By Dan Taylor, CIO, at Man Numeric.

Quantitative equity investing is having a bit of a mid-life crisis. Will the same approach that has worked for many of us for several decades continue to work in the future?

Introduction

Quantitative equity investing is having a bit of a mid-life crisis. Notwithstanding 2021, some of the most popular quantitative strategies have recently fallen on tough times. Will the same approach that has worked for many of us for several decades continue to work in the future? In a world of seemingly unlimited data and far more computing power than many of us could have imagined decades ago, what tenets of the process should we retain? Here, we endeavor to lay out a path forward and highlight what we need to do better.

Our focus will be on what we believe to be among the most commonly implemented quantitative strategies: cross-sectional, generally bottom-up, strategies.[i] Though these sorts of strategies have been around for decades in one form or another, they really started to gain traction and market share starting in the 1990s. Cross-sectionally oriented quants have historically focused on behavioural anomalies, often revolving around notions of Value (over-reaction) and Momentum (under-reaction). Other types of approaches have also gained popularity, such as Low Volatility or Low Beta strategies. We often attempt to capture phenomena that we believe are pervasive across markets and over time in a systematic and repeatable fashion.

Typically, quant equity strategies are heavily backtest-driven[ii] and therefore, at least somewhat backward looking. If one believes the future will look at least somewhat like the past (and often it does!), then a strategy that worked in the past stands a good chance of working in the future. We also know that there will be periods of time when certain strategies are not effective. And conveniently, we are often convinced that those periods often provide the best prospective opportunities! The research process generally consists of generating an insight, backtesting the insight, refining the insight and repeating. If we find that a signal struggles for a period of time, we may conduct additional research to ‘fix’ the problematic period. Besides signal generation, we also focus heavily on portfolio construction, risk management and execution.

Where Are We Today?

The landscape has become incredibly competitive over the last few decades and there has been wide-spread adoption of quant factors, strategies and techniques. Much of the last decade has been a challenging environment for many quant equity strategies, especially those that focus on Value, Quality, or Low Risk. And in certain regions (like the US), the performance has raised serious questions about whether some of these strategies even work anymore. We think it is important to distinguish between the cyclical and secular challenges that factors like Value may be facing.

On the cyclical side, quants have likely suffered from increasing knowledge about and usage of some traditional factors. Indeed, one might plausibly suggest (with the benefit of hindsight) that many factor-oriented strategies became too crowded at some point over the last decade.[iii] Additionally, there is no question that Value has been out of favour for some time[iv] and that Defensive or Low Volatility strategies have more recently fallen out of favour. Some of this cyclicality may be linked to monetary policy and the interest rate environment, which is difficult to handicap. Clearly, low nominal and negative real interest rates have had an impact on asset pricing, and while that is useful as a contemporaneous explanation for the performance of some factors, it is not necessarily predictive. The notion that many of these factors tend to be cyclical is a reasonable foundation to be positively disposed towards factor-oriented strategies today, and in fact, appears to be at the core of the arguments of some proponents.

However, there are also significant secular issues at play. The increased power and prevalence of computers today, combined with the amount of time that many of these factors have been in the public domain, raise serious questions about what edge some of these strategies may reasonably be expected to have moving forward. In fact, it appears obvious that simplistic factor-oriented strategies have exhibited significant secular decay over time, and innovation has been necessary to mitigate that headwind.

Figure 1 shows the rolling 10-year efficacy of the non-beta factors from the Fama-French 5-factor model plus their Momentum returns.[i] It used to be rare for more than one of these factors to exhibit negative returns; however, over the last decade, many of them have struggled, and the simple average of these five factors has been negative over the last 10+ years. And do note this is also before transaction costs.

This is not to say factor-oriented investing will be irrelevant going forward. But it is not reasonable to expect these factors to work as well as they have historically, and that should help inform how we design and implement strategies. In fact, we should generally assume that signals will decay over time and plan accordingly.

Where to From Here?

