By Tyler Rosenlicht, portfolio manager for Global Listed Infrastructure and Head of Natural Resource Equities, and Ben Ross, Head of Commodities at Cohen and Steers.

The world is transitioning from an era of commodity abundance to one of undersupply. We believe this shift may result in significant returns for commodities and resource producers over the next decade.

KEY TAKEAWAYS

- Megatrends are impacting the commodities market

Secular forces are resulting in inadequate availability of many natural resources, which may potentially drive prices for many commodities higher in the coming years. - An alpha-generation setting for active managers

Supply and demand imbalances across the natural resource universe are creating both winners and losers among commodities and the equities of metals, energy and agriculture producers. - The case for a strategic real assets allocation is strong

Whether as standalone investments or in a multi-strategy real assets allocation, natural resource equities and commodities merit strategic positions in a well-diversified portfolio, in our view.

Megatrends are reshaping demand for commodities

Throughout history, commodity demand has been a function of population and economic growth. This relationship is becoming supercharged, as powerful secular forces are increasing the intensity of commodity use globally.

The green energy transition

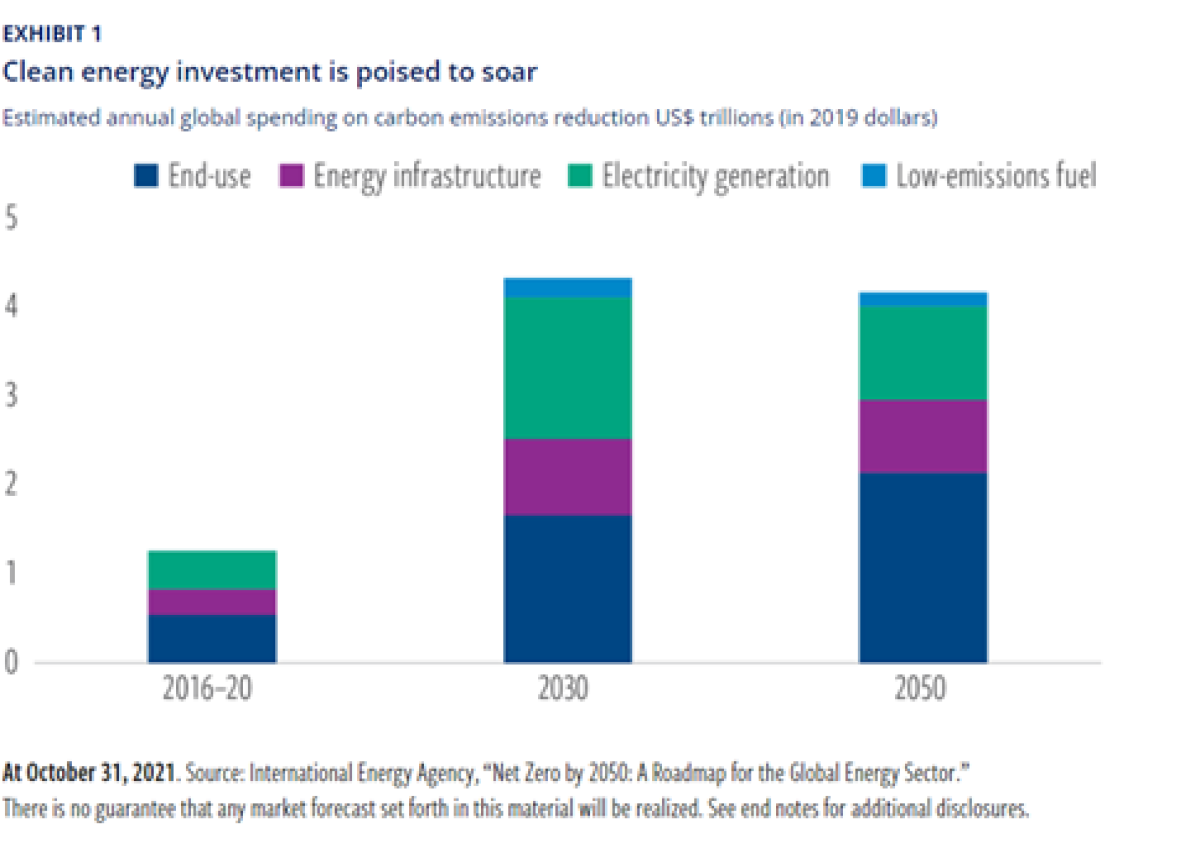

Still in the early innings, efforts to reduce global carbon dioxide (CO2) emissions are fueling the rapid adoption of renewables and energy- efficient technologies (Exhibit 1). The International Energy Agency (IEA), in a joint analysis with the International Monetary Fund (IMF), estimates that total annual investment in clean energy and energy infrastructure will more than triple by the end of the decade, adding an extra 0.4 percentage points per year to annual global GDP growth.

The green/decarbonization transition has been and will likely continue to act as an accelerant to the demand for many raw materials, including base metals, precious metals and agriculture commodities (such as sugar, corn and soybeans used to make biofuels). For instance, the amount of copper used in an electric vehicle (EV) can be as much as three times greater than what’s in a conventional auto. As the world adopts EVs and invests in powerlines, wind turbines and other facilitators of the energy transition, we expect commodity demand to benefit materially.

Of course, the energy story is not just about alternatives. As we reasoned in a recent paper (Changing the imperative from ‘energy transition’ to ‘energy addition’), aggregate energy demand is likely to continue to increase for decades due to economic growth. This will create opportunities in the traditional energy value chain as well.

