By Matthew Sallee, CFA, President, Tortoise.

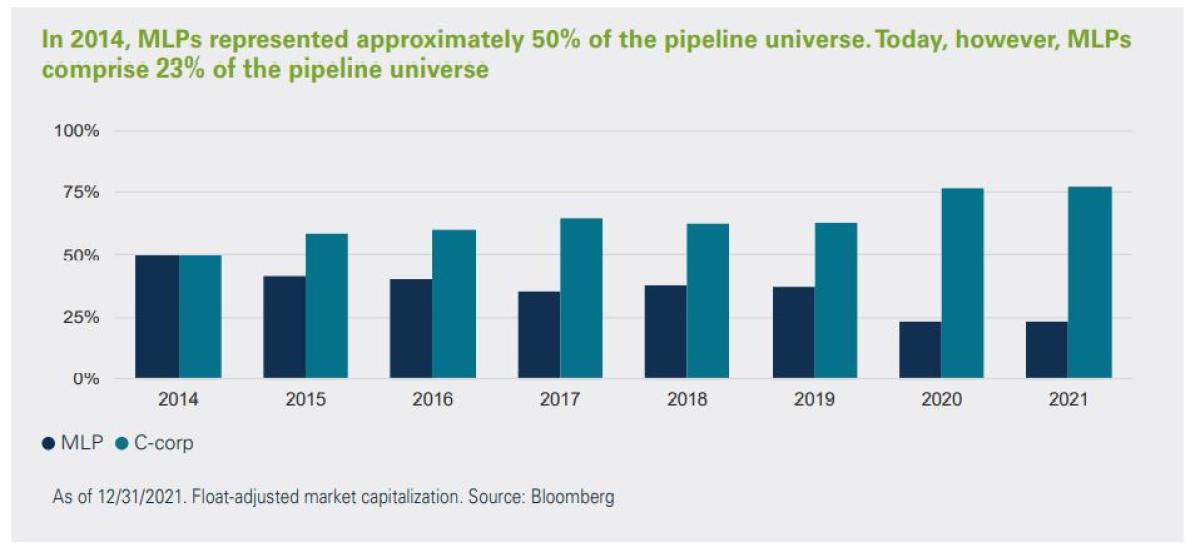

The midstream energy sector has undergone major changes in recent years and it’s become increasingly difficult to achieve a passive diversified MLP-only portfolio. At the end of 2021, MLPs only represent approximately one-quarter of the total midstream market cap. Sector dynamics have shifted as many simplifications/mergers have occurred, sources of capital have changed, tax reform plans were put into effect (both broad and industry specific) and regulations continue to evolve. Midstream energy companies can be structured one of two ways: as a Master Limited Partnership (MLP) with no corporate tax, or as a C-Corp, a traditional taxable corporation. At TortoiseEcofin, we’re firm believers in the fundamentals of pipeline companies, regardless of the corporate structure. We think that an all-inclusive pipeline index may more accurately represent the risk/return profile that investors are looking for.

