared to the Private Ivys. The University of Texas controls more money than Princeton; Michigan is bigger than Columbia or Penn; and the University of California has an AUM higher than Duke or Cornell. In terms of endowment assets, our twelve Public Ivys range from about $18 billion for the University of Texas system down to $1.5 billion at University of Minnesota.  There are only about 45 U.S. endowments over $1.5 billion, so our 12 Private Ivys (in our last newsletter) and 12 Public Ivys comprise more than half of them, including the lions' share of total assets. Taken together, their performance should give us a pretty good picture of how the country's big, professionally-managed endowments are doing as of Fiscal Year 2012, ending last June. We'll look at longer-term performance further along, but first: who excelled (and who didn't) in FY 2012. The stock market did pretty well in this period, with the S&P 500 up 5.4 percent between July 2011 and June 2012. Domestic bonds did even better, such that a plain-vanilla 60/40 stock/bond portfolio would have returned about 6.2 percent. But the average large (over $1 billion) endowment earned 1.2 percent in 2012, per NACUBO. As we shall see, a big allocation to alternative assets didn't pay off for most of these investors in FY2012.

There are only about 45 U.S. endowments over $1.5 billion, so our 12 Private Ivys (in our last newsletter) and 12 Public Ivys comprise more than half of them, including the lions' share of total assets. Taken together, their performance should give us a pretty good picture of how the country's big, professionally-managed endowments are doing as of Fiscal Year 2012, ending last June. We'll look at longer-term performance further along, but first: who excelled (and who didn't) in FY 2012. The stock market did pretty well in this period, with the S&P 500 up 5.4 percent between July 2011 and June 2012. Domestic bonds did even better, such that a plain-vanilla 60/40 stock/bond portfolio would have returned about 6.2 percent. But the average large (over $1 billion) endowment earned 1.2 percent in 2012, per NACUBO. As we shall see, a big allocation to alternative assets didn't pay off for most of these investors in FY2012.  The clear winner is University of Virginia, with a very good 5.1 percent return. This is especially impressive when we note that five of our twelve state schools had negative returns, including the giant University of California system, with a dismal -1.10 percent. After all, as the media keep telling us, we are now enjoying an economic recovery. This should be gratifying for Lawrence E. Kochard who took over as head of the University of Virginia Investment Management Company (UVIMCO) in the middle of FY 2011, and reflects well on the UVIMCO board who hired him away from Georgetown University. FY 2012 performance can properly be credited to Dr. Kochard but, as we shall see below, the UVIMCO team also did well under his predecessor, Christopher Brightman. Harkening back to our original Private Ivy rankings for 2012, we also see that UV's performance beat all but three of the privates. UV topped Harvard, Yale and Princeton, and was surpassed only by MIT (8.0), Chicago (6.8), and Dartmouth (5.8). The news is not so good for University of California. With almost $11 billion on the line, their endowment (run by a patchwork of separate campus foundations, plus the central UC Regents Treasurer's office) managed to lose millions of dollars in a year when the stock market did pretty well. With the legislature already pinching state support for UC in recent years, this couldn't have been welcome news in Sacramento. More about UC further along. Any given portfolio in any given year can take a bad (or good) bounce; ask anyone who runs one. For our purposes, we think five-year investment return is the Goldilocks number. Since we're in the executive search business we want a number which can (usually) be attributed to identifiable individuals. Most fund managers don't have the longevity of Warren Buffett. Our research suggests that average tenure among endowment chief investment officers and senior staff is, coincidentally, about five years. Here are returns for our twelve Public Ivys over the eventful half-decade FY 2008 through FY 2012:

The clear winner is University of Virginia, with a very good 5.1 percent return. This is especially impressive when we note that five of our twelve state schools had negative returns, including the giant University of California system, with a dismal -1.10 percent. After all, as the media keep telling us, we are now enjoying an economic recovery. This should be gratifying for Lawrence E. Kochard who took over as head of the University of Virginia Investment Management Company (UVIMCO) in the middle of FY 2011, and reflects well on the UVIMCO board who hired him away from Georgetown University. FY 2012 performance can properly be credited to Dr. Kochard but, as we shall see below, the UVIMCO team also did well under his predecessor, Christopher Brightman. Harkening back to our original Private Ivy rankings for 2012, we also see that UV's performance beat all but three of the privates. UV topped Harvard, Yale and Princeton, and was surpassed only by MIT (8.0), Chicago (6.8), and Dartmouth (5.8). The news is not so good for University of California. With almost $11 billion on the line, their endowment (run by a patchwork of separate campus foundations, plus the central UC Regents Treasurer's office) managed to lose millions of dollars in a year when the stock market did pretty well. With the legislature already pinching state support for UC in recent years, this couldn't have been welcome news in Sacramento. More about UC further along. Any given portfolio in any given year can take a bad (or good) bounce; ask anyone who runs one. For our purposes, we think five-year investment return is the Goldilocks number. Since we're in the executive search business we want a number which can (usually) be attributed to identifiable individuals. Most fund managers don't have the longevity of Warren Buffett. Our research suggests that average tenure among endowment chief investment officers and senior staff is, coincidentally, about five years. Here are returns for our twelve Public Ivys over the eventful half-decade FY 2008 through FY 2012:  Again, team UVIMCO at University of Virginia leads, and by a good margin, with an annualized five-year return of 4.7 percent. For comparison, the NACUBO number for all large endowments, public and private, was just 1.7 percent; and the weighted average among our twelve Public Ivys was 1.9 percent. And look at that annualized CPI inflation over this period: 2.3 percent. Deflate those nominal returns for inflation and there are only a few positive real returns. This should be worrisome for any endowment investor who, above all, wants to preserve the purchasing power of the corpus. UVIMCO's return wasn't just good for a public college; it was good, period. Only a hair lower than Columbia University's 4.9 percent, which led the Private Ivys. Dr. Kochard's team out-invested every other traditional Ivy endowment in the period, including much bigger funds at Harvard, Yale and Princeton. Taking all 24 schools together, Virginia ranked 2nd out of 24. Not bad at all. Thomas Jefferson would be pleased. For