By Richard Barkham, Ph.D., Global Chief Economist, Head of Global Research & Head of Americas Research, Darin Mellot, Vice President, Capital Markets Research and Carsten Raaum Associate Research Director CBRE | Americas Research.

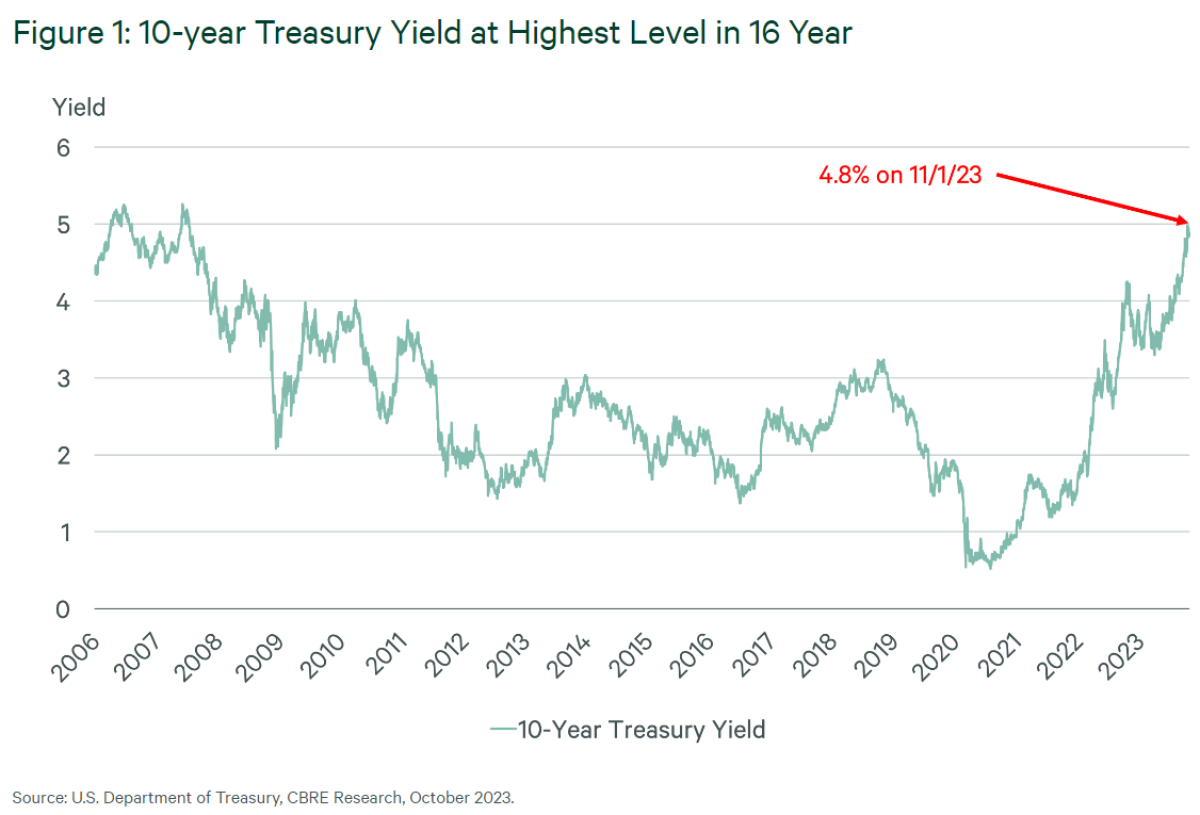

The recent bond market sell off has lifted the 10-year Treasury yield to nearly 5% and further dampened investor sentiment for commercial real estate.

Several factors are undermining bond values, but higher inflation is not one of them. Inflation has been falling and is near the Fed’s most recent 10-year expectation of between 2% and 3%.1 Three-month annualized core inflation is close to the Fed’s 2% target.

Rather than inflation, a mix of short- and medium-term economic and political pressures is driving up bond yields. These include a stronger-than-expected economy with robust consumer spending, increasing term premiums,2 the surging government deficit and reductions in the Fed’s balance sheet (quantitative tightening).

