By Andrew Smith, CAIA

Institutional investors are significantly increasing their allocations to real assets. What do they know that the broad investor pubic does not? How are they utilizing real assets to protect the value of their portfolios in downturns and to increase growth in bull markets? In this article, we answer these questions as well as discuss the numerous benefits, as well as the risks, of real asset investing.

What are Real Assets?

Real assets cover a broad range of tangible, and some intangible, hard assets. Basically, real assets are non-financial assets, in that investors in real assets purchase the physical asset itself as opposed to financial contracts that entitle the investor to said assets (equity shares or debt notes/bonds). Real assets, according to the Chartered Alternative Investment Analyst (CAIA) Association include Real Estate/Land Equity & Debt, Infrastructure, Farmland, Timberland, Mining Land/Rights, Physical Commodities and Intellectual Property (Copyrights, Trademarks, Patents, Trade Secrets, etc.). Other investors may also include assets such as Inflation Protected Securities as real assets, however for the sake of this article we will focus on the physical.

While there are unique benefits and risks to each real asset subcategory, generally speaking, real assets as an asset class carry very similar benefits and risks across the sub-categories. These benefits, are the primary reason institutional investors are significantly increasing their allocation to real assets, and are doing so with an extremely long-term time horizon. However, investors should also carefully consider and fully understand the risks associated with gaining exposure to real assets.

What are the Benefits of Real Assets?

Diversification

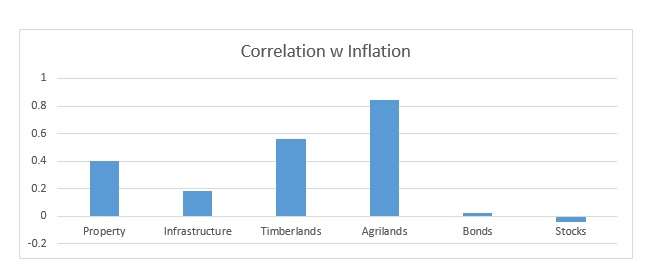

Real assets returns have very low, if not negative correlation to traditional public equity investment returns, providing investors with significant diversification benefits. Further, real assets provide investors exposure to a different stage of the economic cycle. Including real assets as part of a diversified portfolio of stocks, bonds and alternatives allows investors to minimize losses during market downturns, while maintaining exposure to market upside during bull markets.

Inflation Hedging

Real assets have proven to be the best way to hedge against both expected and unexpected inflation. Real assets are inputs into many end consumer products. The price that one can sell real assets, or in the case of income producing real assets, the income generated from leasing/operating these assets, typically rise prior to prices on consumer products rising. Real asset price and income appreciation is often a leading indicator of inflation. The value appreciation combined with the income appreciation provides investors among the best inflation hedges, and allows investors to preserve their capital, grow their wealth, and prevent inflation from eating away at their purchasing power.

Sources: 4; 5; 6; 7; 8; 9

Value Appreciation

Real assets are scarce by nature because they are physical assets that have a finite, limited supply. However, as global population grows and demand for these assets increases, the supply is not necessarily able to increase, or in some cases, the supply available to purchase, is not necessarily able to increase fast enough to meet the demand. The result is an increase in the value of real assets, leading to a substantial monetary gain for the investor, often outperforming the returns of traditional equity and debt investments.

Sources: 4; 5; 6; 7; 8

Stable Income

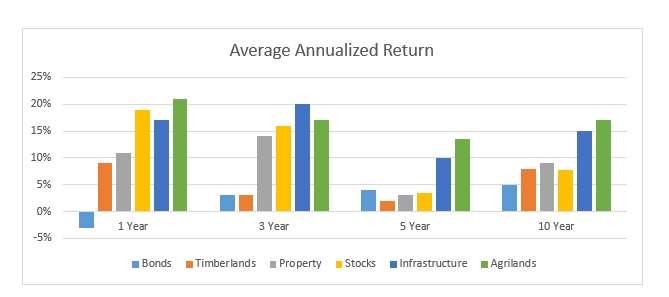

Real assets often throw off significant and very stable cash flow to investors, most often in a very tax efficient manner. This income fits the goals of many investors, particularly institutional investors and individuals that are approaching, entering, or are in retirement. Stable income combined with price appreciation is a highly desirable trait for investments.

