By Aaron Filbeck, CFA, CAIA, CIPM, Associate Director, Content Development at CAIA Association, and Keith Black, PhD, CFA, CAIA, FDP, Managing Director, Content Strategy at CAIA Association

“Diversification is back” – now that’s not a phrase we’ve heard in a long time…long time. Considering recent market performance, we thought that now is a good time to remind ourselves of the benefits of diversifying and rebalancing portfolios. We’ll save you the quotes about blood on the streets or having a plan until you get punched in the face, but having a sound investment process and strong portfolio construction can allow you to weather the storm a little bit better. In this post, we want to discuss two important portfolio management concepts: diversification and the art of rebalancing.

Diversification

Let’s start with the importance of diversification. We talk a lot about correlations, alphas, and betas in the portfolio construction process, and it’s nice to put together the puzzle pieces of multi-asset class portfolios. Diversification is meant to smooth out the (upward) trending line that represents growth of capital, but it should also mitigate other risks like concentration to different risk premia and, perhaps more importantly, reduce tail risk.

Exposure—Bringing Balance to the Portfolio

Exposure to alternative asset classes provide investors with alternative sources of “beta” in their allocations. Alternative betas can increase diversification, which can have a pronounced effect on total portfolio volatility. Having allocations to real assets, private credit, and private equity introduce alternative economic return and risk drivers into the portfolio, thereby reducing the contribution of equity risk to total portfolio risk, which tends to dominate most traditional portfolios.

In previous pieces, we have written about some of the considerations an investor should know before investing in alternative investments, namely return smoothing due to infrequent pricing of illiquid assets and return dispersion of manager performance. In other words, your eyes can deceive you—don’t trust them. In periods of drawdown, however, holding illiquid asset classes might actually provide some behavioral benefits to an investor with a long time horizon.

We are all tempted to sell assets during times of crisis. Being in a lock-up period, whether it is 10 years for private equity or real estate or even one year for hedge funds, prevents us from easily liquidating assets during a time of crisis. While investors in 2008 and 2009 were upset about gates preventing withdrawals from fixed-income and relative value hedge funds, it was absolutely the right thing for the hedge funds to do. Later in 2009 and 2010, the gates were justified when investors were able to withdraw their assets at valuations billions of dollars higher than if they forced the liquidations at the depth of the crisis.

Tail Risk—The Ultimate Path to the Dark Side

Alternative strategies, namely hedge funds, can provide investors with strong drawdown protection. Hedge funds have been an unpopular asset class as equity markets have gone straight up and the value proposition of hedge funds haven’t been needed. As we enter bear market territory, this view may begin to change. Depending on the strategy, hedge fund managers can short individual securities or entire markets, meaning hedge fund strategies can be positive in broader equity drawdowns.

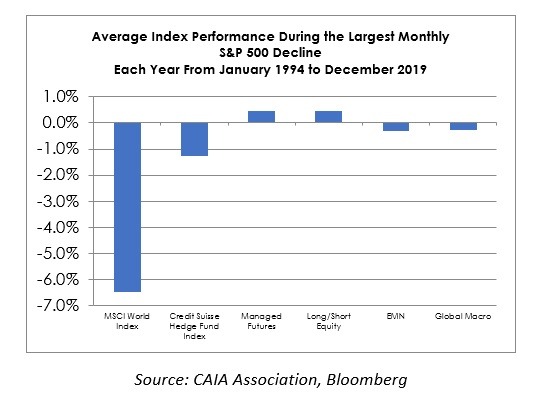

In the exhibit below, we show the average performance of hedge fund strategies relative to the worst monthly drawdown of each calendar year from 1994 to 2019.

Historically, most hedge fund indices have protected investor capital in difficult markets, either by losing less or generating positive returns. Managed futures strategies, for example, have historically generated positive returns in periods of equity drawdowns due to their ability to systematically take short positions as markets fall.

