By Peter Shepard, Managing Director, Head of Analytics Research and Product Development MSCI; Grace Qiu Tiantian, Senior Vice President, Total Portfolio Policy & Allocation, Economics & Investment Strategy GIC; and Ding Li, Senior Vice President, Total Portfolio Policy & Allocation, Economics & Investment StrategyGIC.

Our joint paper with MSCI introduces an asset-allocation framework that aims to help investors build greater resilience into their portfolio against continued macro uncertainties.

Instead of relying on short-term, backward-looking measures of risks, we map out five potential macro scenarios for the decades ahead and analyze how they could potentially play out across different asset classes and time horizons.

Our case study looks at how the macro-resilient portfolio, based on this long-horizon framework, can mitigate long-term macro risks while maintaining the same level of expected returns as a portfolio optimized to a shorter horizon.

Long-term investors face two major shifts in the investment environment. One has been steadily building, while the other has materialised suddenly: We are witnessing the rise of private assets to the core of many asset allocations from a peripheral “alternative,” and we have entered a new period of heightened macro uncertainty. Both could require a fundamental evolution of the asset-allocation process.

Decades of moderate inflation and falling interest rates have given way to higher inflation and interest rates. Other secular forces, such as climate change and deglobalisation, are also transforming the investment environment to one unlike any we have experienced before. These regime shifts suggest the need for a fundamentally forward-looking asset-allocation process.

Today’s investors also face an investment universe that is quickly expanding beyond traditional public equity and bonds. Private assets have often promised investors higher returns and lower risk, but their opaque valuations and limited history have made them hard to evaluate and incorporate into the asset allocation process alongside public markets.

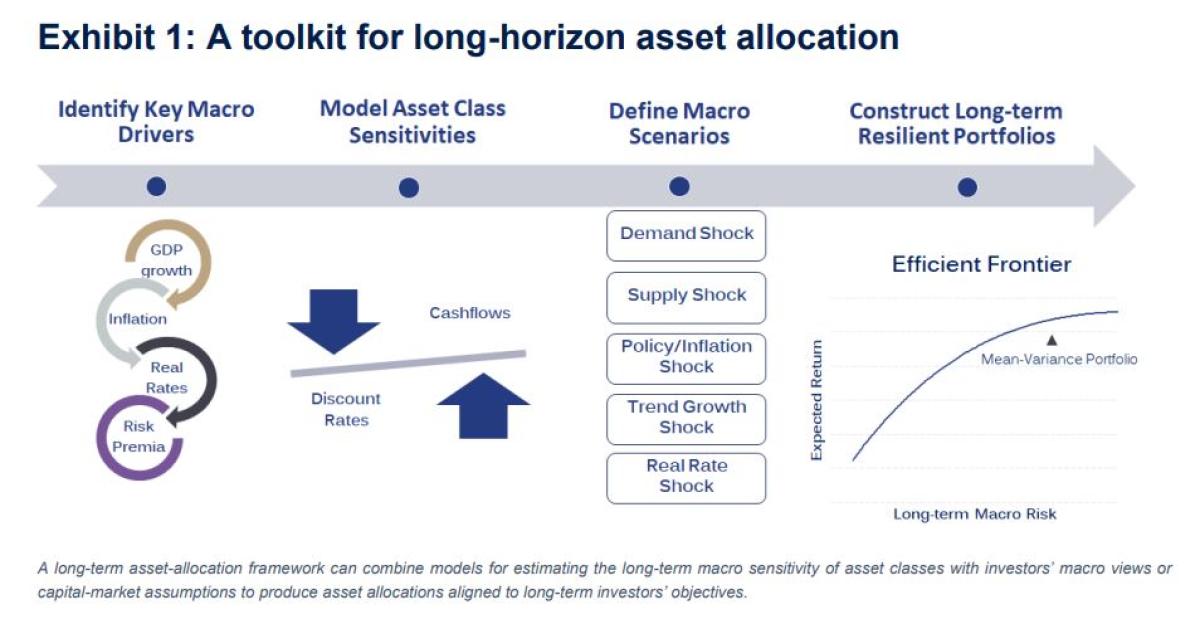

In this paper, MSCI and GIC introduce an asset-allocation framework to help investors navigate a new regime. We start by moving away from short-term, backward-looking measures of risk to tools for understanding the macro risks that could dominate the coming decades, and how they may play into asset returns over long horizons. Some of these macro risks — including supply-driven inflation, a less-credible central bank, rising real rates and slowing productivity growth — were modest risks in recent decades but could significantly change the trajectory of the markets in the years ahead.

We use five potential macro scenarios to demonstrate a framework for constructing asset allocations aimed to be more robust to long-term risks. By putting less emphasis on reducing backward-looking, short-term risk, allocations can instead prioritize resilience to potential macro uncertainties, while preserving the same level of investors’ long-run expected returns. In addition, placing public and private assets on the same footing can help manage long-term risks and returns across the total portfolio.1

The macro-finance framework we use differs from traditional, statistically based risk measures in four main ways:

- First, a long-horizon view aligns with many institutional investor mandates — to meet liabilities and preserve wealth over the long run — instead of trading off short-term risk and return.