Why does a stronger-than-expected economy impact the 10-year Treasury yield if inflation is falling? The logic is that a strong economy leads to job creation and low unemployment, which means that inflation—particularly wage inflation—is not fully under control. This near-term fear is also related to the return of the term premium. Some say that the Fed finds it more socially acceptable to have inflation in the 3% to 4% range alongside low unemployment. This means that investors will require a higher premium to commit their capital for 10 years or more. The main risk of a long-term, fixed-interest investment is unexpected inflation.

Another factor pushing up bond yields is the growing federal deficit, which is on an unsustainable path3 in the long term. The deficit rose to 7.5% of GDP in fiscal year 2023 from 5.3% in fiscal year 2022. While there are several reasons for this,4 the increase is contrary to the general expectation that deficits should shrink when the economy is growing.

Investors also have little confidence that government spending will soon be restrained, given increased U.S. military commitments to overseas allies and congressional gridlock over setting a budget. Other factors causing bond yields to surge include the need to refinance more than one-third of total federal government debt and the Fed’s ongoing quantitative tightening program.

Consequences of higher Treasury yields

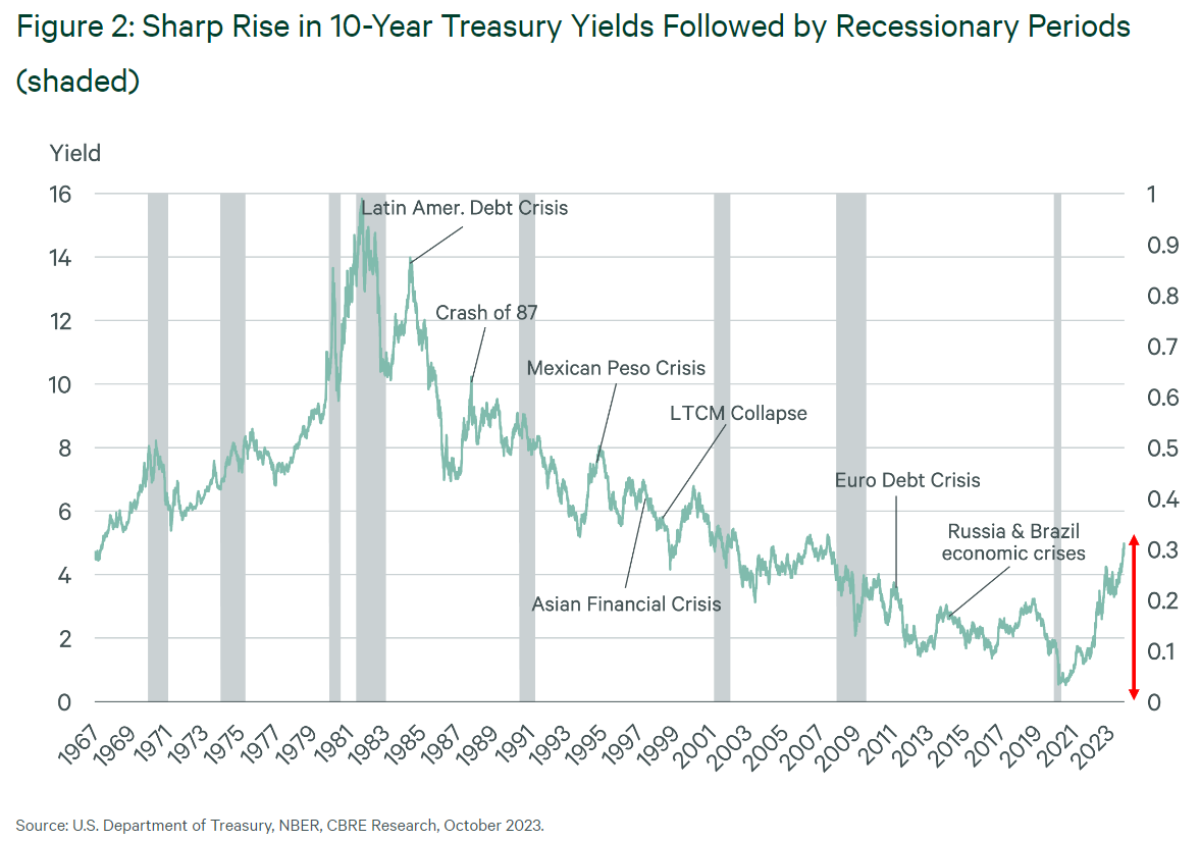

History shows that 10-year Treasury yield spikes often precipitate turbulence in the global economy. After a long period of very cheap debt, it is likely that some unsustainable financial positions have built up in the global economy. Increasing rates and a strong dollar will put some pressure on dollar-denominated debts abroad and also increase pressure on banks.

