By Andrew D. Beer, Co-Founder of DBi, a pioneer in hedge fund replication.

Research shows that replication, rather than investments in single manager hedge funds, may make sense for most allocators.

Managed futures arguably offer greater diversification benefits than virtually any other alternative investment: a roughly zero correlation to both stocks and bonds over time, strong risk-adjusted returns and a tendency to perform best during market crises. Last year, the strategy rose approximately 20 percent during a bear market in both stocks and bonds.

In an ironic twist, simple replication of managed futures funds — also known as Commodity Trading Advisors — may be the most straightforward and efficient way to get broad exposure to a category that has historically been out of reach for many investors. Research shows that replication, rather than investments in single manager funds, may make sense as a cornerstone allocation to managed futures for most portfolios. While there are pros and cons to any asset class or strategy, the efficiency and simplicity that replication provides make it almost perfectly suited to helping investors incorporate the long-term benefits of managed futures exposure into a diversified portfolio.

Why Replication Should Work Well

Managed futures funds, in general, hunt for trends in futures contracts across four asset classes — rates, currencies, commodities, and equities. The funds evaluate historical price data to predict whether, say, crude oil will keep going up — or down. You can think of them as “wave detectors”: they constantly monitor 50, 70 — or more — individual futures contracts across the market sea. At any given point in time, a portfolio will be betting on many waves rising and others falling. The funds are best at detecting slow moving waves — those that gradually build momentum over months, not days. As waves crest and bottom, so too will the portfolios.

An obvious, but overlooked, point is that waves move in clusters, and the clusters drive alpha generation. The 2000s commodity supercycle lifted most, if not all, commodities during the “lost decade” for equities; the return of inflation last year created a once-in-a-decade opportunity to generate alpha by shorting bonds. Following this framework, an efficient replication model analyzes managed futures funds to determine the key clusters today and then invests in the deepest and most liquid corresponding futures contracts to gain comparable exposure.

How Well Does Managed Futures Replication Work?