- Second, by relating investors’ cash flows and discount rates to a common set of macro drivers, the macro framework provides an intuitive and consistent view spanning all asset classes.

- Third, the macro framework can project asset returns through a range of time horizons, making it potentially useful for both strategic and tactical portfolio positioning.

- Last, the framework may aid decision-making that considers potential new macro environments that may emerge, rather than optimizing relative to the previous market regime.

This paper is organized as follows:

- First, we explain why a cash-flow-based, long-term view of risk may be useful for investors’ strategic asset allocation process, describe new tools to estimate macro risk and introduce the five potential scenarios that may shape the macro regime in the decades ahead: shocks to demand, supply, trend growth, central bank policy and long-term real rates.

- Second, we analyze how these macro scenarios could play out across different asset classes and time horizons and highlight the key features of the investment landscape faced by long-term investors. We discuss how discount-rate shocks, mean reversion, shocks to trend growth and regime shifts could have starkly different effects for short-horizon versus long horizon investors.

- Last, we demonstrate a systematic asset-allocation framework that incorporates a view of the long horizon investment landscape, with a case study of asset allocations aiming to be more macro-resilient. We illustrate some potential benefits and costs of replacing short-term volatility with such long-term risk measures and explore the implications for long-term investors.

Redefining risk for long-term investors

Long-term investors aim to meet their liabilities and maintain the purchasing power of their wealth far into the future, but they have often made decisions based on the backward-looking, short-horizon behavior of asset returns. Such a view tends to suggest that stocks are very risky, bonds behave like insurance and private assets are low-risk and mildly correlated. Allocations typically have followed accordingly, including large allocations to fixed income even as real yields went negative.

