Christopher M. Schelling, CAIA, Director of Alternative Investments for Venturi Wealth Management.

Alpha versus beta is the single biggest debate in all of investing. Does it make more sense to simply passively accept the market return, or is it worth it to actively select a subset of assets within a market in an attempt at beating the benchmark?

True believers on both sides passionately defend their arguments.

The efficient markets proponents, like Nobel Prize winning Economists Burton Malkiel and Eugene Fama, argue that consistently beating a benchmark is impossible. With enough informed participants in a market, all information will be reflected in prices, making persistent outperformance impossible. And their research seemed to back it up; any excess returns found historically in stocks disappeared quickly, statistically looking quite similar to luck.

On the other hand, a small group of investors also seemed to consistently outperform their respective markets dramatically for longer periods of time than could be attributable solely to chance alone, luminaries like Warren Buffet and Bill Gross. Perhaps the most extreme example is that of the Capital Group’s Investment Company of America. Since its launch in 1934 by founder Jonathan Bell Lovelace, this large cap stock fund has outperformed the S&P 500 by roughly 100 basis points annually, although that number has declined in recent years.

But what if both sides are both right?

In one of history’s great ironies, it was the godfather of efficient markets theory – Eugene Fama himself – who proved the existence of statistical factors associated with predictable excess returns. It turns out that what these investment gurus were doing wasn’t buying assets that exactly mirrored the broader market, but they were purchasing securities with features that predictably lead to higher returns, like stocks at discounted prices or bonds with higher yields.

So, in some ways, Professor Fama simultaneously proved his theory correct and incorrect. While it is very hard to beat a market per se, it is indeed possible to find a slightly better market to buy.

And over time, thousands of asset management products have emerged to do just that, creating rules-based strategies that provide access to value tilted equities, or low volatility portfolios, or systematic trend following, or even merger arbitrage replication. The rules of these games are now broadly known, easy to mimic, and via the availability of liquid alternatives or alternative risk premia strategies – a $300 billion marketplace – are widely accessible to most investors.

Of course, during this same time, as both the amount of academic research on various factors and the number of competitive offerings around previously inaccessible strategies exploded, the excess returns which these risk premia previously offered has begun to disappear. This is how what once looked like alpha evolves – or perhaps devolves – inevitably into beta over time.