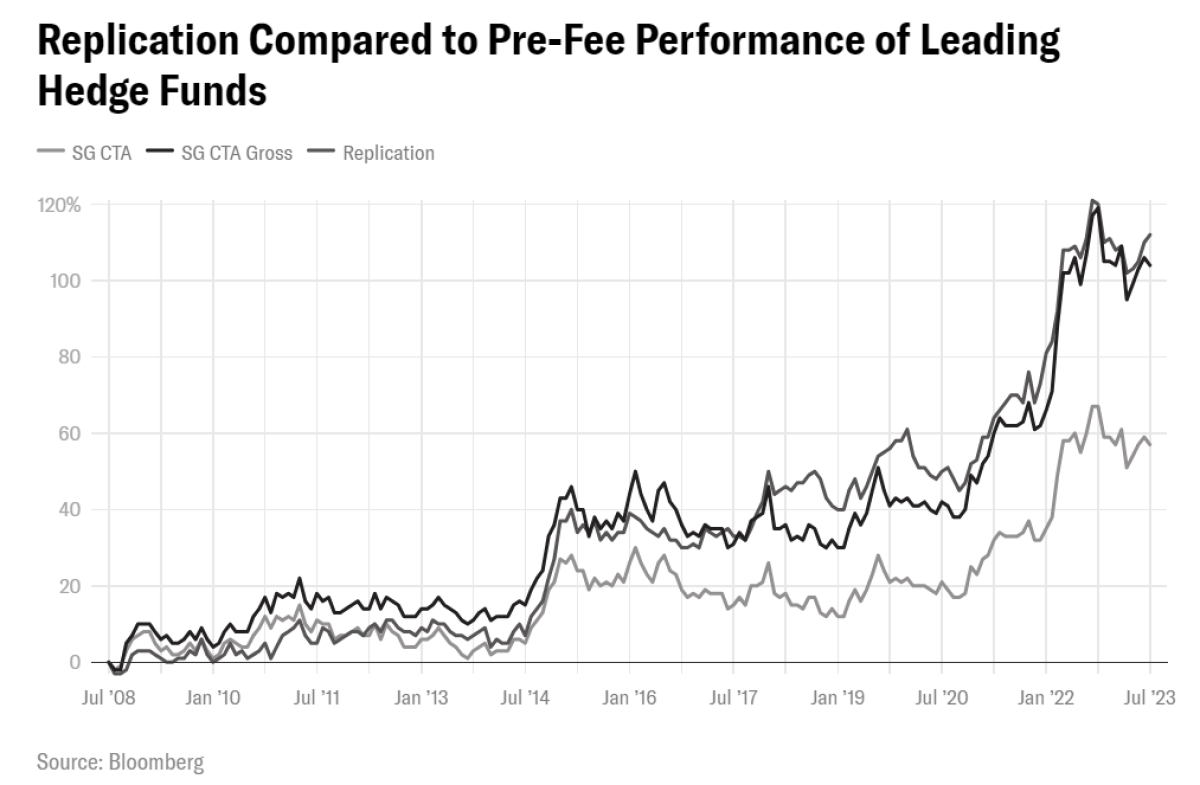

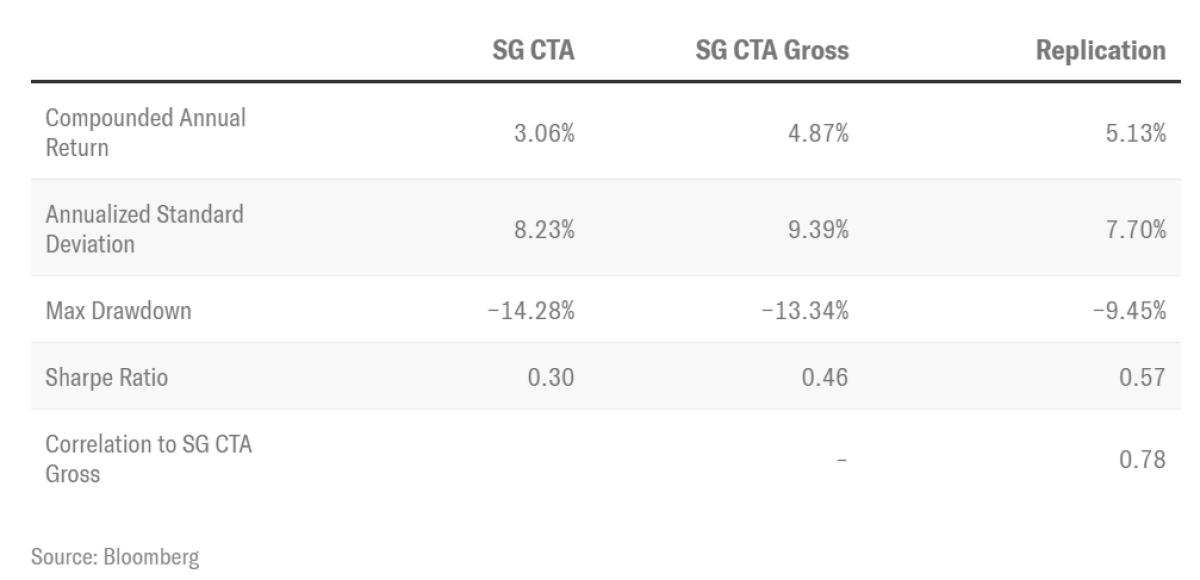

In the chart below, we show the performance results of a replication of the SocGen CTA Hedge Fund index over the past fifteen years, using only four exposures, or factors. As the index is published net of fees, we approximate pre-fee performance by adding back a 1 percent management fee and 20 percent performance fee. Each week starting in 2008, the replication model seeks to isolate the key drivers (“clusters”) of recent pre-fee performance of the index, then approximates those exposures (both long and short) using only one futures contract per major asset class: the 10 Year Treasury, crude oil, S&P 500 and Euro contracts. For an apples-to-apples comparison to pre-fee hedge fund returns, we show the replication model gross of fees, but net of estimated trading costs.

As shown above, the four-factor replication would have approximated — actually, slightly outperformed — the pre-fee performance of leading hedge funds with a correlation of nearly 0.8. Perhaps counterintuitively, the concentrated replication portfolio would have had a lower standard deviation and materially lower drawdown than the far more diversified basket of hedge funds underlying the index.

Importantly for allocators, the replication would have delivered superior diversification: roughly zero correlation and beta to stocks and bonds, but far more alpha than actual hedge funds after fees and expenses.

Pros and Cons

By charging lower fees, replication has the potential to outperform hedge funds, with the possibility of additional outperformance due to lower trading costs. Replication potentially can provide broad-based exposure to the strategy and mitigate the persistent landmine of single manager risk. The focus on the deepest and most liquid contracts reduces front-running risk or asymmetric drawdowns common in less liquid futures contracts. Similarly, simpler portfolios and daily transparency can make it easier understand current positioning and performance drivers.

Replication does have limitations. First, it is an approximation, not an exact copy, and hence will show noise relative to the benchmark. Second, it relies on recent historical data, and hence can move somewhat more slowly during sharp market reversals. Third, it can underperform during periods where the largest available contracts are not sufficiently representative of the cluster. Lastly, during any given period, there will also always be individual funds that outperform the index — even before fees, but few allocators have shown an ability to predict which managers can do this consistently.

Complexity: Innovation or Inefficiency?

The most strident criticism of replication, understandably, comes from those being replicated. Most sophisticated investors agree that the space has been on a three-decade road to commoditization as the spread of computing power, data availability, and knowhow means that even retail investors can post their own trend following models on social media. To counter this, many practitioners today seek to differentiate themselves from “simple” trend-following models, and replication, through complexity: statistical innovations and expansion into more esoteric, less liquid markets. This complexity should, in theory, result in higher risk-adjusted returns and therefore justify higher fees. However, replication of single manager mutual funds demonstrates conclusively that complexity can detract from returns over time, materially increase execution costs, exacerbate single manager dispersion, and magnify downside risk.

Recent appearance on The Compound:

About the Author:

Andrew D. Beer is the Co-Founder of DBi, a pioneer in hedge fund replication, and co-Portfolio Manager for the firm’s investment strategies. DBi takes the biggest drivers of leading hedge funds’ performance, and replicates them in simple, accessible products. With thirty years of experience in the hedge fund industry, over the past decade his singular focus has been to identify and develop strategies to match or outperform portfolios of leading hedge funds with low fees, daily liquidity and less downside risk. Mr. Beer received his MBA as a Baker Scholar from Harvard Business School, and his BA, magna cum laude, from Harvard College.