By Andy Weisman, Chief Investment Strategist, Windham Capital Management.

Basing effects have a significant impact on reported annualized inflation. Reported annualized inflation has the potential to cause confusion concerning the de facto pace of inflation, thereby mischaracterizing current economic conditions. Such confusion could drive inappropriate decisions at both a personal and governmental policy level.

Basing effects occur when data is dropped from a statistic as we step forward in time. Notably, when presenting a one-year measure of inflation, as we step forward by a month, we systematically drop off one period of old monthly data and base the new measure of inflation off a potentially very different starting point. Given we have recently had a big run-up in inflation as we transitioned through and emerged from the COVID pandemic, basing effects will now have a significant impact on reported annualized inflation rates.

Analysis of Reported One-Year Inflation Rates

This short study presents seven static inflation scenarios for the purpose of isolating basing effects on reported inflation. This is accomplished by producing a series of inflation “projections” that result from stepping through the next thirteen months, dropping monthly inflation data that is more than a year old, replacing it with assumed static annualized inflation outcomes.

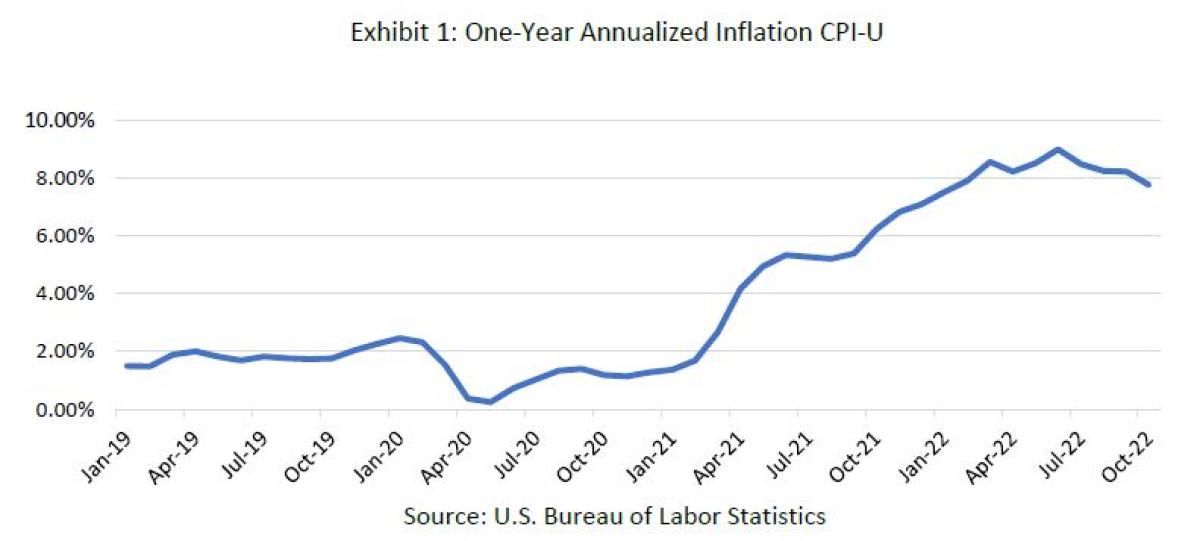

Exhibit 1 below presents a time series of the widely-reported-on annualized inflation rate drawn from the Consumer Price Index for all Urban Consumers (CPI-U). Inflation is now understood to be close to 8%.