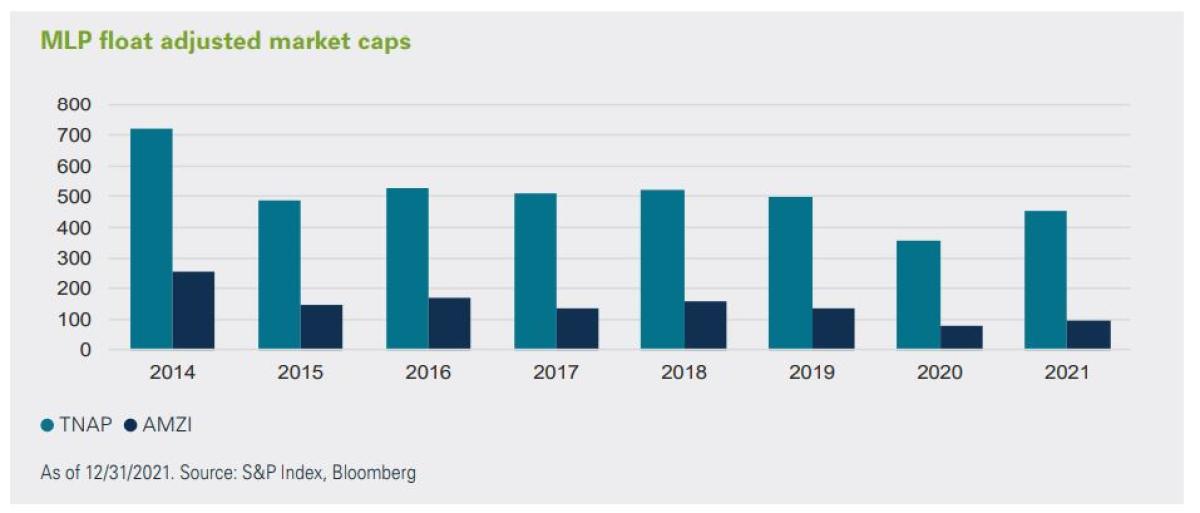

While MLPs have become synonymous with midstream energy, the pipeline universe is much broader. At the end of 2021, Alerian MLP Infrastructure Index (AMZI) constituents, which consists of midstream MLPs, had a market cap of $165 billion and a float adjusted market cap of only $83 billion. The Tortoise North American Pipeline IndexSM (TNAP), which consists of MLPs and c-corps had a market cap of $553 billion and a float adjusted market cap of $453 billion.

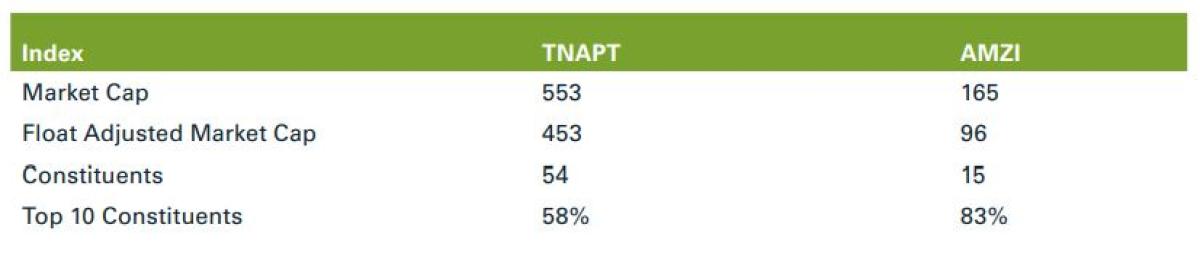

The table below highlights key characteristics between AMZI and TNAP indices.

A quick assessment of the liquidity of the MLP asset class can further emphasize the relative size of the space in 2020. Based on existing AMZI constituents, and assuming 25% of volume is reasonable, approximately $25 million is tradeable in a single day based on the liquidity of the individual AMZI constituents. With more than $10 billion in passively managed MLP products there is significant potential risk and enhanced volatility since even only 2-3% of the money coming out could very easily create a liquidity event. There is more to midstream energy investing than just MLPs, and TNAP is our representation of the complete midstream universe. With 54 names in TNAP compared to only 15 names in the AMZI, investing in the broad midstream sector provides a more diversified portfolio with significantly less concentrated exposure and more market cap.

In addition to the benefits provided by a much larger and more diversified universe, midstream indices with a broader strategy have historically provided better returns, lower volatility and thus better risk adjusted returns.

While current valuations and strong market fundamentals are attracting investors into the midstream space, we think it’s important to pay attention to the changing dynamics and how it might affect indices and the passive products that track them. A product with broader midstream exposure has historically provided investors greater diversification, lower volatility and higher total and risk-adjusted returns.

About the Author:

Mr. Sallee joined the firm in 2005 and is an Executive Committee member and a member of the Tortoise Development Committee and serves as President of the Tortoise platform.

He oversees Tortoise’s energy investment team and Tortoise/Ecofin co-managed energy products. Mr. Sallee serves as president of the Tortoise Energy Infrastructure Corp. and Tortoise Midstream Energy Fund, Inc. closed-end funds, and is a member of the Investment Committee. He has more than 21 years of industry experience and regularly speaks on national media (CNBC). Previously, he served for five years as a senior financial analyst with Aquila, Inc., where he was responsible for analysis of capital allocation at the firm’s communications infrastructure subsidiary, Everest Connections. Mr. Sallee serves on the National Board of Directors of the Gabby Krause Foundation an organization, dedicated to bringing joy, laughter and relief to children fighting life threatening disease. Mr. Sallee graduated magna cum laude from the University of Missouri with a degree in business administration. He is a CFA® charterholder.

Original Article: choosing-the-right-index-for-midstream-energy_12312021.pdf (tortoiseecofin.com)