By David Donahue, Partner at Mbuyu Capital Limited.

EXECUTIVE SUMMARY

This brief explores the burgeoning ecosystem that has propelled the rapid increase in the availability and consumption of Alternative Protein.

Private investment, including venture capital and private equity, plays a pivotal role in transforming industries and solving societal and environmental problems by providing funding, guidance, and support to innovative startups and early-stage companies followed by growth capital and combined with later stage private equity investment. Consequently, private capital investments can contribute significantly to addressing critical issues and transforming industries for the betterment of society and the environment. As a result, venture capital and private equity fund managers are frequently the focus of private market participants, including allocators and investors.

However, while perhaps less recognized, a large support system exists which enables these developments. Where appropriate, consideration is given to why this industry vertical may evolve differently than other growth segments as a result of this support.

Introduction: What is Alternative Protein & Why Review the Ecosystem?

Consumer food products produced using various protein sources have been gaining popularity due to their sustainability and potential health benefits. These product types include:

The description Alternative Protein is frequently used to differentiate food products containing protein derived from non-animal sources. Beyond its immediate role in human nutrition, the innovative expansion of protein sources also extends to animal nutrition and contributes to the broader human food supply chain. This article focuses primarily on the more recent developments in the area of Alternative Protein consumer foods including meat, egg, or dairy replacements that are plant-based or fermentation-derived, thus produced without conventional animal agriculture.

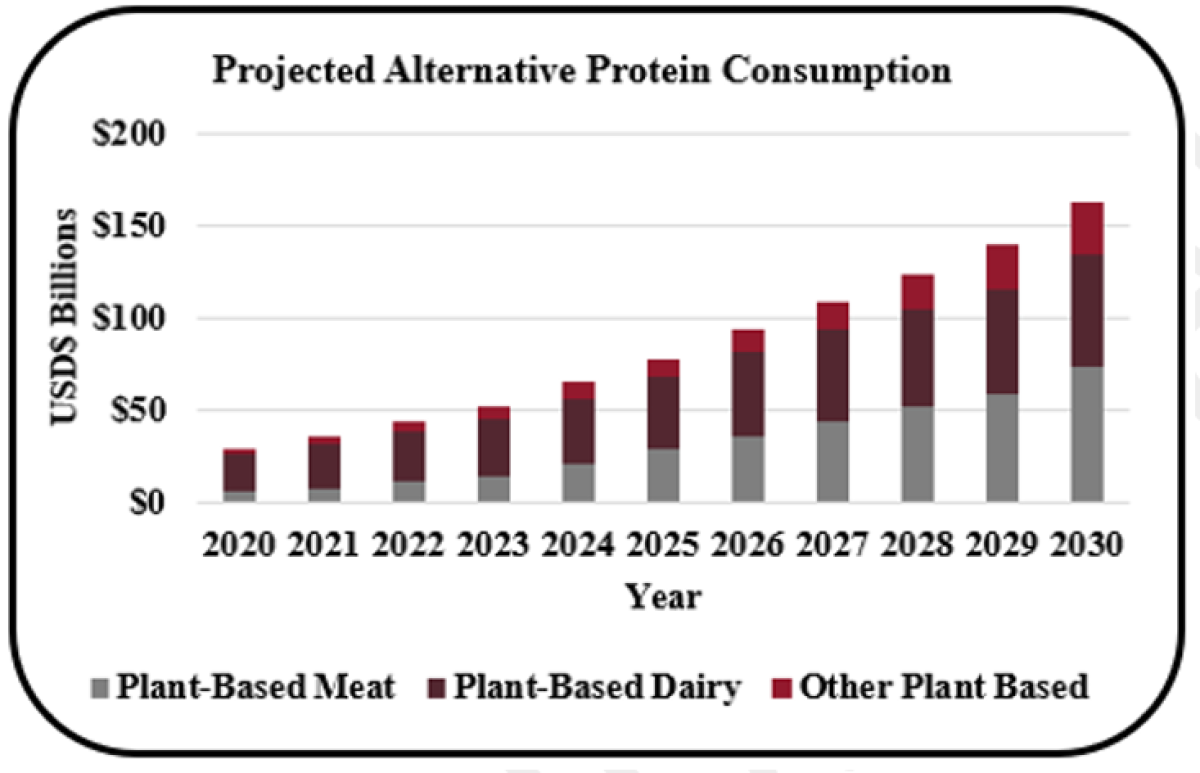

There are many fundamental drivers of the more recent rapidly growing interest in this area from consumers, investors, and others including 1) health & wellness, 2) animal welfare and the associated risk to humans of antibiotic resistance, 3) increasing availability of improved product offerings, and 4) environmental concerns, including climate, related to traditional animal-based food production. The symbiotic rise in consumption and investment within the Alternative Protein vertical underscores its transformative potential and, according to numerous forecasts, is expected to continue:

Source: Bloomberg Intelligence (additional industry forecasts appear below).