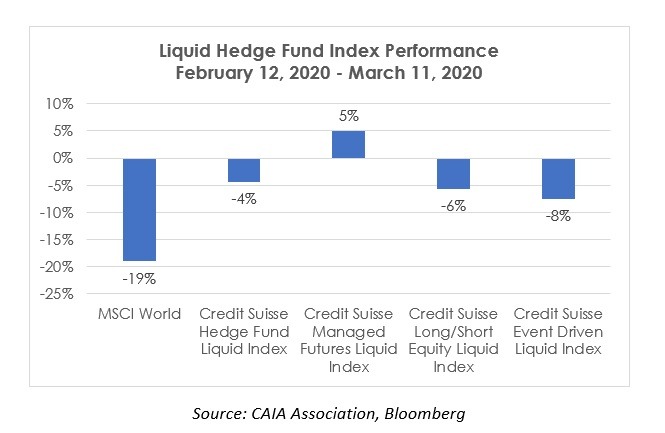

While this chart displays performance figures over the past 25 years, we wanted to obtain some idea of recent performance figures. Given the shorter time horizon, we were unable to use Credit Suisse’s hedge fund indices, and instead opted for their Liquid Indexes as a proxy (Credit Suisse Liquid Indices are designed to replicate hedge fund performance risk and return). We examine performance from Feb. 12, 2020, the peak for the MSCI World Index, through March 11, 2020.

Even in this drawdown period, the graph above shows that hedge funds have held up very well, with managed futures generating positive returns. The other strategies posted losses, but the magnitude of those losses is far less than that of the global stock market. While short-term performance doesn’t make for a longer term trend, it does bring forth the original value proposition of most hedge funds—to hedge.

The Art of Rebalancing—Do, or Do Not—There Is No Try

A diversified portfolio should also be rebalanced on a regular basis. Especially for investors with heavy public equity allocations that have continuously increased in value, rebalancing can seem painful, at least at the time. The goal of a strategic asset allocation is to generate long-term returns at a desired level of long-term risk, not to have a 10-year plan and suddenly liquidate assets in the third year. Part of this plan should be to regularly rebalance back to strategic asset allocation weights.

Consider an investor with a $100 million portfolio in October 2019. The portfolio’s target weights are 50% U.S. stocks, 30% 10-Year Treasuries, and 20% in alternative investments. Let’s assume the investor chooses not to rebalance or liquidate any of our alternative investments in this exercise but will rebalance their stocks and bonds allocations.

The S&P 500 moved from below 2,900 in October 2019 to more than 3,300 in February 2020, an increase exceeding 14% in just five months. Over the same time period, the 10-year US Treasury yield moved from 1.7% to 1.6%, meaning that stocks outperformed bonds by about 13%.

To rebalance, the investor sells 5% of their equity portfolio at 3,300 and reinvests the proceeds into 10-Year Treasuries at a 1.6% yield. Rebalancing typically happens infrequently, such as on an annual basis or whenever relative returns across asset classes move in excess of 10%, which can often take more than one year. It is not often that the benefit of rebalancing can be seen so quickly.

In this example we started with $50 million in stocks at $30 million in bonds. The traditional portion of the portfolio was worth more than $87 million in late February before the investor rebalanced the portfolio back to its strategic weights.

This quick bear market allowed for a second rebalancing opportunity on March 11, when the 10-year Treasury yielded 0.87% and the S&P 500 had fallen to 2,740. After the decline in stocks and the rise in bonds, the investor performs the opposite rebalancing action in March, buying stocks and selling bonds.

Note that the stocks the investor buys at 2,740 are the same ones they sold three weeks prior at 3,300 and the bonds the investor sells have fallen in yield from 1.6% to 0.87%. With rebalancing, the investor’s traditional portfolio on March 11 is valued at $83 million—$800,000 more than if they were a buy-and-hold investor, letting their allocation drift away from their strategic asset allocation weights.

Simply rebalancing increases the investor’s return from 2.6% to 3.8% since October. Of course, rebalancing adds value during volatile markets and detracts value during trending markets. Even if the investor missed the chance to sell in February, perhaps they would take this chance to rebalance in March.

Putting It All Together

Investing takes discipline, and navigating markets is tough. It has taken some time, but diversification may finally be striking back. Diversification can further be enhanced by following a disciplined rebalancing process that hardly involves timing the market. When the other investors start to “have a bad feeling about this,” take comfort in that discipline.

Aaron Filbeck, CFA, CAIA, CIPM is Associate Director, Content Development at CAIA Association. You can follow him on Twitter and LinkedIn.

Keith Black, PhD, CFA, CAIA, FDP, is Managing Director, Content Strategy at CAIA Association. You can follow him on Twitter and LinkedIn.