By Bob Elliott, Co-Founder, CEO, and CIO of Unlimited, which uses machine learning to create index replication ETFs of 2&20 style alternative investments like hedge funds, venture capital, and private equity.

Liquid alternatives products often offer the allure of returns that could benefit most portfolios - equity-like returns with lower market beta. Many managers in the sector are able to deliver that kind of outcome, but once these managers take their cut, most of these products go from making sense to being a bad deal.

But there are diamonds in the rough that offer opportunities to benefit investors’ portfolios. They are hard to find since “rational” indicators like higher AUM or “you get what you pay for” fees are poor indicators of quality in this set of funds. The products that are most compelling are those that not only deliver alpha, but also sport lower fees relative to that alpha than others in the sector.

Below we take a look at performance over the last 5 years of 100+ liquid alt ETFs and mutual funds to give some perspective on the sector’s managers. In the end, we propose a couple of good rules of thumb for selecting the managers in the space as well as which funds offer a unique combination of benefits that could be interesting for investor portfolios.

Liquid Alts Fees Are Too Expensive...

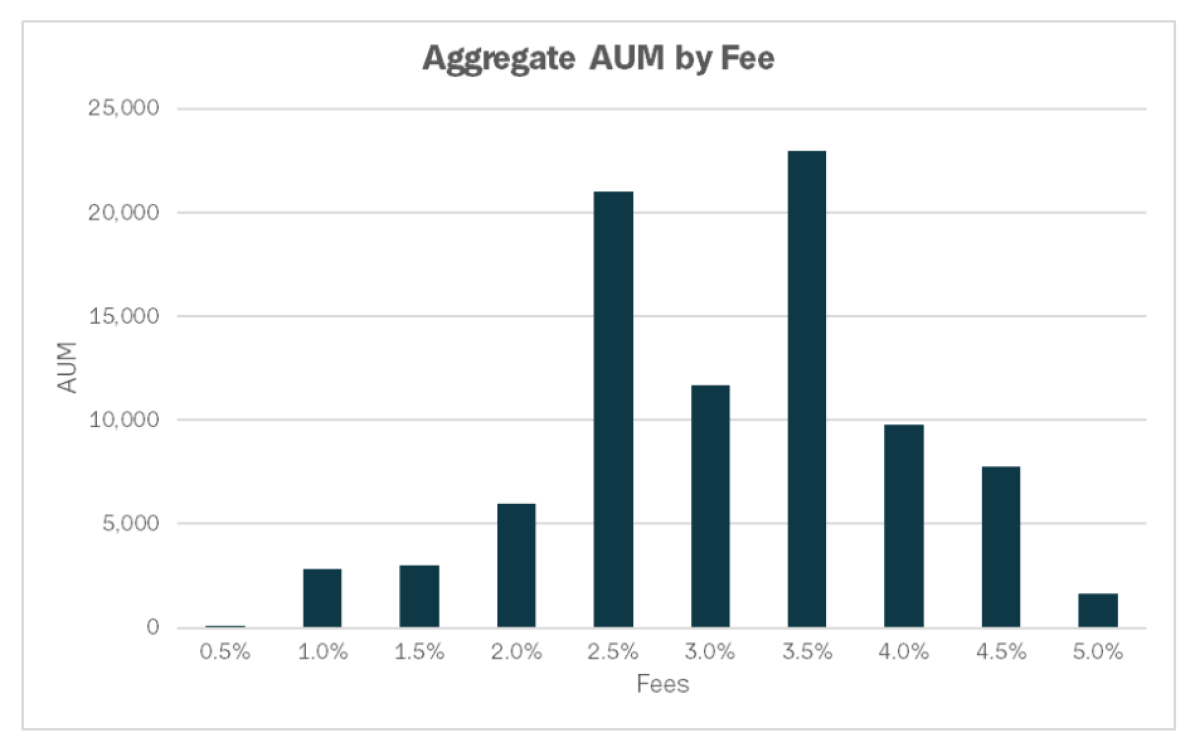

Let’s start with the fees, which are as you might expect, are too damn high.1 The figure below shows the distribution of AUM by the all-in fees charged for small-scale investors (including a 3-year amortized load if applicable). Almost 50% of investor funds are in products with a 3% annual fee or higher.