An expanding global middle class

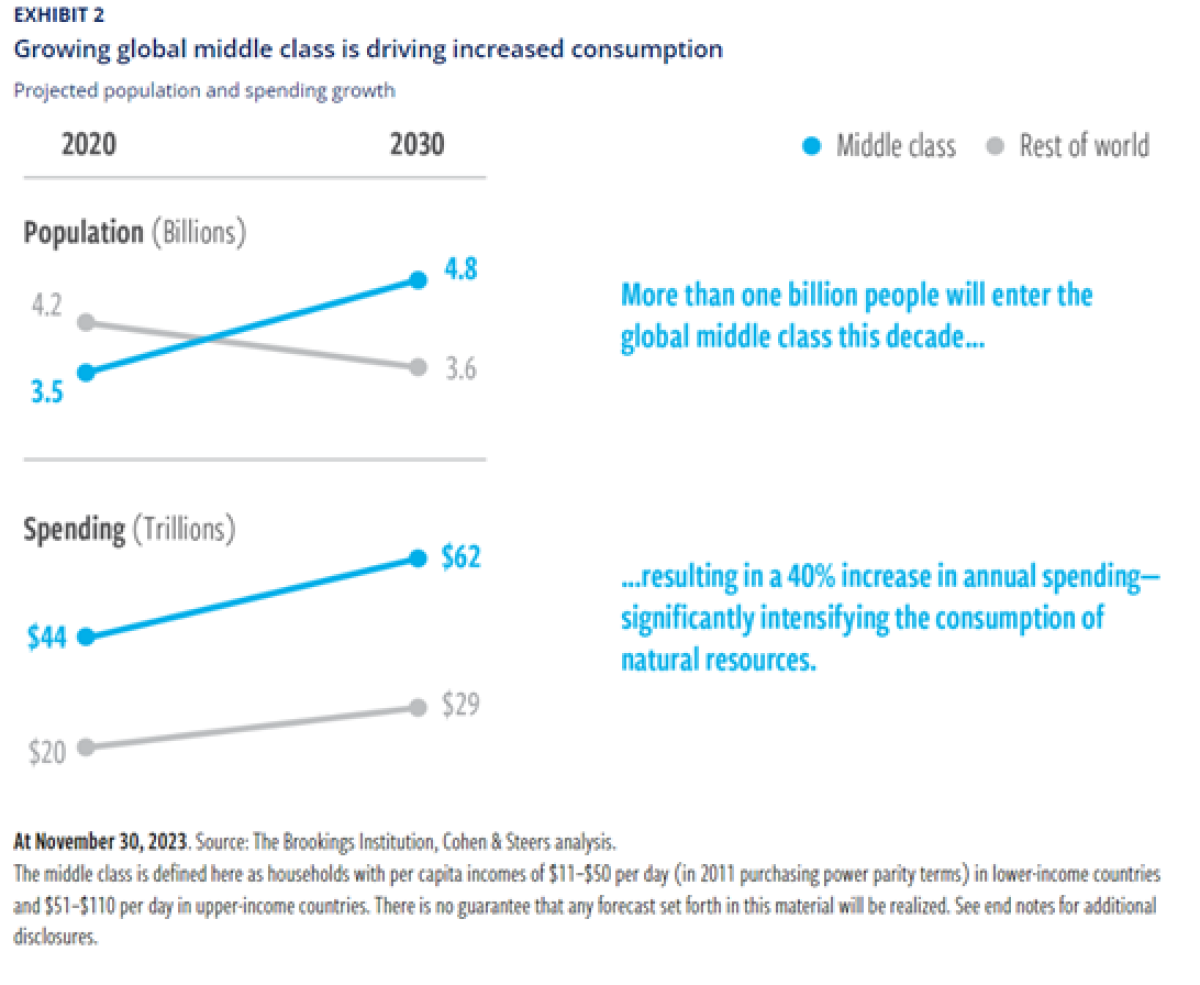

In the next six years alone, the world’s population will increase by approximately 500 million to reach 8.4 billion (on its way to 9.7 billion by 2050), according to United Nations estimates. Population growth and urbanization have long driven resource consumption. Humanity’s call on resources will be stretched further, with 700 million more people living in cities by 2030 than in the previous decade.

Even more significant is the rapid expansion of the global middle class. The middle class is already the largest spending group in the world, accounting for one-third of the global economy. By 2030, the global middle class (also termed the “consumer class”) is expected to reach 4.8 billion people. This group’s purchasing power is expected to rise to $62 trillion annually, which would have a meaningful impact on consumption—and, consequently, demand for natural resources (Exhibit 2).

Most of this growth is occurring in developing economies, where per capita consumption of energy and materials is significantly lower than in developed economies. According to the IEA, lower-middle income countries currently consume 6,658 kWh of energy per capita, compared with 56,469 kWh in high-income countries. With its increasing wealth, the expanding middle class will require more food, energy and many other commodities to help meet its needs.