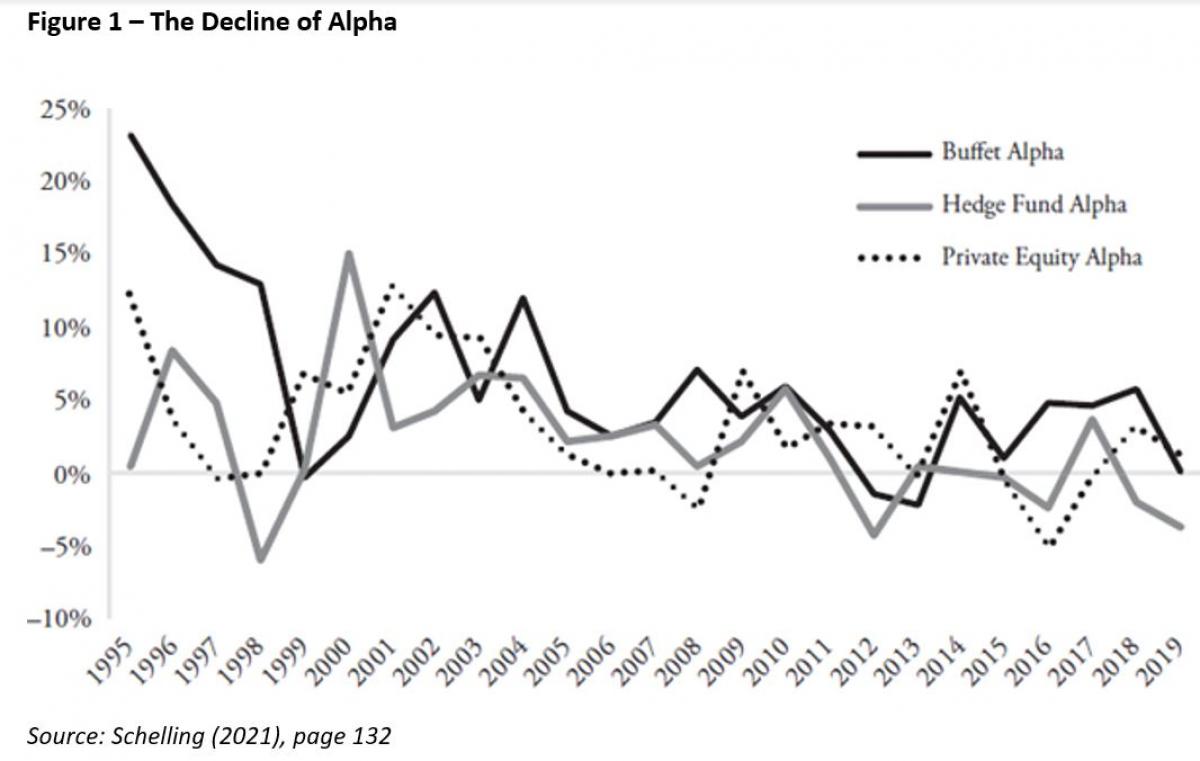

Even the rock stars of the alternative investment community have not been immune to this effect. Since 1995, the average excess return to the average hedge fund, private equity, and even Warren Buffet himself have effectively declined to zero.

When the rules become known, the market becomes pretty efficient.

And if that is the case, it suggests other logical inferences, namely, that market efficiency is neither a homogenous nor a static characteristic of financial assets. Not all markets are the same. Some are heavily overcapitalized, some are not. Some are widely followed, others less so. It stands to reason that if asset classes are stratified and style-boxed inputs into the investing architecture, then asset class efficiency must be a stratified output of market behavior.

Put another way, if efficiency is the result of competitive price discovery of informed market participants, then those markets with more information and more participants relative to the opportunity set should be far more efficient than those with less of either.

For instance, let’s compare two hypothetical markets. Imagine one with 1,000 investments, but over a million individuals engaged in active price discovery, and real-time access to virtually unlimited information on the assets for all market participants.

Now, compare this with a different market with 200,000 unique assets, perhaps 40,000 professional market participants, and massive asymmetry in the availability of investment information.

Even though both of these represent markets for stocks of corporations with revenues between $10 and $100 million – the first, public small caps[i] and the second, privately owned businesses[ii] – it would strain credulity to suggest that two such disparate markets would be equally efficient.

And of course, they are not. The spread between top and bottom quartile managers in small cap stocks is only 2% to 3% typically[iii], whereas the same for small market private equity funds is nearly 20%[iv].

It is probably easier to generate excess returns in the latter than it is in the former, but that still doesn’t make it alpha. What you get is still the same drivers of return – value and growth – that you find in the public markets; the reduced competition and information accessibility means there is simply more of it laying around to pick up.

It’s analogous to competing in two different games that I am roughly equally good (or bad, depending upon your perspective) at – chess and checkers. I can envision a scenario where I will almost certainly lose every game of chess and win every game of checkers, and that’s if I play chess versus the University of Texas Chess Club and checkers with my son’s sixth grade classmates.

But playing an easier game doesn’t mean I’m any smarter. And worse, it won’t be long before those kids have learned all my tricks, and my ability to consistently win is no more.

It seems to me that’s sort of what we are doing when we focus on beating a benchmark. Gaming an index or just putting more risk into the portfolio isn’t alpha at all, even if we’d like to tell ourselves it is. I think chasing this benchmark-linked version of alpha has been a fool’s errand for most, a complete waste of investment time and resources.

Instead, investors would be better served with a new framework for thinking about alpha, because beating a benchmark doesn’t help achieve investment objectives. By starting with our investment objectives first and foremost, we can reframe alpha as making investment decisions which increase the probability of meeting or exceeding our required return objectives. But let me explain a little more.

Investment success isn’t beating a benchmark; it is meeting a required rate of return, like the 7.0% target for a pension or endowment, or the return required in a 401(k) to allow someone to retire at a certain age. So, if success is meeting or exceeding this cost of capital, failure is simply not hitting your bogey, regardless of what indices do. If you don’t generate enough from the returns, you have to save more, work longer, or spend less. The financial picture can still be fixed, but the investments didn’t do their job.

By extension then, investment risk can clearly be redefined as the ex-ante probability of failure, or 1 minus the probability of success. This represents an important philosophical shift.