First, let us categorise three types of quant equity strategies: factor risk premia [FRP], enhanced beta capture [EBC] and true idiosyncratic alpha [TIA]. In our opinion, most quant equity strategies fall into the FRP or EBC categories. Value- or Momentum-oriented strategies fall in the FRP category, while Low Volatility or Risk Parity portfolios fall into the EBC category. The FRP and EBC categories are different in that FRP requires an asset-specific forecast of returns (typically a transformation of one or more factors), while EBC strategies only require a view on risk (volatility and correlation structure). The stated benefits of these types of strategies are that they may provide attractive returns and/or risk profiles over long periods of time, have meaningful capacity, and capitalise on behavioural or structural biases that are likely to persist over time. TIA is the most difficult type of strategy to build for a number of reasons – to be truly uncorrelated, it will tend to be more niche and less durable. While some of the content in traditional quant equity strategies may have one day actually been TIA, over time it is has morphed into FRP. We believe recognising the difference between true alpha and factor risk premia is important – for investors and allocators alike.

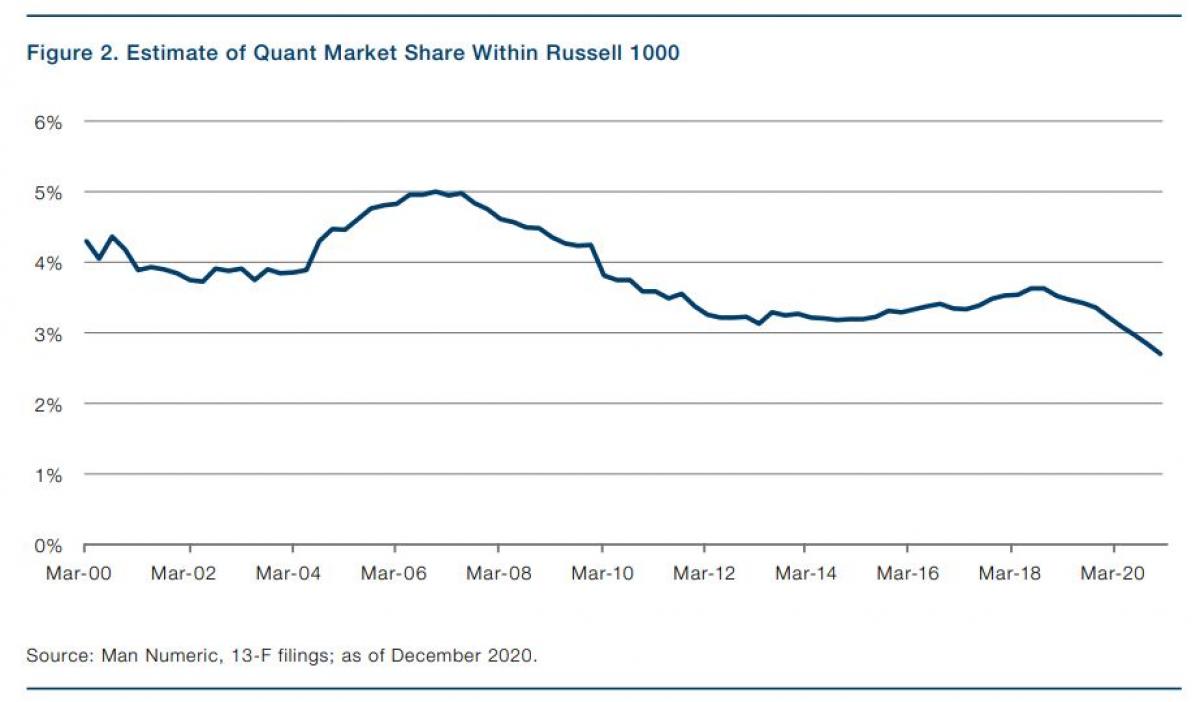

Let us now posit that most quant equity content belongs in the FRP and EBC categories – so what? While many of the concepts within these categories have been shown to be effective over long historical periods, they can often struggle for periods long enough to test an investor’s patience. Value has struggled immensely over the last decade as real rates have gone negative in most of the developed world. Low Volatility may have benefitted from a 30-year bull market in bonds as bond-like equities became more attractive, but what will happen to this type of strategy in a stable or rising interest rate environment? Another issue is that when quant equity strategies work, a lot of capital tends to flow into them which often begets more good returns and flows (note this may be a challenge for any type of investment strategy). Naturally, as more capital attempts to profit from a particular anomaly, prospective profits will fall until a new equilibrium is found. And then the positive feedback loop between performance and flows can quickly reverse (as many factor-oriented strategies have seen over the last few years). Figure 2 shows our estimate of quant market share within the Russell 1000, rising in the mid-2000s (a period of good performance), followed by outflows from quant strategies from 2008 to 2012, and then again from 2018 to 2020.[ii]

Those are two big problems, but the biggest issue may be that quant equity is almost myopically backward looking. Most quantitative strategies rely on backtesting to find out what would have worked in the past, and then convincing oneself it is likely to continue in the future. Oftentimes, the backtests look unreasonably attractive as a fair amount of ‘research’ may be conducted to mitigate historical paper drawdowns. It feels like it should go without saying, but quants really need to be more forward-looking in our approach to systematic equity investing. This is not to say history is irrelevant – it is merely stating it is one draw from a distribution, and likely a biased one which could create a false sense of security. When something hasn’t worked for a period of time, our prior is that it is due for a rebound, not that it doesn’t work anymore, because that is what happened historically.