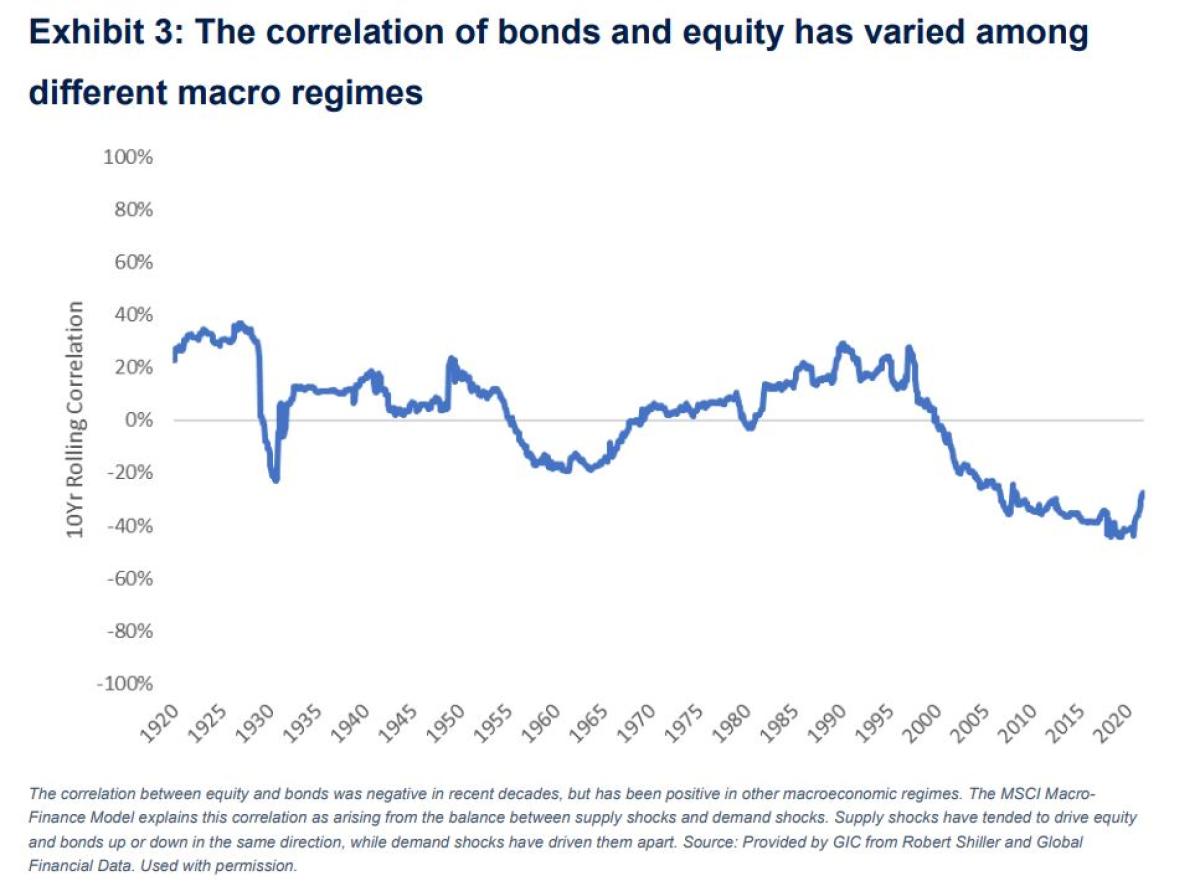

The outlook for long-horizon investors, however, may be very different from what conventional wisdom suggests. Although bonds tended to act as a hedge to equity when demand shocks were the dominant macro risk, bonds have typically moved down together with equity in response to supply shocks, when the threat of inflation superseded the central bank’s aim of fighting recession. Further, the low volatility and correlations of private assets are largely artifacts of their smooth valuations, rather than reflecting a lack of systematic risk.

Despite these challenges, significant opportunities may remain for long-horizon investors. Private assets are not uncorrelated over a long horizon, but their spectrum of exposures to macro risks may enable them to be used to help manage long-term risks across the total portfolio. In addition, while equity is highly volatile over a short horizon, volatility driven by fluctuating equity risk premia may be much milder for the long-horizon investor.

The use of backward-looking statistics may be increasingly ill-suited to the challenges facing long-term investors today, who need a framework to understand and manage the risks and return opportunities they face across all asset classes.

This paper introduces a framework to understand the long horizon risks and returns of all asset classes by relating their prices to uncertain future cash flows sensitive to the overall economy and discounted with a combination of real rates and market-dependent premia. This view provides a direct connection between the assets in the portfolio and the long horizon investor’s objectives — sustained cash flows and spending power — and it enables projections into the new macroeconomic regimes that may prevail in the years ahead.

The macro view connects an ancient concept in finance — the discounted-cash-flow model — to a framework for understanding how assets’ cash flows and discount rates may change with the macro regime.

Among a wide range of possible macro scenarios, we identify the key factors driving long-horizon risks and returns across asset classes, each represented by a downside scenario2 :