Impacts on commercial real estate

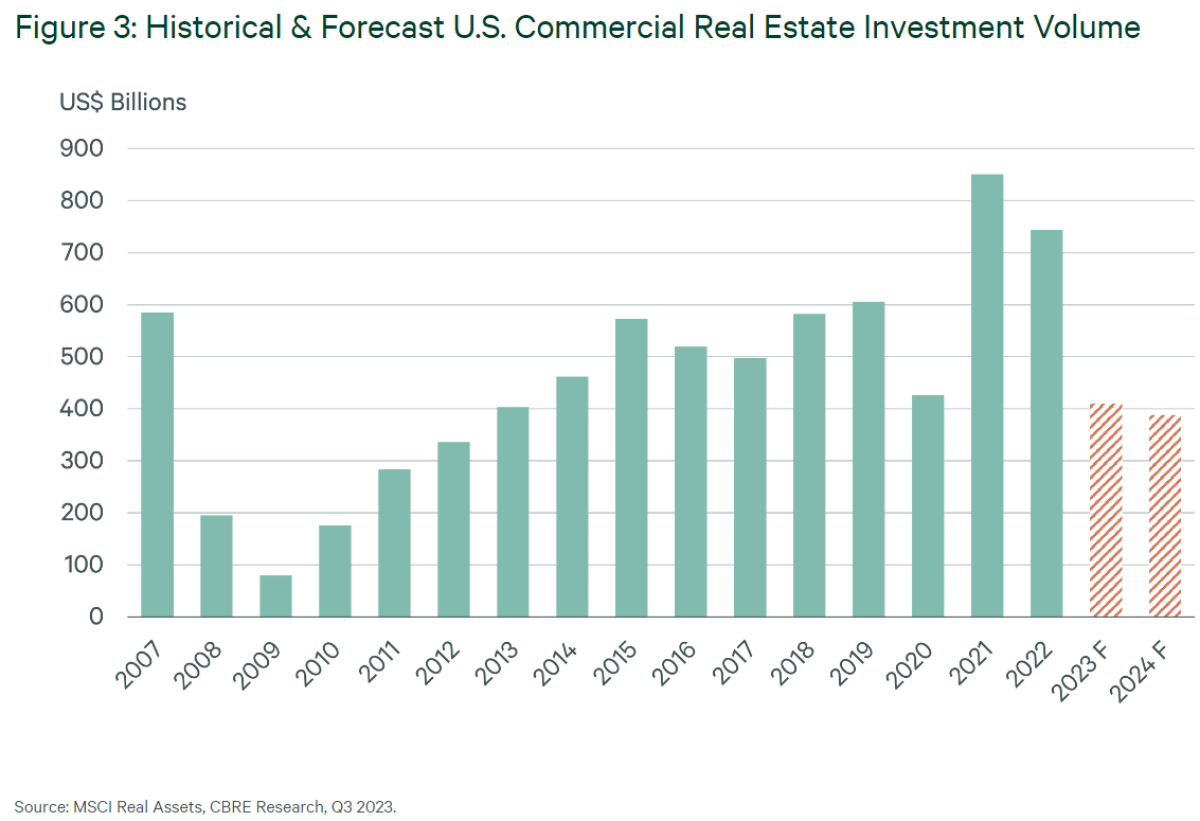

CBRE has lowered growth expectations for commercial real estate investment volumes next year to minus 5% from plus 15%. The increase in the 10-year Treasury yield will raise the cost of capital and make banks more cautious of lending.

