By Dan diBartolomeo, President and founder of Northfield Information Services, Inc. Based in Boston since 1986, Northfield develops quantitative models of financial markets.

A Tale of Two WYNNers

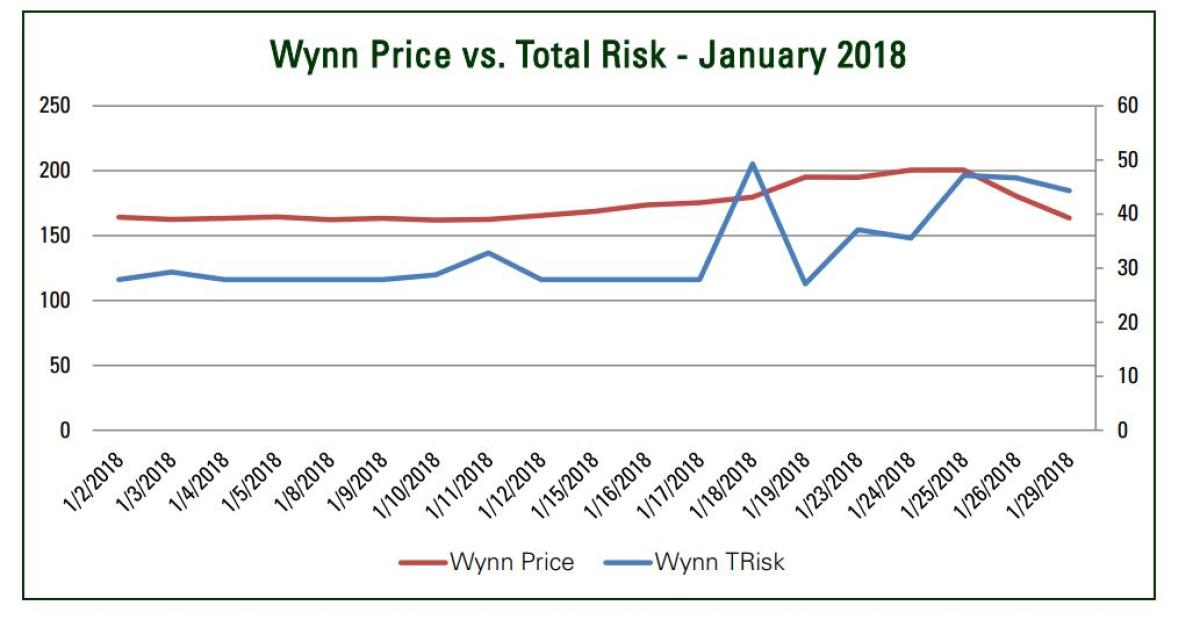

During the month of January 2018, the stock of Wynn Resorts (WYNN) experienced a “roller coaster” ride opening the month at about $164 and closing it near $163. During the month, WYNN hit a high of $200 per share. Examining the timeline of events provides an excellent illustration of why our new Risk Systems That Read® (RSTR) technique is such an important advance in risk analytics.

As of the regular US Fundamental Model update at December 31, 2017, the forecast volatility for WYNN was 38.44% per annum (with a one-year forecast horizon) This equivalent to 1477 variance units, of which 1200 variance units were perceived as idiosyncratic stock specific risk. The forecast idiosyncratic variance was 81.2% of the forecast total variance. While this looks like the explanatory power (R-squared) of the model is low at 18.8%, it should be recalled that forecast idiosyncratic variance in Northfield models reflects not only past residual volatility, but also adjustments for serial correlation and kurtosis in the distribution of returns. For more information on the rationale for these adjustments see Parkinson (Journal of Business, 1980).

After the passing of the New Year holiday on which there was no trading, as of January 2, 2018, the “near horizon” forecast for WYNN (annualized value of volatility looking ahead ten trading days) with RSTR 27.8%, reflecting the recent generally low volatility of the market (this is all before the high market volatility in early February 2018). The divergence of the risk values shows the extent to which the “near horizon with RSTR” model forecast and regular forecasts can diverge for periods of time.

By January 18th, 2018, the share price of WYNN had already moved up to $180 from the start point of the month at around $164. The near horizon risk estimate moved up from about 28% to over 49% in a single day, indicating that large price movements were possible in the near term (up or down). The high-risk estimate came as the result of a scheduled upcoming earnings announcement. This is typical going into an earnings announcement as pre-announcement press coverage becomes material.

On January 22, Wynn announced fiscal fourth-quarter earnings that were materially better than expected. The announcement directly created one news story, the announcement itself. Immediately after the earnings announcement things went quiet again on the news front as investors analyzed the meaning of the results. In subsequent days, the positive earnings event motivated Morgan Stanley, Instinet, Motley Fool, Zacks and others to put out “buy” recommendations on Wynn which created follow up news stories. Between the 18th and the 25th, there were a number of additional articles on Wynn, and the casino industry in general (mentioning Wynn among other firms). The stock continued to rise quickly from $180 to $200 over five trading days. The near horizon risk estimate for the US Fundamental model continued to climb from 27 to 47% in this time span. It should be noted that our long-term risk estimate of 38 was about in the middle of the 27 to 47% range of the relevant near horizon estimates. Everything made sense for routine conditions.