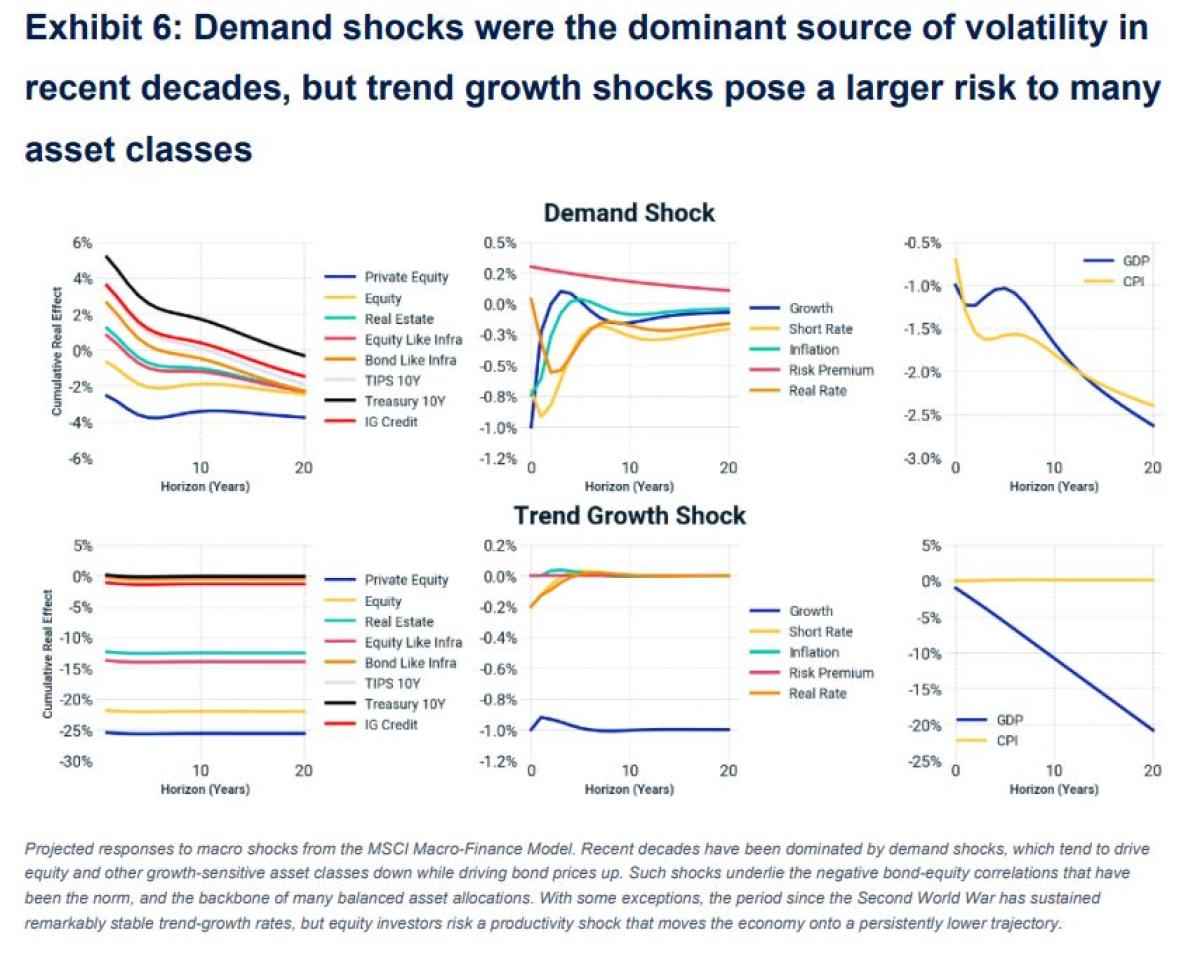

- Demand shocks: Growth, inflation and real rates are driven down together by decreasing economic demand. Demand shocks were the primary source of market volatility in most developed markets in the past two decades and were responsible for the negative correlation between equities and bonds.

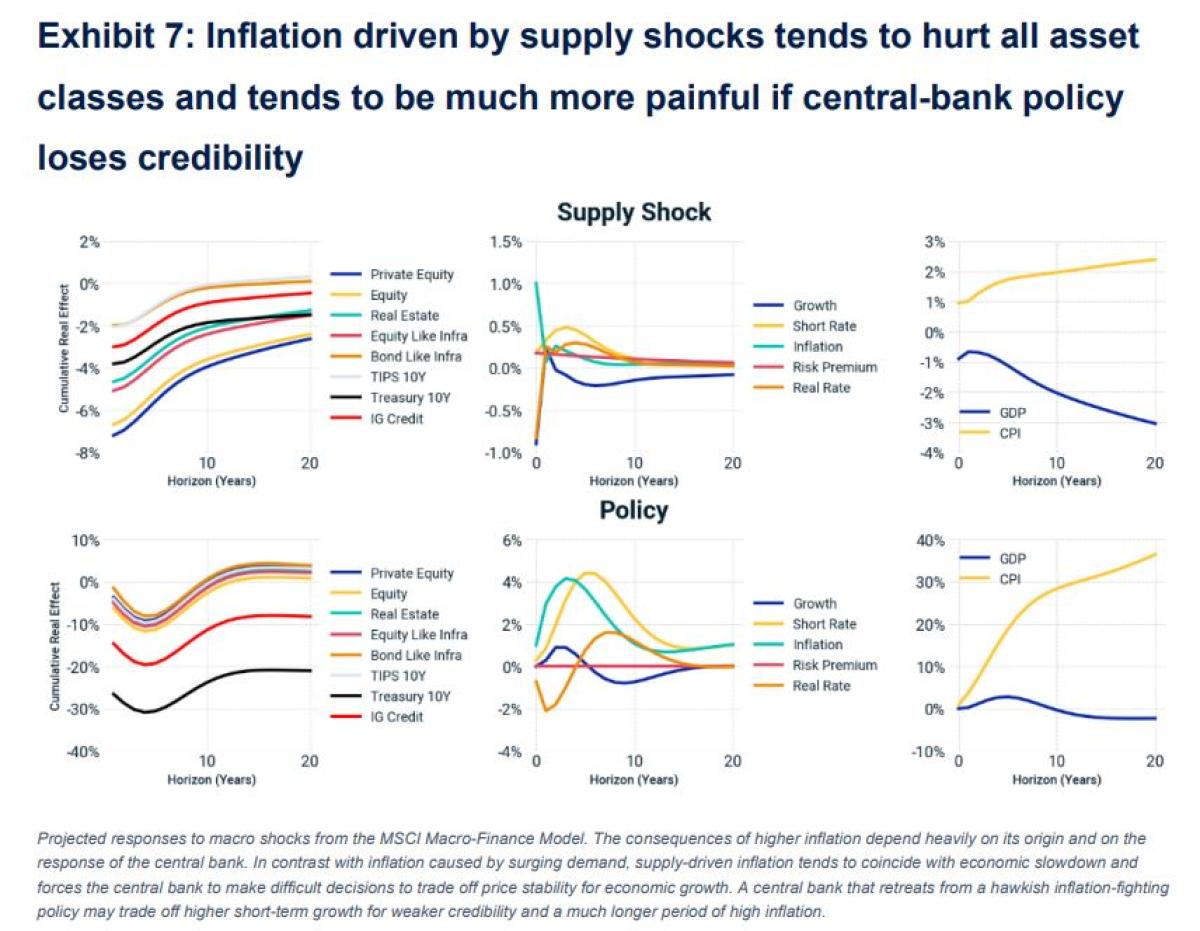

- Supply shocks: Decreasing economic supply drives growth down while inflation and rates rise. Supply shocks drive equities and bonds down together, as in the stagflation period of the 1970s.

