By Chung-Hong Fu, Ph.D., Managing Director Economic Research and Analysis, Timberland Investment Resources, LLC.

Introduction

During the early months of the Covid-19 pandemic, and despite the broad-based economic fallout that ensued, North American lumber markets (markets for building materials like 2 x 4s used for construction framing) experienced historic gains. After hitting a low point in April 2020, lumber prices more than doubled by July and broke all-time records in August. The price surge was due to a surge in home improvement spending by homeowners who were sheltering-in-place because of the coronavirus outbreak. In addition, a rapid recovery in the rate of new home construction during the period added to the heavy demand for structural-grade lumber.

Regardless of the cause, timberland investors have expressed curiosity about how such large swings in lumber prices (the finished products produced from the timber that is grown on their timberland assets) are likely to influence the performance of their portfolios. This paper assesses the link between lumber price and timber markets – which, in turn, naturally affect timberland investment performance. It explores two questions: If lumber prices surge, is it a sign to go long or short on timberland? Or, are lumber market movements irrelevant in making good investment decisions with regard to one's exposure to timberland?

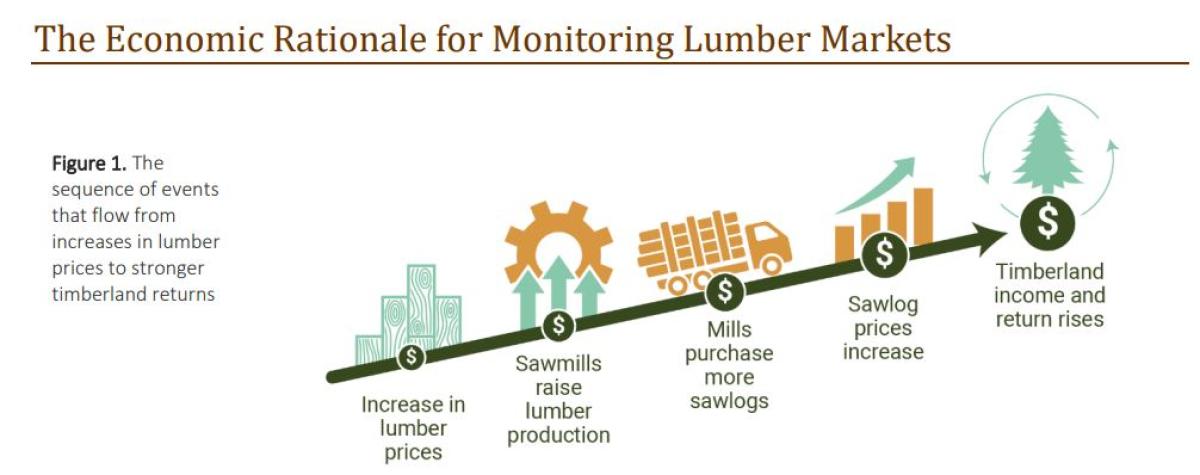

In theory, there is an economic basis for timberland investors to pay close attention to lumber prices. The typical chain of events that occur when lumber prices increase is illustrated in the diagram above (Figure 1). The logic is as follows: (1) higher lumber prices prompts sawmills to increase lumber production to profit from the higher prices; (2) in order to raise output, mills purchase more sawtimber, which are logs greater than 8 inches (20 centimeters) in diameter; (3) timberland owners are willingto sell more timber if mills are willing to pay higher prices for their logs; and (4) the end result is that higher sawtimber prices improve the harvest income and capital appreciation generated by a timberland investor's assets.