most of this period Christopher Brightman was president and CIO of UVIMCO. Although he left Charlottesville in 2010, most of that performance was under his aegis, so he and his team deserve recognition for their excellent performance. In this half-decade, including the calamitous 2008/2009, equity investors faced severe headwinds. Even including the "recovery" of 2010-2012, the S&P lost 2.5 percent. On the other hand, the flight to safety and Fed intervention boosted domestic bonds, and the Barclay's index was up 6.8 percent. A passive investment in a traditional 60/40 blend would have given investors about a 1.2 percent return. As we can see, half of the Public Ivys beat that modest benchmark, but half didn't. Two of them had essentially zero returns, and two posted small losses. On a five-year basis, U of California is now in the middle, at 6th place, but it still managed only a highly mediocre 0.9 percent return. Someone has to finish last, and here it was Ohio State University, in 12th place with a negative 1.0 percent five-year return. However, on a 3-year basis, not shown here, they rise to 6th place, the middle of the pack. Notwithstanding our preference for a five-year measurement, we should note that there were some special circumstances in play in Columbus. Until late 2006, OSU's endowment was handled by long-time Treasurer James L. Nichols. Mr. Nichols was pushed out after an audit found that he had misled trustees about the size and performance of the endowment and made some other mistakes (although no criminal acts were alleged). A former state budget director was hired as interim investment manager and a long eighteen months elapsed as they did a national search for real CIO. When Jonathan Hook was recruited from Baylor University in June, 2008 (where he'd had an outstanding record as that school's first CIO). He had to begin from scratch at OSU with a retro-looking portfolio and no staff, not to mention having to cope with the implosion of world financial markets just as he was setting up shop. If we look at Mr. Hook's 3-year return in FY 2010 - 2012, we see that he has recently done pretty well, with an annualized return of 10.5 percent. But on the same three-year basis, University of Virginia still tops the league with a 14.6 return. Arguably, this is best way to measure overall investment performance, even if it isn't quite as intuitive as raw returns. High returns are only desirable if they don't involve excessive risk. Re-ranking these endowments by Sharpe ratio (where higher is better), we get this:

Again, team UVIMCO at University of Virginia leads, and by a good margin, with an annualized five-year return of 4.7 percent. For comparison, the NACUBO number for all large endowments, public and private, was just 1.7 percent; and the weighted average among our twelve Public Ivys was 1.9 percent. And look at that annualized CPI inflation over this period: 2.3 percent. Deflate those nominal returns for inflation and there are only a few positive real returns. This should be worrisome for any endowment investor who, above all, wants to preserve the purchasing power of the corpus. UVIMCO's return wasn't just good for a public college; it was good, period. Only a hair lower than Columbia University's 4.9 percent, which led the Private Ivys. Dr. Kochard's team out-invested every other traditional Ivy endowment in the period, including much bigger funds at Harvard, Yale and Princeton. Taking all 24 schools together, Virginia ranked 2nd out of 24. Not bad at all. Thomas Jefferson would be pleased. For most of this period Christopher Brightman was president and CIO of UVIMCO. Although he left Charlottesville in 2010, most of that performance was under his aegis, so he and his team deserve recognition for their excellent performance. In this half-decade, including the calamitous 2008/2009, equity investors faced severe headwinds. Even including the "recovery" of 2010-2012, the S&P lost 2.5 percent. On the other hand, the flight to safety and Fed intervention boosted domestic bonds, and the Barclay's index was up 6.8 percent. A passive investment in a traditional 60/40 blend would have given investors about a 1.2 percent return. As we can see, half of the Public Ivys beat that modest benchmark, but half didn't. Two of them had essentially zero returns, and two posted small losses. On a five-year basis, U of California is now in the middle, at 6th place, but it still managed only a highly mediocre 0.9 percent return. Someone has to finish last, and here it was Ohio State University, in 12th place with a negative 1.0 percent five-year return. However, on a 3-year basis, not shown here, they rise to 6th place, the middle of the pack. Notwithstanding our preference for a five-year measurement, we should note that there were some special circumstances in play in Columbus. Until late 2006, OSU's endowment was handled by long-time Treasurer James L. Nichols. Mr. Nichols was pushed out after an audit found that he had misled trustees about the size and performance of the endowment and made some other mistakes (although no criminal acts were alleged). A former state budget director was hired as interim investment manager and a long eighteen months elapsed as they did a national search for real CIO. When Jonathan Hook was recruited from Baylor University in June, 2008 (where he'd had an outstanding record as that school's first CIO). He had to begin from scratch at OSU with a retro-looking portfolio and no staff, not to mention having to cope with the implosion of world financial markets just as he was setting up shop. If we look at Mr. Hook's 3-year return in FY 2010 - 2012, we see that he has recently done pretty well, with an annualized return of 10.5 percent. But on the same three-year basis, University of Virginia still tops the league with a 14.6 return. Arguably, this is best way to measure overall investment performance, even if it isn't quite as intuitive as raw returns. High returns are only desirable if they don't involve excessive risk. Re-ranking these endowments by Sharpe ratio (where higher is better), we get this:  Virginia is still number one with a bullet. This implies that they're not ramping up risk to achieve their good earnings. Interestingly, Texas jumps up three places in the rankings as we move from raw to risk-adjusted performance. In fact, Mr. Zimmerman's team achieved by far the lowest standard deviation of returns in this group. Remember, too, that a negative SR means that an investor would have done better just closing up the office and putting her money into T-bills for five years. Be warned, not every theoretician thinks that after-the-fact standard deviation of returns is a proper measure of risk, per the Sharpe ratio. This statistic presumes that investment returns are normally distributed per the traditional Gaussian bell-shaped function. Some critics, such as the redoubtable Nassim Nicholas Taleb think that real risk is something darker and deeper; it's where the unknown unknowns and Black Swans lurk. That's all way above our pay-grade. We still think the SR helps to understand how managers are balancing risk and return, which is the essence of their job. If you're a board member, recruiter, or just dying to know, here's the good stuff. Who runs the investment office, and how much are they paid?

