By Joe Elmlinger, Head of Client Solutions and Alex DeFeo, Senior Portfolio Manager at Lake Hill.

We wrote about weekly options nearly a decade ago after the exchanges listed them and volumes subsequently skyrocketed (The Popularity and Pitfalls of Weekly Options - 2014). We are seeing nearly the same phenomenon with 0DTE options (zero days to expiration) along with similar eye-catching headlines. We conducted an identical analysis for 0DTEs and our conclusions may surprise some investors.

There are a ton of pundits promoting 0DTE option trading strategies. Many recommend selling or shorting 0DTE to collect the fast-decaying option premiums (theta). Others advise on buying them for the potential lottery-like payouts. Currently, back-tests that only go back a year or so are used to justify shorting 0DTE outright or in a spread format. Some strategies also involve midday entry, exit, and legging signals. In addition, just as with the weeklies, the 0DTE options have the benefit of self “hedging”. They automatically expire which provides a “stop loss” of sorts. This was and is also a reason for trading the weeklies.

Simply selling (or buying) a weekly would naturally delta hedge in 5 business days. This makes it easy to trade without the added complexity of rolling positions or hedging with futures. The 0DTE is the same except on a much shorter time scale, 6.5 hours or less!

The problem with relentlessly selling or buying options is that it depends if those options are expensive or cheap based on simple odds over time (i.e., What is the Expected Value?).

As all options traders know: Options are all about odds, and odds can only be calculated properly after repeated bets. Without any complicated options mathematics, what are the odds of a 0DTE payoff?

To answer this, we did a very simple study. We looked at the historical daily open-to-close returns and plotted a histogram.

While the future may not match the past, and things are obviously different today, it behooves anyone who makes an investment decision – especially if they trade options – to at least look at what the historical base odds are. At a minimum, it provides insight into what something might be worth. Adding various filters to the data such as “use all days” vs “use only days when VIX is greater/less than a threshold” or “intraday hi-low data” or “5-minute bar data” can refine the analysis. We found that the results are all basically the same irrespective of how one manipulated the data.

Our conclusion: 0DTE’s on average are fairly priced. There is no material advantage to systematically shorting or buying them. Currently, they appear to be slightly “cheap”, but profiting from that cheapness takes many bets taken over a long period of time, probably more time than most traders can stomach.