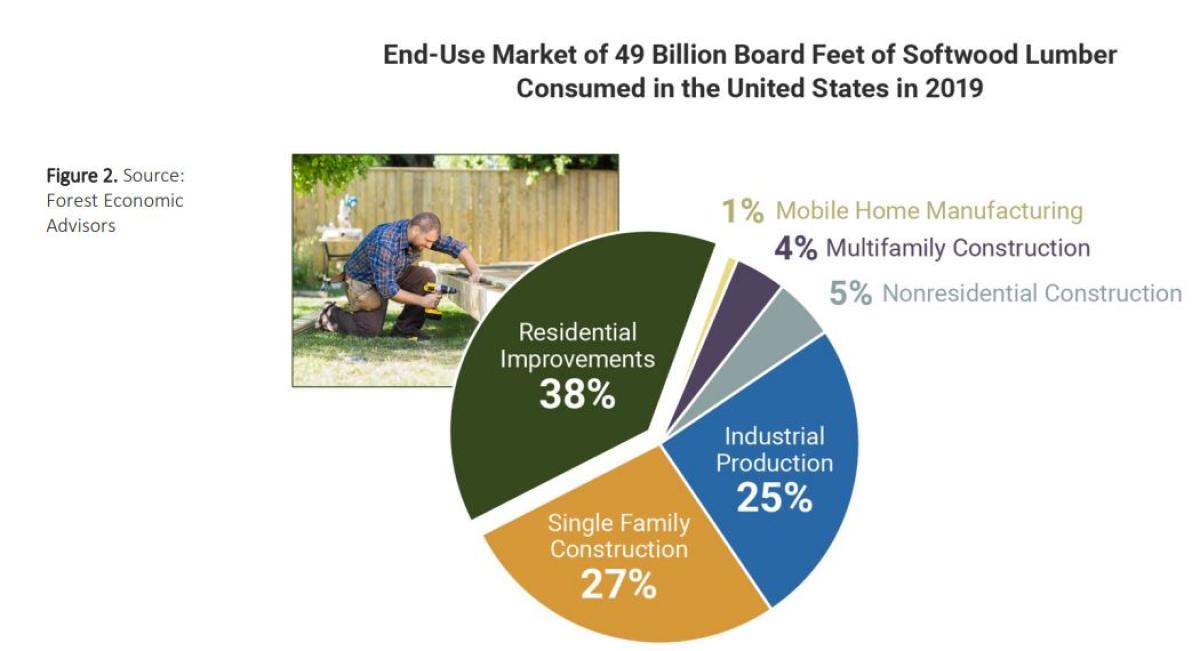

In the case of the United States, and as the pie chart below illustrates, lumber markets are largely driven by residential construction. In fact, new home construction in combination with home repair and remodeling make up more than two-thirds of lumber consumption in the United States.

Confirming whether this theory that lumber demand and price increases have an effect on timber markets and, by extension, timberland returns, requires a statistical analysis of historic market data.