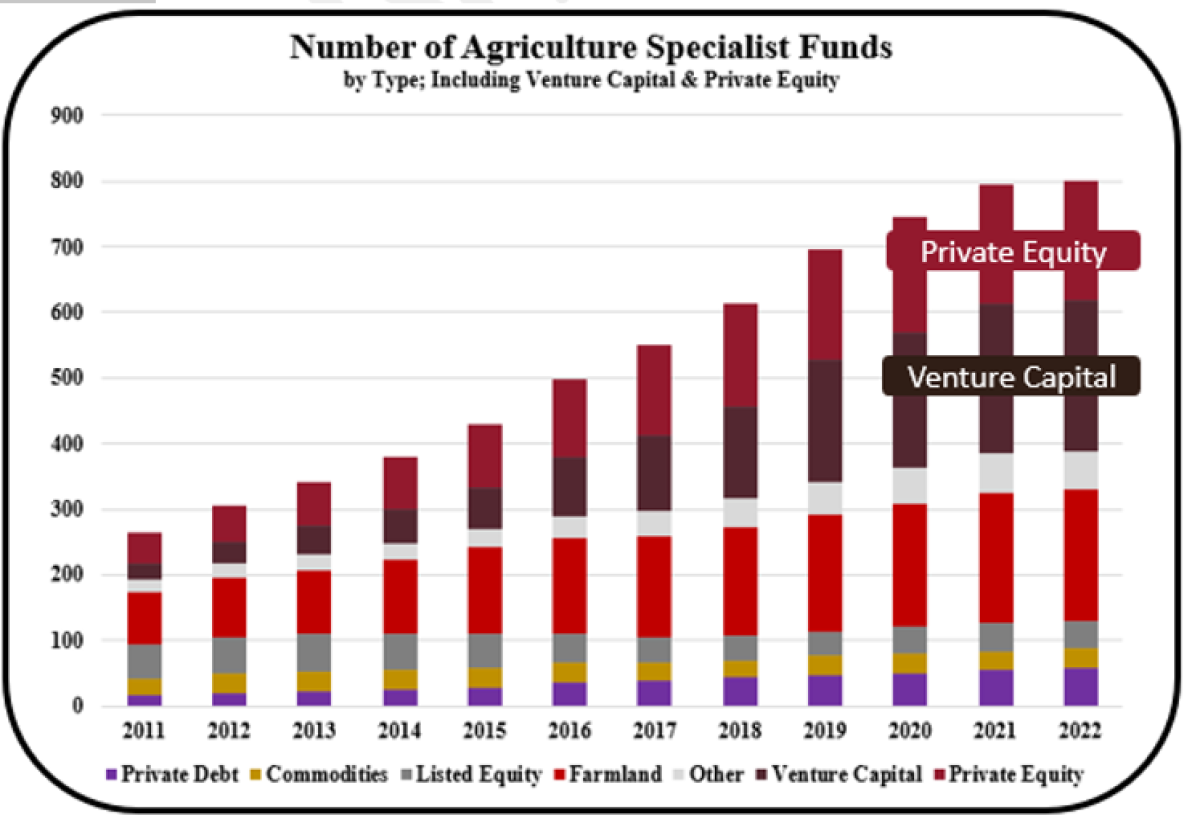

Investor interest in the agriculture sector broadly has increased over the past decade for many reasons, including interest in increasing food security, resulting in a growing number of agriculture specialist-only funds:

Source: Valoral.

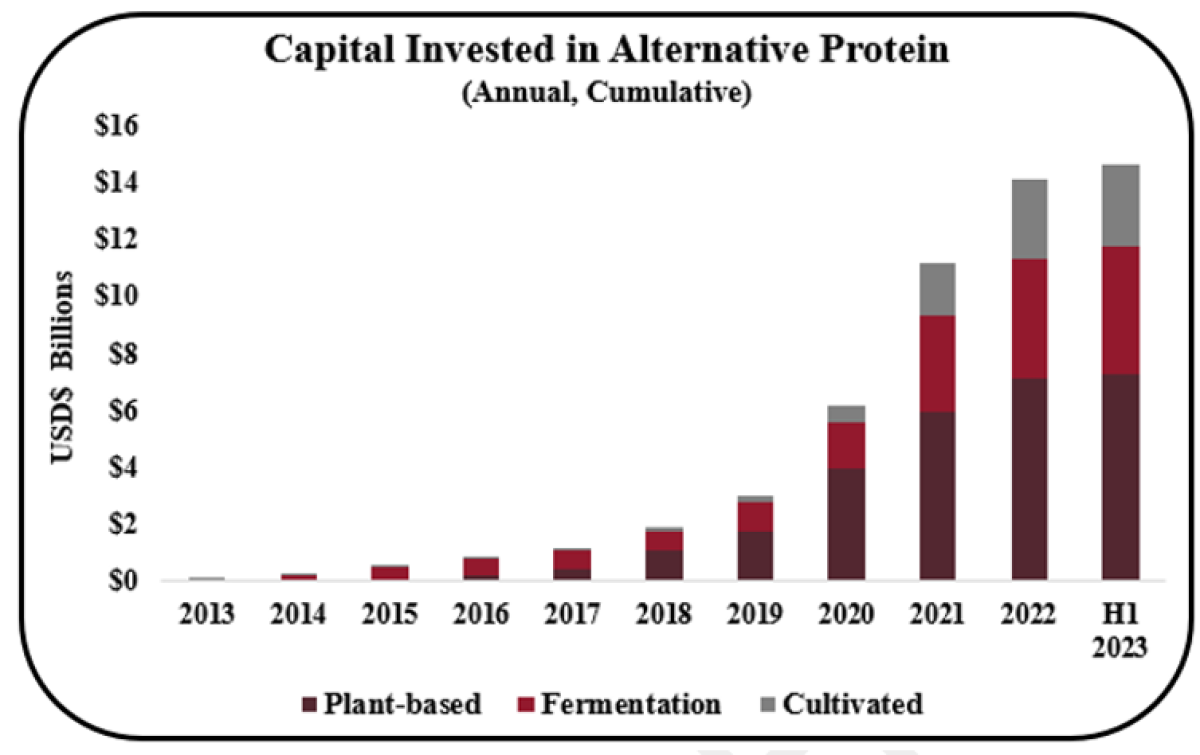

Against a backdrop of recent slowing overall investment in venture capital and private equity, after a period of unprecedented high activity, there remains continued interest in Alternative Protein investment given medium and long-term expectations, the transformative potential, and resulting opportunity:

Source: GFI.

When sourcing investment opportunities it is always necessary to understand the industry participants, drivers, constraints and general environment, and this appears particularly relevant in the case of Alternative Protein for reasons discussed further in the following sections. The sections below provide a brief general overview of ecosystem components, with a description of the developments and activity supporting the Alternative Protein vertical specifically.