Commodity supply growth may be hampered by structural factors

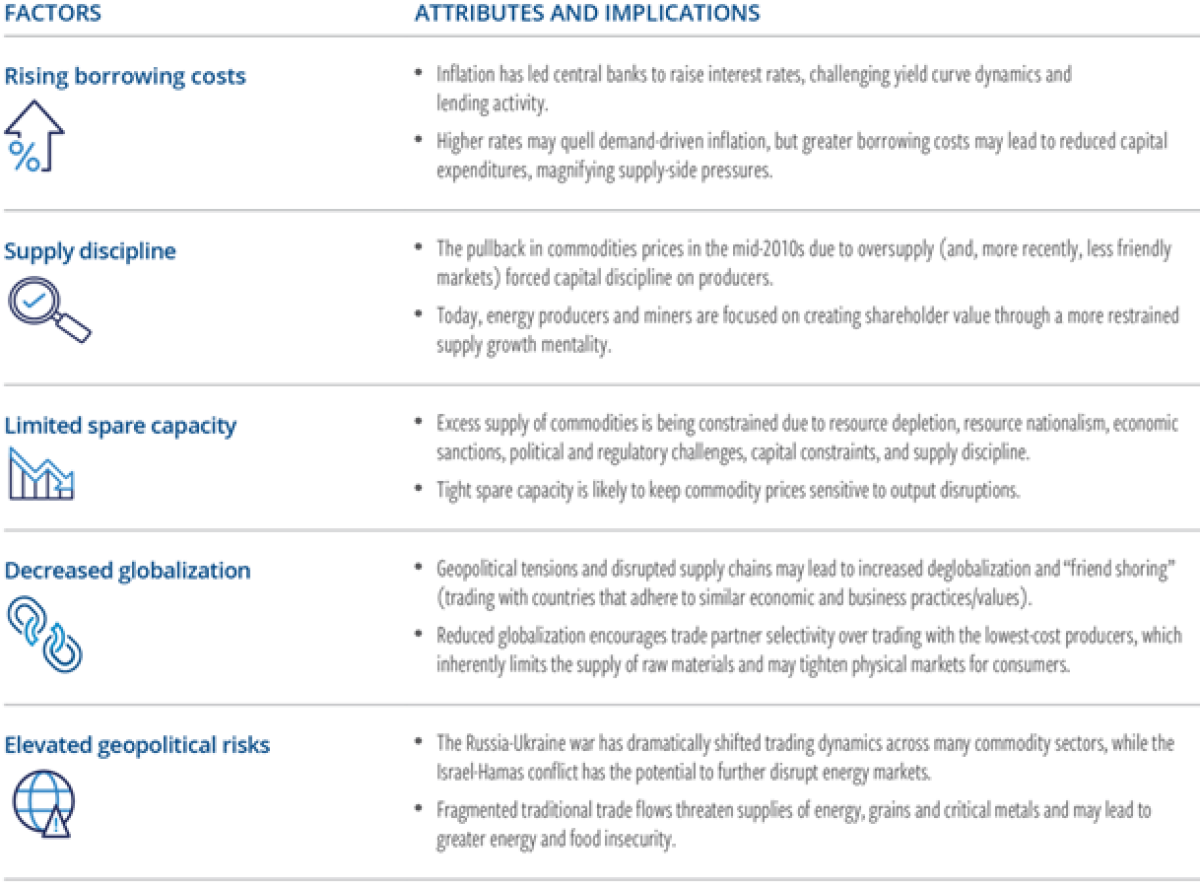

The current decade is likely to be distinctly different than the last, which was a period marked by persistent surplus and, as a result, relatively low commodity prices. Today, inventories for many commodities are below their respective long-term averages, and we believe the supply of many commodities will remain structurally constrained going forward—contributing to the risk of unexpected inflationary bouts—due to numerous factors, including:

We believe the combination of secular demand drivers and limited ability to accelerate supply growth will result in higher commodities prices.