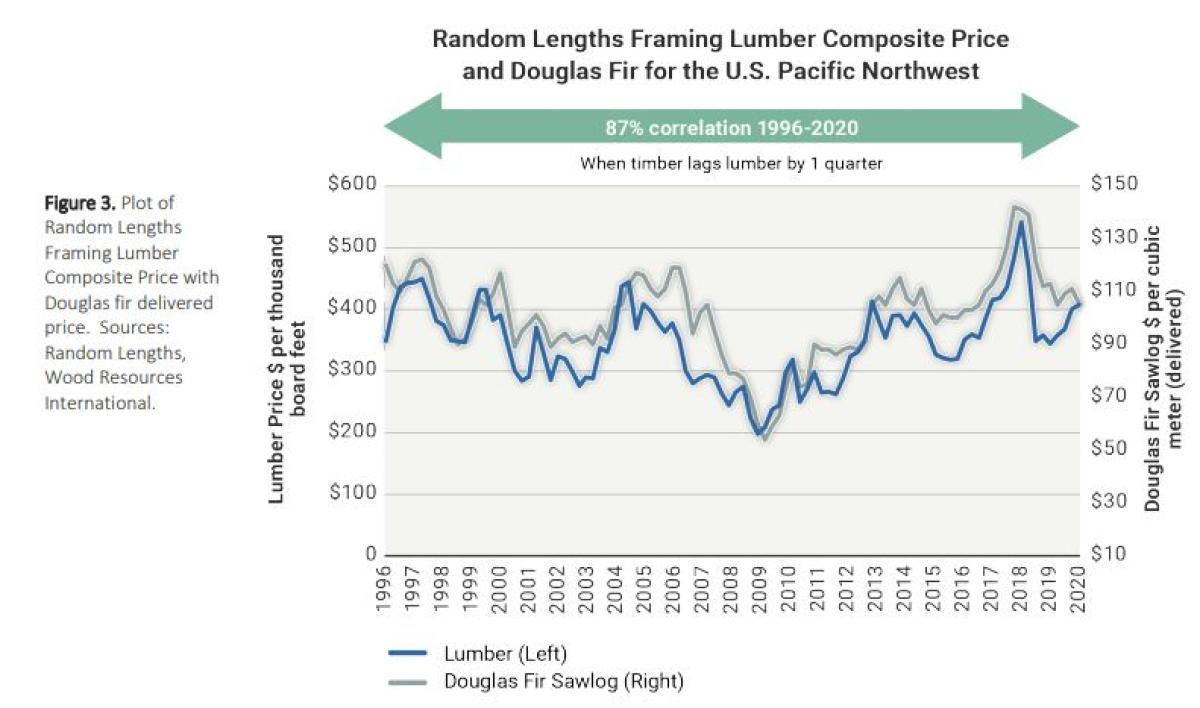

Assessing the Link Through Market Evidence Before we look at that data, however, it is best to define the market. Lumber that is used to build, repair and remodel homes is structural-grade lumber made from softwoods – a classification of trees that feature needle-like leaves but lack flowers. The long fibers of softwood trees are what provide lumber with the load-bearing strength required for many types of construction, such as house framing. The two major regions of the United States that produce softwood lumber are the South and the Pacific Northwest. Plotting Lumber and Timber Prices Upon examining a plotting of lumber and timber prices for the Pacific Northwest and South (Figures 3 & 4), a clear relationship becomes evident. For the Pacific Northwest, there are a variety of commercial softwood species that are used to make lumber, but Douglas fir is often considered the bellwether. When Random Lengths Framing Lumber Composite Index is plotted with the delivered price of Douglas-fir for the past 25 years, it is clear they are closely related (Figure 3).

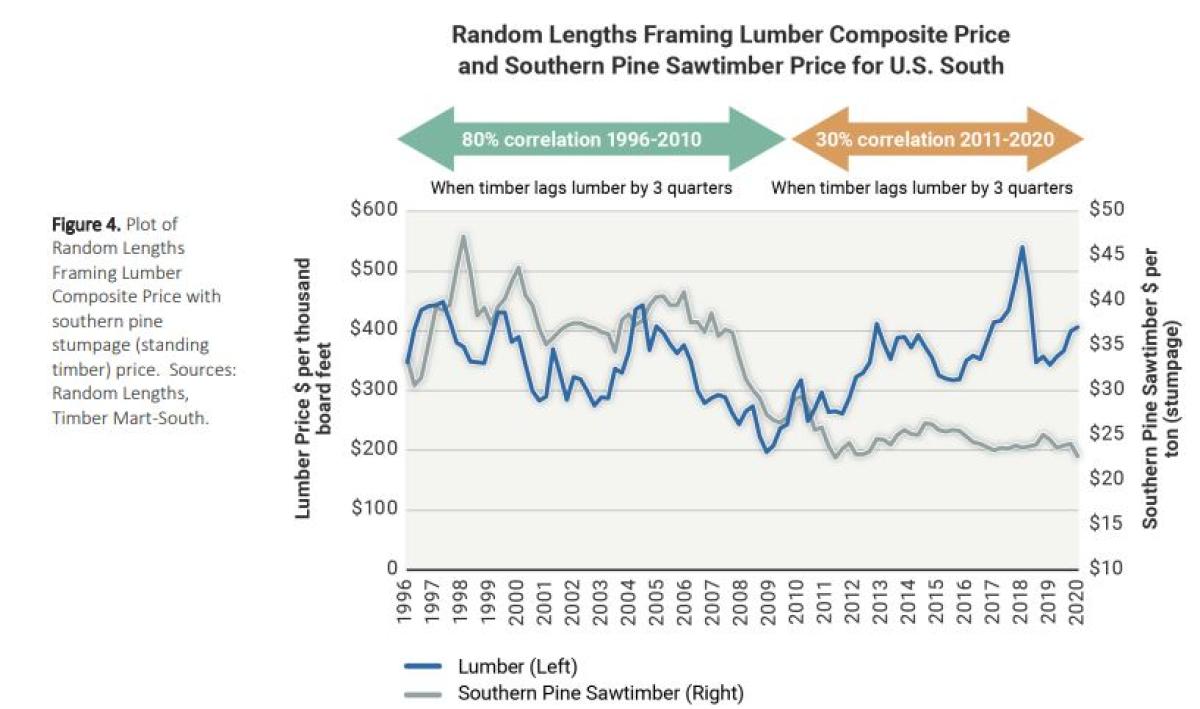

In the South, however, the pattern is different (Figure 4). It is easy to see that southern pine sawtimber prices trended in alignment with national lumber prices before 2010, but a disconnect between lumber markets and sawlog markets in the South became apparent following the Great Financial Crisis (GFC) of 2007-2008. A fundamental change occurred post-GFC that made sawtimber markets in the region largely unresponsive to lumber prices. We will investigate that market dichotomy in greater depth in the following section of this paper.