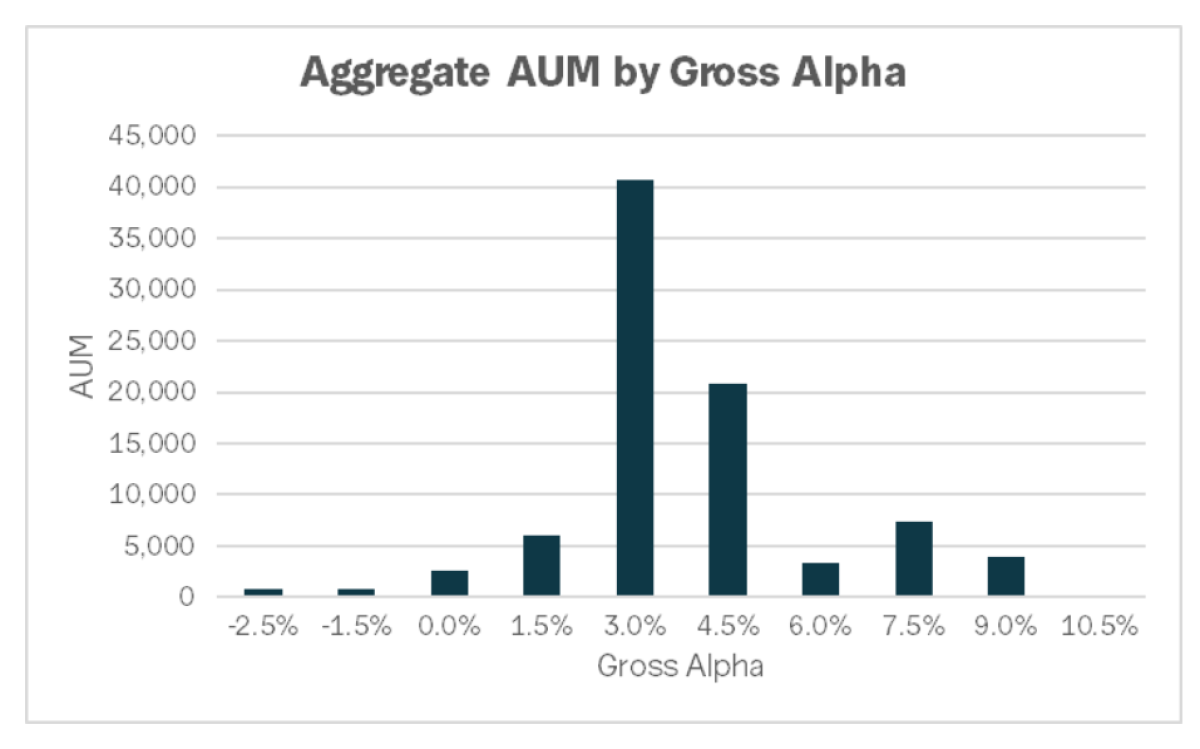

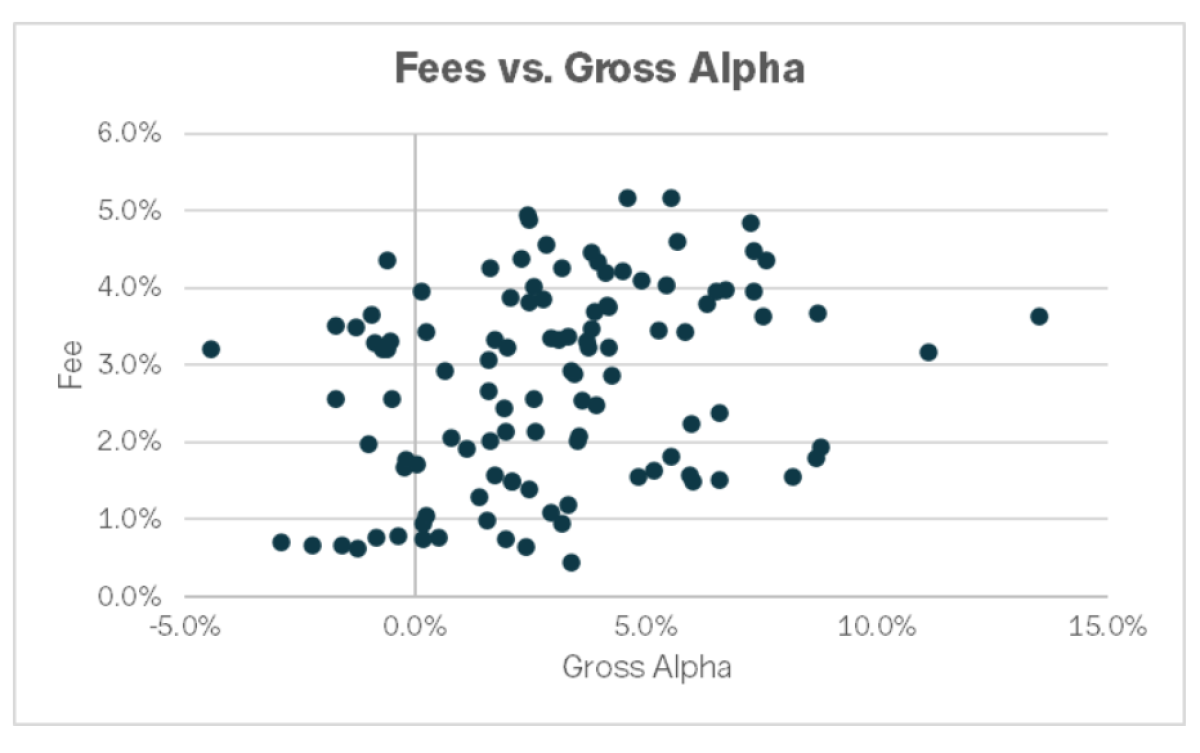

Those fees mean that, on average, the industry takes 100% of the alpha that it generates. The figure below shows the distribution of AUM by gross alpha (before fees). While it’s expected that the majority of investors are with managers that are able to generate some alpha relative to a 60/40 benchmark portfolio, the concentration around the 3% gross alpha number below looks like that around the 3% fee number above.