An alpha-generation setting for active managers

Energy

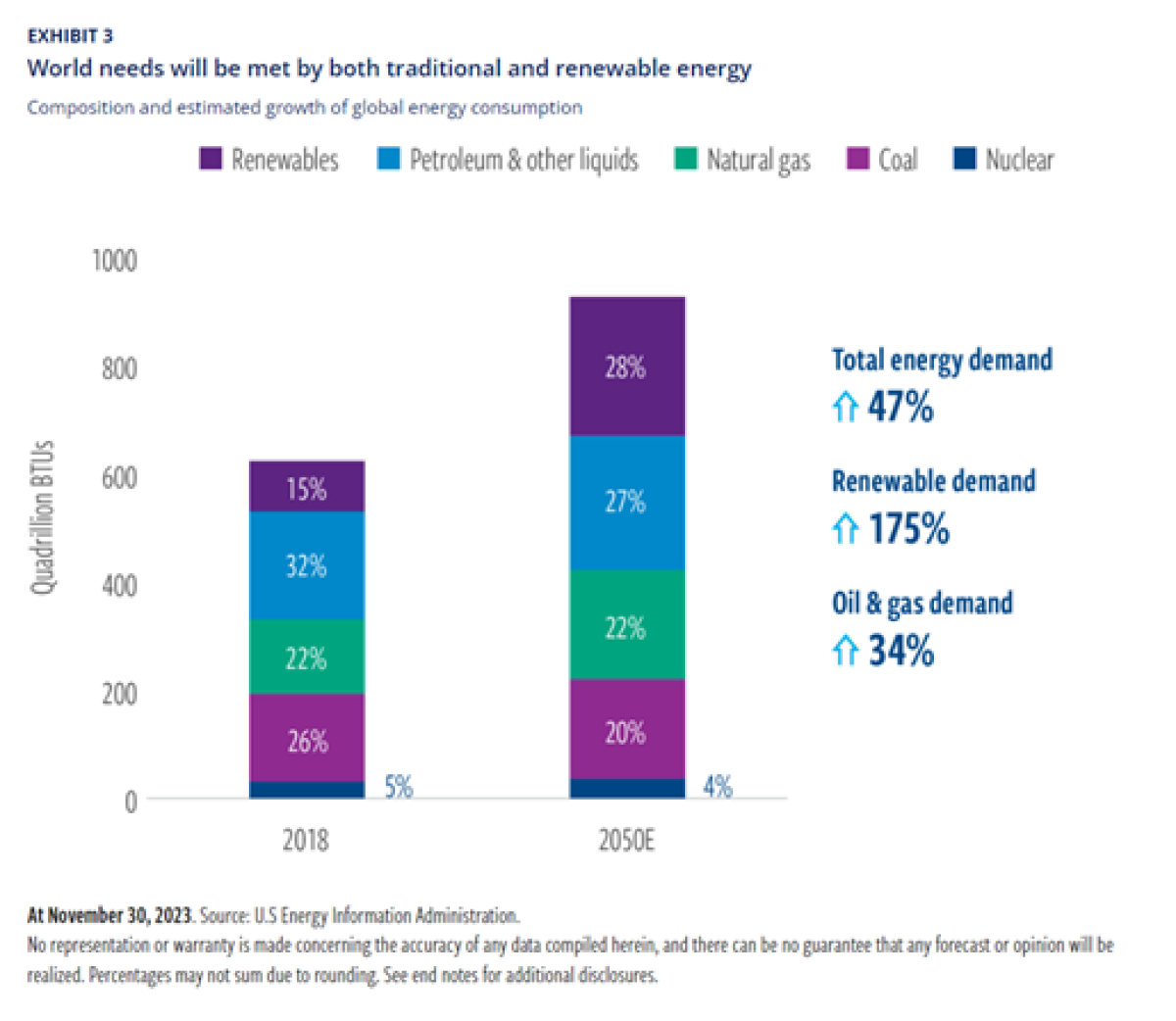

Population growth and rising incomes in developing economies mean the world’s consumption of energy will continue to expand for decades, even as energy efficiency accelerates and net-zero carbon emissions initiatives across 110 countries take hold. Alternative energy is expected to see significant market share gains, but demand for fossil fuels should increase meaningfully as well (Exhibit 3).

We believe the global energy markets will see significant declines in demand for coal and biomass. We expect crude oil demand to grow through the 2020s and then plateau and modestly decline during the 2030s; in our view, growth afterward will come from natural gas, nuclear and renewables such as wind, solar and hydrogen.

Within the resource equities space, we see four possible outcomes for energy companies: (1) traditional energy businesses that will adapt and thrive under the new energy regime, (2) traditional energy businesses that will become obsolete, (3) alternative energy businesses that will become the growth engines of the future and (4) alternative energy businesses that will fail to live up to their hype.

Metal

Metals demand has been steadily growing, driven by the global forces surrounding industrialization and urbanization. The last supercycle resulted from China’s rapid industrialization, urbanization and capital formation. Many other large, emerging economies, such as India, remain in the early stages of economic development and have a growing appetite for metals.