Correlating and Quantifying Linkages Between Lumber and Timber Markets

The visual relationships between lumber and timber prices that we see in the preceding charts can be quantified. A statistical measure known as correlation can gauge how closely two prices (or any other variable) can track each other. If they move in perfect unison, then the correlation value is 1.0 (or 100 percent). If they move independently from each other, then the correlation is zero (0). By extension, a negative correlation number indicates movement in opposite directions.

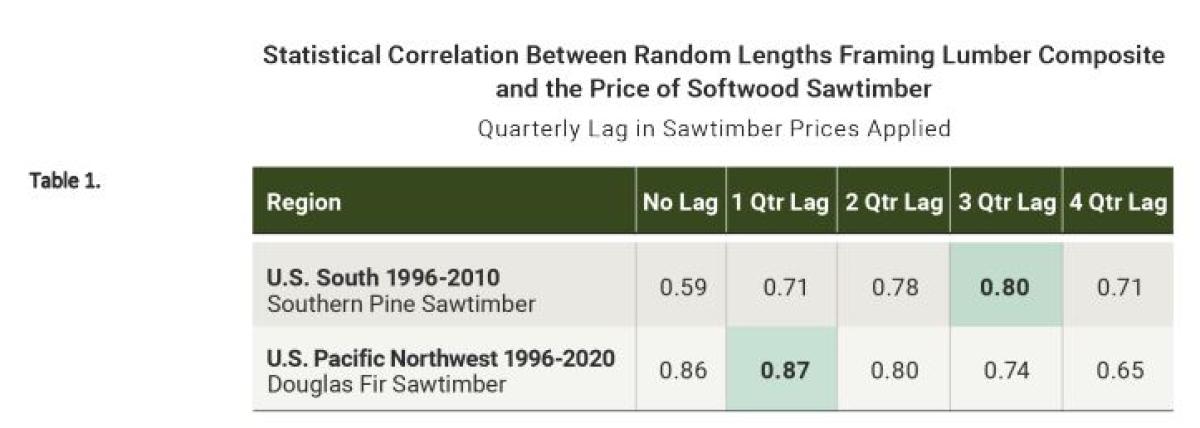

For purposes of this analysis, we calculated the statistical correlation between lumber prices and log prices. Quarterly lags were added to timber prices to test whether a delayed effect exists between lumber and timber markets. The results, as shown in Table 1 below, indicate that there is, indeed, a significant relationship between lumber and timber prices. For the South, before 2010, the relationship was strongest with a correlation of 0.80 when sawtimber prices lagged lumber by three quarters. In the case of the Pacific Northwest, the correlation was highest at 0.87 with a one quarter lag.

The lag effects just referenced can be explained, in part, by inventory conditions at sawmills. Many lumber manufacturers hold several weeks of finished lumber at their mill sites before shipping their products to market. Furthermore, mills often hold inventories of raw logs in their wood yards for several weeks prior to using them to produce lumber. Maintaining inventories of both logs and lumber creates a buffer of several weeks before mills need to raise timber prices to purchase more logs.

The greater lag in the South of three quarters compared to the Pacific Northwest’s single quarter may be explained by the structures of the two markets. The Pacific Northwest market largely operates on a "delivered log" model. This means timberland owners are responsible for harvesting and then transporting their timber to mills in the region. In contrast, in the U.S. South, markets largely operate on a "stumpage" model. With the stumpage model, it is the responsibility of the mill, or an independent logger who serves as an intermediary, to buy and harvest standing timber from forestland owners and to transport it to the log yards of the mill or mills that intend to use it to manufacture lumber. When a mill or independent logger purchases standing timber from a forestland owner, the purchase contract (or "stumpage contract") normally provides a 12-to-18-month window within which to harvest and haul the timber. This means it can take as long as a number of months before shifts in lumber markets are actually reflected in how mills may bid for a landowner’s timber.