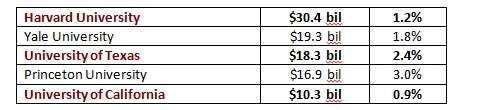

Virginia is still number one with a bullet. This implies that they're not ramping up risk to achieve their good earnings. Interestingly, Texas jumps up three places in the rankings as we move from raw to risk-adjusted performance. In fact, Mr. Zimmerman's team achieved by far the lowest standard deviation of returns in this group. Remember, too, that a negative SR means that an investor would have done better just closing up the office and putting her money into T-bills for five years. Be warned, not every theoretician thinks that after-the-fact standard deviation of returns is a proper measure of risk, per the Sharpe ratio. This statistic presumes that investment returns are normally distributed per the traditional Gaussian bell-shaped function. Some critics, such as the redoubtable Nassim Nicholas Taleb think that real risk is something darker and deeper; it's where the unknown unknowns and Black Swans lurk. That's all way above our pay-grade. We still think the SR helps to understand how managers are balancing risk and return, which is the essence of their job. If you're a board member, recruiter, or just dying to know, here's the good stuff. Who runs the investment office, and how much are they paid?  N.B.: Compensation figures are for calendar 2010 unless otherwise noted. (1) Brightman left UVIMCO in March 2010. 2010 comp includes final separation payout. (2) Kochard joined UVIMCO Jan 2011. Calendar yr 2011 comp per FY2012 unreleased Form 990. (3) Zimmerman 2010 comp excludes $1.9 million deferred comp. (4) Lundberg comp for calendar 2012. (5) King's 2010 comp excludes $139.3 K deferred comp. (6) Ferguson comp is for calendar 2011. (7) Krueger comp as of Dec, 2012 (8) Branigan comp estimate for calendar 2012. (9) Ellison joined U of Illinois Fdn in Jan 2013. Comp is estimate for calendar 2013. (10) Stratten comp excludes $35.3 K cumulative deferred comp and $25.5 K nontaxable benefits. As executive recruiters, we tend to think that the ability to pay more will attract better talent. And, we have a meritocratic bias; we like to think that superior performance should be rewarded with superior compensation. There's a lot to be said for both those positions but, of course, things don't always work out that neatly. The size of the job in terms of AUM is also an important factor. As we've noted, University of California's endowment performance has been unimpressive. However, while Marie Berggren handles about $6 billion of the whole UC endowment, she's also responsible for investing a whopping $70 billion in pension funds. Her salary is commensurate with running that much money. And, consider Amy Krueger Marsh. Ms. Marsh, the long-time Treasurer and CIO at University of Pittsburgh, has produced a good 5-year return of 2.5 percent, ranking 4th among our twelve Public Ivys. For this she's paid only about $400 thousand. That's better 5-year performance than Mr. Zimmerman at UTIMCO (with his $1.3 million comp) or Ms. Mendillo at Harvard (with her $3.6 million). And, CIO is just one of her hats. She's also responsible for the whole Treasurer's office. On a performance-for-pay basis she's a star, and her board should be glad to have her. Three of the four largest public Ivys are getting pretty good investment returns on a 5-year basis: Virginia, Michigan, and Texas. The exception is University of California, earning only 0.9 percent over five years. We should carefully note that this return figure for UC is a composite, averaging together 1.5 percent for the $6.0 billion in the general endowment pool operated by the UC Regents Treasurer's office in Oakland, with lower returns from the $4.3 billion in the separate campus foundations. On this basis, UC has a $10.3 billion endowment, the 5th largest in the country (after Harvard, Yale, Texas, and Princeton), but its investment performance is the lowest among these five mega-endowments:

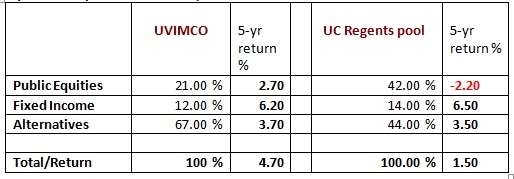

N.B.: Compensation figures are for calendar 2010 unless otherwise noted. (1) Brightman left UVIMCO in March 2010. 2010 comp includes final separation payout. (2) Kochard joined UVIMCO Jan 2011. Calendar yr 2011 comp per FY2012 unreleased Form 990. (3) Zimmerman 2010 comp excludes $1.9 million deferred comp. (4) Lundberg comp for calendar 2012. (5) King's 2010 comp excludes $139.3 K deferred comp. (6) Ferguson comp is for calendar 2011. (7) Krueger comp as of Dec, 2012 (8) Branigan comp estimate for calendar 2012. (9) Ellison joined U of Illinois Fdn in Jan 2013. Comp is estimate for calendar 2013. (10) Stratten comp excludes $35.3 K cumulative deferred comp and $25.5 K nontaxable benefits. As executive recruiters, we tend to think that the ability to pay more will attract better talent. And, we have a meritocratic bias; we like to think that superior performance should be rewarded with superior compensation. There's a lot to be said for both those positions but, of course, things don't always work out that neatly. The size of the job in terms of AUM is also an important factor. As we've noted, University of California's endowment performance has been unimpressive. However, while Marie Berggren handles about $6 billion of the whole UC endowment, she's also responsible for investing a whopping $70 billion in pension funds. Her salary is commensurate with running that much money. And, consider Amy Krueger Marsh. Ms. Marsh, the long-time Treasurer and CIO at University of Pittsburgh, has produced a good 5-year return of 2.5 percent, ranking 4th among our twelve Public Ivys. For this she's paid only about $400 thousand. That's better 5-year performance than Mr. Zimmerman at UTIMCO (with his $1.3 million comp) or Ms. Mendillo at Harvard (with her $3.6 million). And, CIO is just one of her hats. She's also responsible for the whole Treasurer's office. On a performance-for-pay basis she's a star, and her board should be glad to have her. Three of the four largest public Ivys are getting pretty good investment