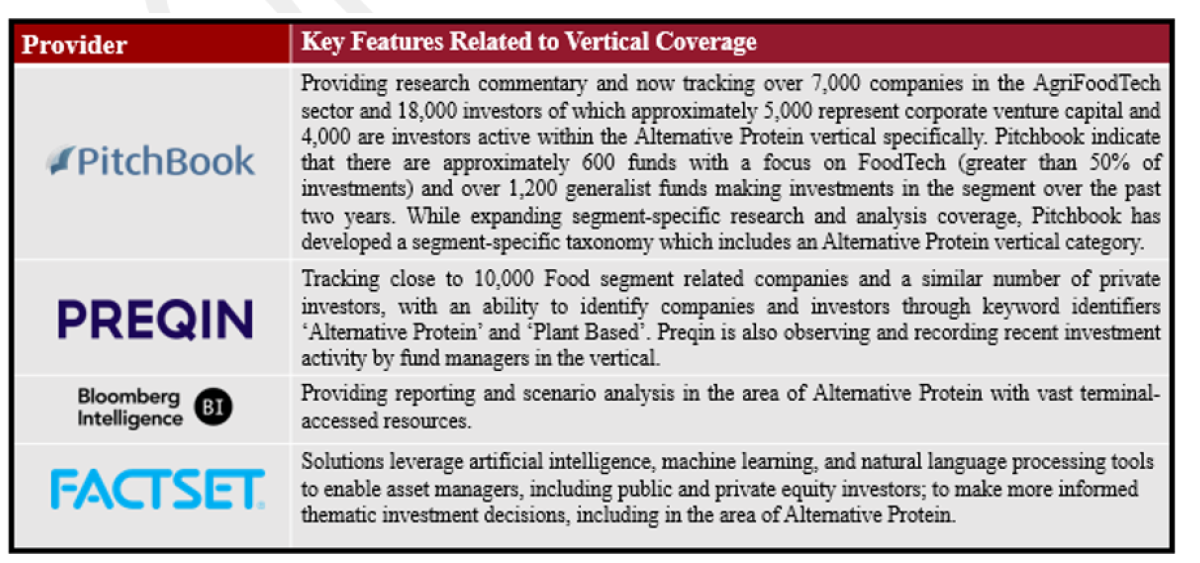

1. INFORMATION & ANALYTICS SERVICE PROVIDERS

Leading information and analytics systems now enabling vertical specific analysis include:

Other providers initiating vertical coverage include Crunchbase, CB Insights, and Tracxn. For investors seeking specific company investment opportunities there are platforms available including Aurigin and PrimaryMarkets with a number more focused on the AgriFoodTech segment, for example; Foodtech Database maintained by dealroom.co, Seedblink, ForwardFooding, the Good Food Institute’s (GFI’s) Investor Directory and Company Database, DigitalFoodLab, TRIDGE, and additionally Vevolution providing access to Alternative Protein-focused funds.

Expanding coverage of the vertical is beneficial as investors frequently rely on these systems to inform the investment decision-making process.

2. INDUSTRY ASSOCIATIONS & PHILANTHROPIC SUPPORT

Alternative Protein is differentiated from most evolving industry verticals as there has been meaningful philanthropic support promoting a transition within the established food system for reasons including climate, human health, and animal welfare. Organizations advancing adoption, with some that have been established to specifically support investment in the Alternative Protein vertical, include:

While multi-faceted, the communication and knowledge dissemination these organizations furnish, with an increasing reach, is essential to advancing activity for emerging solutions.

3. DEDICATED MEDIA & CONFERENCES

Media outlets focused on the Food and Alternative Protein segments include:

AgriFoodTech investment manager, AgFunder, recognized this need and established AgFunder News to promote awareness. These organizations, and others, host an increasing number of events to promote awareness and allow for the exchange of new ideas including:

Media outlets and related conference events are key in providing education and drawing attention to new areas for investment with attention paid to consumer and investor interest through surveys and on-line monitoring.

4. FINANCIAL SERVICES PROVIDERS AND INVESTORS

Investment Fund Managers

Leading private fund investors include a combination of specialist AgriFoodTech and Alternative Protein-focused investment managers along with more generalist fund managers. While there are hundreds of funds which focus on AgriFoodTech, more recently active fund managers investing in Alternative Protein include:

It should be noted that generalist investment managers, as well as investment managers with a climate focus, such as Generation Investment Management, have also been active in the vertical. More vertical-focused fund managers include:

Other focused funds are recorded by dealroom.co and hosted on the Vevolution platform. These investment managers have received commitments from institutional investors such as Unigestion and Nuveen.

Placement Agents & Fundraising Consultants

External placement agents can be extremely beneficial with some positioned to access investors motivated, at least partly, by ESG and Impact considerations. Examples include Valoral Advisors, specializing in the food and agriculture sector, Campbell Lutyens, a leading fund placement and secondary advisory firm supporting sustainable agriculture strategies, XS Investments, having recently supported fundraising for Unovis Asset Management, and related efforts of c*funds, and Provenance Capital Group.

Accelerators, Incubators & Tech Hubs

A pivotal force driving vertical growth, accelerators, incubators and tech hubs are designed to fast-track start-up development. They provide resources such as mentorship, funding, networking opportunities, and access to industry-specific expertise. Tech hubs, often providing physical space, serve as collaborative ecosystems where entrepreneurs, researchers, and industry experts converge to foster innovation.

Accelerators and incubators supporting the development of Alternative Protein ventures include:

Additional examples can be found on this Accelerator Map. StartLife is a leading European example:

Investment Banks & Asset Managers

Many traditional and investment banks have supported Alternative Protein companies’ equity and debt fundraisings with ongoing analyst coverage, mergers and acquisitions, risk management including hedging for commodity exposure and other corporate finance functions. Rabobank is a leader with dedicated resources including research, broader agriculture sector expertise, the support of accelerators and an investment fund. JP Morgan, BNP Paribas, Invesco and Barclays have also been active regarding more sustainable food and agriculture production. Arranging investment from bank and investment manager clients, especially those with an ESG Impact focus related to climate or other issues, has attracted additional interest and capital. For example, Agri-Food investor PeakBridge is a member of the Edmond de Rothschild Private Equity Partnership. For listed equities, five investment managers including Fidelity International, USS, Columbia Threadneedle, BNP Paribas Asset Management and AVIVA Investors, representing $3 trillion of assets, have recently formed the Asia Protein Transition Platform with a goal of security by growing the share of sustainable protein.

Providers of Sustainable and Impact Capital, Including Blended Finance

Agriculture and food production of any type is commonly exposed to sector-specific risks including commodities prices, disease, climate and immediate weather events, pests, and perishability resulting in supply-chain requirements such as cold-chain capability. Additionally, partly given these factors, lead times for innovation and capacity building can take time that exceeds a venture capital or private equity fund’s intended holding period. Within this context it is recognized that additional financing sources suitable for the risks faced by some business models and plans will be required. Examples of appropriate financing sources, including blended finance, venture debt, asset based lending, venture philanthropy, revenue based financing, cover a range of approaches from many institutions e.g. Triodos Bank, AgDevCo, IFC, IMPACT ENGINE and many development finance institutions and agencies (DFIs and DFAs), with more expected to fill the requirements of abundant transformation opportunities.