According to Michael Underhill, the Chief Investment Officer of Capital Innovations, a leader in real asset fund management, infrastructure plays in particular will continue to provide strong income. In an article written for Daily Alts in which he discusses the current yield of MLPs despite falling oil prices, Michael Underhill said “we expect almost all midstream MLPs under coverage will not need to slash distributions”. Underhill also indicates in the same and other articles that he believes REITs, Agriculture lands and Timberlands will also continue to offer stable income.1, 2

Inelastic Demand

Real assets provide exposure to assets or outputs from assets that have an inelastic demand. For example, real estate; people need places to live and businesses need office space. Another example is farmland; farmland produces food and food is necessary to life. This stable and increasing demand provides investors a very predictable income stream, easily predictable risk, and value appreciation.

Long-Term Holding Period

Many real asset investments have very long-term investment horizons. Investors can benefit from a no-nonsense buy and hold strategy where they “clip coupons”, capturing income and watching the value of their portfolio increase over a long period of time without worries of when to buy or when to sell.

Global Exposure & International Opportunities

Real asset investments as a category are generally not “domestic” by nature. Typically, real asset investments provide investors exposure to global economic and population growth. As population grows, and as economies globally develop or update their infrastructure, demand for real assets increases. To this point, in a white paper written for BNY Mellon, Underhill states that investors increasingly demand “real asset investments as a means to capitalize on demand generated as a result of explosive population growth in emerging markets.”3

Assets that produce food, energy, metals, etc. produce these commodities for the highest bidder, not solely their own locality or country. Despite the fact that many of the markets for the commodities produced on or by real assets are global, they are often priced in US Dollars. This allows investors to gain exposure to international opportunities without taking the currency risk.

What are the Risks Associated with an Investment in Real Assets?

Economic Downturns

Real assets are often the first to be affected by both economic growth and contraction. A downturn in the global economy, or a large developed country, could affect both the income produced by and the value of real asset investments. Some real assets, however, such as farmland are often considered a “disaster hedge” by many investors and increase in value as economies struggle. Exposure to economic downturns, as an asset class, is fairly strong. However investors considering a specific real asset investment should consider the risks of that specific asset alone, and as a part of a diversified portfolio.

Political Risks

Commodities, and assets that produce or are vital to producing such commodities, particularly internationally, are often subject to regulations and potentially, in some countries, nationalization. In the US, during World I the US Government nationalized railroads, during WWII it was coal, during the Korean War the steel industry was subjected to government control. In some cases, particularly during war, other industries deemed vital to the US economy or military efforts have been nationalized, or partially nationalized. If an investor owns vital infrastructure required for energy or water transportation or storage, such facilities could become subject to nationalization, particularly in countries other than the US, and investors could lose their entire investment in this scenario.

Other political risks real asset investors could face include environmentalist pressures, particularly in the energy and timber industries. These pressures could lead to regulatory requirements that impose costs on producing the commodities the investment targets. This has the potential to make the operation of the assets unprofitable, as with coal mines over the past decade. The risks of each specific subcategory, and further, each individual asset should be considered very carefully, as even within the US, States have different political pressures that could add or minimize political risks.

Weather-related Risks

When investing in real assets such as farmland, timberland, mining operations, and in some cases real estate, weather risks need to be considered, and likely insured. A bad storm, a bad drought, or other natural disasters, such as earthquakes or volcanic events, could lead to total losses of a crop, a piece of real estate or a mine. These risks are real, and must be considered, particularly since real asset investments are often very long-term. For example, even weather/nature events that are thought to be unlikely could potentially occur. Take investors in real estate along the New Jersey Shoreline that were ravished by Hurricane “Super Storm” Sandy.

How does an Investor Gain Exposure to Real Assets?

Depending on the sophistication and amount of capital that an investor has to deploy, there are many different options for investors seeking exposure to real assets. Everything from private investment funds & clubs to publicly traded funds and operating companies. Different structures carry different risk/return profiles, however, more often than not they offer similar asset class exposure. Building a diversified portfolio that includes real assets in some form or another allows investors to benefit from the diversification, value appreciation, stable income, global exposure, and hedge against inflation. Below readers can learn about most of the structures currently available to investors seeking real asset exposure.

