By Aaron Filbeck, CFA, CAIA, CIPM, FDP, Director of Global Content Development, CAIA Association

A machine learning algorithm walks into a bar.

The bartender says, “What’ll you have?”

The algorithm says, “What’s everyone else having?”

Machines can sift through higher volumes of data at a far faster rate than humans can, potentially generating insights that escape us completely. The degree to which humans remain involved in that process depends on the strategy being used. I believe there is a balance—machines and algorithms are designed to win in the world that’s constructed for them, but what happens as that world changes? Artificial intelligence’s role in the investment process has the potential to be revolutionary, allowing investment managers to better recognize patterns, forecast (and nowcast) events, and make better decisions. While the use cases for AI may seem infinite, the reality is that most of the innovation has occurred in back- or middle-office functions. A report from Deloitte lays out the use cases for it quite eloquently. It just goes to show that machine learning algorithms can be simple, such as training and automating your spreadsheet to do everyday tasks, or complex, such as identifying relationships amongst seemingly disparate pieces of information. The latter may not require any human oversight at all.

Use Cases for Artificial Intelligence Algorithms

| Alternative Data | Utilizing alternative data (e.g., weather forecasts, shipping movements) to gain better real-time insights |

| Automated Insights | Automating traditional sources of information, such as earnings transcripts |

| Operations Automation | Automating repetitive back-office functions |

| Risk Management | Monitor suspicious transactions, and trigger responses |

Source: Adopted from “Artificial intelligence: the next frontier for investment management firms.” Deloitte. 2019.

Human behavior is fascinating

In the stages of truth, I’m not sure where AI currently sits, but I would guess we are “all-in”. Longer term, however, I would imagine the court of public opinion will oscillate, cycling back and forth between the three stages for some time. Like any new “thing,” our industry moves through these “three stages of truth” quite often. See: liquid alternatives, indexing, smart-beta factors, ETFs, and ESG. The ridicule and violent opposition stages of truth are probably where most of the opportunity lies for early adopters. It’s the “self-evident” stage that can be a tricky place for investors to find the signal through the noise. In ESG, it’s greenwashing…in AI, let’s call it machinewashing!

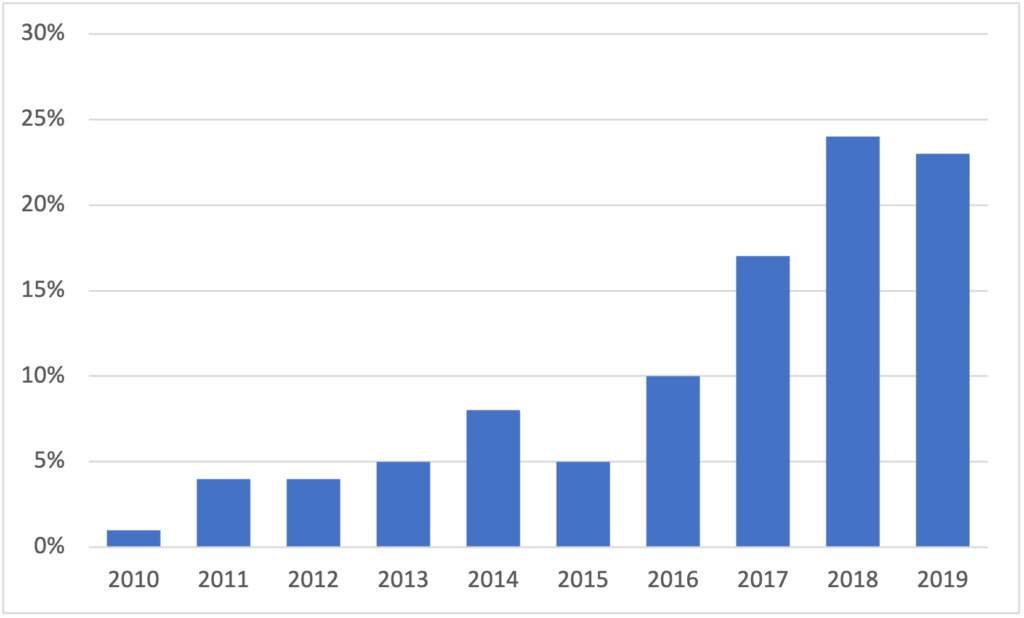

Proportion of Systematic Hedge Fund Launches that Use AI & ML

Source: Preqin 2020 Global Hedge Fund Report

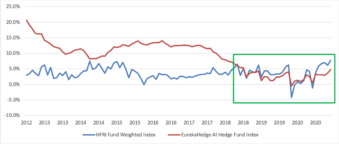

Artificial intelligence-machine learning (AI-ML) hedge funds have grown in popularity and are quickly becoming a larger proportion of the systematic hedge fund industry, according to Preqin. At least recently, empirical research has concluded that machines aren’t the silver bullet to generating alpha. With so much noise in our financial markets, algorithms run the risk of finding meaning where there is none.[i] As demand increases for these strategies and competition takes hold, it will be interesting to see what happens to performance. After all, one of the many criticisms of “traditional” hedge fund strategies is their high and rising correlation to traditional publicly listed equities and fixed income without the high absolute returns. Will that hold true for AI hedge funds eventually? The correlations of AI-driven hedge funds have historically been quite dynamic, but recently the correlations and betas of these strategies relative to a global 60/40 portfolio have converged to the broader complex.

