By Chris Carsley, CFA, CAIA: Chief Investment Officer & Managing Partner, Kirkland Capital; Group & Chief Investment Officer & Managing Partner Arch River Capital and John Canorro, CFA, CAIA: Director of Operational Due Diligence, Pathstone.

Introduction

The alternative investments universe, once the exclusive purview of institutional and ultra-high net worth investors, is proliferating and being democratized such that these investment opportunities are now accessible to a new cohort of investors who may be less familiar with the potential risks and pitfalls inherent in this space. [i] This new cohort is growing rapidly as a result of the technology boom and the expansion of the start-up industry. These investors are looking outside of traditional equity and fixed income markets. Further fueling the potential investor expansion are modifications to the accredited investor definition, changes to Crowd Funding platforms under both Regulation A and Regulation Crowdfunding, and the ability for 401(k) plans to include investment options with diversified private equity exposure.[ii]

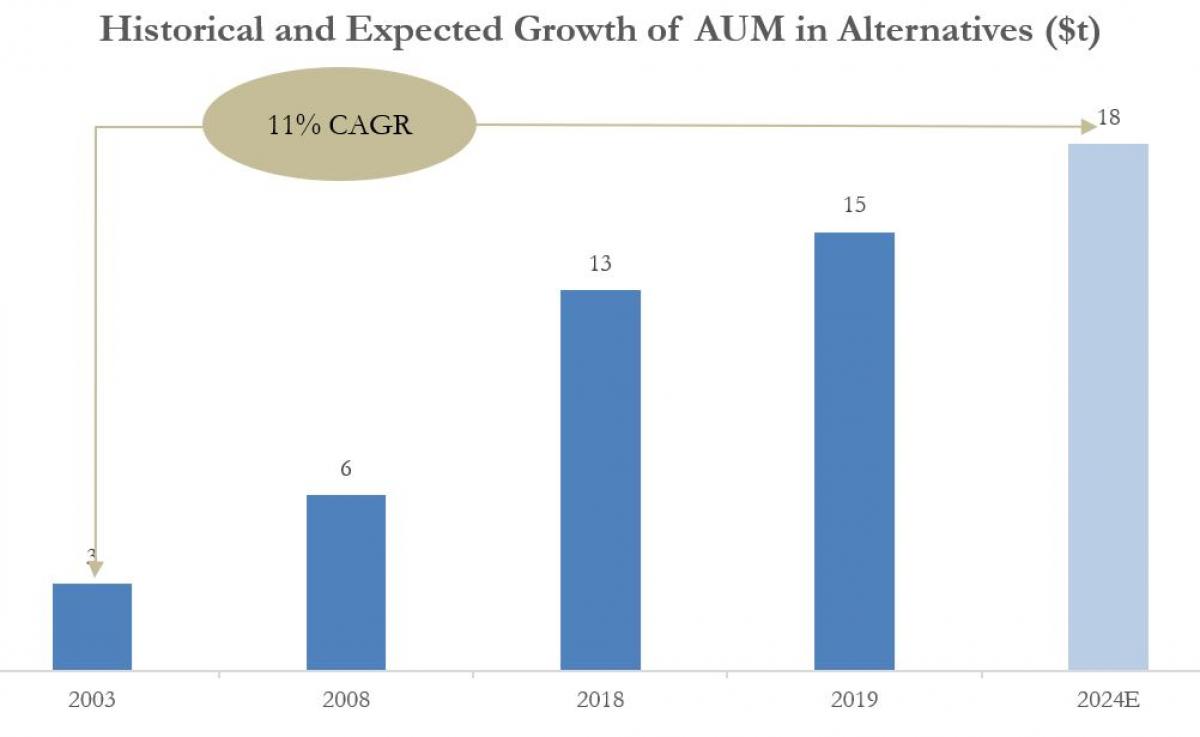

Over the past eighteen years, assets under management (“AUM”) for the Alts space has grown from $3 trillion to $15 trillion[iii]. By 2024, the Boston Consulting Group predicts that Alts will represent 17% of global AUM as investors continue to seek uncorrelated returns, illiquidity premiums and nontraditional return profiles.