On Friday January 26th, the situation became not routine as the NY Times broke a story about sexual harassment allegations against CEO Steve Wynn. Unsurprisingly, this was analyzed as “bad news” within the text analytics. The stock moved down from about $200 at the close of January 25th to about $163 by the closing on January 29th. That’s an 18% downward move in two trading days. Given our risk estimate of 47%, the random likelihood of a move this big is about 1 in 60,000 under the assumption that returns are normally distributed. Rather than assume normality we usually assume daily stock returns have a T-5 distribution. Under the T-5 assumption, the likelihood of such a large move occurring randomly is about 1 in 250. Over the period from January 25th through January 30th, the S&P 500 market index was almost flat so the big down move in Wynn was about Wynn, not the market. The near-horizon forecast risk levels remained in the high 40s.

Due to the intense news coverage of the misconduct allegations over the weekend (January 27th and 28th) and on January 29th, the risk estimate for Wynn moved up to 70.5% nearly double the prior long-term estimate of 38.44%. As of January 31st, the long-term risk estimate for WYNN was 38.46%, almost identical to the forecast as of December 31st, 2017. Of the total variance of 1479, the idiosyncratic portion was 1119, or 75.7%. The long-run (unconditional) risk estimate is essentially unchanged, while the long-term idiosyncratic risk decreased slightly reflecting the positive fundamental business outlook, as evidenced by better-than-expected fourth-quarter earnings.

While the long-term risk forecast for WYNN was unchanged over the month of January, the “near horizon” risk forecast went from roughly 28% to 47% in the run-up to an earnings announcement, and then up to over 70% in the aftermath of a very negative news store late in the month. What is even more important is the simple fact that the model is responding to real-life events that represent real risks to a company and their shareholders. This is in contrast to most models that rely simply on a statistical description of past price movements. Estimating future volatility just from recent price volatility can be a very misleading. Many large price movements arise out of temporary liquidity imbalances as described in Govindaraj, Livnat, Chen and Savor (Journal of Investment Management, 2014). A majority of large price moves seem to have no fundamental cause, and hence are of very limited relevance to the estimation of future risk.

Wynn Resorts related corporate debt also exhibited market value volatility during January. Wynn has multiple corporate bond issues outstanding related to the parent company, and separately for the casino operations in Las Vegas and Macau. In the Northfield multi-asset class “Everything, Everywhere” risk model, a contingent claims type model is employed. In such a model a corporate bond can be thought of as a weighted combination of a riskless bond and equity in the firm. The respective weights of the components is based on the expected value of investor loss in the event of a bond default (i.e. loss given default or LGD). As the forecast volatility of WYNN evolved day by day during January, the credit risk associated with the Wynn organization would move in a related, but potentially complex fashion. For example, a price decline of about 3% had been reported for corporate bonds of Wynn Las Vegas on January 29th subsequent to the release of the misconduct allegations. On the other hand, our analyses of Wynn Macau bonds at January 31st suggests that the expected loss given default for these bonds had actually declined very slightly, presumably due to the strong earnings announcement. It should be noted that Wynn Macau equity trades separately in Hong Kong. As of both December 31, 2017 and January 31, 2018 our separate model of long term corporate “sustainability” (see diBartolomeo, Journal of Investing, 2010) projected that there isa 50% chance that Wynn Resorts would go bankrupt by 2044, which is equivalent to a 2.4% per annum likelihood. For a detailed explanation of how our RSTR technology relates to credit risk, see diBartolomeo (2016)1.

To the extent that we have two efficient forecasts of risk over different horizons (10 trading days and one year), investors also benefit from being able to interpolate between these values, so as to create a customized forecast risk time horizon (e.g. three months). The ability to blend forecasts arises from using the exact same underlying model (e.g. same factor loadings and sample period). Horizon blending has been available to our clients for many years.

We believe that the case of WYNN in the month of January 2018 clearly demonstrates how our text analytics process improves portfolio risk estimates over short horizons for all investors. The RSTR process varied the near-horizon risk estimates around the central value of the long-term estimate in ways that are very intuitive. During the timeline, two major events unfolded (one positive and one negative) in the span of less than two weeks. For active managers, it also provides a new way to think about the magnitude of idiosyncratic risk as representing alpha generation opportunities determined by real world events, as opposed to a statistical measure describing the lack of explanatory power in the basic model. For more information on the RSTR methods, please see http://northinfo.com/documents/795.pdf.

Footnotes:

1. diBartolomeo, Dan. “Credit Risk Assessment of Corporate Debt Using Sentiment and News,” in G. Mitra and X. Yu Editors, “Handbook of Sentiment Analysis in Finance,” Albury Books, 2016.

The Northfield/CQF Video Course on Investment Risk is Now Available. This is a ten-episode educational video series produced by Northfield and the CQF Institute. Hosted by Dan diBartolomeo.

About the Author:

Mr. diBartolomeo is President and founder of Northfield Information Services, Inc. Based in Boston since 1986, Northfield develops quantitative models of financial markets. The firm’s clients include more than one hundred financial institutions in a dozen countries.

Dan serves on the Board of Directors of the Chicago Quantitative Alliance and is an active member of the Financial Management Association, (“QWAFAFEW”), the Society of Quantitative Analysts. Mr. diBartolomeo is a Director of the American Computer Foundation, a former member of the Board of Directors of The Boston Computer Society, and formerly served on the industry liaison committee of the Department of Statistics and Actuarial Sciences at New Jersey Institute of Technology.

Dan is a Trustee of Woodbury College, Montpelier, VT and continues his several years of service as a judge in the Moscowitz Prize competition, given for excellence in academic research on socially responsible investing. He has published extensively on SRI, including a forthcoming book (with Jarrod Wilcox and Jeffrey Horvitz) on portfolio management for high net-worth individuals.