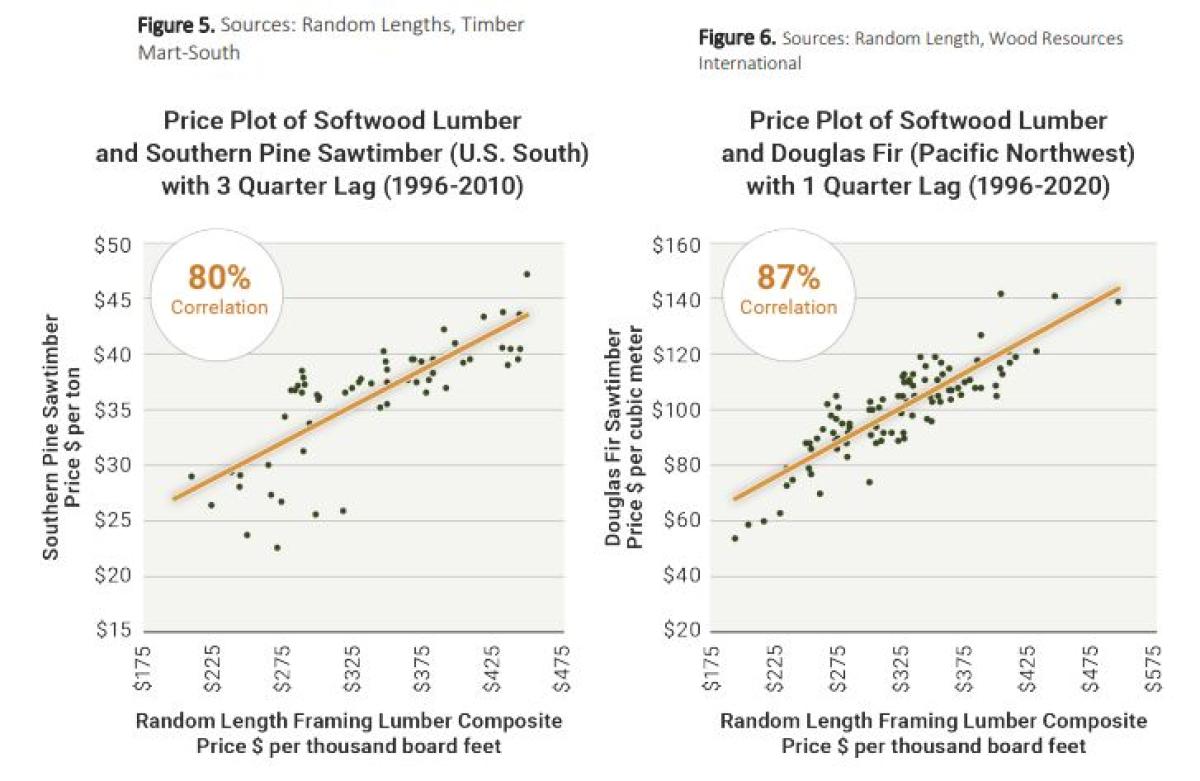

To better visualize this market linkage, the charts in Figures 5 & 6 show lumber prices plotted against timber prices for the South and Pacific Northwest using a quarterly lag that provides the highest correlation. A regression line was added to better define the link.