What about true idiosyncratic alpha? Wherever it exists, it is unlikely to persist indefinitely, and also likely has very limited capacity. The alpha may be generated from an operational advantage, a temporary dislocation in the market, or an insight or dataset that has not been commoditised or popularised. But the nature of true alpha is that it will decay and so monitoring alpha decay and correlation structures are critical. To do this well, and at scale, one needs an excellent platform, process and people.

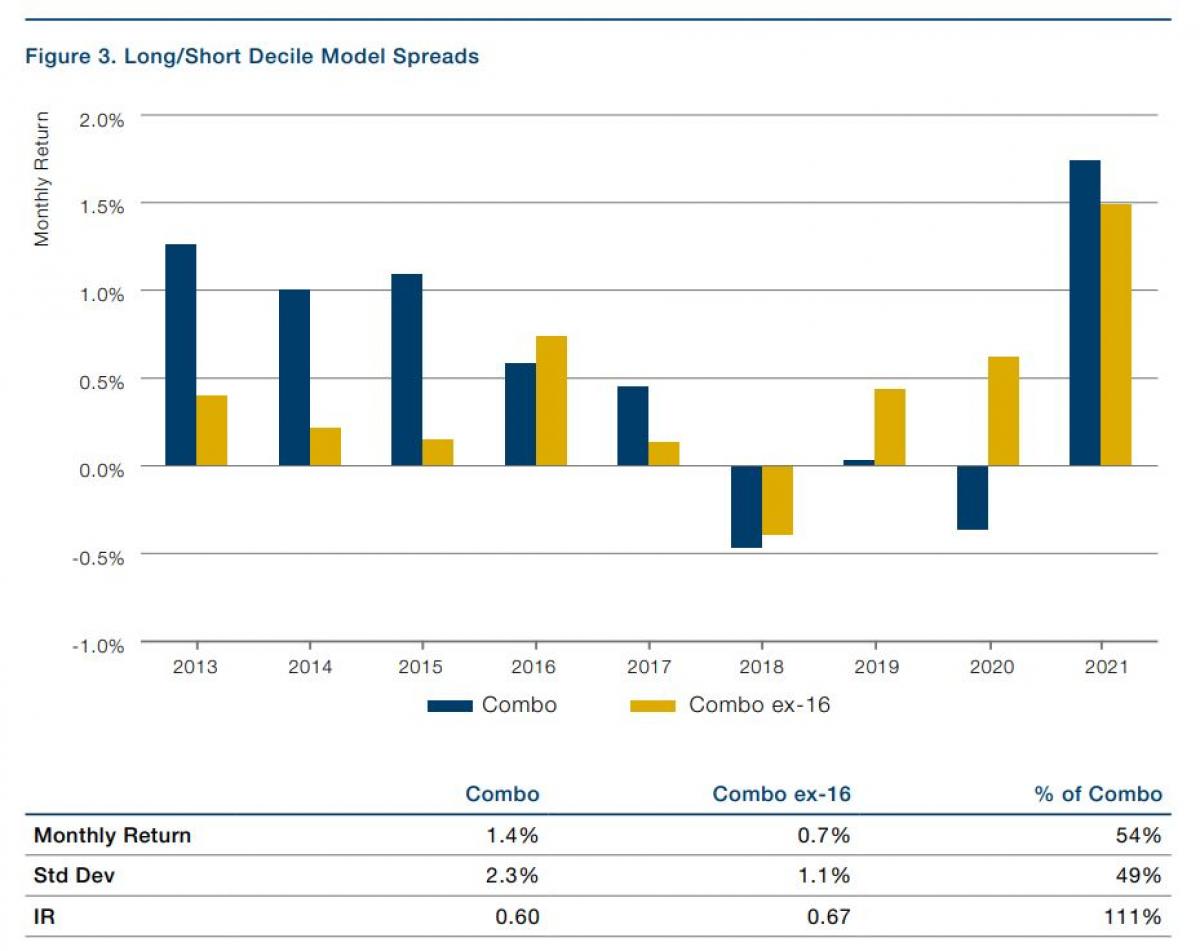

Source: Man Numeric; 1 January 2013 – 26 March 2021

Note: All model spread performance shown is gross-of-fees and does not represent the performance of any Man Numeric portfolio or product and should be considered hypothetical. The model spreads shown are long quintile model spreads, (long the top 10% and short in the bottom 10% ranked names) and display the return. These spread returns are instantaneously rebalanced, sector-neutral and do not reflect transactions costs.

Increasingly, we believe investors should focus on trying to understand which insights are more commoditised or proprietary. One method to do this would be to cross-sectionally neutralise an alpha by a set of generic factors (for example, the Barra fundamental risk factors). Another method is a technique we call Return Neutralisation, which attempts to neutralise to risk factors by estimating a hedge ratio from the time-series of historical returns. Both methods are attempts to determine how much of the ‘alpha’ process is real alpha versus what can be explained by generic factors. Figure 3 shows the backtested efficacy of the composite alpha within the Global (developed large cap) universe with and without (ex-16) the Barra fundamental risk factors. In the earlier years in the sample, a significant portion of the paper alpha was actually exposure to several generic fundamental risk factors, while in 2019 and 2020, those generic fundamental risk factors were a material drag.

From a product development and positioning perspective, it is quite important to understand the value-add proposition and how one is positioned relative to other participants in the marketplace. True alpha is extremely valuable, but not quite as abundant as most of us would like. Fees should be higher and capacity more restrained. That being said, FRP and EBC portfolios can be valuable components to a well-diversified investment program if implemented skillfully and with a focus on minimizing both direct (e.g. fees) and indirect (e.g. transaction costs) drag.

The Future of Quant

So, what does success look like?

First, success in trading or investing must be process-driven – but that process must be dynamic and flexible. The market and players change over time, and at an increasing rate, and a process that does not acknowledge those changes will struggle to consistently prosper.