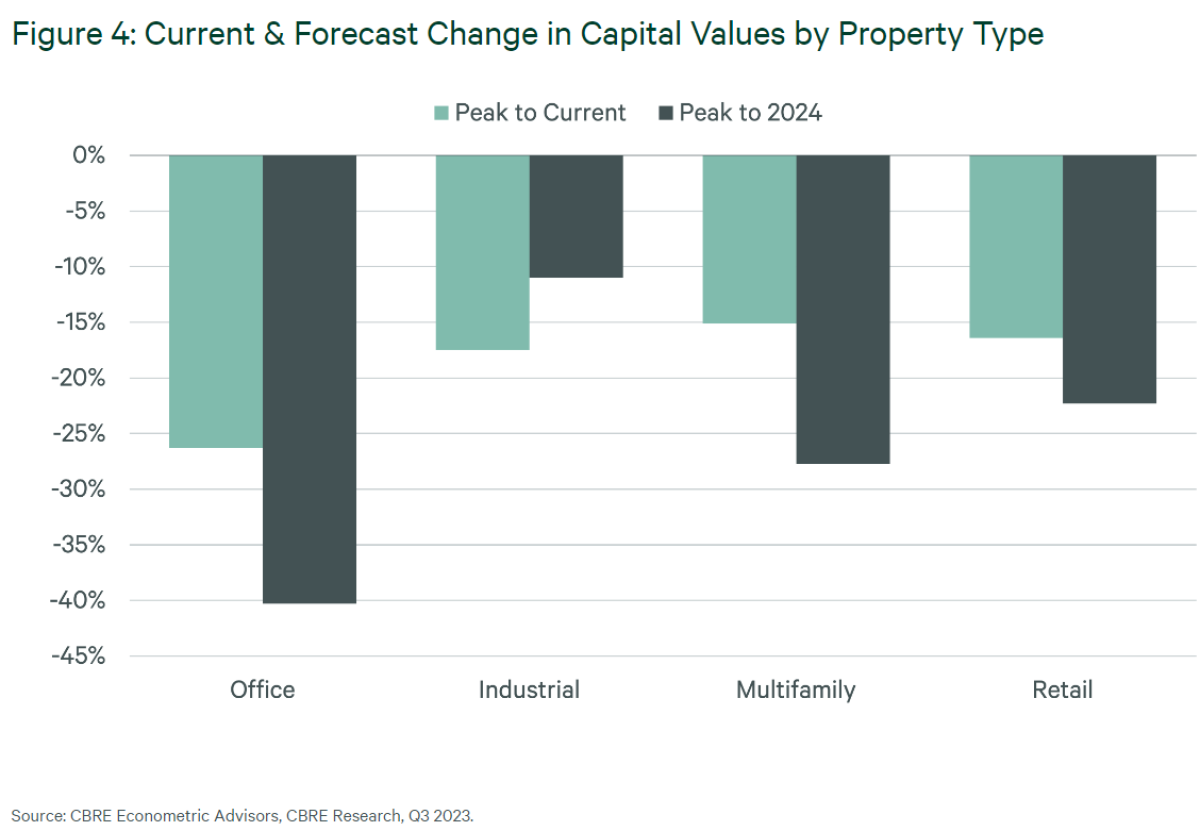

Our econometric models indicate that the rise in the 10-year Treasury yield to 5% or more, if sustained, will raise cap rates and lower capital values for commercial real estate.