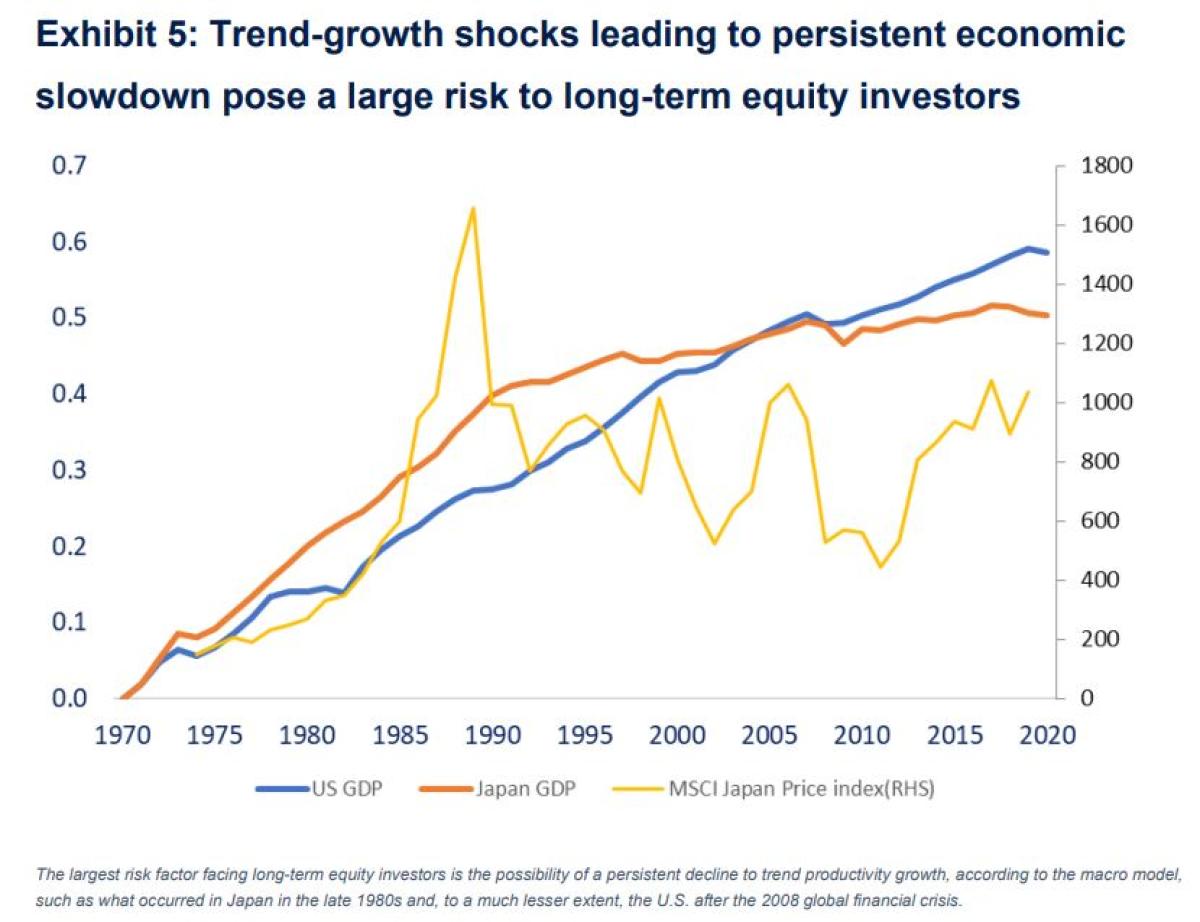

- Productivity shocks: Trend growth slows, moving the economy to a lower-growth path that persists for many years. Although growth slows only moderately in the short term, the cumulative effect of lower growth year after year is a much smaller economy and much smaller cash flows to growth-sensitive assets. Such a scenario could describe the end of Japan’s explosive growth in the 1980s and, to a lesser degree, the aftermath of the 2008 global financial crisis. However, it may pose a significantly larger risk to the global economy than was the case during the economic boom that has taken place since the Second World War.

- Policy shocks: The central bank becomes less willing to cool the economy to control inflation and, in turn, becomes less credible. Weaker central-bank policy results in higher short-term growth, but the loss of credibility creates a cycle of higher inflation that lasts for years before eventually being brought under control with a Volcker-like recession. Nominal bonds suffer large real losses, while other assets suffer more mildly through the doldrum years, during which inflation is brought back under control.