Second, we believe it is imperative for us to differentiate between true idiosyncratic alpha and risk premia or portfolio construction-oriented strategies. There are important implications on fees, capacity, risk management, aggressiveness of trading and performance expectations. A factor risk premia strategy packaged as an alpha product is as likely to disappoint as an alpha strategy packaged as a risk premia-oriented strategy. It will be increasingly important to understand the differences and implement accordingly.

Third, we as quants need to be more forward looking (and less backward looking!). We need to have a view of what the future might look like and either conviction that a certain signal will be relevant going forward or a strict process to tell us when we are wrong: what is different today or tomorrow versus our backtesting period? Everyone has more access to computing power, data, academic research, historical trading strategies and social networks. How does this impact the rationale of a particular strategy?

Fourth, the price or value of a market or asset does matter. While it is inherently difficult to price or value markets or assets, and there will be periods of time where investors/traders are unbothered by such mundane concerns, having a valuation framework as an input into an investment process should always be relevant (contrary to what some pure growth investors might suggest). The current debate about the relevance of Value or whether or not it is dead is misguided: at a certain price, almost any asset could be attractive or unattractive.

Conclusion

The essence here is to more clearly define how we think about quant equity. While traditional factor-oriented strategies have prospered (on and off) for decades, we need to better harness our strengths and recognise our weaknesses. To be clear, this is a direction Man Numeric has been strategically moving towards over the last several years, and in fact, have tried to employ historically. Going forward, there is a need to utilise analytical skills to look forward and identify opportunities and then make judgment calls. The rise of passive, the adoption of ESG, the threat of climate change, the challenges of income and wealth inequality, the integration of technology into our daily being and the changing demographics of the world all potentially provide opportunities to apply analytical prowess to solve the investment problems of the future in a way that cannot be answered in a backtest.

Summary: Typically, quant equity strategies are heavily backtest-driven and therefore, at least somewhat backward looking. The rise of passive, the adoption of ESG, the threat of climate change, the challenges of income and wealth inequality, the integration of technology into our daily being and the changing demographics of the world all potentially provide opportunities to apply analytical prowess to solve the investment problems of the future in a way that cannot be answered in a backtest.

[i] Notably we will not be discussing CTA strategies which is something our colleagues at AHL may have a little better insight on.