Corporate Venture Capital & Incumbents or Strategic Players

Corporate Venture Capital and investment by incumbent or strategic players are significant as the food industry is a competitive space and new entrants must operate initially without the advantages enjoyed by large, established providers already benefiting from scale advantages, established networks/distribution channels, and vast experience.

Key players operating in the global plant protein market for food and beverage include:

In addition to making strategic acquisitions in the sector many have established Corporate Venture Capital (CVC) arms in order to maintain presence and remain competitive as the industry evolves rapidly through research & development. Examples include Tyson Ventures, Cargill Protein, ADM Ventures, Kellogg’s Eighteen94 Capital and Unilever as the company is “seeking to shift to non-animal-derived product and ingredient replacements”. Many large retailers have introduced own-label plant-based lines. Of the 60 largest global meat, dairy, and seafood companies tracked in The Coller FAIRR Protein Producer Index, half are investing in the Alternative Protein market as of 2022, more than double the amount in 2019. Moreover, large food companies see protein diversification as a material business issue; according to FAIRR, 35% of the 23 largest food manufacturers and retailers globally have committed to increasing the volume or sales of meat alternatives and/or dairy alternatives, up from 28% in 2021.

All of the related activities, often acting in combination, are essential to advancing activity.

5. CONSULTANTS, DUE DILIGENCE & ADDITIONAL SERVICE PROVIDERS

Consultants & Due Diligence Providers

Larger consulting firms covering the growth and potential of the vertical include McKinsey, Boston Consulting Group (BCG), Bain & Company, Roland Berger, L.E.K. Consulting, Kearney, and OC&C Strategy consultants with NielsenIQ (NIQ) providing necessary consumer trend data and insights. Notably, ‘Big Four’ professional services firms PwC, EY and KPMG have all initiated coverage of the vertical, with Deloitte having established a future of food practice area.

Detailed segment research produced by Future Market Insights (forecasting 19% market CAGR 2023 to 2033), BCC Research (forecasting nearer term market growth to 2027), Global Data, EuroMonitor, Grand View Research, Mintel, and Meticulous Research (forecasting 13% CAGR to 2030) is important, partly as demand projections can guide investors, including strategic investors, towards better opportunities. As an example, Meticulous Research’s dedicated practice area uses a detailed top-down and bottom-up methodology, employing technology, to collect updated market information from a wide range of public and private sources to inform projections.

More segment-specialist consultant work is progressed by groups focused on consumer food products, and even on Alternative Protein specifically, with examples including NIZO, Bright Green Partners with an established expert network, Food XLerator, AFRY, Digital Food Lab, sevendots, GEP, Pen & Tec, CADENT Consulting, Bryant Research, GlobalData-Foodservice, Cadence Consulting, Forward Fooding and The Food Institute.

For many larger investors, consultants such as Meketa Investment Group, Callan, Hamilton Lane, Albourne Partners, Aksia, StepStone Group, and Cambridge Associates are influential and continue to enhance their ESG and Impact capabilities with some highlighting the potential of the agriculture and food sectors.

ESG & Impact Consultants

Activities includes risk assessments, ESG due diligence, reporting and disclosure with ESG performance measurement against key performance indicators, along with ongoing training and education which can be of particular importance to investors promoting agriculture-related impact goals or with climate related objectives. Climate assessments across Scope 1 through 4 reporting areas are of growing importance generally, and especially so given the potential for exposure related to food production.

While the extent of the work of the external professional services firms can often be underestimated, it is essential to acquire suitable, reliable, and investable opportunities. The expanding coverage of industry experts and consultants is essential due to the influence on decision-making that results from expertise accessed. Many investors tend to focus on ESG, and the assessment and measurement of impact objectives is increasingly crucial, particularly due to the sustainability concerns in the agricultural sector.

6. ACADEMIC LINKS

Support from educational institutions can be formal and/or informal. In addition to entrepreneurship and venture investment programs, advancement towards sustainable food systems is facilitated through many functions including:

Research and Development

Disciplines include food science and technology, agriculture and environmental sciences, engineering and automation, sensory science and consumer behavior, economics and policy studies, and health and nutrition. For example, food science research and applications are instrumental in developing products that appeal to consumers and provide nutritional benefits. From an early stage of development it can be expected that further advances will result from new research efforts. Studies of the nutritional benefits of plant-based protein are increasingly being conducted as necessary for health considerations and to satisfy consumer concerns about the suitability of product choices.

Understanding consumer behavior, delivering attractive products and encouraging familiarity and comfort with new products will be essential to further on-going consumer adoption.

It is crucial that development and training in engineering and automation is necessary to develop production of new food products as necessary to achieve production efficiency and economies of scale and price competitiveness.

Collaborative Partnerships & Knowledge Dissemination

Partnerships and knowledge dissemination can take many forms and are suitable for an audience that is increasingly concerned about issues related to animal agriculture. Recognizing the potential, the GFI is establishing student groups at a growing set of institutions including Cambridge University and is supporting interdisciplinary research. In the United States, Land Grant Universities engage in agriculture-related research and generally have established networks providing extension services to agriculture growers which can be beneficial in allowing a transition to the supply of profitable outputs. Public-private partnerships such as the Foodvalley sited on the Wageningen University campus in the Netherlands are designed to increase collaboration. The National University of Singapore has initiated an Alternative Protein Module.

Educational institutions can offer convenient access to menus that provide introductions to various Alternative Protein brands and unbranded products. Given the demographic is generally interested in issues that Alternative Protein consumption can help solve, this experience can accelerate consumer acceptance as part of a longer-term plan. For example, the University of Massachusetts Amherst dining services program offers a menu with independent carbon footprint ratings and wide selection, including of Alternative Protein options. This leading dining services program will be used as a model and base for The Purpose-Driven Plant-Based Incubator™ program to be launched across 12 additional universities, intended to increase the awareness of the alternative offerings, partly through brand recognition, as part of a new partnership with Nestlé Professional and Wholesome Crave. As another example of knowledge dissemination, Givaudan, the world’s leading flavor and fragrance company, engages in collaboration with University of California Berkeley’s Product Development Program which includes the annual release of white papers.

Universities can also be employed to provide greater access to research through the release of Open Access Research, which can advance the industry in addition to work being completed by private companies. This can be particularly beneficial in avoiding repeat work in areas that have been found to be less promising and less able to generate commercial results.