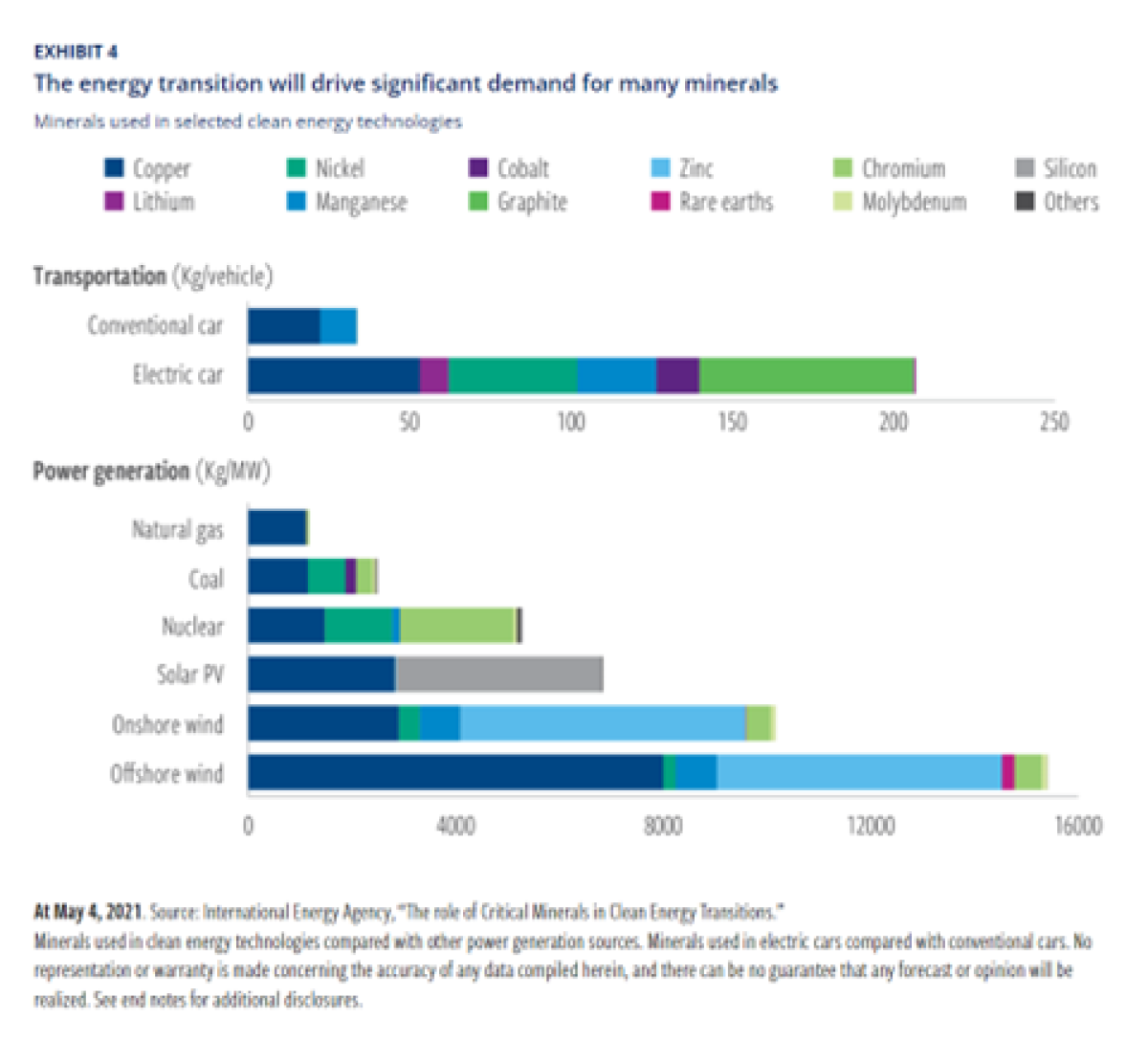

Metals demand will be further lifted by energy transition needs (Exhibit 4). Carbon-neutral requirements call for the massive deployment of a wide range of clean energy technologies, many of which rely on critical minerals such as copper, lithium, nickel, cobalt and rare earth elements. As demand pushes prices meaningfully higher, users will typically seek out alternatives. In some important instances, however, economically viable substitution is not always possible.

For copper, perhaps the most critical element in the energy transition, demand is expected to grow 82% between 2021 and 2035 as economies target the goal of net zero emissions by 2050, according to S&P Global.

We believe the marginal cost for many metals will rise sharply over time given (1) a higher cost of capital, (2) operating expenses pressured by inflation, (3) continued erosion of supply resiliencey, and (4) management teams that remain unwilling to greenlight new investments.

Agriculture

Rising income levels, shifting diets and an increasingly crowded world will require a significant expansion in food production over the next several decades. It is well established that the average caloric intake per person increases as per capita income rises. Additionally, higher incomes translate into an increase in animal-derived protein consumption.

In addition to feeding humans, crops such as soybeans, corn and sugarcane are also used as feedstock for the production of biofuels. Increasing demand for biofuels, supported by government green energy policies worldwide, is reigniting the food vs. fuel debate that contributed to price spikes in the mid-2000s to early 2010s. The IEA expects global biofuel demand to increase by more than 20% in the five years ending in 2027. Increased production of feedstocks to meet the growing demand will require additional resources and compete for arable land, which will likely drive prices higher, benefiting producers.

