By John Bhadki

By John Bhadki

In 2010, we started the development of i2X by taking a deeper look into the economics of seed stage investing. A Kauffmann study on returns of angel groups showed 27% annualized returns at a median return of -20%. This summarizes the central challenge in seed investing: outstanding average returns, but at unacceptable risk levels.

The risk problem can be put into perspective by a simple thought experiment: if you capture one Facebook at seed stage, it offsets over 5000 total losses in the same portfolio within 7 years; one Dropbox creates a 2x return for a 500 startup portfolio, even if all others return 0% p.a.

But thought experiments are not actionable. As long as we don't know the empirical truth of portfolio returns, seed investing will remain an irrational act. And so, our mission was to find a filter and reference point that enables the design of a structured seed stage investment framework.

15 Accelerators With 1000+ Historic Start-ups

Our approach for building this reference point was the new generation of startup accelerators that had emerged over the past few years. We chose 15 leading accelerator programs as our analytics target, and started the analytics process. The first step turned out to be the most difficult: building a comprehensive data layer that would entail all investment rounds, dates and valuations for every historic start-up in these ecosystems. This was a daunting task: we had to develop new ways to acquire highly confidential data, and build a system of proprietary algorithms to complete missing data points with sufficient accuracy by using reference points in the wider VC data universe.

After 12 months and endless operational and mathematical hacking of the problem, we finally achieved our goal: an advanced robust data engine that minimized the margin of error, and provided us with a uniquely complete picture of the i2X accelerator ecosystem and over 1000 technology startups from our accelerator network. All we had to do now was to create an analytics layer on top of this data matrix to simulate fund performance and risk.

Today, the i2X engine provides us with analytics on-par with elite scientific hedge funds, and allows us to simulate risk/return profiles across different accelerators with a high level of accuracy.

The results provide us with a comprehensive insight into the economics of “Breeding Pioneers”. The following projections simulate the outcomes for one specific fund design (the exact design is confidential, but think a combination of clusters such as 10% consumer web startups / DreamIt Ventures, 15% enterprise start-ups / Y-Combinator, etc.) across four portfolios sizes: 5, 25, 75 and 100 start-ups.

Advanced Analytics Reveal the Empirical Performance of Seed Stage Portfolios

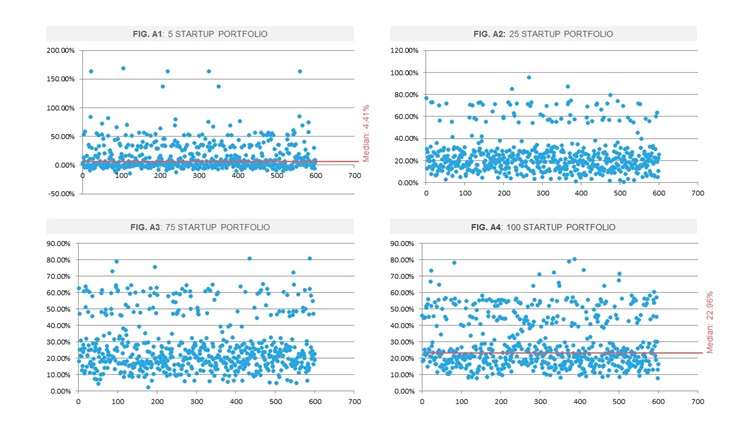

To simulate the outcome, we run 600 simulations per portfolio size that randomly pick start-ups in the target clusters from the historic data base. Each blue dot represents the annualized returns of one portfolio (Fig. A1-A4).

The simulation reveals an interesting dynamic moving from a 5 to a 100 start-up portfolio: the median return moves up dramatically from 4.4% to 23%, the spread of returns gets reduced from a 180% spread to a 75% spread, and the entire set of returns moves up.

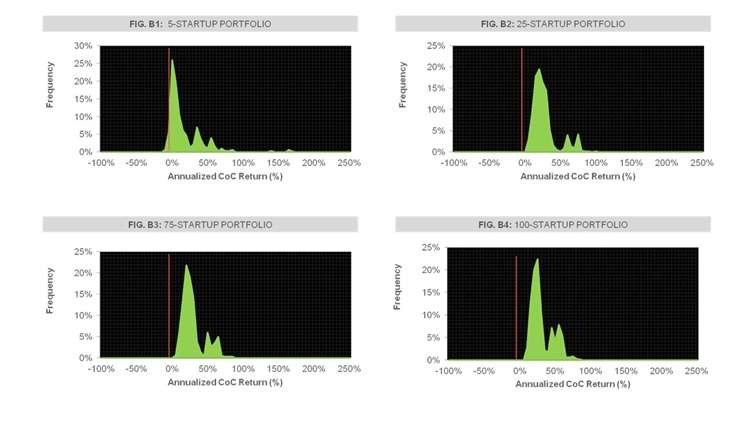

The return histograms give us an even more sophisticated perspective:

We see how the distribution for the smallest portfolio (Fig. B1) stretches far across the spectrum, indicating a high level of risk. The distribution peak is frighteningly close to the 0% return mark, and a significant portion of returns are negative. Going up to 25 (Fig. B2), 75 (Fig. B3) and 100 (Fig. B4) start-ups in each portfolio, we see how the distributions get narrower, indicating a lower spread and risk, and how both peak and larger share of distributions move away from the 0% return mark into higher yield territory.