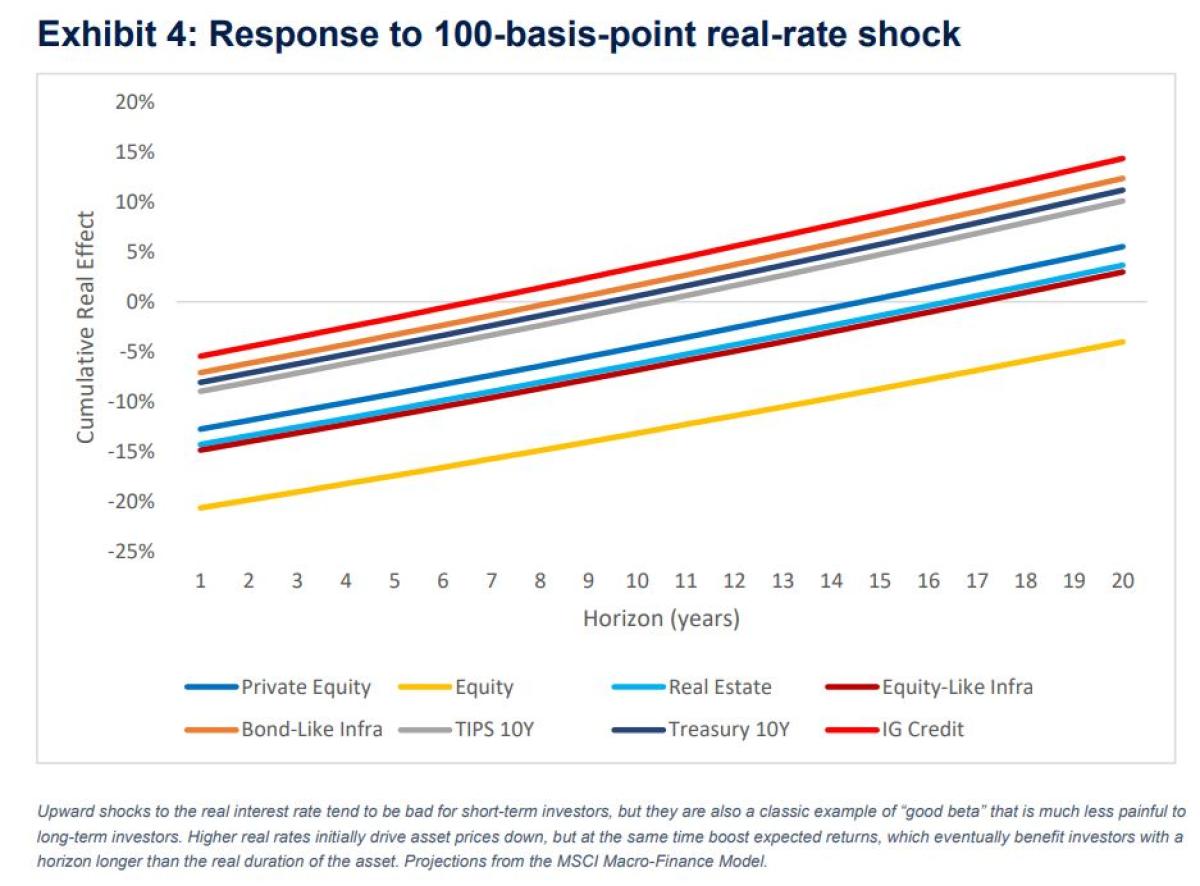

- Real-rate shocks: The secular trend of decreasing real rates reverses. Immediate losses across asset classes are accompanied by higher expected returns, which ultimately benefit long-horizon investors.

The past decades were largely dominated by demand-shock volatility against a background of secularly declining real rates. In the future, however, any of the five macro scenarios could loom large, and each represents a different source of systematic risk to a long-term investor.

However, because the effects of these macro influences differ widely — across asset classes and time horizons and compared to what has dominated in the past — they also represent an opportunity for long-horizon investors to balance risks across assets classes and to take advantage of their long horizon. We introduce a framework to model these long-horizon macro dynamics and account for them in the asset-allocation process.