returns on a 5-year basis: Virginia, Michigan, and Texas. The exception is University of California, earning only 0.9 percent over five years. We should carefully note that this return figure for UC is a composite, averaging together 1.5 percent for the $6.0 billion in the general endowment pool operated by the UC Regents Treasurer's office in Oakland, with lower returns from the $4.3 billion in the separate campus foundations. On this basis, UC has a $10.3 billion endowment, the 5th largest in the country (after Harvard, Yale, Texas, and Princeton), but its investment performance is the lowest among these five mega-endowments:  In our report on the Private Ivys we spent some time trying to figure out why mighty Harvard, with all its investment expertise, earned only an annualized 1.2 percent over five years. So, now let's see what's up with UC. There doesn't seem to be any obvious reason why a public university can't build a first-rate investment team. University of Virginia and University of Texas have shown that it can be done. But we think there are some institutional constraints which may make it harder for a public endowment to achieve consistently good returns. There may also be some clues in the UC asset allocations, and we'll take a look at those, too. Endowments report their asset allocations and performance in idiosyncratic ways which make it hard for amateurs like us to make strict comparisons. But if the UC Regents pool (GEP) earned 1.5 percent, while UVIMCO earned 4.7 percent in the same period, then it should be possible to make some surmises about what caused that gap, and whether they're due to allocations or execution (excess returns versus benchmarks). This chart involves some rather crude rounding, classifying, and interpolating, but we think it's basically correct. (FY 2012 reported allocations)

In our report on the Private Ivys we spent some time trying to figure out why mighty Harvard, with all its investment expertise, earned only an annualized 1.2 percent over five years. So, now let's see what's up with UC. There doesn't seem to be any obvious reason why a public university can't build a first-rate investment team. University of Virginia and University of Texas have shown that it can be done. But we think there are some institutional constraints which may make it harder for a public endowment to achieve consistently good returns. There may also be some clues in the UC asset allocations, and we'll take a look at those, too. Endowments report their asset allocations and performance in idiosyncratic ways which make it hard for amateurs like us to make strict comparisons. But if the UC Regents pool (GEP) earned 1.5 percent, while UVIMCO earned 4.7 percent in the same period, then it should be possible to make some surmises about what caused that gap, and whether they're due to allocations or execution (excess returns versus benchmarks). This chart involves some rather crude rounding, classifying, and interpolating, but we think it's basically correct. (FY 2012 reported allocations)  As of 2012, UC had a 42 percent allocation to public equities (both U.S. and non-U.S.). The corresponding number for UVIMCO was just 21 percent. That's a fairly striking difference right there. UC's allocation was markedly higher than the NACUBO average for all big endowments (27 percent), and UVIMCO's was significantly lower. About half of UC's public equity was non-U.S., and they lost an annualized 5 percent on that portion. Returns on domestic equity were -0.2 percent, so returns average out to -2.2 percent for all public equity over five years. UVIMCO doesn't break out U.S. vs. non-U.S. equity, but their overall 5-year return for public equity was positive: 2.7 percent. The MSCI All Country World Equity 5-year return was -2.2 percent in this period. If we take that as a benchmark, then UC hit it on the nose, whereas UVIMCO beat it handily, with an excess return of 4.9 percent. (UC benchmarks its domestic equity against the Russell 3000, but it missed that, too; by 37 basis points). Both portfolios are highly diversified and each had some hits and misses, but without getting into all the grittiness, we think that little chart above tells the story. UVIMCO's higher allocation to alternatives vs. equities helped somewhat in this period, but it was superior execution of their equity strategies that gave them a real edge. One way that public school endowments can help level the investment playing field is by creating a semi-autonomous investment management company (SAIMCO?). This idea began among the old Private Ivys, but was soon aped by their public sisters. Among our twelve Public Ivys, Virginia, Texas and North Carolina have one each. The University of California system now actually has two, as we'll see in a moment. A SAIMCO has at least two advantages: First, it provides an additional layer of insulation between the endowment and its ultimate overseers, remembering that, among the publics, the powers-that-be are usually hip-deep in state politics, which can interfere with effective management. Unfortunate examples abound in the world of public pensions, which face similar governance issues. Second, an "independent" investment company can usually get away with paying the investment staff more generously when they are, technically, no longer state employees. As recruiters, we are particularly aware of this problem. As an added bonus, a SAIMCO makes it easier to dodge each Spring's new crop of matriculants as they parade around the quad demanding immediate disinvestment in whatever. The president and trustees can point to their SAIMCO and truthfully say that it's out of their hands. At University of Virginia's UVIMCO, for instance, the president/CIO is normally paid about $1.3 to 1.5 million, including bonus (as of 2010). And, as we've seen, Mr. Brightman -- and now Dr. Kochard -- have been earning their keep. Their pay, however, is still not quite comparable to CIOs at the top Private Ivys such as