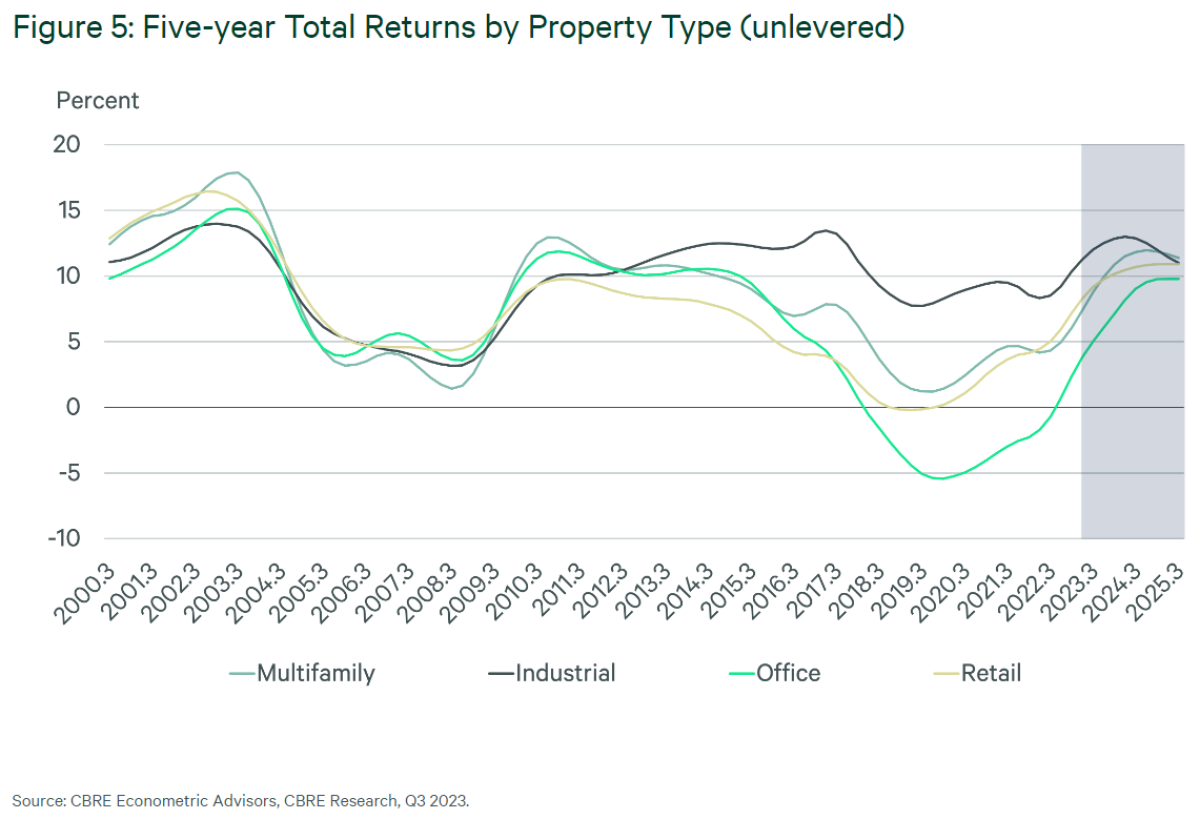

However, the drop in values this year and the relative health of most commercial real estate sectors except for office makes forward internal rates of return (IRRs) increasingly attractive. If the economy manages a soft landing and long-term bond rates ease, investment activity may surprise on the upside.

Long-term interest rates expected to fall over next five years

Although the 10-year Treasury yield has briefly reached 5%, we expect it will end the year at 4.6% and decline to around 3% in 2025. We predict it will remain at approximately 3% over the next 10 years, well above the 1.9% average between 2009 and 2019 but low enough to drive recovery in real estate values.

The basic factors that drive global interest rates have not changed. There is too much capital in the global economy chasing too few real investment opportunities. So, surplus capital will once again find its way into financial markets, boosting prices and reducing yields.

Long-term interest rates (e.g., the 10-year Treasury yield) are determined by three factors: inflation expectations, inflation volatility and the real (inflation-adjusted) interest rate that is determined by the balance between capital supply and demand.

The biggest driver of capital supply is increasing life expectancy. People tend to save more for longer retirement. Surplus capital tends to flow into markets perceived as reliable and safe, such as the U.S. This does not affect the global balance of capital supply and demand but it benefits the U.S. by exerting downward pressure on its long-term real interest rate.

With little business productivity growth in the developed economies and weak growth in emerging markets, global capital demand is expected to remain subdued.

Increased government spending to reduce carbon emissions could boost capital supply and demand. Government spending can be financed by taxation, which reduces savings, or by bond issuance, which absorbs savings. Either one will boost real interest rates, but it is not the predominant factor.

The International Monetary Fund does not expect a major increase in real interest rates globally in the longer term. We share this view, but with two caveats: It will take several years for long-term interest rates to fall back—even with lower inflation—and they will not return to the low levels of 2009 to 2019.

Well-entrenched global factors will put downward pressure on long-term interest rates once the market becomes convinced that inflation is under control and the federal government makes the necessary moves to reduce the budget deficit. This, combined with more attractive real estate prices, will help revive real estate capital markets activity in the second half of 2024.