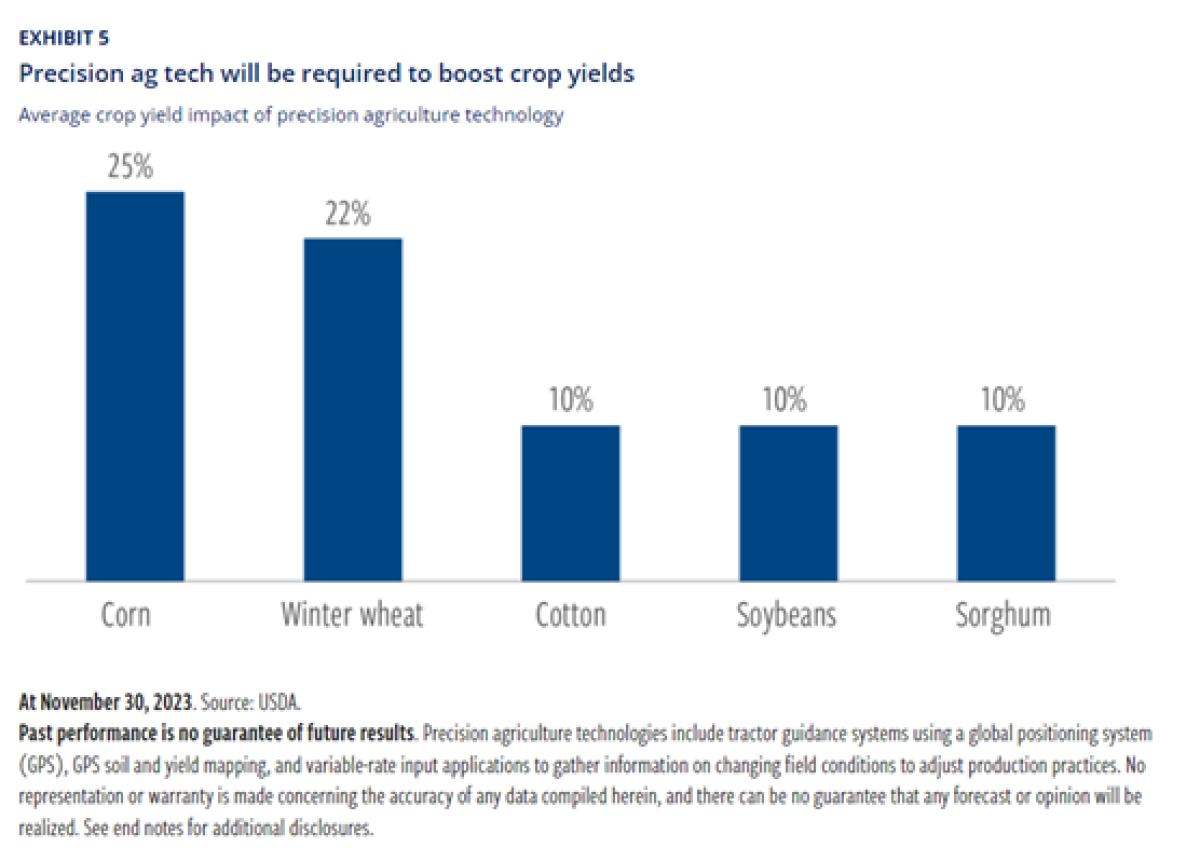

The continued adoption of technology that allows farmers to increase efficiency will play a central role in meeting these needs (Exhibit 5). The future of agribusiness and agricultural commodities rests on creating more output per acre, and those companies well positioned to facilitate this transition stand to benefit materially.

Precision ag adoption and optimizing for other factors that affect yield (chemicals, seed variety, etc.) can generate considerable increases in crop yields.

Regime shift favors inflation-linked assets

Considering the anticipated gap between strong demand and limited supply, potential issues such as labor shortages, a move towards more selective trade partnerships, and the potential for increased geopolitical uncertainty, we expect inflation to average 3% or more in the coming decade. We also believe the next decade will feature significantly higher volatility of inflation, with the potential for periodic inflationary shocks. In contrast, in the last decade, inflation was stable and averaged less than 2%.

We believe this new environment will favor real assets—asset classes that typically have high, positive sensitivity to inflation.

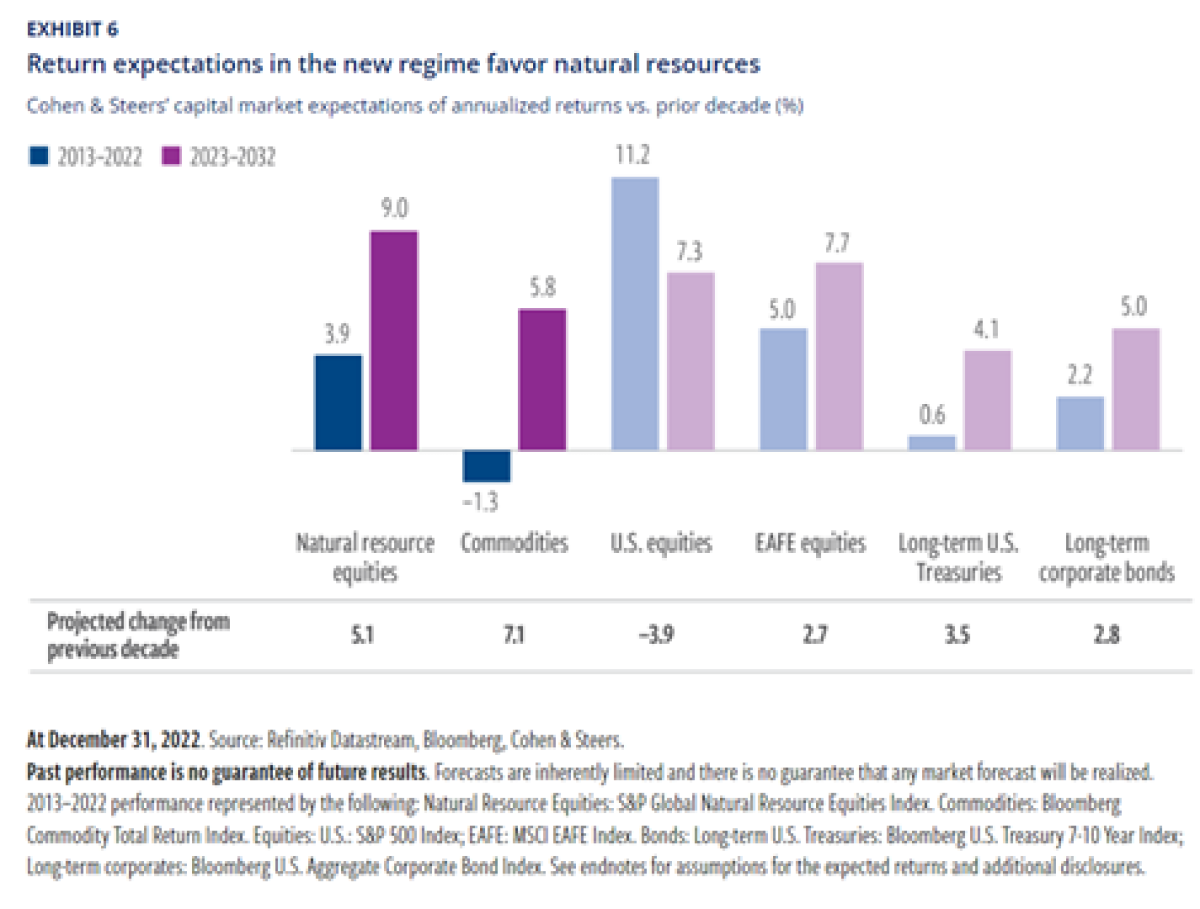

Commodity returns could see a marked improvement over the previous decade (Exhibit 6). This would be driven by a combination of supply/demand imbalances, higher production costs, and higher expected collateral returns. In the case of the latter, the sharp rise in short-term interest rates in the past two years (and the potential for rates to remain “higher for longer” going forward) is likely to result in greater interest income on collateral set aside for the purchase of commodity futures.