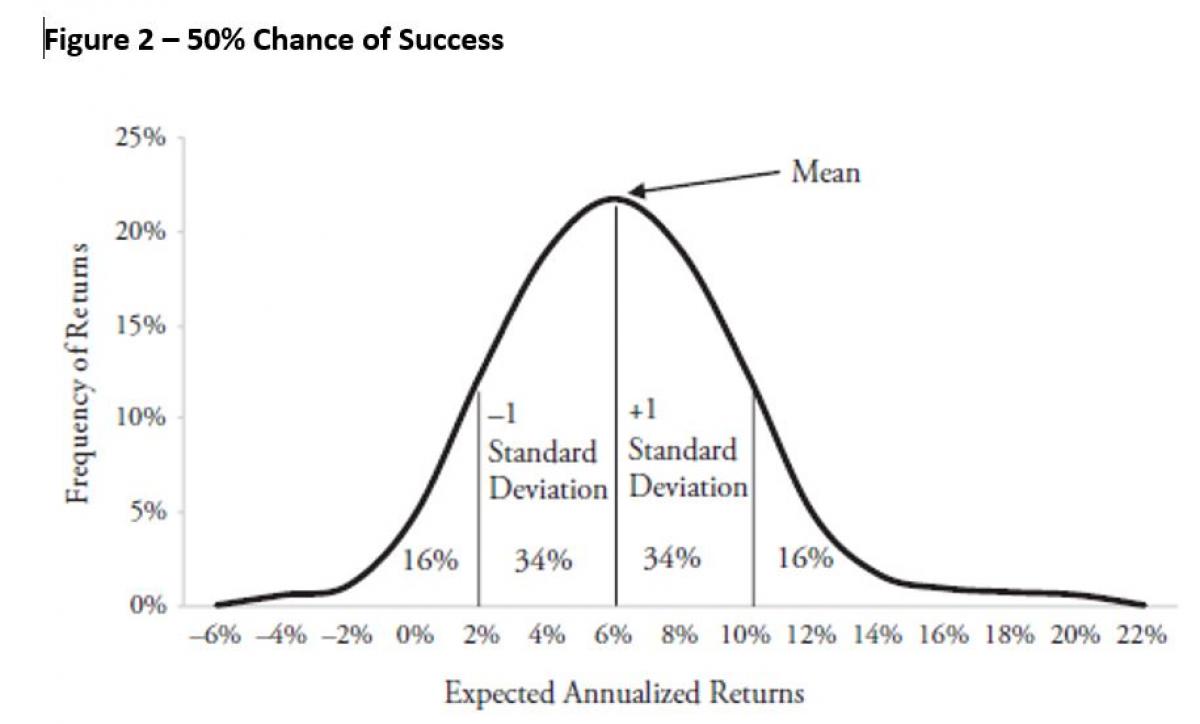

If we think in the context of building a portfolio, using the classical Mean-Variance Optimization framework, risk was always assumed to be the volatility of returns. But to long term investors, this isn’t the same as risk of investment failure. Figure 2 below presents a roughly normal distribution with a mean expected return of 6% and a volatility of approximately 10%. Translated into a probability distribution, roughly half the expected returns fall above the mean and half below. I’m not exactly sure how we ever accepted 50/50 odds of a success as a strategic plan, but this is the standard in the industry.