Harvard, Yale, and Columbia. (See: http://www.charlesskorina.com/775/) Bruce Zimmerman, head of UTIMCO at University of Texas also does well, receiving about $1.3 million in 2010. Jon King, head of North Carolina's UNC Management Company, made significantly less, about $711 thousand in 2010, but his endowment is much smaller than UTIMCO's, and only half the size of Virginia's. Another institutional constraint faced by UC is getting into top private equity funds without having to disclose more about them than the general partners would like. It's well known that the top-tier of private equity performs a lot better than the rest. An endowment the size of UC Regents should be able to invest in those top firms; except when it can't. According to UC, some top-shelf firms like Sequoia and Kleiner Perkins have blacklisted them from future funds after a court ruling forced the Regents to release details about fund performance in 2003. As of right now, the matter is still being litigated. The UC Regents is an organ of the state government and various state laws require that they tell the world what they do with their money. Harvard and its sisters are private corporations which don't have to make such disclosures. How about the private campus foundations and their SAIMCO satellites which run a big chunk of the total UC endowment? A question for the lawyers, but we suspect not. U.S. public universities have been in a financial bind for several years. This may puzzle any readers who have had to stump up for constantly-rising tuition at one of these fine institutions, but it seems to be true. In the gravy decade of 1999-2009, state financial support for colleges grew steadily, with spending across the country up almost 50 percent. It was good times on the campuses, with schools expanding their plants and, especially, their administrative headcount and compensation. But, after the crunch of 2008/2009, the trend reversed. Total state spending is now down almost 11 percent in the five years 2008 - 2013. California, with by far the biggest higher-ed budget, has taken the biggest hit, with annual spending down 24 percent over five years: from $11.6 billion to $8.8 billion. (All figures per Center for the Study of Education Policy at Illinois State University http://grapevine.illinoisstate.edu/index.shtml). None of this is supposed to be a direct concern for endowment managers, in California or elsewhere, but it would be naïve to think that it doesn't affect the context in which they operate. When campus personnel are being cut and tuition is escalating, it becomes politically more difficult to staff up the investment office and pay the going rate for top talent. If they aren't segregated in a separate foundation or investment company (and many aren't), they become just one more office competing for a shrinking budget. The fact that they make money, instead of just spending it, should cut some ice, but usually doesn't. Historically, public schools have had smaller endowments than private colleges and haven't relied on them as heavily to fund their annual expenses. But that may be changing. In a country full of tapped-out states, Public Ivy leaders may have to learn to rely much more on private donations if they expect to keep their excellent jobs and perks. Let's take California, which happens to be both big and broke (1). Its world-class University of California system is Exhibit A for this trend. (1) That's not rhetoric. The California State Auditor has just issued her report for FY2012, which says liabilities exceed assets by $127 billion. The technical accounting term for that is: "broke." That doesn't include hundreds of millions in unfunded liabilities for pensions and retiree health care. People running a private business would be imprisoned for such omissions and, indeed, the Governmental Accounting Standards Board and Moody's have been pushing states to include such items in their balance sheets. The legislature, understandably, doesn't agree, and the State Auditor can only follow the rules she's given. See: http://www.sanluisobispo.com/2013/03/28/2448374/capitol-alert-state-auditor-californias.html#storylink=cpyc The annual NACUBO-Commonfund endowment report says that "University of California" has an endowment of almost $6 billion as of June, 26012. This is technically correct, but slightly misleading. The UC Regents (the system's governing body) invests that $6 billion through its Treasurer's office in Oakland. But the total system endowment is much more: about $10.3 billion. The other $4.3 billion is invested by separate campus foundations. Most of the $6 billion controlled by the UC Regents is legally earmarked for spending on some specific campus and could therefore be counted as part of that campus endowment. The $4.3 billion controlled by the separate campus foundations can be invested as their respective boards prefer. They can use external managers, or even choose to invest some of it internally, using their own staff. And now, the two biggest campus foundations, UC Berkeley Foundation ($1.1 billion) and UCLA Foundation ($1.3 billion), have recently set up their own investment companies, each with a chief investment officer and professional staff. So, that 0.9 percent 5-year return we calculated for the UC system is actually generated by a blend of investment managers. In fact, the Regents General Endowment Pool (GEP) returned 1.5 percent over five years. Not great, but only a little short of the NACUBO 5-year average of 1.7 percent for all large endowments, and better than Harvard in the same period. What pulled the system average down was investment performance at the campus foundations, primarily at the two big ones: Berkeley and UCLA. They handle about $2.4 billion, with the rest of the system's endowment money scattered among eight smaller campus foundations. Up in Oakland, Marie Berggren, whose official title is Acting Treasurer and Chief Investment Officer of the Regents, runs an investment staff