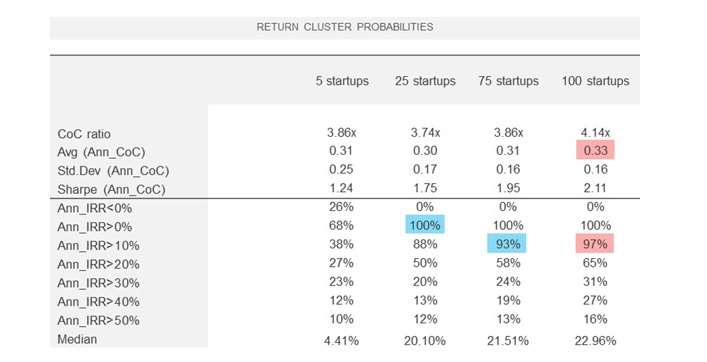

Taking a look at the numbers (Fig. C), we see that the annualized average cash-on-cash (CoC) returns remain pretty stable across all portfolios at a high 30% - 33% yield; but the “Risk of <0%”, representing a portfolio loss, changes dramatically. At 5 startups, our portfolio has a 26% chance of losing money; at 100 start-ups, this chance is reduced to 0%, with a 97% probability of achieving more than 10%, and a 65% chance of exceeding 20% p.a. Measured in standard deviation, risk for this portfolio is at 16%– a fifth lower than that of the S&P 500.

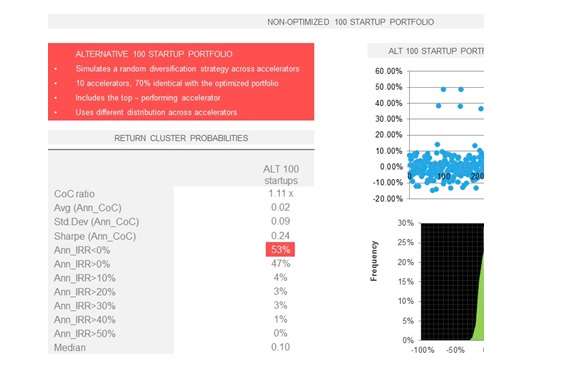

So does this simply prove “spray and pray” – randomly investing in a lot of seed stage start-ups – is an effective investment strategy? Absolutely not. The next experiment shows what happens if we use a less refined portfolio design across similar sources, but keep the portfolio size at 100 start-ups.

The results are a far cry from our optimized portfolio, and resemble traditional venture capital performance. It returns roughly 0% per year at a 53%

chance of loss, a median of 0.1%, and a poor 4% chance of making more than 10% per year (Fig. D).

Structured Optimization Achieves A Superior Risk/Return Profile

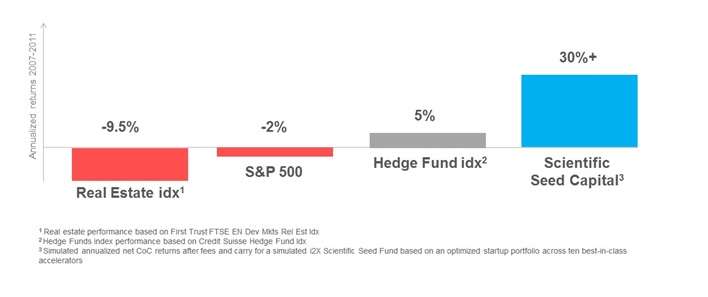

These simulations, in combination with many others we have run, lead to one conclusion: Structured Seed Capital is a game-changer for venture capital. By optimizing VC investing around seed stage portfolios rather than individual companies, empirical evidence shows that we could massively outperform every major asset class by an order of magnitudes (Fig. E).

This is great news for capital markets, but also for startups. Structured Seed Capital changes the fundraising process for entrepreneurs dramatically: by deploying capital into clusters of startups, entrepreneurs become liberated from the endless meetings, unsolicited advice and cronyism that makes raising seed capital the business risk it is today. If seed stage startups indeed spend over 80% of their time fundraising, Structured Seed Capital could accelerate the pace of innovation between accelerators and the first VC (Series A) investment round five-fold.

For Structured Seed Funds, the removal of costly deal sourcing and due diligence would leave vastly bigger budgets to support their portfolio start-ups, making them not just faster, but also more effective seed investors.

But does this approach only work within the limited framework of our current accelerators - or can it unlock innovation on a more massive scale? To answer this question, we have to take a deeper look into the logic of seed stage acceleration, and the macro-trends surrounding it.

John Bhakdi is founder and CEO of i2X. He previously served as an executive in some of the largest Omnicom and WPP companies (S&F, JWT, BBDO, DDB) where he shaped corporate development, M&A and innovation activities as Strategy and Executive Director. During his career, John worked closely together with both entrepreneurs and C-level executives in companies such as MasterCard, Siemens, Sinopec, Ford Motor Group, Dow Jones, Microsoft, The Ritz Carlton, Mercedes Benz, Deutsche Bank and Credit Suisse. In 2008, he decided to become an entrepreneur himself and moved to Silicon Valley which later led to the founding of i2X. Email John at jb@i2x.co.

i2X is a structured seed investment framework that allows institutional investors to capture large clusters of seed stage start-ups at a superior risk/return performance. The i2X framework has been developed with the input from partners at top 10 Venture Capital firms, The White House’s Startup America Partnership, some of the top 25 alternative asset management firms and a large network of technology entrepreneurs and accelerator teams.