Insights from a macro view

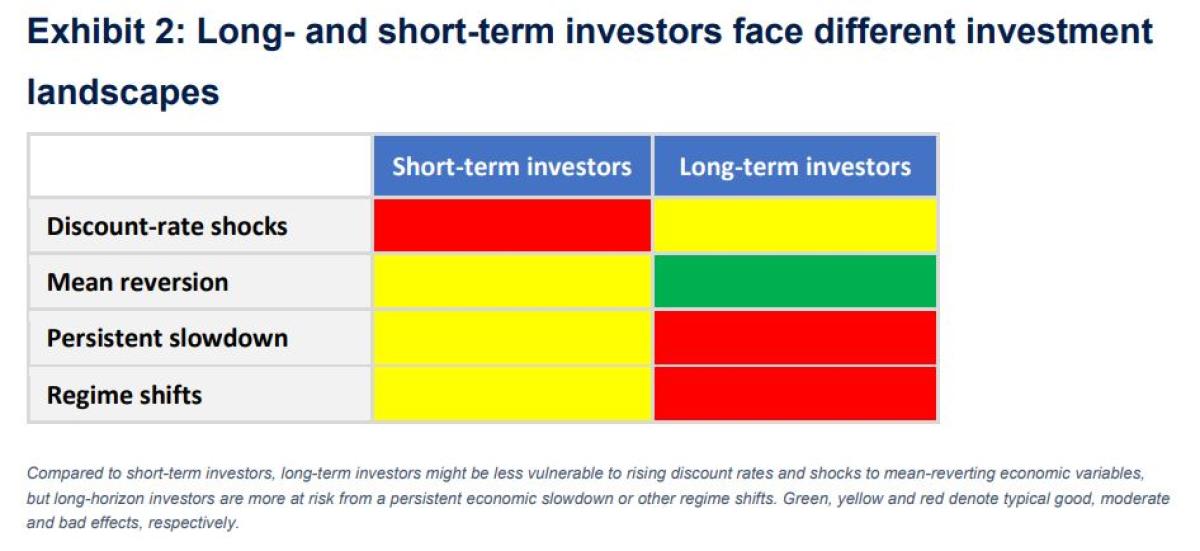

Long-term investors do not face the same investment landscape as the short-horizon investor, so the former may benefit by shifting their risk-return trade-offs to allocate away from risks that matter more to them, while taking on more of the return opportunities that are riskier to short-horizon investors.

We identify four market dynamics — particularly discount-rate shocks and mean reversion — for which a long investment horizon tends to be beneficial, as well as other dynamics to which long-horizon investors are more vulnerable — secular changes and regime shifts — and explore how different asset classes bring exposures to each.

Incorporating these long-term dynamics into the investment process requires understanding how the cash flows and discount rates of each asset class are exposed to the macro factors driving the long-horizon investment landscape. Rather than falling into simple growth/inflation buckets, such as equity to growth or real assets to inflation protection, macro sensitivities cut across all asset classes. Every asset class has a different degree of sensitivity to macro shocks of all kinds.

The consequences of growth or inflation also depend critically on the underlying causes in supply, demand or productivity shocks, as well as on the response and credibility of the central bank. The positive rates-equity correlation that prevailed in recent decades can be understood as caused by the dominance of demand shocks in that era. A demand shock tends to drive growth and interest rates up or down together, but a return of supply shocks or degradation of central-bank credibility could take away the benevolent rates-equity correlation and undermine a key pillar of balanced asset allocations.

Both cash-flow and discount-rate shocks hurt the short-term investor, but a discount-rate shock is much less painful to the long-horizon investor. Higher discount rates typically lead to lower asset prices in the near term, but by definition they subsequently lead to higher expected returns. A long-horizon investor benefits by harvesting the higher returns and can eventually come out better off in the long run. Discount-rate risk therefore tends to be much more benign to a long-horizon investor than to a short-horizon investor — an example of the concept of “good beta/bad beta.”3

Many macro-financial variables, including the equity risk premium, short-term growth, corporate-profit ratio and inflation,4 have historically exhibited some tendency to mean-revert toward the neighbourhood of an equilibrium level. As a result, shocks to mean-reverting variables tend to be short-lived, contributing to short-term volatility much more than long-term risk. Mean reversion can also be the basis of systematic strategies that seek to profit as macro variables move back toward equilibrium.

Notably, the equity risk premium may stand to benefit from both “good beta” and mean reversion, giving equity a very different risk profile for the long-horizon investor. Fluctuations in the equity premium drive short-term volatility, but long-term equity investors who are able to ride out large fluctuations in the equity markets may be able to harvest higher expected returns after premium-driven market crashes. Equity volatility does not always correspond to risk for long-term investors.

What matters much more for long-term equity investors is the long-term path of the economy.

While a long horizon may help investors with the first two dynamics above (shocks to discount rates and mean-reverting macro variables), long-term investors have greater exposure to the risk of a persistent economic slowdown — a trend growth shock. A persistent shock to growth may have only small, short-horizon effects, but can build up gradually to significantly impact the long-horizon investor.5 Fluctuations in the economy from quarter to quarter are very visible, but the risk of a persistent economic slowdown is a greater source of uncertainty. Such a slowdown occurred in Japan in the late 1980s and, more mildly, in the U.S. after the 2008 global financial crisis. Large shocks to trend growth were, however, remarkably rare during the “economic miracle” that took place in many economies for decades after the Second World War. If trend growth were projected to be as stable in the decades ahead as it has been in the past, then long-horizon investors could invest in equity with relatively low risk to their long-term spending power.

Unfortunately, there is no guarantee that growth will continue at the same rate, and trend growth is a primary risk facing long-term investors in equity and other growth-sensitive asset classes.

Long-term investors are also more exposed to a fourth type of risk — regime shifts. As investors look to a longer horizon, it becomes increasingly important to consider a range of possible regimes beyond what is reflected in backward-looking data.6

Today, potential regime shifts include the effects of deglobalization and the decarbonization of the economy, and many investors are considering the possibility that new levels of high inflation could persist and worsen into stagflation.