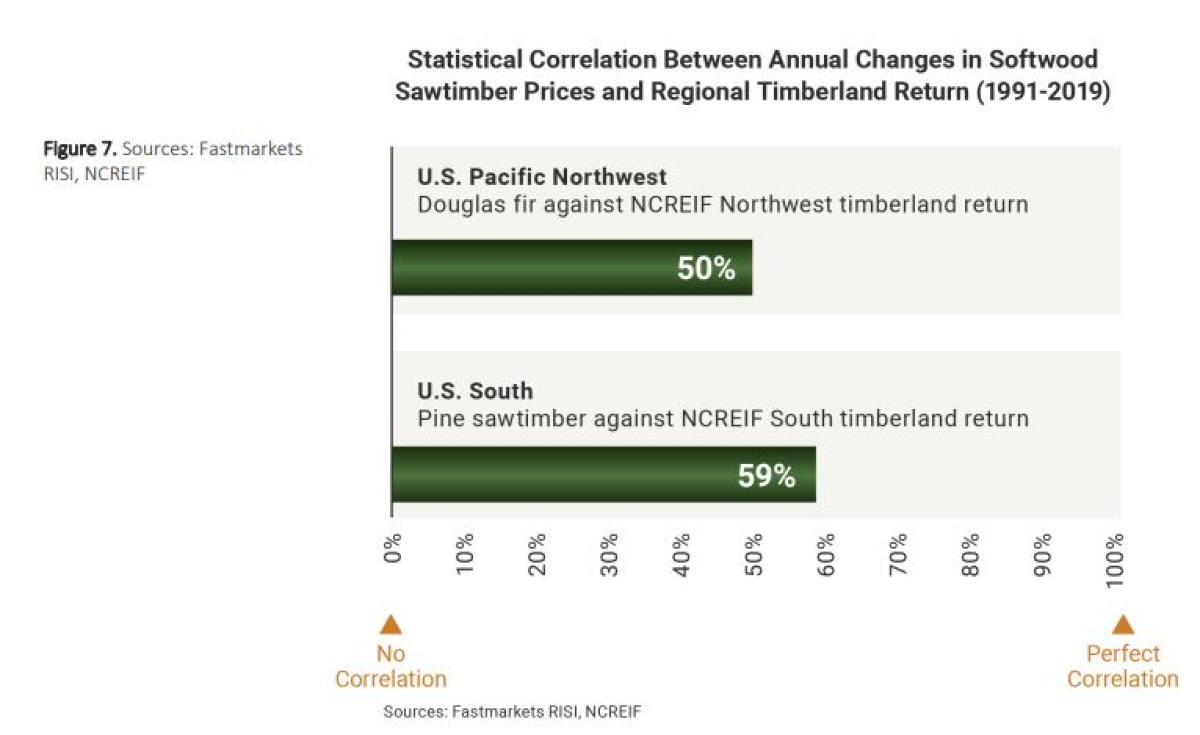

Timber Pricing and Timberland Returns As the charts illustrate, lumber prices in the United States are closely correlated with timber prices in the both the Pacific Northwest and the South. By extension, the reason timberland investors should pay attention to sawtimber prices is that sawtimber prices play a significant role in timberland returns. According to the National Council of Real Estate Fiduciaries’ (NCREIF) Timberland Property Index, the correlation between timberland returns and sawtimber prices has been about 50 percent or better for the past three decades (Figure 7).