Returns in natural resource equities over the next 10 years are expected to exceed those of the broader global equity market. Greater extraction costs, increased regulation, resource scarcity and recent underinvestment are all likely to play a role. At the same time, the revenue pressures resource producers have faced in recent years have instilled greater capital discipline and a focus on profitability, which may also support valuations.

A counterbalance for traditional stock/bond portfolios

The current economic environment—marked by elevated inflation, rising interest rates, deglobalization, tight labor markets and heightened geopolitical risks—is likely to drive long-term investor interest in real assets, particularly natural resource equities and commodities. Whether as standalone investments or as part of a diversified real assets allocation, we believe natural resource equities and commodities merit permanent positions in a balanced portfolio.

Given their vital role in sustainable development and decarbonization, commodities and resource producers potentially stand to generate above-average returns in the coming decade. History shows that inflation tends to be most damaging to stocks and bonds when it is unexpected. In contrast, our analysis suggests that real assets tend to experience strong returns precisely during those periods when realized inflation exceeds prior expectations.

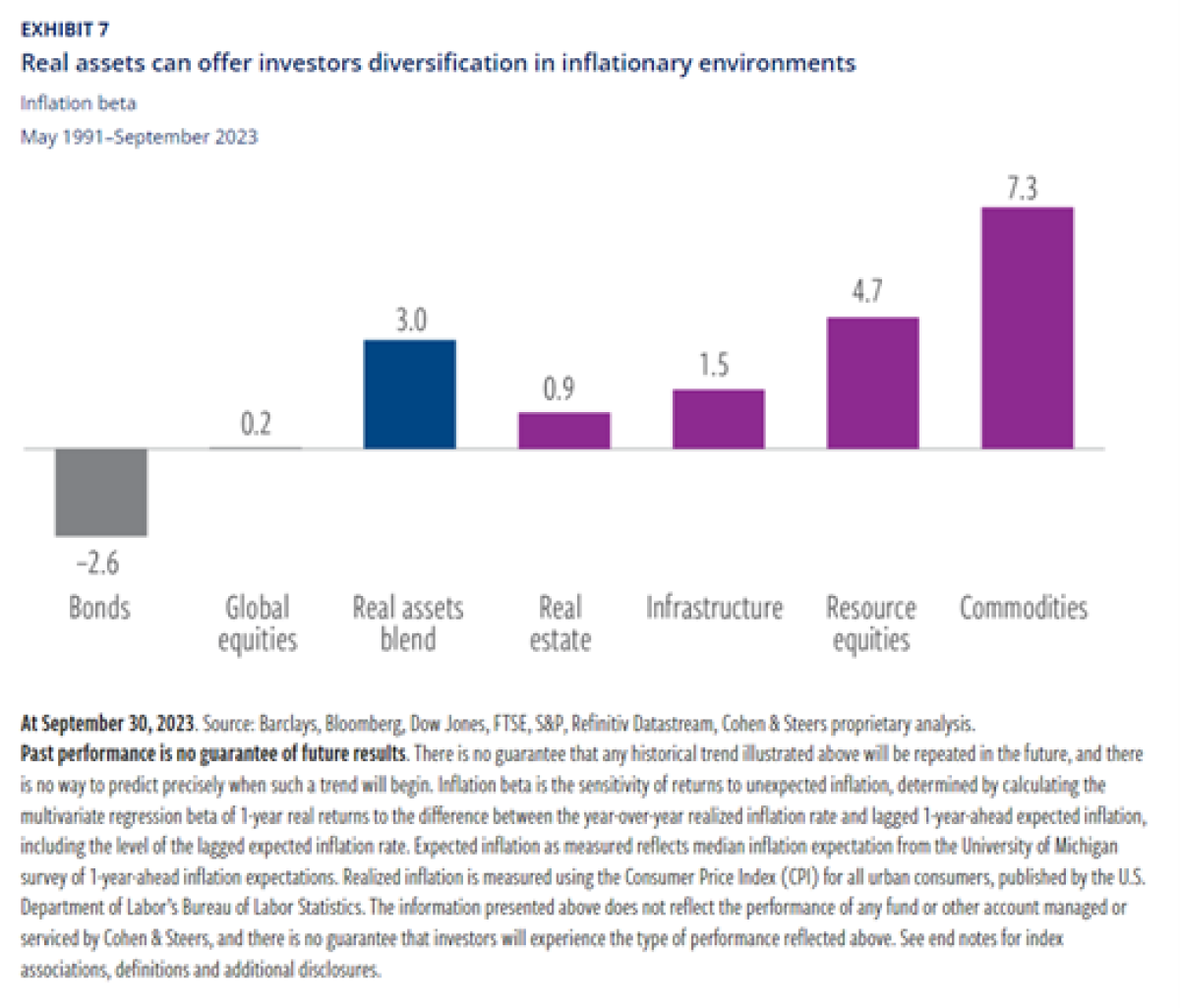

Exhibit 7 shows the impact of unexpected inflation using a metric we call “inflation beta.” Inflation beta measures the sensitivity of returns to a 1% upside surprise in realized inflation (relative to the inflation estimate from a year before). An asset class with a positive inflation beta should generally react favorably to inflation surprises. For instance, the chart below shows that commodities historically outperformed their long-term average by 7.3% for every 1% that inflation exceeded its prior-year estimate. We believe this is a strong indicator that real assets can serve as an effective inflation hedge (though they are not dependent on inflation to produce strong returns).