The high inflation of 2022 has been notable not only for its magnitude,7 but for its origin in supply shocks, which tend to drive inflation higher and growth down, forcing the central bank to choose between controlling inflation and stimulating recovery. An initially slow policy response further led to doubts about central banks’ commitment to stabilizing inflation.

The consequences for investors could be wide-ranging. Central banks’ primary mechanism for fighting inflation is to raise interest rates to cool the economy. A supply shock in the context of strong central-bank policy would typically hurt all asset classes through both higher discount rates and, more importantly for long-term investors, lower cash flows. If central banks instead accommodate higher inflation to avoid recession, they would run the risk of losing credibility, which could create a protracted period of high inflation and require even more painful measures to eventually control inflation. Either of these scenarios would likely lead to the end of the benevolent rates-equity correlation that has effectively provided a hedge between the bond and equity components of balanced portfolios.

xx

Footnotes:

1 In practice, few investors have the luxury to be completely immune to short-term pressures. This framework focuses on the idealized, pure long-horizon investor, while recognizing that, in practice, most long-term investors would likely seek some intermediate balance with short-term objectives. The aim of this note is not to recommend a particular asset allocation for long-term investors, but to introduce a new set of tools for these investors to use.

2 These factors were chosen to reflect the most important drivers of long-term returns across asset classes. Among many possible drivers of asset class returns, these were selected for their importance across asset classes, time horizons and market regimes. This paper focusses on a single downside for each of these factors, but the framework can incorporate a wide range of upside and downside scenarios for these factors and other macroeconomic scenarios.

3 Campbell, John Y., and Vuolteenaho, Tuomo (2004). “Bad Beta, Good Beta.” American Economic Review 94, no. 5: 1249-1275.

4 Mean reversion of inflation is much more tenuous than the other examples. In the MSCI model, described in the appendix, inflation is mean reverting as long as the central bank is credible, but inflation can run away if that credibility breaks down.

5 An important subtlety for trend shocks is that although the trend plays out over a long horizon, market expectations may change much more quickly. Our model distinguishes these with separate factors to reflect the long-term trend and changing market expectations about the trend. The latter can be a significant source of short-term volatility, as markets may quickly price in changes to long-term expectations.

6 It is always possible to find ourselves in a fundamentally different economic or financial environment from one day to the next, but each day usually looks more like the previous. As we look to longer and longer horizons, however, the likelihood of a regime shift increases, and we would be surprised if the next decade is not significantly different from the previous.

7 In contrast to 2022, the inflation observed in 2021 was likely mostly demand-driven, a byproduct of the high growth that came with the pent-up demand released as pandemic restrictions eased and stimulus took effect. This was largely consistent with the macro environment that prevailed in the preceding decades.

About the Authors:

Grace Qiu Tiantian, Ph.D., joined GIC in 2013, is a Senior Vice President in the Economics and Investment Strategy (EIS) Department.

Grace has deep expertise in total portfolio design and extensive industry experience in both public and private (alternative) market asset classes. She published multiple research papers on asset allocation in Industry leading journals including the Financial Analysts Journal and the Journal of Portfolio Management. Prior to this role, Grace has worked as a portfolio manager in the Real Return Program in EIS, leading effort in alternative risk premia (style premia) portfolio across equity, fixed income, commodity and FX.

Before joining GIC, Grace held several roles in investment banking industry, as Emerging Market FX and Rates strategist. She covered Latin America and Asia Pacific markets in Goldman Sachs New York and HSBC Hong Kong, respectively. Grace holds a Bachelor’s degree of Mathematics from Cornell University and Ph.D. in Economics from Harvard University.

Ding Li is a senior vice president in the Economics and Investment Strategy Department (EIS) at GIC Private Limited in Singapore.

He works in the Total Portfolio Policy & Allocation division of EIS, focusing on portfolio construction, multi-asset modelling and quantitative research, and leads the implementation efforts on total portfolio analytics. He previously worked as an investment analyst at the CPP Investments in Toronto, Canada. He has a Master in Mathematical Finance from the University of Toronto.

Peter Shepard is Head of Analytics Research and Product Development at MSCI. He leads a team of researchers responsible for MSCI’s RiskManager and Barra platforms used by institutions in managing upward of USD 20 trillion in assets. The team researches factors, systematic strategies, portfolio construction, liquidity, machine learning, climate and macro models across equity, fixed income, private assets and digital currencies. Peter also sits on MSCI’s executive committee and the board of directors of Burgiss.

Peter received a Ph.D. in theoretical physics from the University of California at Berkeley, where he researched string theory and the quantum theory of gravity. He has publications in theoretical physics and finance. Peter also holds a bachelor’s degree in physics and mathematics from Brown University.

Acknowledgements: The authors thank William Baker, John Burke, Daniel Luo, Chenlu Zhou and others for their valuable contributions to this work.