Fundamental Changes Facing Southern Timber Markets

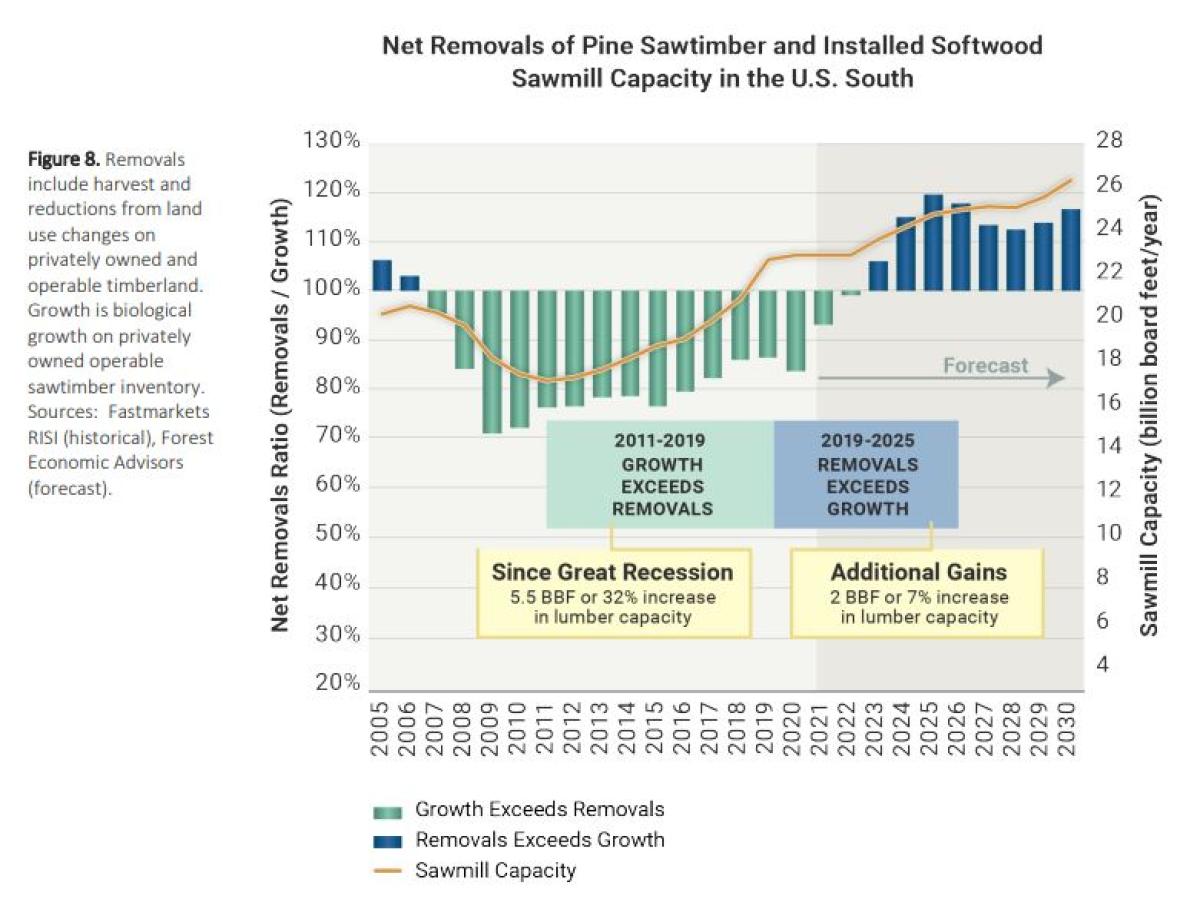

Returning to our prior discussion about the behavior of timber markets in the U.S. South, as was noted, there was clear linkage between lumber and sawtimber market dynamics in the period leading up to the Great Recession and Global Financial Crisis (GFC). However, that linkage became uncoupled after 2010. The source of this disassociation was the fact that sawtimber harvest rates in the region fell well below growth rates after the GFC. This phenomenon is illustrated in Figure 8 below, where the bars measure the ratio of sawtimber removals to growth. The blue bars are periods when harvest rates exceeded growth, which caused log markets to remain tight. However, when harvest rates fell below growth, there was an accumulation of timber inventory, which is indicated by the green bars. This created a surplus of sawtimber across many sub-markets in the South and when excess wood is available, upward shifts in lumber prices have a minimal effect on average sawtimber pricing.

The reason harvest rates in the South fell well below growth rates was the significant loss of sawmill capacity that occurred after the U.S. housing market crashed in 2006. With housing starts falling from more than two million a year in 2005 to one-fourth of that level by 2009, mill curtailments across the region caused lumber capacity to drop from 20.5 billion board feet (bbf) in 2006 to 17.1 bbf by 2011, a 16-percent decrease. This is illustrated by the yellow line in Figure 8, which represents the South’s total sawmill capacity. In comparison, the Pacific Northwest did not experience oversupply conditions following the GFC because of strong export demand from China for both softwood logs and lumber. This helped keep harvest and growth rates in that region in rough alignment between 2012 and 2018. Tight timber markets in the region meant that lumber price movements more readily influenced timber markets in the Pacific Northwest.

Re-establishing the Lumber-Timber Link in the South

Looking ahead, the decoupling of lumber and timber markets in the U.S. South is not expected to continue indefinitely. Over the past several years, more than $3 billion of capital investments have been made in sawmills across the region. These investments have been made both to upgrade existing mills and to build new “greenfield” mills. As of this writing, and since 2011, this has resulted in a total of 5.5 bbf of additional lumber capacity – and increase of more than 30 percent. Forest Economic Advisors projects an additional two bbf of capacity, or an additional seven percent, could be added to that total by 2025.

Altogether, the influx of new lumber capacity will increase total sawtimber removals in the South above growth rates. This could cause regional sawtimber markets to re-align – moving from an oversupplied to undersupplied condition. As supply and demand for sawtimber come back into balance, the cause-and-effect price relationship between lumber and sawtimber could return to the historic pattern observed prior to the GFC – especially if the U.S. housing market rebounds strongly in lockstep with a post-pandemic economic acceleration.