responsible for about $6 billion of endowment funds. In Berkeley, John-Austin Saviano, a former consultant with Cambridge Associates, is president and CIO of the Berkeley Endowment Management Company (BEMCO), investing about $1.1 billion. BEMCO was set up by the UC Berkeley Foundation in 2009. As of 2010, his total comp is $430,390 including a $134,000 bonus. Down in Los Angeles, Srinivas "Srini" Pulavarti, formerly CIO at University of Richmond's Spider Management Company, is president and CIO of UCLA Investment Company, launched in 2012, and managing about $1.3 billion. Srini, one of the country's outstanding endowment investors, was recruited by UCLA just last year and is their first "real" CIO. We think that Mr. Pulavarti's total compensation package, based on his prior earnings, is at least $900 thousand. A lot of money was mobilized to launch these operations. In Berkeley, the William and Flora Hewlett Foundation donated $3 million to set up BEMCO. In L.A., the UCLA Foundation has committed $1 million per year to support their new management company for the first four years. Part of the logic here applies to any endowment as the fund gets big enough to justify full-time, professional management. The hope is always that these pros can reduce fees previously paid to external managers, while also improving returns. In theory, they can pay for themselves and make the office self-supporting within a few years. We think there's also a bigger picture. As state money shrinks, each campus increasingly has to swim for itself. There's a limit to how high tuition can be hiked, and there's only one remaining source of funds: private donations. But the big, sophisticated investors they're targeting want to see proof that their money can be efficiently invested. Having a qualified CIO on hand, with a real track record, can be a major sales tool for the development officers. After all, if the average Silicon Valley mogul thinks he can invest the money better himself, then why would he not do so, and then gift it out of his estate thirty or forty years from now? Obviously, the schools would rather have the money today, and the income it generates. It's too early to see how these new CIOs are working out. BEMCO has only really been up and running for two years, and UCLAIC has just launched. But UC's own reports make it possible to see what investment returns are campus by campus in recent years. The UCLA Foundation earned only 0.3 percent over five years on its self-managed portfolio. If we count the UCLA-earmarked funds managed by the Regents, we could say that the UCLA endowment earned 1.1 percent overall. The money they're plowing into their new investment office is certainly intended to get something more impressive than a 0.3 percent return over the next five years. Berkeley, the other big campus, did only slightly better, with a 5-year return of 0.8 percent on the $1.1 billion they run through BEMCO. Averaged together with Berkeley-earmarked money in the Regents pool, they've made about 1.3 percent on their endowment overall. Again, the BEMCO board, looking forward, would like to see better numbers in the years ahead. In theory, UC is one big happy family, and no one should care whether a donor writes a check to the UC Regents or to a separate campus foundation. In practice, every campus would prefer to have the closest possible relationship to its benefactors and their money. David Blinder, Berkeley's top development exec, told a reporter last year: "It is our belief that the donors...feel a higher level of confidence knowing that it is the campus controlling the investment. Right now, in our conversations with donors, we recommend in the strongest way that endowment gifts and checks and stocks go to the Berkeley Foundation. It gives us that direct link." Mr. Blinder was formerly the top fund-raiser at tony Wellesley College in Massachusetts, where he ran a record-breaking development campaign. In 2011, after four years on the job at Berkeley, Mr. Blinder was handed an out-of-schedule $40 thousand salary boost, from $240 K to $280 K, because he was being aggressively courted by other employers, including Berkeley's sister UC campus at Irvine. Although he was also a VP of the Foundation, he was paid as an Associate Vice Chancellor of the University, constrained by the campus pay-scales. They noted that: "As UC Berkeley comes to rely more on private support, professional development leaders like Mr. Blinder are critical to the campus ability to maximize their philanthropy." In plain terms, he's very good at pulling in the money which the state no longer provides. Unfortunately, their retention efforts fell short. Dr. Blinder was just stolen away by the Scripps Institute, where he started as their senior VP for External Affairs on March 1. We suspect he got a very handsome offer well over the $280 K that Berkeley could afford. But Dr. Blinder left behind his giant database. There are a million names in it, and if you're Berkeley grad, they will find you. Our focus on the UC situation is not intended to demean anyone over there. I know several of the UC Regents managers, who labor just across the Bay from me, and I can attest that they're very good at their jobs. Our question is whether the institutional framework can make optimal use of their talent. But, UC's size makes it conspicuous, and we think their situation is, to a considerable extent, similar to other public universities across the country. They're competing with other potent interest groups, including the public unions and K-12 schools, for slow-growing, debt-strapped state budgets. We think they are inevitably going to have to rely more heavily on private financial support. Spinning off SAIMCOs, as Virginia and Texas did years ago, and UC is doing now, may help. However they go about it, our big public colleges are going to have to get more serious than ever about building and maintaining top-flight, professionally staffed investment organizations.

