By Noel Smith, Founder and Chief Investment Officer of Convex Asset Management.

What if stocks and bonds move down at the same time?

What do your stocks, house, car, lawnmower, and expensive jewelry all have in common? If things get financially desperate enough, you’ll sell them all. At first thought one might assume that there is no real correlation between a lawnmower and a car, but in times of serious stress they all have to go…at the same time! If you think your real estate is worth $500k, maybe you’ll take $495k, but what if you have to sell it in a month no matter what? How about a week? How about a day?

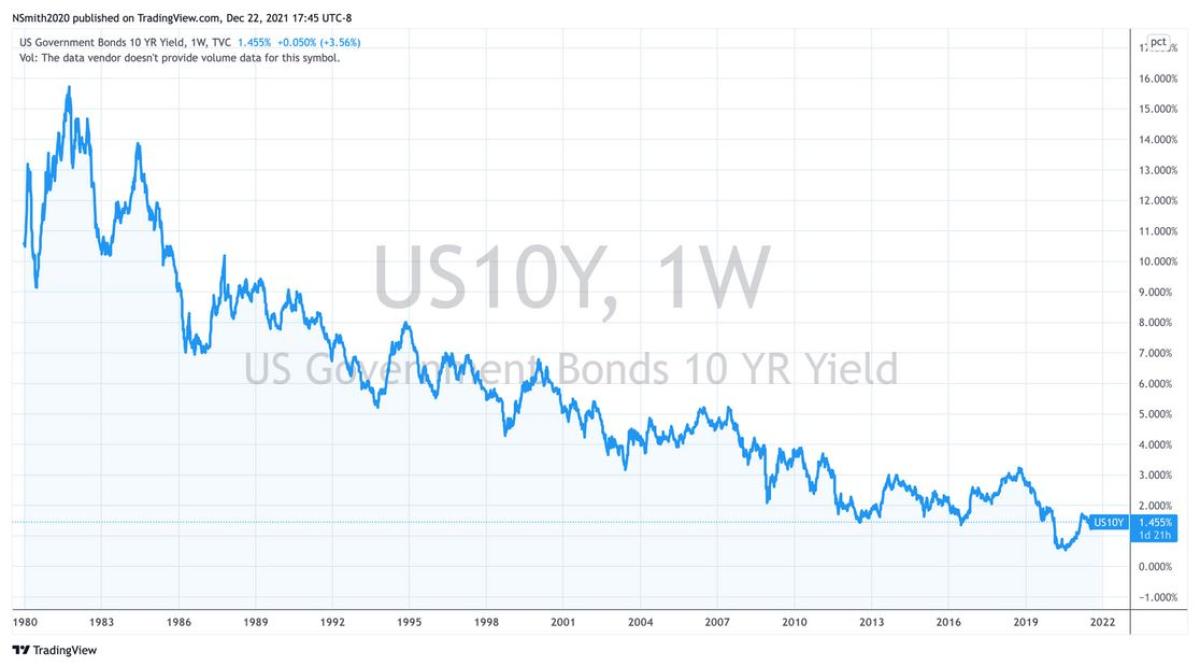

The typical recommended portfolio of 60% of your assets in equities and 40% in bonds has worked well for a long time. The data supports the idea, bonds have been in a bull market since the early 1980’s, and yields have been headed down in kind. Most of the time when stocks go down enough, bonds often go up. And because of this negative correlation it has made sense to have both in your portfolio, bonds acting as a safe haven from stocks and vice versa.

In 1982 with rates at 15% there was a lot of room for bonds to go up (rates down). But now in 2021 with the same rate at 1.4%, it’s not the same. Rates can’t go down another 13.5%. Sure rates can go down 1.4%, to zero, or even negative but there is no data to support a deeply negative interest rate environment. Moreover, with the Fed ending their bond purchase program there will be less downward pressure on rates at the exact same time that inflation is higher than it’s been in decades (The Fed are still buying bonds every month but have signaled they will decrease this purchase by $30 billion per month through the beginning of 2022, ending Quantitative Easing).

While none of us know where the stock or bond market will go, most people have some risk exposure to the standard retirement concept of a 60/40 portfolio whether in their 401k, IRA, mutual funds, etc. This has become a fixture of the modern portfolio but the massive weakness with this plan is that it is predicated on the negative correlation between stocks and bonds…but what happens to a retirement account if this relationship breaks down? What happens if the relationship changes to a positive correlation, stocks and bonds both down at the same time? Inflation is the main reason rates will go up, but if the Fed were to raise rates to fight inflation it could ruin the economy. Consider a 30-year fixed mortgage where the debt on the property is $1m. With an interest rate of 3.5%, the payment would be around $4,500. However, if the interest rate was 8.5%, the payment would balloon to just under $8,000. Very few Americans could afford this percentage change in their financial obligations. A change in rates of this magnitude would clearly destroy demand for real estate, causing prices to plummet. Inflation (as of this writing) is at its highest since the 1980s, arguably higher (note the Boskin Commission).