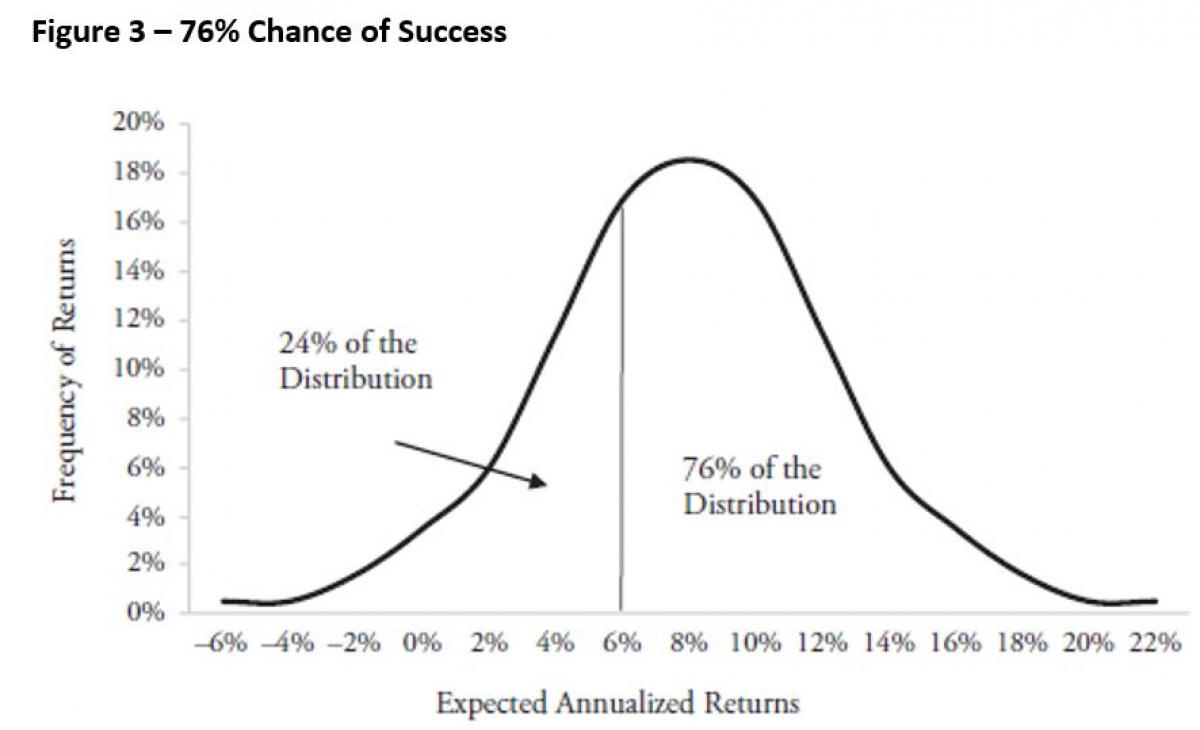

In the new alpha framework, alpha doesn’t mean beating some index; it means increasing the odds of success. In Figure 3 below, we have an expected return distribution with a mean over 8%, and a volatility of nearly 12%. In an MVO framework, an investor would avoid this, as it means accepting more volatility. However, on an ex ante basis, only 24% of the expected return distribution falls below the required 6% rate of return. Doesn’t that mean this has a higher probability of success due to that margin of safety? Isn’t it thus a less risky portfolio?

Of course, calculating these probabilities is not a perfect science, nor is simply pushing up a return distribution. But focusing on decreasing the total cumulative probability of not hitting your required rate of return is a far more intuitive and practical way to think about actual risk than how wide the standard deviation is. Even better, modeling such portfolios will help investors investigate how much exposure – to equities, to volatility, or to illiquidity – they need to accept in order to more realistically hit their required rate of return.

Of course, this inverts the order of operations, and will lead investors down many uncomfortable paths, such as suggesting more equity risk or illiquidity than most might otherwise desire or pointing towards new asset classes and difficult to benchmark, niche investment strategies.

However, I think the benchmark-linked vision of alpha has failed in part because we have focused heavily on mathematical alpha – beta separation, allocating time to more efficient asset classes while at the same time, avoiding assets that are probably more attractive precisely because the rules of the game are not yet known.

Ultimately, I believe improving our investment decision making based upon evidence-based processes can increase the probability of outperforming our required investment returns, a more durable form of alpha. I call these three processes Behavioral Alpha, Process Alpha, and Governance Alpha.

- Behavioral Alpha – Behavioral Alpha is Smart Thinking. Pulling from Daniel Kahneman’s System 2 thinking, Behavioral Alpha requires focusing active investment decisions on only on the biggest and most important factors in investment success. System 2 is deliberate and rational thinking, and it requires significant mental effort, which means it is a limited resource. Behavioral Alpha necessitates making fewer – far fewer – but bigger decisions, and doing so deliberately and intentionally in order to allocate investment resources, both time and money, to only the most important levers. Although deciding which asset classes to focus on, how much of them to own, and how to effectively execute and implement them drives the vast majority of investment outcomes, these efforts could generally be improved by slowing down the decisions and doing even deeper thinking on them. Once those decisions are made – once the investment principals are in place – limited System 2 resources should be spent on automating as much of the day-to-day investment work as possible, which is where Process Alpha comes into play.

- Process Alpha – Process Alpha, or Smart Habits, means systematizing as much of the investment decision making process as possible to take emotions – and mistakes – out of the equation. Once the big, important decisions have been made, System 1 thinking – or quick, heuristic decision making in Kahneman’s framework – will take over, whether we want it to or not. It’s how we make 90% or more of the decisions we are confronted with on a day-to-day basis, and it is not exactly perfectly rational. Automating and standardizing much of the investment work – such as through using checklists and workflow processes – reduces the incidence of numerous investment biases and errors, and ultimately improves performance. Think of Process Alpha as building investment assembly lines; it is the rules used to implement the principals above. However, since markets evolve, these rules also must learn. Sometimes, investment strategies that used to work suddenly stop working, like value investing or many hedge fund strategies. A completely static process, one devoid of any outcome consideration, is destined to fail. Smart Habits are about implementing processes with disciplined monitoring and measuring feedback inputs in place in order to balance the discipline of a consistent process with the gradual evolution and adaptation needed to survive in the long run. Smart Habits are evidence-based, learning processes committed to continual improvement. But these don’t exist in a vacuum; any process is only as good as the people managing it.