Given the increased demand for alternatives investments, investors and investment advisors must ensure they are properly equipped to identify the risks associated with these opportunities. This white paper mini-series is intended to help educate investors on how to identify and vet several prevalent red flags, or risk areas, when investing in alternative investments. Each paper will focus on a key risk by defining it, explaining its significance, offer questions to help vet it, and provide case studies to give real world context.

Investors can no longer simply rely on past performance and pedigree of the portfolio management team as the primary considerations driving an investment decision. Proper due diligence is complicated and multi-faceted. On one end of the spectrum it encompasses quantitative investment analysis, and on the other, it necessitates a qualitative analysis of the investment manager’s operational infrastructure. Furthermore, there are several factors that can result in failed investments. Many of these negative outcomes are derived from areas where Limited Partner and General Partner interests do not always align[i],[ii]. Therefore, it is critical to understand and identify these areas of misalignment during the due diligence process. We hope to help educate investors on how to identify and vet these types of red flags, amongst others, during the pre-investment due diligence process.

Primary Red Flags

There are several areas where investors in Alts funds need to ensure they understand the risks and conflicts of interests that can create a misalignment between manager and investor. Identifying these factors is not enough. Investors must know which questions to ask and where to look to root out these potential snags. Many common areas that have created misalignment in the past, include:

- Investment Allocations: Typically, investment firms manage multiple funds and strategies that usually have some degree of overlap. Investors need to understand the process by which the General Partner allocates investment opportunities among the various funds under their management.

- How do you ensure that the vehicle you are invested in is getting its fair and equitable allocation of investment opportunities?

- How do you ensure that the General Partner is not cherry picking its best ideas by placing those trades in an employee Fund?

- Does the Fund’s Limited Partnership Agreement dilute the General Partner’s fiduciary duty to the Fund? If so, how does that potentially impact deal allocations?

- Does the General Partner manage funds with overlapping investment strategies, e.g., a best ideas fund, global fund vs geographic specific? If so, how are trades allocated amongst these vehicles?

- Does the General partner have the right to create parallel funds and other investment pools that might have preferential treatment to certain trades for a particular investment class?

- Valuations: The process a General Partner undertakes to ascertain the fair value of each investment in the Fund’s portfolio on a periodic basis, e.g., monthly, quarterly, or annually. Non-exchange traded assets, e.g., PE, VC, RE, and illiquid hedge fund positions may be marked by the General Partner[iii]. The General Partner may be conflicted when internally marking their book and their marks may differ materially from what the asset is ultimately sold for.

- If you subscribe into or redeem from a hedge fund with a significant amount of non-exchange traded assets, how do you have confidence in the Fund’s Net Asset Value (“NAV”)? You may pay too much on the way in and sell for too little on the way out.

- If you are considering investing in a Private Equity, Real Estate, or Venture Capital fund, how do you have confidence in the Manager’s track record if the underlying positions are internally marked? The internal rate or return (“IRR”) generated from unrealized positions may differ materially from the realized IRR.

- If the underlying assets in the Fund were publicly traded, would they exhibit materially different volatility and correlation statistics? If so, is the Fund’s valuation process potentially creating a false sense of security?

- Related Party Transactions: General Partners may conduct business, on behalf of Funds they manage, with parties that are affiliated with the General Partner. These business relationships are not conducted at arm’s length and may create conflicts of interests for the General Partner.

- Does the Fund do business with affiliates of the GP? For example, does a real estate manager use affiliated entities to provide property management, construction management or general contracting work to portfolio holdings of the Fund? If so, how does the Manager ensure that the Fund is not being over charged for these services?

- Is the General Partner charging the Fund for the use of internal fund administration, legal, and / or tax services? If so, how does the Manager set the price for these services?