Providing Policy and Regulatory Expertise

There are many examples including the Oxford Martin Program on the Future of Food, an interdisciplinary program of research and policy engagement concerning all aspects of the food system, based at the University of Oxford. Tufts University's Friedman School has hosted conferences and seminars on Alternative Protein and their role in addressing global food challenges which often include discussions on policy and regulatory aspects with examples discussed further in the next section.

The role of educational institutions is vast, and only briefly described here, but essential across innovation transitions.

7. PUBLIC POLICY & REGULATION

Food Sector Development

In understanding the current situation, it is useful to observe that, in many countries, food technology adoption was accelerated as needed during the Second World War. The effort demanded long-lasting and easily transportable rations for soldiers. Widespread innovation led to changes in the way food was produced, stored, and distributed including through refrigeration, freezing, and packaging techniques. As a result, there is more common availability of canned foods, frozen concentrated juices, dehydrated foods, instant coffee, powdered milk, reconstituted eggs, processed cheese and packaged convenience foods like pre-packaged meals, ready-to-eat snacks, and quick-prep mixes. At the time, the scarcity of traditional protein sources led to increased research into soy-based products. Soybeans were used to create meat substitutes, extenders, and other protein-rich products. This laid the groundwork for the later development of soy-based processed foods.

Regulation

New regulatory developments will vary by country and by region with some countries more proactive in developing new policies and fostering advances, including Denmark, Singapore, The United States, and The Netherlands with activity being tracked by GFI and global law firm Dentons. Bringing the cost of Alternative Protein down in-line with traditional animal sources will require a recognition of the subsidy advantages provided to traditional agriculture producers, with updates, to assure the provision of affordable, healthy food and secure supply as intended by policymakers. Policy development is being followed and supported by many organizations including the Center for Strategic & International Studies and the OECD.

Government Policy Support

Historically, government program support and subsidies have been a major driver of innovation for economic development. While the United States is often viewed as a leader in venture capital, with Europe and Asia having seen much more investment over the past 10 years, it is perhaps less appreciated that the activity receives government support in many formats including non-dilutive financing from America’s Seed Fund from the Small Business Administration, working with 11 Federal Agencies including US Department of Agriculture and Department of Energy. Other Federal and many State programs include tax incentives and programs such as BuildBack Better and the Inflation Reduction Act (IRA). Specifically, this type of support was critical to the early success of Silicon Valley and medical technology investment promoted by ‘Orphan Drug’ policies and others.

European countries, and the EU sponsor similar programs such as the European Innovation Council (EIC) and European Institute of Technology (EIT) that provide non-dilutive programs and include the Horizon Europe grant framework and EIT Food. It is assessed that approximately 20% of all European technology venture capital investment over the past five years was from government-funded sources.

Promoting targeted national economic growth objectives is not a new concept, with many other efforts in Singapore, China, Korea, Japan, Malaysia, Taiwan, India and others:

Public policy and regulation are essential for any fast-growing segment and this is particularly the case for Alternative Protein as covered in a United Nations Environment Programme Frontiers Report, stating in detail that appropriate government regulations and backing will be necessary.

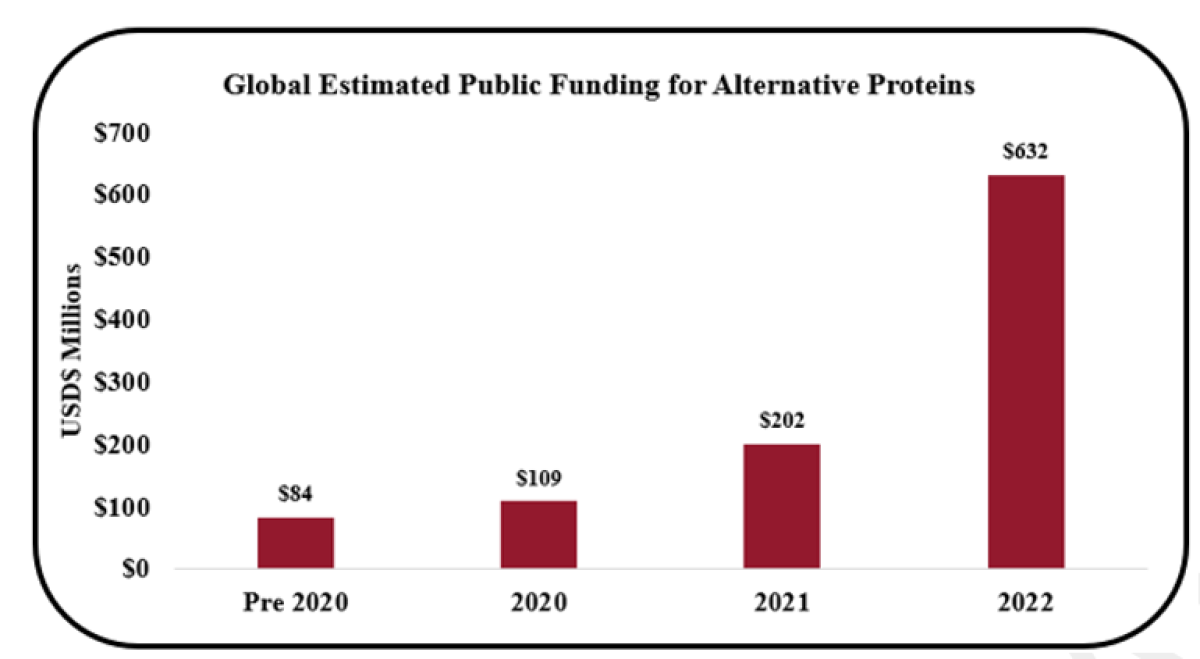

Funding by governments for Alternative Protein has been increasing, including through support for public-private funded projects. GFI reports that governments increased support in 2022 surpassing USD$1 billion led by Europe:

Source: GFI.

Nearly all technological innovation resulting in transformation has required government support and oversight. As is evident over the history of food production resulting in current practices, the involvement of governments through policies, including regulation, many incentives, and subsidies is a critical factor in determining future direction.

Outlook & Conclusion

Constraints Being Addressed

Despite recent rapid growth, there is a need to address issues to enable the creation of production and the supply chain in a sustainable manner, allowing for scale and lower resulting costs. The available products will need to continue to increase and include appealing taste and texture either through analogue offerings or entirely new consumer products. Innovation in the food sector always requires consideration of cultural and culinary preferences. Additional research will need to be conducted to create healthy and nutritious products. As the food industry is heavily regulated, Alternative Protein products must meet various safety and labelling standards which takes time. The industry will need to continue to address environmental and sustainability issues to ensure sourcing and climate impacts are managed properly as with any operational deployment.