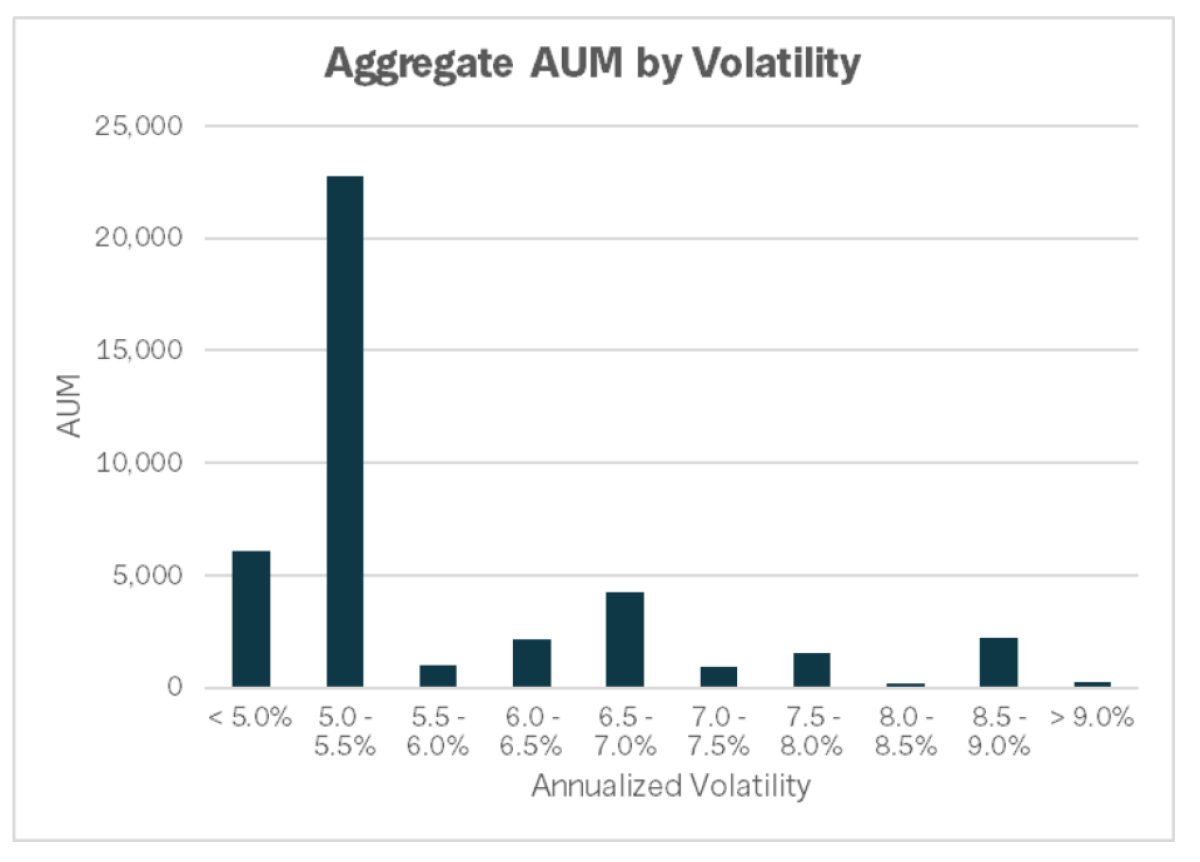

While most managers have skill as noted above, the problem is that they aren't taking enough risk to justify the fees they are charging. It's hard to generate alpha without some volatility. But when we look at our universe of funds, the data show that investors are primarily concentrated in products with low volatility. The average volatility of liquid alt products is 10%, but drops to 8% when