- Cross-Fund Trades: Managers may sell a security or portfolio company between funds that they manage. When this occurs, they are on both sides of the trade and are conflicted in establishing a transaction price. They want to sell as high as possible because of the potential to earn carried interest, but they do not want the buying fund, that they also manage, to pay too high a price. In short, this is not an arm’s length transaction.

- How do you ensure that the price received for the asset you own was equal to fair market value or the price you would receive in an arm’s length transaction?

- What third parties or internal controls are in place to ensure fair treatment between funds? For example, does the Fund seek guidance or approval from a Limited Partner Advisory Committee?

- Use of Operating Partners and Operating Advisors: Private Equity and Venture Capital firms, particularly larger ones, are increasingly using Operating Partners and Operating Advisors to augment their investment teams. These people are not employees of the General Partner, and their use can create several conflicts of interest for the Manager.

- Their compensation is usually not covered by the management fee and instead passed through to the Fund or the underlying portfolio companies. Conversely, compensation for employees of the General Partner is covered by the management fee.

- If these individuals are paid by the portfolio company, then their costs will not flow through the Fund financials. Accordingly, an investor will not know what these people are being paid.

- The fees charged by these groups / people can be substantial, particularly if they are paid success fees for completion of acquisitions. Therefore, an investor may think they are paying management fees of 2%, but actual expenses are closer to 3%-4% per annum.

- What is the Fund paying for in addition to the management fee? Or, conversely, what does the management fee actually cover?

- What is the all-in expense ratio of the fund?

- Asset and Liability Duration: The process for comparing the duration of a Fund’s underlying investments, or assets, relative to a Fund’s equity capital base which is subject to withdrawal terms, or its liabilities. This analysis also pertains to Private Equity, Real Estate, or Venture Capital funds structured as evergreen, rather than traditional closed-end, funds.

- Does the duration of the Fund’s assets match the withdrawal terms of the Fund?

- If the Fund’s underlying assets are non-exchange traded, how does the Manager accurately strike a NAV to determine the price investors pay to enter or exit a Fund?

- During times of stress or heightened redemption requests, can the manager implement fund level gates?

- Service Providers: The process for independently confirming the existence and competency of key service providers to a Fund, e.g., auditor, administrator, prime broker(s), tax advisor.

- Are the Fund’s service providers reputable, and do they have experience in the specific focus area of the Fund in question? Are they all non-related entities?

- Is the fund a majority of the service providers business?

- If the auditor is not Big 4, is it PCAOB reviewed[1]? Does it have any expertise in the field pertaining to the Fund’s strategy? Does it have multiple offices and partners? Does it do work for other funds in this space?

- Can the investor independently confirm the relationship between the service provider and the Fund?

- What information and transparency are obtained directly from the third-party service provider?

- Operational Due Diligence: Does the investment manager have a sufficient operational infrastructure in place, with appropriate checks and balances, in order to minimize the occurrence of problems that may lead to capital impairment from operationally related errors:

- Does the manager have appropriate separation of duties regarding the movement of money? For example, separation between those that can initiate and approve wires.

- Does the manager have adequate protections in place to safeguard information? How does the manager protect clients’ personally identifiable information?

- Is the manager registered with the Securities and Exchange Commission as a registered investment advisor? If not, has the manager established a compliance program that is independent from the investment decision making process?

Upcoming Papers

This white paper mini-series is intended to help investors identify and vet a number of red flags during the pre-investment due diligence process. This is not a comprehensive list. Many funds will have unique, esoteric factors that will need to be sufficiently vetted.

Over the coming months, a new whitepaper will be published focusing on each of these key risks. The paper will define the risk, explain its significance, offer questions and actions that can be taken to help vet it, and provide case studies to give real world context. Our next paper will focus on Investment Allocations and discuss a case study that dives into the conflicts that can occur with a manager that manages multiple funds with overlapping investment mandates.