Private Investment Funds

Private investment funds are exclusively offered to accredited investors, with the funds managed by the best managers only accessible by large institutions due to high minimum investments. Private real asset investment funds often have lock-up periods of 7-15 years with no liquidity, other than cash flows distributed by the fund manager. There are private real asset investment funds that broadly expose investors to real assets, as well as funds that offer exposure to a specific subcategories of real assets.

Private Investment Groups

Private investment groups often called investor clubs come in different shapes or sizes. Private investment groups focused on real assets typically invest in oil and gas partnerships or residential and/or commercial real estate. These organizations often have closed doors, are invite only, and are typically composed of high net worth, or ultra-high net worth investors that have known each other for a while.

Separately Managed Accounts

Separately managed accounts (SMAs) are exactly what they sound like, separate accounts managed by professional managers. SMAs are typically only accessible to institutional investors and ultra-high net worth individuals, with minimum investments of $10million or larger. There are separately managed accounts that broadly invest in real assets, as well as SMAs that provide investors to a specific subcategory of real assets.

Direct Investments

Direct investments are very common among real asset investors, particularly in real estate, farmland and timberland, as well as in physical commodities . Direct investments are accessible to anyone with the capital to make a down payment and the credit/income requirements to borrow money to finance the purchase of the asset. Direct investments are typically lumpy, in that they cannot be made in small increments, and often are illiquid.

Publicly Offered Securities

Publicly offered securities are highly accessible by anyone with enough capital to purchase one share of the security. Some of these offerings are made on the secondary market (on stock exchanges) others are solely through broker/dealer platforms. Typically these investments have intra-day or daily liquidity and daily transparency (in some cases monthly or quarterly liquidity and transparency). Publicly offered securities may offer exposure broadly to real assets, however in many cases they are more focused on a specific subcategory within the real asset classes.

Public REITs

Real Estate Investment Trusts provide investors exposure to real estate equity and/or debt in a liquid, exchange traded format. Typically REITs invest in commercial real estate, but residential real estate, farmland, timberland and other land investments are available through REITs as well.

Public MLPs

Master Limited Partnerships are energy and natural resource focused funds, often providing investors exposure to vital infrastructure such as oil and gas pipelines, refineries, natural resource storage facilities, etc. However, there are also “exploration & production” MLPs that invest in the actual harvesting and mining of natural resources.

Public Operating Companies

There are many companies that are publicly traded that operate real assets, for example real estate, farming operations, timber operations, real estate development, mining, or infrastructure management.. Investors can gain exposure to these companies by buying shares on stock exchanges. However many real asset investors consider this a non-pure play as it is more a bet on management than the asset itself.

Exchange Listed Commodity Futures

If an investor is seeking exposure to commodities, rather than directly investing in the physical commodity and having to store it, they may opt to buy, hold and roll commodity futures contracts that trade on one of the futures exchanges.

Public Closed End Funds

Closed end funds are non-redeemable registered investment companies (RICs), meaning the manager issues shares and invests the proceeds according to their strategy. From that point forward, buyers and sellers only buy or sell shares on the secondary market without the ability to redeem shares. This often results in the fund’s market price being higher (premium) or lower (discounted) than the net asset value. Public closed end funds that invest in real assets may invest broadly in real assets, but more likely invest in a specific sub category of real assets.

Mutual Funds

There are mutual funds that invest broadly in real assets, as well as mutual funds that specifically invest in one or a couple subcategories of real assets.

ETFs

There are very few real asset ETF opportunities other than commodity, REIT, and MLP ETFs. However, market research indicates that there is significant interest among some managers in launching real asset ETFs that focus on other subcategories of the real asset class, as well as ETFs that invest broadly in real assets, across various sub categories.

Sources:

1 http://dailyalts.com/author/munderhill/

3 http://www.adrbnymellon.com/files/PB38782.pdf

4 MSCI

5 Barclays

6 Bloomberg

7 NCREIF

8 S&P Dow Jones Indexes

9 US Bureau of Labor Statistics

10 http://www.nytimes.com/2008/10/13/business/worldbusiness/13iht-nationalize.4.16915416.html?_r=0

Andrew N. Smith, CAIA is a Co-Founder and Chief Product Strategist for OWLshares and serves as the chairperson of the Steering Committee for the Los Angeles Chapter of the CAIA Association.