As of 2012, UC had a 42 percent allocation to public equities (both U.S. and non-U.S.). The corresponding number for UVIMCO was just 21 percent. That's a fairly striking difference right there. UC's allocation was markedly higher than the NACUBO average for all big endowments (27 percent), and UVIMCO's was significantly lower. About half of UC's public equity was non-U.S., and they lost an annualized 5 percent on that portion. Returns on domestic equity were -0.2 percent, so returns average out to -2.2 percent for all public equity over five years. UVIMCO doesn't break out U.S. vs. non-U.S. equity, but their overall 5-year return for public equity was positive: 2.7 percent. The MSCI All Country World Equity 5-year return was -2.2 percent in this period. If we take that as a benchmark, then UC hit it on the nose, whereas UVIMCO beat it handily, with an excess return of 4.9 percent. (UC benchmarks its domestic equity against the Russell 3000, but it missed that, too; by 37 basis points). Both portfolios are highly diversified and each had some hits and misses, but without getting into all the grittiness, we think that little chart above tells the story. UVIMCO's higher allocation to alternatives vs. equities helped somewhat in this period, but it was superior execution of their equity strategies that gave them a real edge. One way that public school endowments can help level the investment playing field is by creating a semi-autonomous investment management company (SAIMCO?). This idea began among the old Private Ivys, but was soon aped by their public sisters. Among our twelve Public Ivys, Virginia, Texas and North Carolina have one each. The University of California system now actually has two, as we'll see in a moment. A SAIMCO has at least two advantages: First, it provides an additional layer of insulation between the endowment and its ultimate overseers, remembering that, among the publics, the powers-that-be are usually hip-deep in state politics, which can interfere with effective management. Unfortunate examples abound in the world of public pensions, which face similar governance issues. Second, an "independent" investment company can usually get away with paying the investment staff more generously when they are, technically, no longer state employees. As recruiters, we are particularly aware of this problem. As an added bonus, a SAIMCO makes it easier to dodge each Spring's new crop of matriculants as they parade around the quad demanding immediate disinvestment in whatever. The president and trustees can point to their SAIMCO and truthfully say that it's out of their hands. At University of Virginia's UVIMCO, for instance, the president/CIO is normally paid about $1.3 to 1.5 million, including bonus (as of 2010). And, as we've seen, Mr. Brightman -- and now Dr. Kochard -- have been earning their keep. Their pay, however, is still not quite comparable to CIOs at the top Private Ivys such as Harvard, Yale, and Columbia. (See: http://www.charlesskorina.com/775/) Bruce Zimmerman, head of UTIMCO at University of Texas also does well, receiving about $1.3 million in 2010. Jon King, head of North Carolina's UNC Management Company, made significantly less, about $711 thousand in 2010, but his endowment is much smaller than UTIMCO's, and only half the size of Virginia's. Another institutional constraint faced by UC is getting into top private equity funds without having to disclose more about them than the general partners would like. It's well known that the top-tier of private equity performs a lot better than the rest. An endowment the size of UC Regents should be able to invest in those top firms; except when it can't. According to UC, some top-shelf firms like Sequoia and Kleiner Perkins have blacklisted them from future funds after a court ruling forced the Regents to release details about fund performance in 2003. As of right now, the matter is still being litigated. The UC Regents is an organ of the state government and various state laws require that they tell the world what they do with their money. Harvard and its sisters are private corporations which don't have to make such disclosures. How about the private campus foundations and their SAIMCO satellites which run a big chunk of the total UC endowment? A question for the lawyers, but we suspect not. U.S. public universities have been in a financial bind for several years. This may puzzle any readers who have had to stump up for constantly-rising tuition at one of these fine institutions, but it seems to be true. In the gravy decade of 1999-2009, state financial support for colleges grew steadily, with spending across the country up almost 50 percent. It was good times on the campuses, with schools expanding their plants and, especially, their administrative headcount and compensation. But, after the crunch of 2008/2009, the trend reversed. Total state spending is now down almost 11 percent in the five years 2008 - 2013. California, with by far the biggest higher-ed budget, has taken the biggest hit, with annual spending down 24 percent over five years: from $11.6 billion to $8.8 billion. (All figures per Center for the Study of Education Policy at Illinois State University http://grapevine.illinoisstate.edu/index.shtml). None of this is supposed to be a direct concern for endowment managers, in California or elsewhere, but it would be naïve to think that it doesn't affect the context in which they operate. When campus personnel are being cut and tuition is escalating, it becomes politically more difficult to staff up the investment office and pay the going rate for top talent. If they aren't segregated in a separate foundation or investment company (and many aren't), they become just one more office competing for a shrinking budget. The fact that they make money, instead of just spending it, should cut some ice, but usually doesn't. Historically, public schools have had smaller endowments than private colleges and haven't relied on them as heavily to fund their annual expenses. But that may be changing. In a country full of tapped-out states, Public Ivy leaders may have to learn to rely much more on private donations if they expect to keep their excellent jobs and perks. Let's take California, which happens to be both big and broke (1). Its world-class University of California system is Exhibit A for this trend. (1) That's not rhetoric. The California State Auditor has just issued her report for FY2012, which says liabilities exceed assets by $127 billion. The technical accounting term for that is: "broke." That doesn't include hundreds of millions in unfunded liabilities for pensions and retiree health care. People running a private business would be imprisoned for such omissions and, indeed, the Governmental Accounting Standards Board and Moody's have been pushing states to include such items in their balance sheets. The legislature, understandably, doesn't agree, and the State Auditor can only follow the rules she's given. See: http://www.sanluisobispo.com/2013/03/28/2448374/capitol-alert-state-auditor-californias.html#storylink=cpyc The annual NACUBO-Commonfund endowment report says that "University of California" has an endowment of almost $6 billion as of June, 26012. This is technically correct, but slightly misleading. The UC Regents (the system's governing body) invests that $6 billion through its Treasurer's office in Oakland. But the total system endowment is much more: about $10.3 billion. The other $4.3 billion is invested by separate campus foundations. Most of the $6 billion controlled by the UC Regents is legally earmarked for spending on some specific campus and could therefore be counted as part of that campus endowment. The $4.3 billion controlled by the