Footnotes:

1 “Inflation Expectations,” Federal Reserve Bank of Cleveland.

2 The market expectation of inflation, currently 2.36%, is priced into the bond yield but unexpected inflation could eliminate the real value of a fixed cash flow at any time. The term premium is compensation for this risk and the possibility of government default. The term premium actually disappeared from the bond market between 2010 to 2020 as inflation surprised on the downside and investors began to think it would never return. That environment, in which inflation never rose above 2%, was called the “new normal.” Investors fear we are now in a another “new normal” of inflation consistently surprising on the upside.

3 “Deficit Tracker,” Bipartisan Policy Center.

4 Reasons include a shortfall in tax receipts due to tax relief (delayed filings) for states affected by natural disasters, lower capital gains tax collection and the Fed no longer sends any profits to the U.S. Treasury since income from its bond portfolio is outstripped by the interest it pays on deposits and reserves.

About the Authors

Richard Barkham PhD. leads a global team of nearly 600 research experts who help CBRE’s clients understand the forces shaping the commercial real estate industry.

One of the world’s leading real estate economists, Richard combines the theoretical framework of an academic with hands-on experience in development to deliver actionable insights for real estate investors and occupiers. A frequent source for both clients and journalists navigating moments of economic volatility, he is particularly interested in the role government stimulus plays in long-term economic recoveries.

Richard began his career as a professor of economics and land management at the University of Reading, where he earned his Ph.D. He is the author of two books and numerous academic and industry papers on the topics of real estate and entrepreneurship, including the acclaimed Real Estate and Globalisation (Wiley Blackwell, Oxford), which explains the impact of the rise of China and Brazil on real estate markets.

After more than a decade, he left academic life for the private sector, serving first as Head of Projects and Consultancy at CB Hiller Parker and later as Director of Research at the London-based property powerhouse Grosvenor Group. He was also a non-executive director of Grosvenor Fund Management, where he was involved in fund strategy, risk analysis and capital raising. He joined CBRE in 2014 as Executive Director and Global Chief Economist. He is also the Chairman of CBRE Econometric Advisors, a specialist real estate forecasting unit.

Richard is Visiting Professor of Economics at the Bartlett School of Architecture at University College London. An avid skier and sailor, he resides in Boston and enjoys spending time with his three grown children.

Darin Mellott is a Vice President of Capital Markets Research at CBRE. In this capacity, Darin leads a global team of Capital Markets Research Analysts and works with other members of senior leadership to provide analysis and develop “house views” on global markets and economic conditions, with a focus on their impact on real estate.

Beyond this, Darin leads and contributes to research and strategy efforts across the globe on behalf of clients, and has authored numerous white papers for the firm. He also represents CBRE with the media and at public forums on a frequent basis. Prior to his current role, Darin was CBRE’s Director of Research for the Americas.

Outside his formal responsibilities, Darin serves on various boards for prominent institutions and is often called upon to provide expert opinion on a wide range of issues beyond real estate, including public policy and economic matters. He also regularly provides economic and real estate insights to policymakers at the local, state and federal levels. Darin currently serves as a Senior Advisor to the Kem C. Gardner Policy Institute at the University of Utah and is a member of the Utah Economic Council.

Both in his native Utah and more broadly, Darin is recognized as a respected contributor to economic thought leadership and the business community. Recently, he was named a Forty Under 40 honoree by Utah Business, and Harvard Business School selected him to be a participant in the Young American Leaders Program—an extension of the school’s U.S. competitiveness project aimed at promoting cross-sector collaboration to solve pressing issues and achieve shared prosperity in communities.

Darin completed his Master’s Degree in Real Estate Finance at the University of Cambridge and received a Bachelor of Arts in Political Science from Brigham Young University.

Carsten Raaum is the Associate Director of Global Capital Markets Research at CBRE. Along with his team, Carsten provides commentary on the commercial real estate investment market both in the U.S. and globally. He is also involved in forming CBRE’s house-view on the economy. Carsten joined CBRE five years ago after receiving his Master’s in Economics & Policy Analysis from DePaul University in Chicago.