- Organizational Alpha – Organizational Alpha is Smart Governance; it is putting the right people in the right positions to make the right decisions. Whereas the first two processes help us control our own behavioral tendencies and improve our individual investment decision making, Organizational Alpha is the institutional equivalent. It is removing internal bureaucracies, perverse incentives, and problems of agency that come along with unintentionally designed decision-making structures. Optimizing all of the important investment levers requires intelligently designing an investment architecture with consideration to the level of internal resources, and relevant skills and experiences, as well as legal or regulatory constraints, and how these interact with the institution’s investment objectives, time horizons, and cash flow needs. There is no one size fits all governance, but there are certainly structures which objectively work better (or worse) for certain types of investments and portfolios. For instance, no organization with a single investment person should be trying to select alternative investments in-house. Tools like a skills/responsibilities matrix can provide a rational framework for not only deciding who should own what parts of the investment process, but what investment levers the organization should realistically be trying to pull.

By improving all the little decisions along the way where costs leak out, biases creep in, and

underperformance results, investors can still increase their odds of outperformance. In the old benchmark-linked, security selection paradigm, alpha was a zero-sum game. For every investor who found alpha, there had to be someone who gave it up. In the new paradigm of alpha, meaning improving the odds of investment success, there is not a fixed pool of collective odds, where market participants must take from the probability distribution of others to improve their own outcomes.

Excess returns can still be found relative to our required returns, but those excess returns must come from predictable drivers of return, like income and capital appreciation. But in truth, that’s all it’s ever been. There probably never was any investor with the Midas touch, any true superior ability to select securities absent other factor tilts. It’s always been about intelligently accessing factors in various quantities to hit return targets. Outperforming your underwriting should be the goal of the exercise. That’s a margin of safety; that’s alpha.

The final chapter of alpha has certainly yet to be written. The research around precisely how to best meet our investment objectives will undoubtedly change going forward, but that’s what makes investing such an intellectually stimulating endeavor. Keeping a completely open mind, implementing a scientific approach that couples fundamental theories with empirical research, all the while acknowledging investing is a probabilistic, not deterministic, activity will allow us to make better decisions in the future.

Learning requires that we remain open to change, and change brings the potential for mistakes. But the reality is, no one bats a thousand in investing. Perfect is not attainable, but better always is. Now more than ever, institutional investors must be willing to embrace change and be open to mistakes, as long as they are not fatal ones. Small mistakes are the best source of learning.

In fact, I can’t wait to find out what works next, and unlearn that which no longer does! Perhaps that’s real alpha. Come to think of it, maybe that’s not alpha at all, but it’s better than alpha.

References

Schelling, Christopher, Better than Alpha: Three Steps to Capturing Excess Returns in a Changing World, McGraw-Hill, New York, NY, 2021

[i] According to information from S&P and Greenwich Associates

[ii] According to information from Pitchbook and Preqin

[iii] According to information from eVestment

[iv] According to information from Burgiss

About the Author

Christopher M. Schelling is the Director of Alternative Investments for Venturi Wealth Management. Chris is focused on sourcing, performing due diligence, and building portfolios of alternative investments for clients. As an institutional investor, Chris has invested roughly $5 billion and met with over 3,000 managers across hedge funds, real assets, private credit, and private equity in his career.

Previously, Chris was a managing director at Windmuehle Funds, a boutique investment firm, leading sourcing and structuring for niche alternative investments. Prior to this, Chris was the Director of Private Equity at the $30 billion Texas Municipal Retirement System, and before that, the Deputy Chief Investment Officer and Director of Absolute Return at the $15 billion Kentucky Retirement Systems. Chris has over 20 years of experience in the investment industry, nearly all focused on alternatives.

Chris is currently a contributing columnist for Institutional Investor and has authored over 60 articles on investing. He is also the author of Better than Alpha: Three Steps to Capturing Excess Returns in a Changing World.