separate campus foundations can be invested as their respective boards prefer. They can use external managers, or even choose to invest some of it internally, using their own staff. And now, the two biggest campus foundations, UC Berkeley Foundation ($1.1 billion) and UCLA Foundation ($1.3 billion), have recently set up their own investment companies, each with a chief investment officer and professional staff. So, that 0.9 percent 5-year return we calculated for the UC system is actually generated by a blend of investment managers. In fact, the Regents General Endowment Pool (GEP) returned 1.5 percent over five years. Not great, but only a little short of the NACUBO 5-year average of 1.7 percent for all large endowments, and better than Harvard in the same period. What pulled the system average down was investment performance at the campus foundations, primarily at the two big ones: Berkeley and UCLA. They handle about $2.4 billion, with the rest of the system's endowment money scattered among eight smaller campus foundations. Up in Oakland, Marie Berggren, whose official title is Acting Treasurer and Chief Investment Officer of the Regents, runs an investment staff responsible for about $6 billion of endowment funds. In Berkeley, John-Austin Saviano, a former consultant with Cambridge Associates, is president and CIO of the Berkeley Endowment Management Company (BEMCO), investing about $1.1 billion. BEMCO was set up by the UC Berkeley Foundation in 2009. As of 2010, his total comp is $430,390 including a $134,000 bonus. Down in Los Angeles, Srinivas "Srini" Pulavarti, formerly CIO at University of Richmond's Spider Management Company, is president and CIO of UCLA Investment Company, launched in 2012, and managing about $1.3 billion. Srini, one of the country's outstanding endowment investors, was recruited by UCLA just last year and is their first "real" CIO. We think that Mr. Pulavarti's total compensation package, based on his prior earnings, is at least $900 thousand. A lot of money was mobilized to launch these operations. In Berkeley, the William and Flora Hewlett Foundation donated $3 million to set up BEMCO. In L.A., the UCLA Foundation has committed $1 million per year to support their new management company for the first four years. Part of the logic here applies to any endowment as the fund gets big enough to justify full-time, professional management. The hope is always that these pros can reduce fees previously paid to external managers, while also improving returns. In theory, they can pay for themselves and make the office self-supporting within a few years. We think there's also a bigger picture. As state money shrinks, each campus increasingly has to swim for itself. There's a limit to how high tuition can be hiked, and there's only one remaining source of funds: private donations. But the big, sophisticated investors they're targeting want to see proof that their money can be efficiently invested. Having a qualified CIO on hand, with a real track record, can be a major sales tool for the development officers. After all, if the average Silicon Valley mogul thinks he can invest the money better himself, then why would he not do so, and then gift it out of his estate thirty or forty years from now? Obviously, the schools would rather have the money today, and the income it generates. It's too early to see how these new CIOs are working out. BEMCO has only really been up and running for two years, and UCLAIC has just launched. But UC's own reports make it possible to see what investment returns are campus by campus in recent years. The UCLA Foundation earned only 0.3 percent over five years on its self-managed portfolio. If we count the UCLA-earmarked funds managed by the Regents, we could say that the UCLA endowment earned 1.1 percent overall. The money they're plowing into their new investment office is certainly intended to get something more impressive than a 0.3 percent return over the next five years. Berkeley, the other big campus, did only slightly better, with a 5-year return of 0.8 percent on the $1.1 billion they run through BEMCO. Averaged together with Berkeley-earmarked money in the Regents pool, they've made about 1.3 percent on their endowment overall. Again, the BEMCO board, looking forward, would like to see better numbers in the years ahead. In theory, UC is one big happy family, and no one should care whether a donor writes a check to the UC Regents or to a separate campus foundation. In practice, every campus would prefer to have the closest possible relationship to its benefactors and their money. David Blinder, Berkeley's top development exec, told a reporter last year: "It is our belief that the donors...feel a higher level of confidence knowing that it is the campus controlling the investment. Right now, in our conversations with donors, we recommend in the strongest way that endowment gifts and checks and stocks go to the Berkeley Foundation. It gives us that direct link." Mr. Blinder was formerly the top fund-raiser at tony Wellesley College in Massachusetts, where he ran a record-breaking development campaign. In 2011, after four years on the job at Berkeley, Mr. Blinder was handed an out-of-schedule $40 thousand salary boost, from $240 K to $280 K, because he was being aggressively courted by other employers, including Berkeley's sister UC campus at Irvine. Although he was also a VP of the Foundation, he was paid as an Associate Vice Chancellor of the University, constrained by the campus pay-scales. They noted that: "As UC Berkeley comes to rely more on private support, professional development leaders like Mr. Blinder are critical to the campus ability to maximize their philanthropy." In plain terms, he's very good at pulling in the money which the state no longer provides. Unfortunately, their retention efforts fell short. Dr. Blinder was just stolen away by the Scripps Institute, where he started as their senior VP for External Affairs on March 1. We suspect he got a very handsome offer well over the $280 K that Berkeley could afford. But Dr. Blinder left behind his giant database. There are a million names in it, and if you're Berkeley grad, they will find you. Our focus on the UC situation is not intended to demean anyone over there. I know several of the UC Regents managers, who labor just across the Bay from me, and I can attest that they're very good at their jobs. Our question is whether the institutional framework can make optimal use of their talent. But, UC's size makes it conspicuous, and we think their situation is, to a considerable extent, similar to other public universities across the country. They're competing with other potent interest groups, including the public unions and K-12 schools, for slow-growing, debt-strapped state budgets. We think they are inevitably going to have to rely more heavily on private financial support. Spinning off SAIMCOs, as Virginia and Texas did years ago, and UC is doing now, may help. However they go about it, our big public colleges are going to have to get more serious than ever about building and maintaining top-flight, professionally staffed investment organizations.

Charles A. Skorina & Co is retained by the boards of institutional investors and asset managers to recruit chief investment officers, portfolio managers, and financial professionals. Charles Skorina earned an MBA at the University of Chicago and began his professional career at Chemical Bank (now JPMorgan Chase), completing the management training program then working as a credit and risk analyst in New York and Chicago. After a stint with Ernst & Young in Washington, D.C., he founded his own search firm headquartered in San Francisco, focused on the global financial services industry.