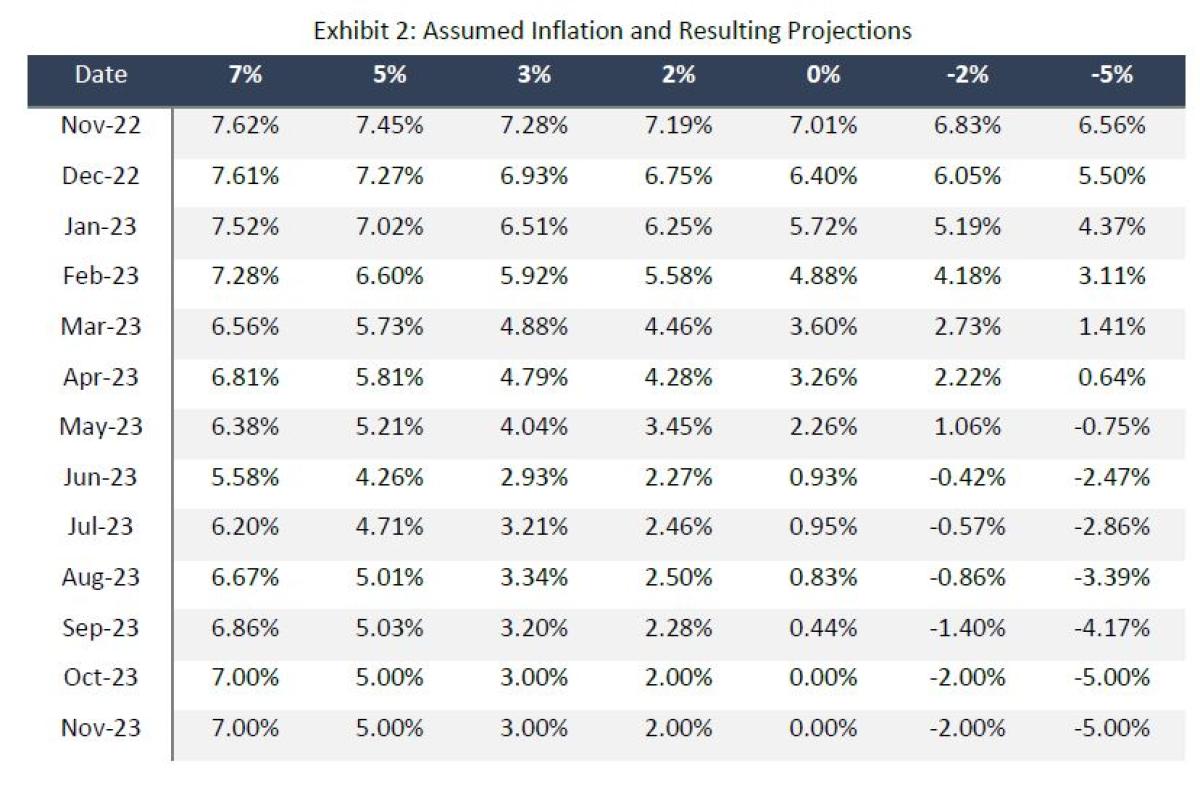

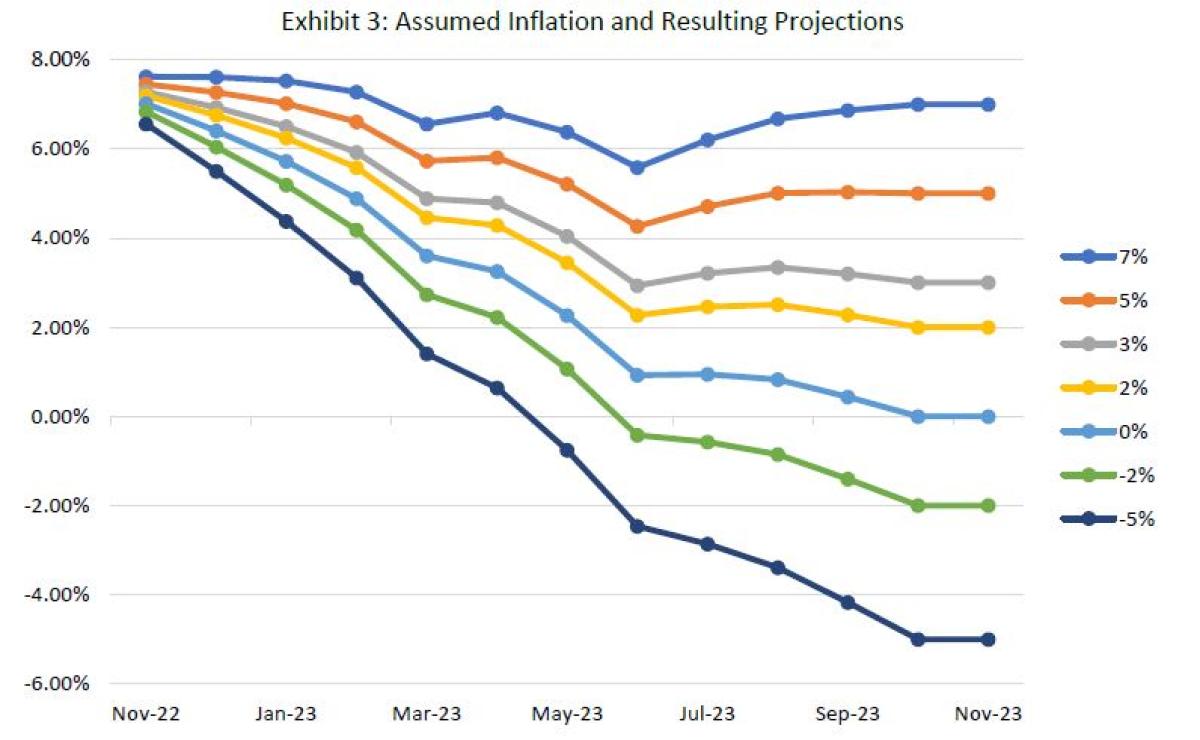

Exhibit 2 and 3 below, present seven separate scenarios, each scenario representing an assumed static annualized monthly inflation rate.

Scenario (7%) presents the path of reported annualized inflation under the static assumption that the monthly annualized rate of inflation is now 7% and remains at that rate for the foreseeable future, i.e., the current static annualized inflation rate, beginning now, remains at 7%. Despite inflation remaining at a de facto 7%, we would observe a pronounced decline in the trend of reported inflation until June of next year, where the reported rate would bottom out at 5.58%. After that point, reported inflation would begin to move up again. This scenario highlights the possibility that reported inflation could give false hope that the Federal Reserve is doing its job of reining in inflation. Scenarios (5%) and (3%) present similar results; inflation is not coming down to where the Fed would like it to, but it appears as though it is.

Scenario (2%) highlights another challenge. In this scenario, the de facto inflation rate is now already at the Fed’s target but reported annualized inflation remains stubbornly above target until October of next year, thereby producing a persistent overstatement of inflation that could drive both individual expectations and even an overly aggressive policy response. This effect is more dramatically illustrated in Scenario (-2%) which illustrates the path of reported annualized inflation under the assumption that it has already declined to -2%, i.e., we are in a de facto deflationary environment. In this scenario we see that reported inflation remains above the Fed target of 2% until May of next year even though we are in a de facto deflationary environment.

Summary