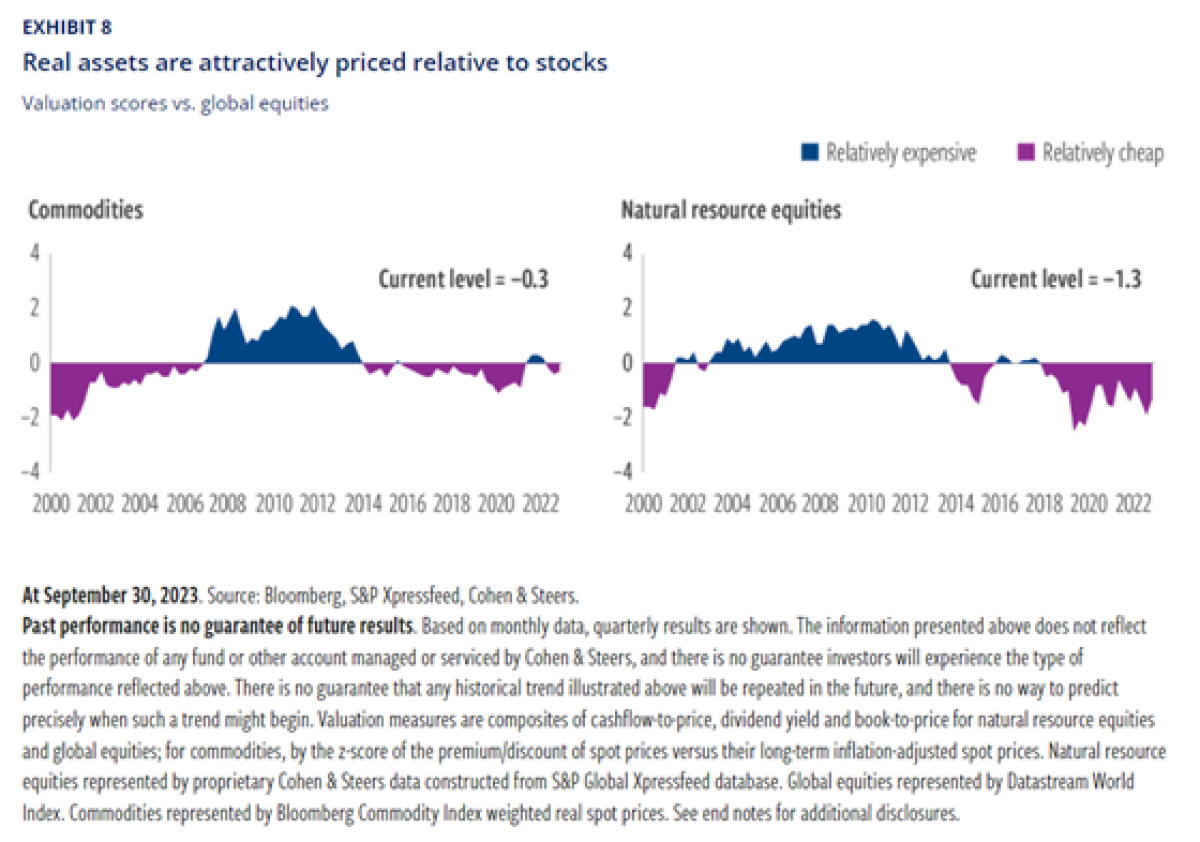

Enhancing their appeal, commodities and natural resource equities’ current valuations and financial profiles are attractive compared with history (Exhibit 8). For instance, as a whole, natural resource producers today are generating significant free cash flow, have low debt-to-equity ratios and have limited capital outlays compared with past cycles.

A blended solution

Given the regime shift now underway, a diversified multi-asset-class approach to real assets offers distinct advantages from an investment perspective, historically providing:

- Outperformance in inflationary periods

- Enhanced risk-adjusted returns via portfolio diversification

- Strong total returns over full cycles

No single real assets category (including global real estate and global listed infrastructure, in addition to natural resource equities and commodities) offers a “silver bullet” solution that excels across all three criteria of prospective diversification, expected returns and potential inflation protection. However, a diversified portfolio of real assets may help investors better navigate the tradeoffs of individual categories and may effectively enhance the risk/return profile of portfolios concentrated in stocks and bonds.

Given supportive fundamentals and attractive valuations, we believe real assets are poised for a multi-year period of outperformance.

About the Authors:

Tyler Rosenlicht, Senior Vice President, is a portfolio manager for Global Listed Infrastructure and serves as Head of Natural Resource Equities. Prior to joining the firm in 2012, Mr. Rosenlicht was an investment banking associate with Keefe, Bruyette & Woods and an investment banking analyst with Wachovia Securities. Mr. Rosenlicht has a BA from the University of Richmond and an MBA from Georgetown University. He is based in New York.

Ben Ross, Senior Vice President, is Head of Commodities and a portfolio manager for Cohen & Steers’ commodities strategy. Prior to joining the firm in 2013, Mr. Ross was a co-portfolio manager at GE Asset Management and a manager of the GE Active Commodities strategy since its 2006 inception. Previously, Mr. Ross was a senior trader at GE Asset Management, leading the international equity trading desk. Before joining GE in 1996, he worked at State Street Bank & Trust. Mr. Ross has a BS from Northeastern University and is based in New York.