weighted by AUM, which is less than half the 18% annualized volatility of the S&P 500.

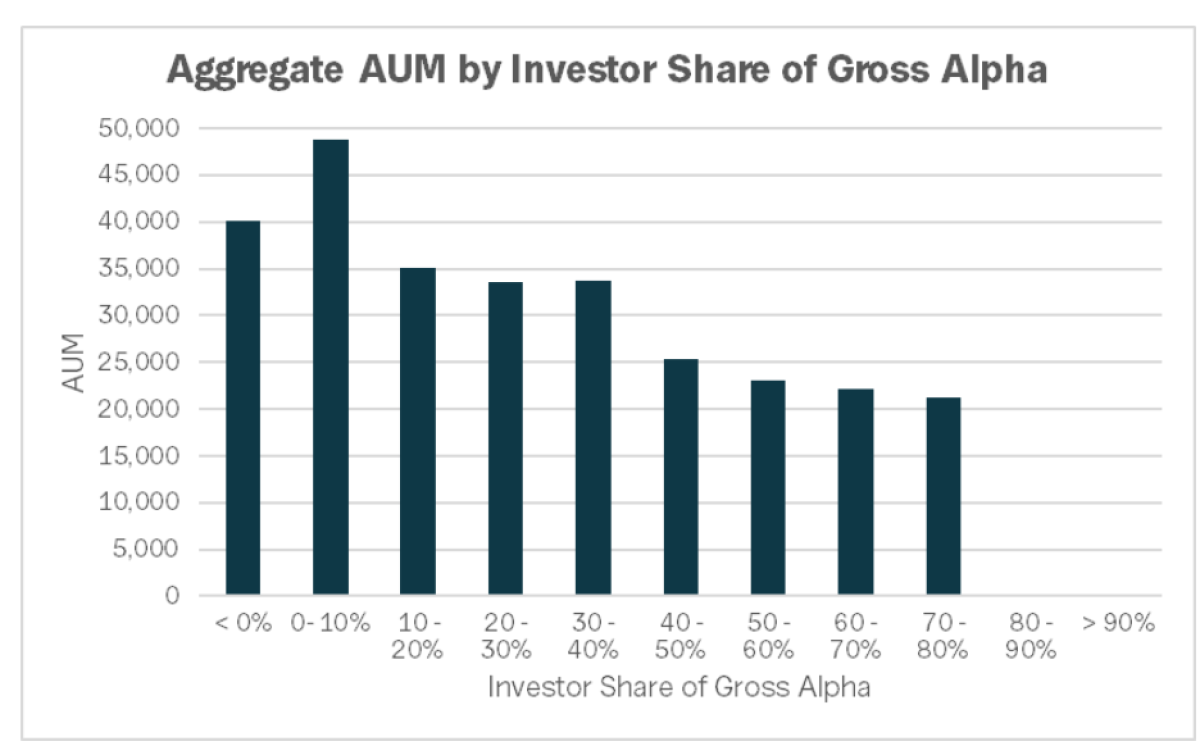

The result is that for more than half the AUM in the sector, the managers take the entire gross alpha or more in fees. The figure below shows that only 19% of AUM is in funds where investors keep more than 30% of gross alpha. Managers are getting rich and investors are getting the short end of the stick.