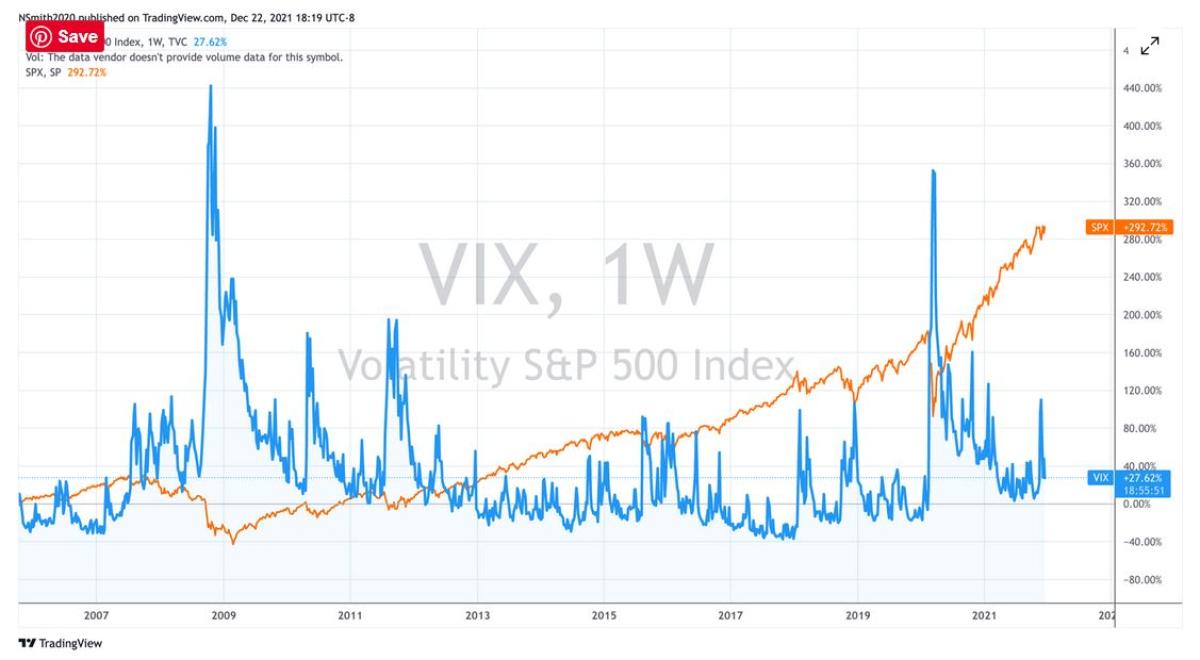

Historically, stocks and bonds have had long periods of positive correlation but not since the 1980’s when most portfolios were constructed, the effect of stocks down and bonds down on the Baby Boomer generation would be devastating. So what is the answer? Real Estate? Hedge Funds? Commodities? Gold? Bitcoin? The problem is that all of these can go down if the economy as whole really starts to struggle, there is one asset class that will very likely do well if the rest of these struggle: volatility. The concept is simple, if things get messy then asset prices will swing much more violently and historically volatility has almost always gone up when stocks go down.

True diversification takes into account not just the current correlations but also how these correlations will change if prices change dramatically in the future. For that reason, volatility as an asset class can be an extremely valuable part of a truly diversified portfolio.

About the Author:

Noel Smith is a Founding Partner and the Chief Investment Officer of Convex Asset Management, a private investment firm.

As a member of the CME, CBOT and CBOE Noel has over 25 years of experience trading volatility, market making, and managing risk. Noel was previously the CIO and Portfolio Manager of two separate Chicago-based proprietary derivatives trading firms. Additionally, he was the seed investor who financed the launch of global high-frequency trading firm GETCO LLC (KCG/Virtu) which grew to account for 20%+ of trading volume in the U.S. As a founding member of Third Millennium trading in 1996 his firm became one of the largest options market-making firms in US Equity Options Markets backing over 65 market makers and traders at the CBOE, CME and CBOT. Noel is an expert in options, stocks, bonds, ETPs, commodities, futures, and volatility. As a quantitative investor and risk manager, Noel is versed in high-frequency trading (HFT), relevant market structure, and the underlying technology.

Original Article: Correlation, A Hidden Risk To Your 60/40 Portfolio (convexam.com)