Recently, negative attention has been brought to Alternative Protein by characterizing them collectively as “ultra-processed foods” and therefore, by categorization, unhealthy. This may have contributed to very recent slower consumption growth in the United States. Work will continue on updating research to follow product innovation and independent science-based health assessments including the recent study “Consumption of ultra-processed foods and risk of multimorbidity of cancer and cardiometabolic diseases: a multinational cohort study” which explains a consideration in balance with traditional animal sources and by specific product type is necessary to make informed decisions.

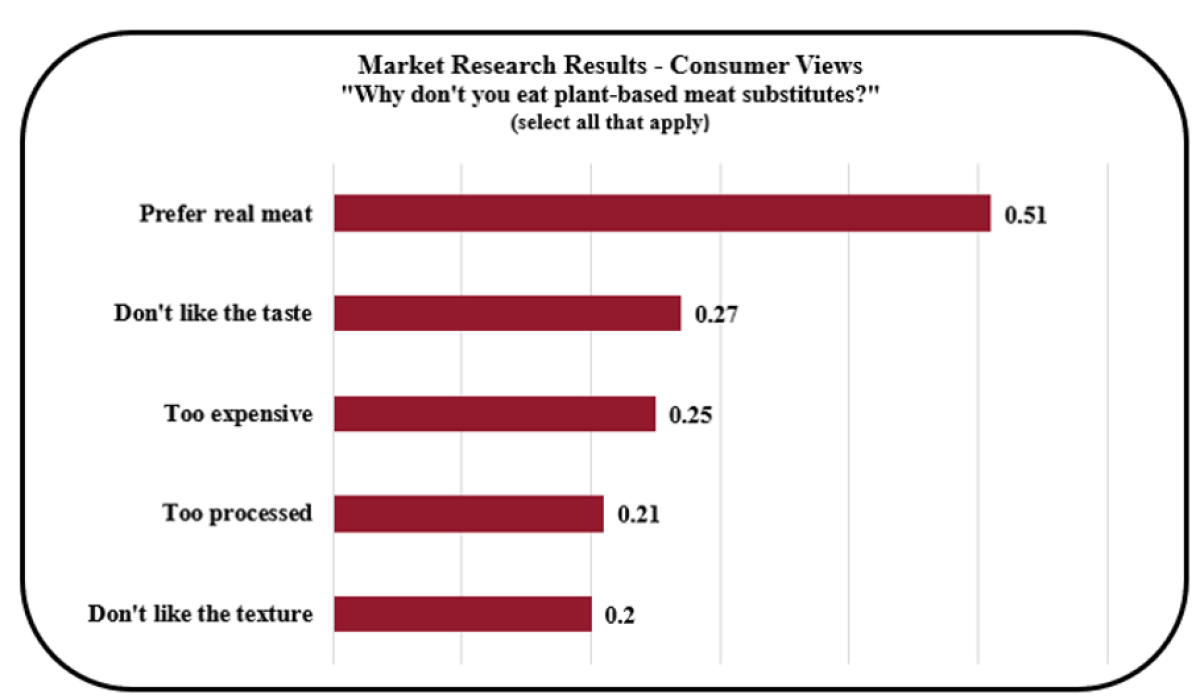

As end-consumer acceptance is essential, there have been many studies conducted to inform updated views on status and the key considerations that will allow for further growth. Consumers’ experience in terms of taste and texture are, not surprisingly, a key factor among all of the constraints mentioned. Consumer perceptions and expectations must be managed and satisfaction delivered regularly considering the key decision drivers of taste and price along with safety, clean labels, and nutritional value with recent research released by GFI explaining the importance of taste and ranking key factors:

Source: GFI Academic Papers, Mintel global market research, consistent with recent survey[i]

One approach towards improving the consumer experience, now receiving increased attention, is the development of new products which provide alternative sources of nutrition without an attempt to directly replicate the taste and texture of meat products. This allows for improved consumer satisfaction as creating close equivalents at this time can be difficult and costly and sensory science research suggests that higher consumer acceptance results for mixed (hybrid) or plant-based products that avoid direct competition with meat. In general, overcoming current constraints to growth creates additional market opportunities for companies and investors addressing concerns and advancing product offerings.

State of the Ecosystem

Continued investment from public and private sources, including incumbent food producers, will be required to provide for innovating products at lower prices, allowed by economies of scale that can only result with higher volumes. Alongside the investment by established food producers, much of the private investment in the sector has been at an earlier venture and growth-stage, which is logical given the development of the vertical.

A change in investor sentiment related to many growth and technology sectors is evident. It has been observed that the Alternative Protein vertical is moving through a well-predicted and typical hype cycle with the potential for adoption in North America to advance from this point with higher consumption in Europe and Asia continuing. Public market sentiment seems influenced by negative news flow in regards to more pure play B2C companies. In recent history, many companies were listed at much higher valuations, especially if given valuation comparisons to technology stocks, and will need to transition to a status as a listed company that needs to deliver on expectations. Many companies are adapting to market conditions by shifting from a ‘growth-at-any-cost’ strategy to a ‘path to delivering profitability’ approach. While these listed companies may draw attention as they are indeed public, it remains the case that - in addition to the activity and stated plans of the larger food manufacturers - over 600 vertical-specific, venture-backed companies are active. As market sentiment calms generally, private investors may find better opportunities to invest at better valuations than over recent years.

Demonstrating the broadening general interest in the opportunity and need for investment created by evolving food systems, a number of listed market Exchange Traded Funds (ETFs) and indices have been established:

The indices employ varied construction methodologies and technologies, in some cases allowing for a broader, if less direct, exposure to long-term, plant-based investment themes. Market sentiment for these ETFs appears to have been recently affected, possibly by falling agricultural commodity prices and calmed market views regarding some innovating companies overall, possibly allowing for a relatively opportunistic entry. Enabling this effort further, as the number of listed companies focused on the vertical is limited, coverage may be enhanced to expose more opportunities through investor calls for greater disclosure.

Additional impact-focused investor interest may result as recently, for the first time, the food sector is identified as of key importance in statements released during the recent United Nations Climate Change Conference where “134 countries, covering 70% of the world’s land, have signed the Emirates Declaration on Sustainable Agriculture, Resilient Food Systems, and Climate Action, committing to integrate food into their climate plans by 2025”.