Even though the sector as a whole is a bad deal, there are some good managers out there that generate solid alpha. The trouble is that it is darn near impossible to find them. That’s because the most logical indicators are unrelated to realized outcomes for investors. For instance, there is no obvious relationship between performance and fees.

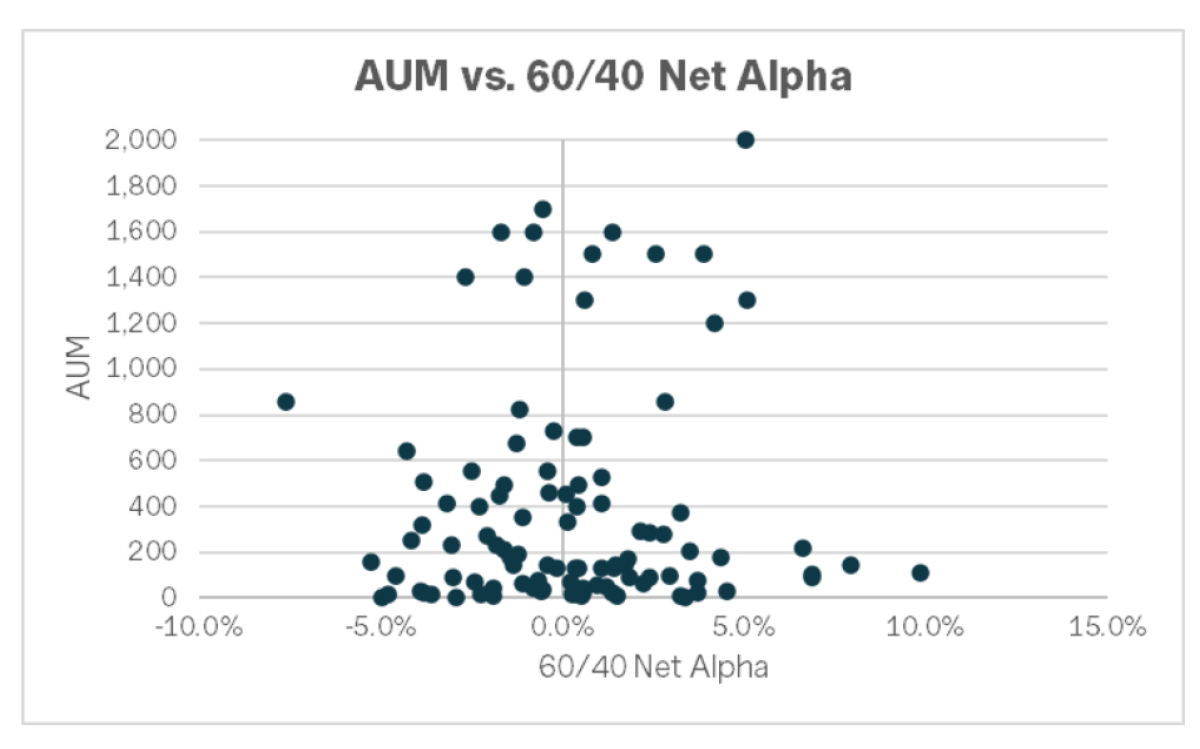

Because it is difficult to identify good individual strategies, the data show that there is no obvious relationship between AUM and net alpha at the fund level. In other words, it doesn’t seem like the market has found a tractable approach for selecting managers offering strong fee-adjusted performance.