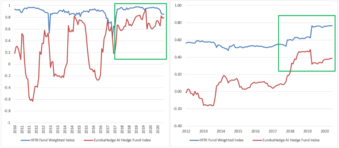

Rising Correlation and Beta of AI-Driven Hedge Funds to a Global 60/40

Source: Author’s calculations.[ii] HFRI, EurekaHedge

Even more interesting is the convergence of the alpha generated by these strategies.

Convergence of Alpha Between AI-Driven and Broader Hedge Fund Complex

Source: Author’s calculations.[iii] HFRI, EurekaHedge

There are, of course, many ways to measure alpha and beta(s)[iv], and I’m not trying to make any forward-looking statements about the efficacy of any individual strategy. In fact, as we have written previously, looking at any alternative investment index can be misleading due to the underlying diversification of the strategies. Rather, these charts simply illustrate how much more competitive the space has become. Have the machines lost it? Have new entrants made the quest for alpha that much more competitive? Was it COVID? Early players may have enjoyed alpha aplenty, but more competition eventually converts alpha into beta. The long-term value proposition of machine learning and data AI’s value proposition isn’t based entirely on its ability to generate alpha. In fact, some of its most powerful applications focus on everything but alpha generation. AI and ML can be used to prioritize longer-term objectives like capital preservation, “operational alpha” (i.e. eliminating internal inefficiencies), and enhanced communication and culture.

Machine washing, no more!

How do you gain insight into a black box when the content of that black box is constantly changing? In my view, qualitative analysis of a quantitative approach is likely to be the best approach. Sure, you need the quantitative foundations to understand nuts and bolts, but it always comes down to asking better questions. Like greenwashing, how do we avoid machine-washing our portfolio?

Focus on Culture

One of the biggest differences between technology companies and traditional financial companies is culture. Stereotypically, technology companies are much more open and collaborative while financial organizations operate in siloes. For simplicity, let’s assume that machine learning managers are closer to a tech firm than a legacy asset manager.

To ensure a fund is successful, you must approach culture checks and qualitative due diligence factors differently. Insights are open-source and shared throughout the investment team, a contrast to the culture of finance, which prioritizes competitive edge even relative to ones’ colleagues. The funds that fail are the ones that don’t embrace this way of work.[v]

Be a Backtesting Skeptic

I’ve never seen a bad backtest. Find ways to test the underlying assumptions of the strategy out-of-sample and, better yet, utilize a process that doesn’t suffer from look-ahead bias. Failing to do so will lead to an overfitted model that may not adapt to the new normal. How many of these AI strategies were able to adapt to the COVID-19 pandemic? More traditional strategies certainly weren’t able, but we should expect more from strategies that are literally super-human!

Flirt with Models

Diversification not only applies to asset classes, but also to the models of a strategy. To reduce the risk of overfitting a strategy and increase the probability of out-of-sample success, one of the suggested frameworks[vi] is to diversify and combine multiple models together:

- Use more than one algorithm and combine forecasts

- Combine forecasts and test training data based on different periods

- Use different forecast styles for different horizons (e.g., technical for short-term vs. fundamental for long-term)

Putting it all together

“If you torture the data long enough, it will confess to anything.”

- Ronald Coase

We say past performance is no indication of future results, and this is especially true when trying to analyze a strategy that is quite literally learning as time goes on. The confusion, and lack of education, can cause us as investment professionals to be afraid to ask the necessary questions to determine the efficacy of a strategy. The world is messy, but let’s not machine-wash it.

Seek education, diversification of both your portfolio and people, and know your risk tolerance. Investing is for the long term.

Aaron Filbeck, CFA, CAIA, CIPM, FDP is Director of Global Content Development at CAIA Association. You can follow him on LinkedIn and Twitter.

[i] Rasekhschaffe, K. and R. Jones. Machine Learning for Stock Selection. Financial Analyst Journal, Forthcoming.

[ii] Monthly rolling 1-year correlation against a 60% ACWI/40% Barclays Aggregate Bond.

[iii] Calculated using a 3-year Jensen’s alpha relative to a monthly-rebalanced portfolio of 60% MSCI ACWI/40% Bloomberg Barclays Aggregate Bond Index

[iv] Since this is for illustrative purposes, I did not utilize style factors.

[v] Lopez de Prado, M. (2018). The 10 Reasons Most Machine Learning Funds Fail. The Journal of Portfolio Management, 44 (6) 120-133.

[vi] Rasekhschaffe, K. and R. Jones. Machine Learning for Stock Selection. Financial Analyst Journal, Forthcoming.