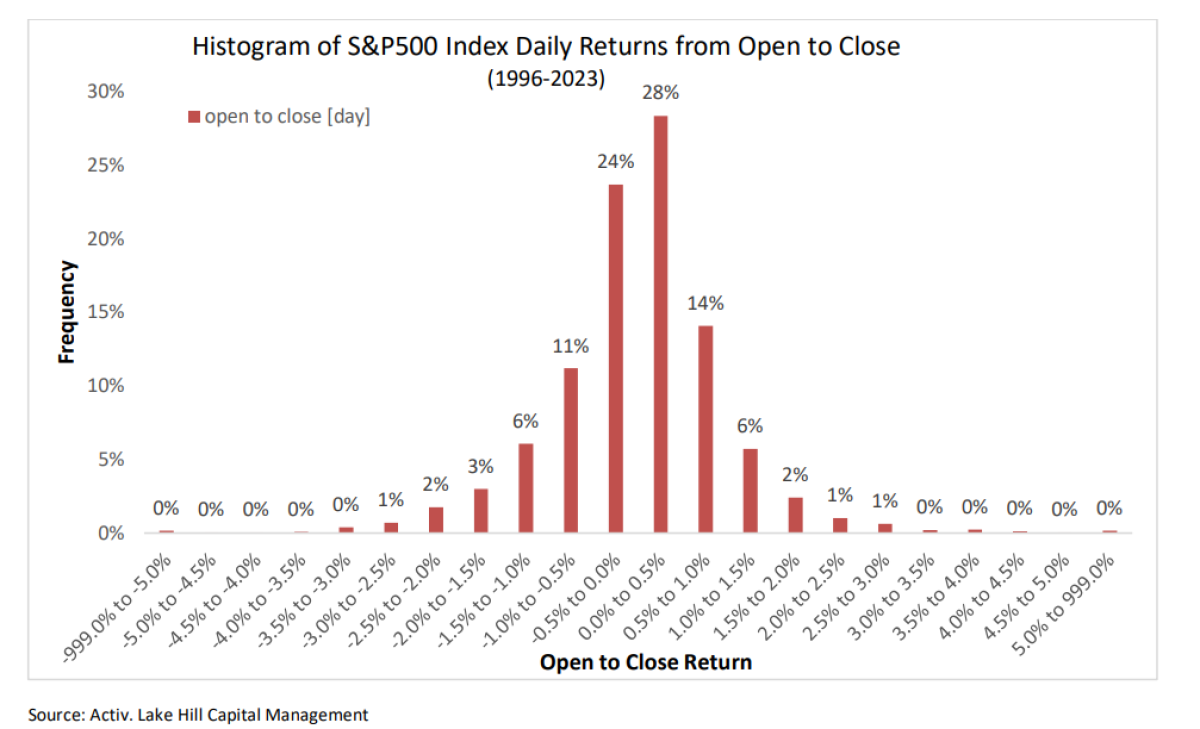

We first analyze a histogram of S&P 500 returns from open to close 0930 ET to 1600 ET using data from 1996 to 2023. The fair value of an at-the-money (ATM) straddle, is simply the sum of the frequency of returns times the return bin.

An example: If the 0DTE ATM straddle is trading for $20 with the S&P500 Index at 4000 (50bps of the index), is it wise to sell that straddle?

According to the histogram below, we can make money so long as the 50 bps we collect covers the expected daily market moves. If the market stays within the two largest bins [24% + 28% = 52%] We are winners. So currently 52% of the time we will be profitable. That sounds nice.

The problem with winning 52% of the time is that you might be winning pennies 52% of the time but losing dollars 48% of the time.

On further analysis we see that when we win, the market moves on average 0.23%. When we lose, the market moves an average of 1.20% against us and sometimes much more. When we win, we earn an average profit of $10.80 [50bps minus 0.23bps *4000], but when we lose it’s a whopping average loss of $28.00 [50bps minus 120 bps *4000].

This rudimentary analysis shows that given today’s prices (50bps for the ATM straddle), buying the straddle is the more advantageous trade.

The problem: Selling this straddle, even for negative edge, will show profits more often until the losses eventually show up, so most folks opt to sell in search of short-term profits.

0DTE as a new trading tool is likely here to stay. There is lots of commentary on their risks, benefits, impact on the markets. We think they add value to the toolkit for traders and investors. They do not seem particularly mispriced. If you have a strategy for buying them or selling them, each can work. The key is to have a basic handle on the odds. Currently, the simple analysis shows they are not seriously mispriced, just slightly cheap if one has staying power.

Frequently Asked Questions About 0DTE Options

Lake Hill is actively monitoring the 0DTE options and their overall impact on markets and the options ecosystem. Volumes in 0DTE have exploded and now account for a significant amount of overall trading volume in the equity index options markets.

- How exactly 0DTE options work and what's driving the growth?

0DTE are options that expire on the same day, at the end of the trading day. That is, they have zero days left to expiration and therefore are extremely short-term investment products.

- Who is driving this trading -- Retail/institutional or a mix of the two?

The primary volume in 0DTE is in S&P500 Index options, not single stocks. Given that these index option products have traditionally been used by institutional traders, we believe that most end users are professional traders and sophisticated market-makers. There has also been some uptick in retail traders, but we suspect that they are among the more sophisticated retail traders and that they are not the driving force in 0DTE options. To gain insight into the type of end-user, one would have to know which firms are clearing the trades, which is non-public information that only the exchanges have access to.

- What is the intent here? Is it short term options selling to generate income?

The advantage of 0DTE is that one can take an extremely short term (daily) view of the market. While the 0DTE has only recently proliferated, one can look if historically selling them (for premium collection) or buying them (for hedging/protection) is the better trade. Our analysis indicates that BOTH strategies can be profitable. For example, a simple strategy of selling 0DTE option premia (either outright or via various option spread trades) has recently been profitable. However, our research indicates that over longer periods of time (multiple years), it may be more advantageous to be a net buyer of 0DTE options.