Due to the recent run-up of inflation that occurred during the emergence from the COVID pandemic, basing effects will have a substantial impact on reported annual inflation rates over the next year. First, if no real progress is made to rein in inflation, the reported trend-rate of inflation will show a decline until the middle of next year. If inflation declines substantially near term, reported annual inflation will remain substantially above the Federal Reserve’s stated target of 2% well into next year, even in the presence of de facto deflation. When making decisions that require a characterization of current macroeconomic conditions, basing effects should be accounted for. Further, when considering annualized measures of inflation, the use of multiple look-back periods, some shorter and some longer, is highly recommended.

About the Author:

Andrew B Weisman is a Managing Partner and Chief Investment Strategist of Windham Capital Management, LLC. Andy has more than 30 years of experience as a portfolio manager of alternative investment strategies. Prior to joining Windham, Andy was the Chief Investment Officer of Janus Capital’s Liquid Alternative Group. Prior to joining Janus Capital, he was Managing Director and Chief Portfolio Manager for the Merrill Lynch Hedge Fund Development and Management Group, and Chief Investment Officer for Nikko Securities International. Andy has a Masters in International Affairs/International Business from Columbia University’s School of International and Public Affairs, and a BS in Philosophy/Economics from Columbia University and has completed all of the course work and comprehensive exams toward a PhD from Columbia University’s Graduate School of Business.

He is a recipient of the Bernstein Fabozzi /Jacobs Levy Award for outstanding article published in the Journal of Portfolio Management and the Roger F Murray Prize (First Place) awarded by the Institute for Quantitative Research in Finance. He is on the board of the International Association for Quantitative Finance, the Board of The Institute for Quantitative Research, and the Editorial Advisory Board of the Journal of Portfolio Management. He served for three years as President of the Society of Columbia Graduates.