[ii] A point we will come back to again. And again. And again.

[iii] And potentially in the prior decade, circa 2007.

[iv] At least up until recently…

[vi] Man Numeric; quarterly 13-F data. Based on a list of ~50 quantitative managers.

About the Author

Daniel (‘Dan’) Taylor is CIO of Man Numeric. He also serves on the Man Group Executive Committee and the Man Numeric Investment Committee. Dan has had multiple roles at Man Numeric since joining as an intern in 1998, including director of small cap strategies, head of hedge fund strategies, and senior member of Man Numeric’s strategic alpha research team. During his tenure at Man Numeric, Dan has conducted a wide range of research, including areas such as momentum, earnings quality, valuation, investor behavior, and market timing. Dan holds a Bachelor of Arts degree in economics with honors from Harvard University. He is also a CFA charterholder.

Hypothetical Results are calculated in hindsight, invariably show positive rates of return, and are subject to various modeling assumptions, statistical variances and interpretational differences. No representation is made as to the reasonableness or accuracy of the calculations or assumptions made or that all assumptions used in achieving the results have been utilized equally or appropriately, or that other assumptions should not have been used or would have been more accurate or representative. Changes in the assumptions would have a material impact on the Hypothetical Results and other statistical information based on the Hypothetical Results. The Hypothetical Results have other inherent limitations, some of which are described below. They do not involve financial risk or reflect actual trading by an Investment Product, and therefore do not reflect the impact that economic and market factors, including concentration, lack of liquidity or market disruptions, regulatory (including tax) and other conditions then in existence may have on investment decisions for an Investment Product. In addition, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points which can also adversely affect actual trading results. Since trades have not actually been executed, Hypothetical Results may have under or over compensated for the impact, if any, of certain market factors. There are frequently sharp differences between the Hypothetical Results and the actual results of an Investment Product. No assurance can be given that market, economic or other factors may not cause the Investment Manager to make modifications to the strategies over time. There also may be a material difference between the amount of an Investment Product’s assets at any time and the amount of the assets assumed in the Hypothetical Results, which difference may have an impact on the management of an Investment Product. Hypothetical Results should not be relied on, and the results presented in no way reflect skill of the investment manager. A decision to invest in an Investment Product should not be based on the Hypothetical Results. No representation is made that an Investment Product’s performance would have been the same as the Hypothetical Results had an Investment Product been in existence during such time or that such investment strategy will be maintained substantially the same in the future; the Investment Manager may choose to implement changes to the strategies, make different investments or have an Investment Product invest in other investments not reflected in the Hypothetical Results or vice versa. To the extent there are any material differences between the Investment Manager’s management of an Investment Product and the investment strategy as reflected in the Hypothetical Results, the Hypothetical Results will no longer be as representative and their illustration value will decrease substantially. No representation is made that an Investment Product will or is likely to achieve its objectives or results comparable to those shown, including the Hypothetical Results, or will make any profit or will be able to avoid incurring substantial losses. Past performance is not indicative of future results and simulated results in no way reflect upon the manger’s skill or ability.

Important Information This information is communicated and/or distributed by the relevant Man entity identified below (collectively the ‘Company’) subject to the following conditions and restriction in their respective jurisdictions. Opinions expressed are those of the author and may not be shared by all personnel of Man Group plc (‘Man’). These opinions are subject to change without notice, are for information purposes only and do not constitute an offer or invitation to make an investment in any financial instrument or in any product to which the Company and/or its affiliates provides investment advisory or any other financial services. Any organisations, financial instrument or products described in this material are mentioned for reference purposes only which should not be considered a recommendation for their purchase or sale. Neither the Company nor the authors shall be liable to any person for any action taken on the basis of the information provided. Some statements contained in this material concerning goals, strategies, outlook or other non-historical matters may be forward-looking statements and are based on current indicators and expectations. These forward-looking statements speak only as of the date on which they are made, and the Company undertakes no obligation to update or revise any forward-looking statements. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those contained in the statements. The Company and/or its affiliates may or may not have a position in any financial instrument mentioned and may or may not be actively trading in any such securities. This material is proprietary information of the Company and its affiliates and may not be reproduced or otherwise disseminated in whole or in part without prior written consent from the Company. The Company believes the content to be accurate. However accuracy is not warranted or guaranteed. The Company does not assume any liability in the case of incorrectly reported or incomplete information. Unless stated otherwise all information is provided by the Company. Past performance is not indicative of future results.