- What are some of the advantages and disadvantages of these types of options?

The advantage is the daily instant feedback on market events with no overnight risk and daily recalibration to the market level. A disadvantage is the 0DTE is unlikely to respond to longer term movements in VIX or offer protection to overnight moves. They are unlikely to provide significant protection or significant income for an institutional sized portfolio - hence it's more of a "traders product".

- What is the average hold time and typical size of these trades?

The average trade size is around 2 contracts. However, the ultimate positioning by a trader is very likely much higher. Average trade size across the industry has been declining due to the advent of algorithmic execution in the options market. Brokers have offered execution algorithms in stock trading for many years but have developed algorithms for options trading in the past few years. A simple example of an execution algorithm would be one in which the executing broker can break a 100 lot order into small “odd lots” to minimize market impact and effectively deal with high frequency traders. Most 0DTE positions are NOT held to the end-of-day expiration but rather are closed out at some point during the trading day.

- What strategies are conducive to such trading?

There are many strategies that can benefit from 0DTE both for hedging or income (see answer #3 above). However, given the balance of risks and potential benefits, we think 0DTE is best suited for shorter term and smaller traders. We do not currently see it as viable for larger institution investors who use or want to use index options. Note that even if one invests in longer dated index options (say, 30 days out or more), one should have advanced systems in place to monitor the 0DTE because they can impact other options. We also suspect that quantitative traders could be using 0DTE in place of index futures. An intraday momentum strategy, for example, could be executed using 0DTE options and a built-in stop-loss.

- What effect is this having or can have on the broader market? Does this in some way increase or decrease market volatility? Why?

Our analysis is that 0DTE may suppress volatility over short periods of time but could actually increase volatility over longer periods of time. The logic is that anything that squeezes the market (VIX, realized volatility, or anything else) ultimately resurfaces at other times (i.e., the overall volatility level ultimately evens out). With 0DTE options, we believe that there is potentially a risk that if the trading activity is suppressing volatility (due to the counterparties/market makers hedging the 0DTE trades in the underlying index), then ultimately positioning could build up over time and can cause an explosion of volatility, potentially at the worst possible time.

- And does this pose a broader danger to markets? Why?

There may be unintended systemic risks to the markets arising from 0DTE options. This is not necessarily due to 0DTE options themselves but may arise if some clearing firms lack the systems to charge margin or manage risk for intraday positioning. Some brokers/clearing firms primarily (and perhaps only) look at positions at the end-of-day. Therefore, traders may be able to trade 0DTE without posting any margin or collateral. This puts the broker/clearing firm at risk if their client loses money and has not posted margin in their account. Many smaller brokers/clearing firms may potentially be at risk which further puts the overall clearing mechanism at risk. This is our top concern currently with the proliferation of 0DTE option products.

About the Authors:

Joe Elmlinger is Head of Client Solutions at Lake Hill. For over thirty years, Joe has been a pioneer in derivatives sales and is recognized as a leader in equity derivatives, structured products, and customized financial engineering for clients.

Previously Mr. Elmlinger was Head of Sales for Equities & Derivatives at Société Générale. Mr. Elmlinger spent the majority of his career at Citigroup and its predecessor, Salomon Brothers, as Global Head of Equity Derivatives. He has also held senior roles at Bankers Trust Company, Merrill Lynch, the Board of Directors of ISDA and The Options Clearing Corporation.

He has a B.A. from the University of Vermont and an M.B.A. from Stanford University.

Alex DeFeo is a Senior Portfolio Manager at Lake Hill with a finance career spanning more than two decades. Prior to joining Lake Hill, he was a Senior Portfolio Manager at Goldman Sachs where he focused on Alternative Risk Premia and Volatility Strategies. He has also held senior positions at Credit Suisse, where he served as the Head Trader and Portfolio Manager for the Alternative Beta Strategies group and at Bank of America.

Alex has been a guest lecturer at the London School of Economics and an instructor at UC Berkeley. Some of his research has been funded by the US Army, Department of Defense, and the National Science Foundation.

Alex earned an M.S. in Mechanical Engineering from the University of California, Berkeley and a B.S. in Mechanical Engineering from the Massachusetts Institute of Technology.