Conclusions and Recommendations

This paper demonstrates that lumber markets do have an impact on timber markets. When lumber prices surge, timberland investors may see improved pricing for their timber in portions of their U.S. timberland portfolios one to three quarters later. Following the Global Financial Crisis of 2007-2008, this traditional relationship was broken in the U.S. South because of a significant decline in harvest rates, which led to a surplus inventory of sawtimber in the region. Looking ahead, TIR expects this surplus to be winnowed and eliminated in the near future because of the large expansion of sawmill capacity that has occurred in the region over the last decade. This expansion is expected to cause harvest rates in the South to exceed growth rates by 2023. At that point, the lumber-to-timber price linkage that historically characterized market dynamics in the region will reassert itself and be similar to that linkage in the Pacific Northwest.

Focus on Lumber Demand Fundamentals, Not Spot Market Movements

With this in mind, we believe timberland investors can be confident that the economic fundamentals that drive lumber prices (higher or lower) in the future will filter into timberland markets. Consequently, if future demand drivers for lumber are strong, timber markets are likely to improve as well.

Having made that point, it is important to also recognize that lumber markets are very volatile, with price surges (and dips) often lasting only a few months to two years. Consequently, sharp, but brief, price movements in lumber markets should not be the basis for buying or selling timberland assets. The process of acquiring and liquidating timberland can take six months to a year, or more. This means investors cannot jump into or out of the timberland asset class easily or quickly enough to realistically capitalize on short-term lumber market cycles. Instead, the focus should be on long-term lumber-market fundamentals, like macroeconomic trends for single-family home construction and anticipated activity in the home repair and remodeling sectors.

Diversification is Important

When building a timberland portfolio, it also is important to recognize that softwood lumber market trends are just one of several factors that can influence returns. Diversification is important. A portfolio should include timberland assets that are influenced by the behavior and performance attributes of other wood product markets such as those for pulp (for the production of paper and packaging), hardwood lumber (for pallets, railroad ties, furniture and flooring), plywood, oriented strandboard (OSB), and wood pellets. When a portfolio is exposed to a broad spectrum of end-use markets, the diversity and variability of its income streams can improve its risk-adjusted return profile.

Think Tactically When Shaping A Portfolio

Finally, TIR believes it is important for investors to understand that while lumber is a commodity influenced by nationwide pricing trends, timber markets are localized. Most logs, because of their bulky nature, are transported no more than 100 miles (~160 km) to a mill. When making timberland investment decisions, it is important to focus on the mill capacity of the regional wood basket or sub-market in which an asset sits. Local wood markets characterized by high sawmill densities, will have timber prices that are much more responsive to increases in lumber prices.

About the Author:

Hong oversees all economic and market analysis and forecasting for TIR and plays a key role in the development and implementation of the firm’s investment strategy. He was a founding member of TIR and was instrumental in establishing the firm’s research-driven investment ethic.

Hong began his career at Temple-Inland Forest Products Corporation where he served as a resource utilization specialist and business analyst. In these roles, he provided economic and research analysis services that were used by senior executives within the company to make strategic decisions across a range of issues, including asset securitization, acquisitions and resource and business optimization. Prior to joining TIR in 2003, Hong served as senior investment analyst with Global Forest Partners where he performed global timber acquisition analysis, created a variety of decision support models and directed currency risk management analysis. Hong is recognized in the timberland investment arena for his measured and comprehensive analysis of the trends and events that drive investment performance and that influence the long-term risk and return profile of the timberland asset class. He writes extensively on these and related topics and is frequently consulted by market participants and analysts, including the news media, for his unique and well-informed perspectives. Hong is a graduate of Northwestern University where he received a BS in biology. He also earned an MS in environmental management at Duke University and an MBA at Columbia University. He received his Ph.D. in forest economics at North Carolina State University.

Disclaimer This paper is provided for the education of its readers. The opinions and forecasts made are for informative purposes only and are not intended to represent the performance of an investment made through Timberland Investment Resources, LLC. No assurances are made, explicit or implied, that one’s own investments in timberland or with Timberland Investment Resources, LLC specifically, will perform like what has been described in the paper.