[i] When discussing alternative investments or “Alts” this paper is referring to asset managers that offer investment funds, structured as limited partnerships, to investors, e.g., hedge funds, private equity, private real estate, private credit and venture capital. While this white paper mini-series will focus on alternative investments, the red flags discussed throughout the series are also applicable to many private markets, less regulated, investments, such as making direct investments in private companies through exchanges, fund sponsors, or one’s professional network.

[ii] Please see Democratizing Access To Private Markets With The Rise Of Alternative Venture Capital in Forbes Magazine.

[iii] Boston Consulting Group (Global Asset Management 2020 Report)

[iv] On June 23, 2020, the SEC Office of Compliance Inspections and Examinations (OCIE) issued a risk alert, Observations from Examinations of Investment Advisers Managing Private Funds, highlighting several deficiencies that caused investors in private funds to pay more in fees and expenses than they should have or resulted in investors not being informed of relevant conflicts of interest concerning the private fund adviser and the fund.

[v] This paper may use the acronyms LP and GP when referring to Limited Partner(s) and General Partner(s), respectively. Additionally, the term “Manager(s)” may be used interchangeably with “GP”.

[vi] This paper may use the acronyms PE, RE, and VC when referring to Private Equity, Private Real Estate, and Venture Capital, respectively.

About the Authors

John Canorro is a Partner of Pathstone and Director of Operational Due Diligence. He is responsible for conducting the operational due diligence on the external managers with whom Pathstone commits capital to.

Previously, John was the Managing Director of Operational Due Diligence at Cornerstone Advisors where he oversaw the operational due diligence efforts across the firm’s $4 billion investment program. John began his career as an investment banking analyst with Cary Street Partners.

John earned a Bachelor of Science in Commerce from the McIntire School of Commerce at the University of Virginia. He also holds the Chartered Financial Analyst designation from the CFA Institute, the Chartered Alternative Investment Analyst designation from the CAIA Association, and is a member of the CFA Society of Seattle.

John is a Seattle area native. He and his young family love spending time at local parks and going on walks around the neighborhood.

Chris Carsley brings over 25 years of investment industry expertise specializing in portfolio management, risk management, valuation, regulatory compliance practices, corporate and venture finance, business operations efficiency, securities research, arbitrage trading, and hedging.

Chris is the Managing Partner and Chief Investment Officer for Kirkland Capital Group. He is responsible for portfolio management, risk assessment, and fund operations for the Kirkland Income Fund, a micro-balance commercial real estate bridge financing fund. Chris is also a managing partner at Arch River Capital, which manager of a seed/angel fund and other private equity positions.

Previously, Chris was Managing Director of Bluewater Global Ltd., an international holding company where he performed corporate analysis and invested in a variety of direct and indirect venture capital projects.

Prior to entering venture capital investments, Chris was responsible for the creation of the business risk and operational due diligence program as a senior member of the investment research and analysis team at Benchmark Plus Management. He was also the head execution trader of futures, options and OTC based trades for the Benchmark Funds. Chris was a trader for Paloma Securities where he negotiated and structured ISDAs, securities lending, and financing agreements that targeted global arbitrage opportunities primarily for Canadian and European markets. Chris was also a senior member of the hedge fund security finance team performing due diligence for the Paloma hedge funds to assist in enhanced finance/margin treatment and short coverage costs.

Chris started his professional investment career as a portfolio manager for Key Asset Management managing institutional and private client discretionary accounts and was responsible for sales, asset research/valuation and portfolio management.

Chris was a member of the Charles Wright Academy Endowment Committee, serving on the Committee since March 2017. He co-founded the Seattle Alternative Investment Association in 2004 and is Co-Head of the executive board of the Seattle CAIA chapter launched in 2017. He earned his Chartered Financial Analyst (CFA) designation in 1998, Chartered Alternative Investment Analyst designation in 2011, and holds a BBA from the University of Portland.