...But Some Managers Are A Good Deal If You Can Find Them

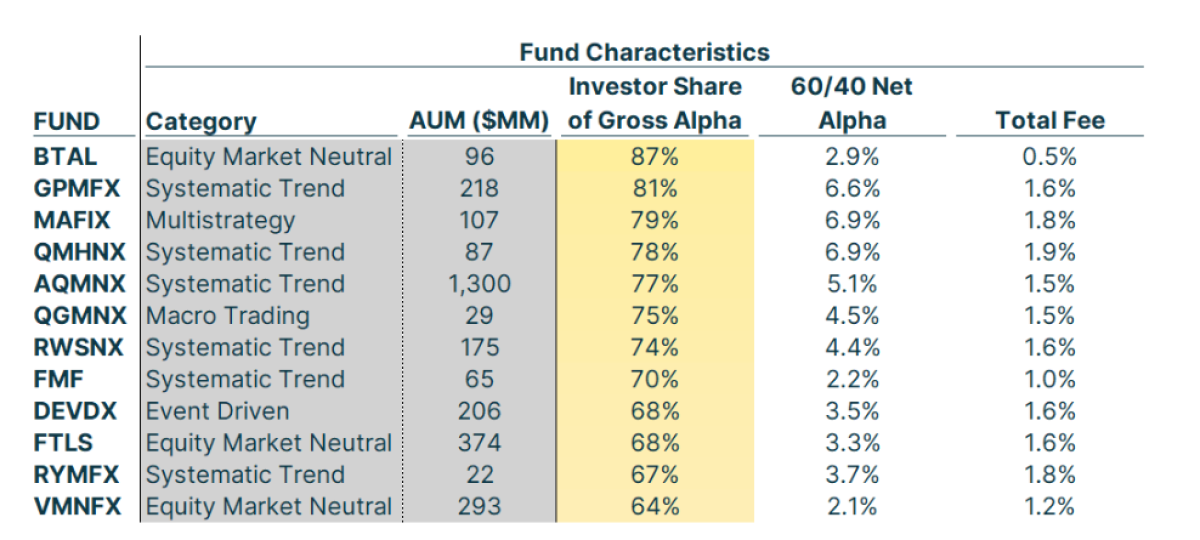

What is an investor to do given this picture? Well part of the story is to look for those managers that generate high quality alpha and don't take too much for themselves. In that search, here are a few criteria we would look at to find good managers:

- Greater than 2.0% annualized net alpha.

- Greater than 50% investor share of returns

- Less than 2.0% overall fees

The idea here is that funds that meet the filters above are structured in a way that is most likely to generate differentiated returns that would be beneficial to a portfolio over time. That will be driven by the combination of actual skill and not charging too much (either on a percentage basis or an outright basis) for the returns they offer. It is of course no guarantee, but it at least gives you a good shot as an investor.

Of the universe of 100+ liquid alts funds, only 12 met this standard over the last 5 years, with nearly all of these funds well below $1bln in AUM.

Selecting good liquid alt managers is tough since strategies are opaque and the traditional indicators of good performance don’t do a lot to help. By screening the managers to find those that charge reasonable fees or the alpha they generate, advisors and investors can find good additions to their portfolios. The key is to find those things that are somewhat counterintuitive - cases where managers aren’t raking in high fees for their work.

Footnote:

1 Fees are too damn high is a play on the single issue Rent Is Too Damn High Party that was an amusing piece of New York City politics from 2005-2010.

About the Author:

Bob Elliott is the Co-Founder, CEO, and CIO of Unlimited, which uses machine learning to create index replication ETFs of 2&20 style alternative investments like hedge funds, venture capital, and private equity.

Prior to founding Unlimited, Bob was a Senior Investment Executive at Bridgewater Associates where he served on the Investment Committee (G7) and created investment strategies across equities, fixed income, credit, exchange rates, and commodities, including many used in the flagship Pure Alpha fund. He also built and led Ray Dalio’s personal investment research team for nearly a decade. He’s the author of hundreds of Bridgewater’s widely read Daily Observations and directly counseled some of the world’s foremost policymakers and institutional investors on economic and investing issues.

Bob has also served as an advisor and executive at several startups including CircleUp, an investment company focused on early-stage consumer brands. There he revamped the investment strategy for the company’s $150mln venture funds leveraging big data approaches to improve decision-making. He was also the co-founder of GiveWell, a startup charity evaluator which now directs more than $500mln in annual contributions.

Bob holds a BA in History and Science from Harvard.