Wider Opportunity Set & Growth Trajectory

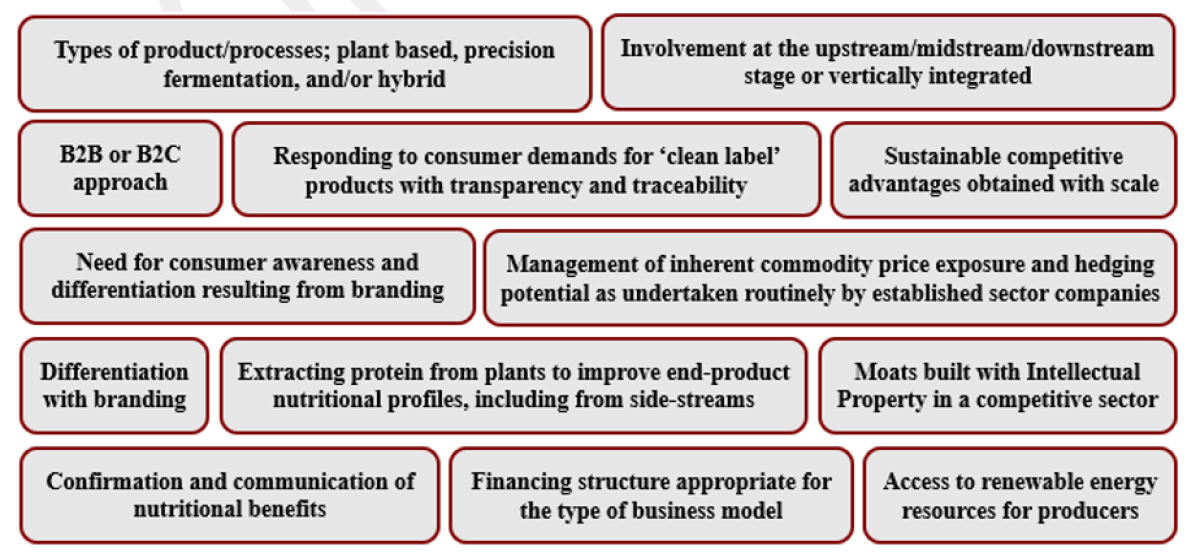

Especially in this environment, private investors need to be aware of the entire ecosystem and competitive environment that is emerging rapidly from a small base of activity. Factors considered when deploying a strategy cover a broad range and may likely be influenced differently against this backdrop:

Various types of investors will have differing abilities to execute components of the above strategy types. Additionally, as discussed above, financial solutions suitable for activities by type and stage must also be considered to meet requirements specific to the sector.

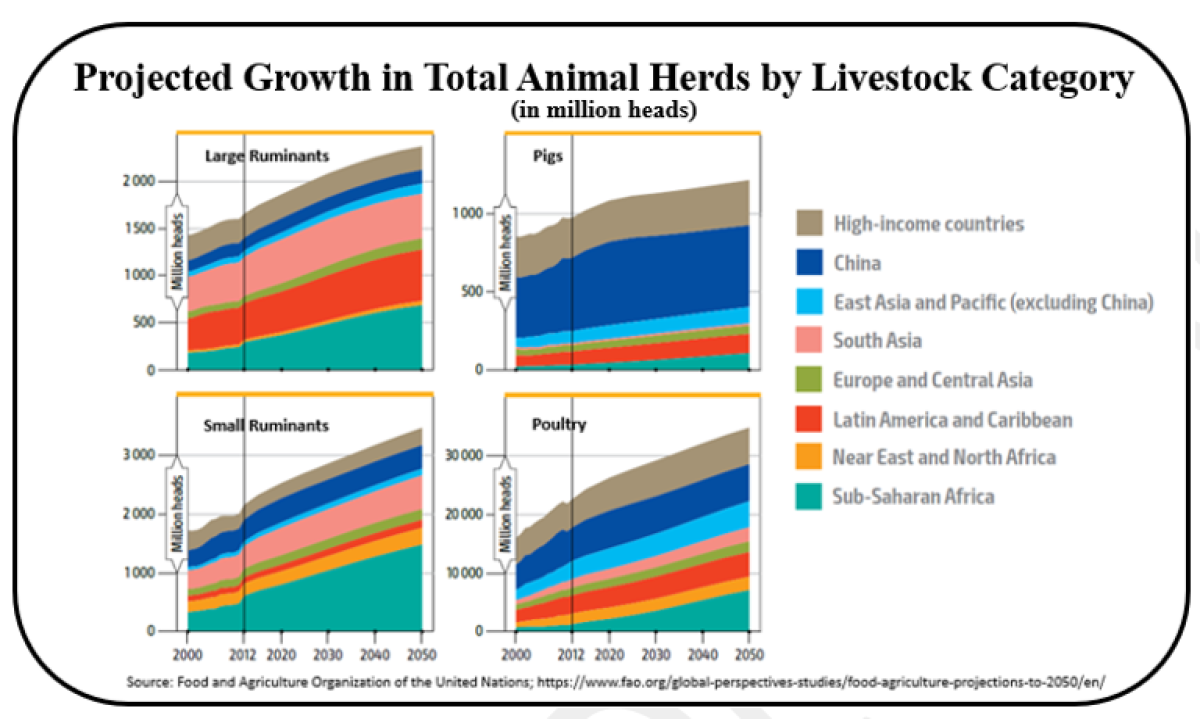

Protein consumption, of all types including from traditional sources, is expected to continue to rise as a result of factors including global population growth and emerging consumers preferring, and increasingly able to afford, benefits of higher protein diets. Without innovation, additional animal-based production along with potential climate impact will be required to meet projected demand:

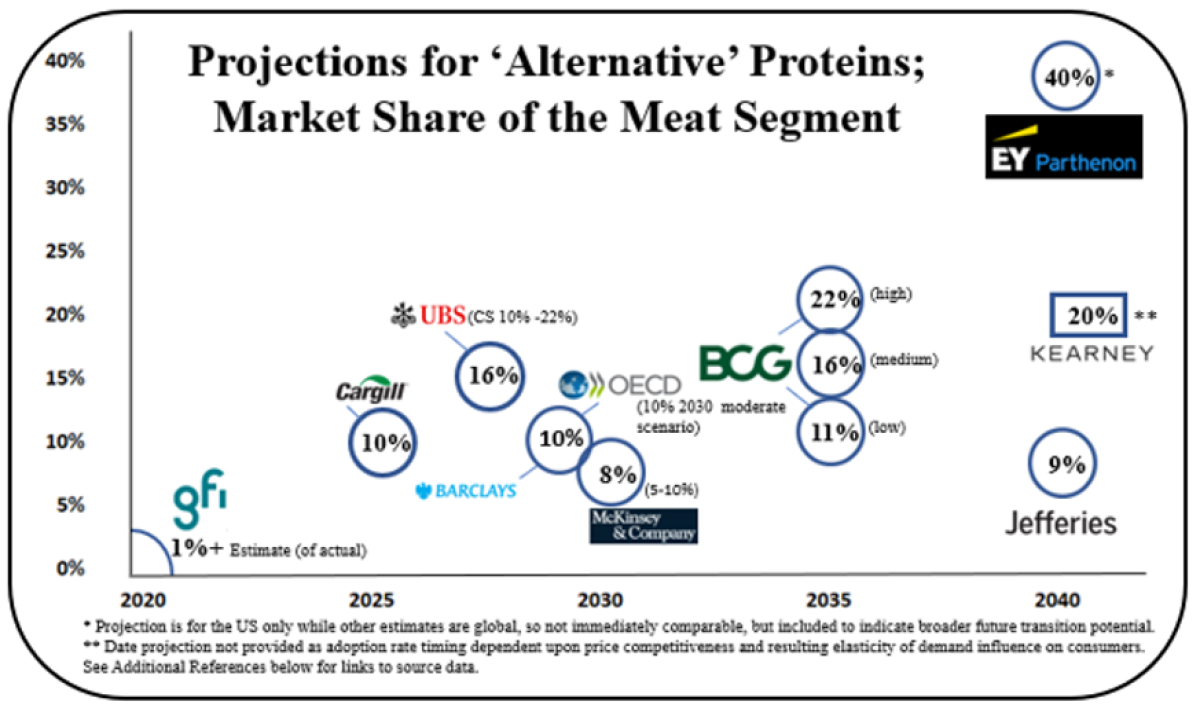

Within this expansion, global growth in the consumption of Alternative Protein appears set to persist, even without substitution, albeit with the potential for variation by regions and countries, as current general forecasts anticipate further adoption, with the primary question being, on what timescale? This results partly from questions about the pace of ongoing policy developments, continued public and private investment, and efforts to advance activity:

Against a backdrop of growing demand and known constraints, now actively being addressed, the Alternative Protein vertical’s development is differentiated partly as 1) nutritious food represents an essential non-discretionary consumer product, 2) food system practices and infrastructure are long established and have often been subsidized as controlling food price inflation is normally a policy priority, 3) awareness of traditional animal protein production GHG footprint is now gaining more attention, and 4) in many regions and countries large portions of the food sector are consolidated. Some of these conditions can inhibit change - but can also allow for rapid adoption as larger players engage and policy shifts encourage activity across the expanding ecosystem.

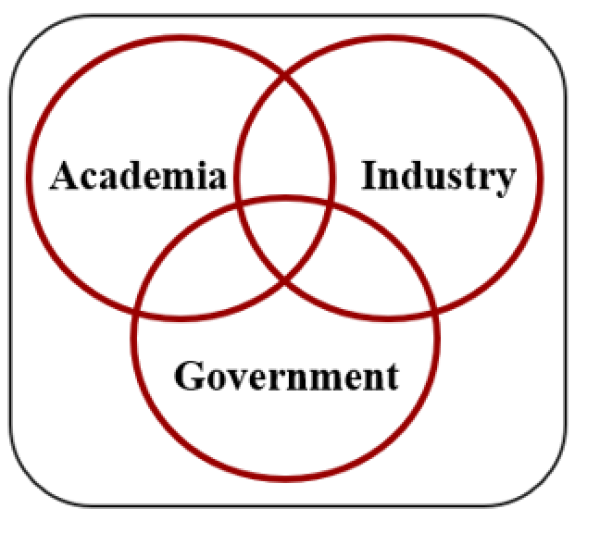

Fostering government, industry and academic links can be expected to be economically beneficial, promoting transformative innovation, as observed across many other verticals and countries. Extensive research has been conducted regarding benefits of this interaction, often described as the “Triple Helix Model of Innovation”.

As an established sector, the broadening interest and recent innovation efforts in the food supply chain are remarkable. The continued activity of participants motivating awareness and build-out of the ecosystem are key to providing nutrition for an increasing global population in a sustainable manner. Drivers, including public policy initiatives, which have been demonstrated as critical in other strategically valuable industries, are now converging to encourage progress on the trajectory forecast. As a result, rapid advances in the delivery and consumption of essential, nutritional foods in a sustainable manner remain well underway, with ample investment opportunity furthering greater adoption of Alternative Protein sources.

Footnotes:

[i] Findings consistent with observations from a November 2023, voluntary on-line survey of students enrolled in the University of Massachusetts Amherst Dining Services program conducted for this article. Survey results included approximately 2,000 respondents, which alone is potentially an interesting indicator of general interest among this demographic. Survey population is unusual as regularly accessing alternative protein offerings, with menu carbon ratings, potentially increasing awareness. Approximately 90% of respondents reported being very familiar, or somewhat familiar, with Alternative Protein products*, significantly higher than other recent general population surveys. Palatability remains most important to respondents, including those familiar with Alternative Protein products and the largest influence for others that would consider adding them to their diet, along with Health Benefits, followed by Price, Environmental Impact, additional Dietary Variety, Ethical Considerations/Animal Welfare, and Cultural or Religious Practice.

About the Authors/Contributors:

Alissa A. Nolden, University of Massachusetts Amherst; James Payling, PitchBook; Ed Rushton, Optiver; Viren Shrivastava, Meticulous Research; London Cross; Sam Haddad; Eva Katsoulakis; Alexander Kirley; Patrick Songo; Davide Rotunno; Ogechi Okereke; Jacob von Linden; Pierre de la Croix-Vaubois; Sarah Streim, and Conor Temple.

David Donahue, CFA, joined Mbuyu Capital Limited in 2015 as a partner. Mbuyu Capital brings the unique investment opportunities offered by African private markets to investors.

Mbuyu is leveraging experience in agribusiness investment towards net zero protein production. Before joining Mbuyu, David was Head of Private Equity and Real Estate at Ignis Advisors, responsible for a $1 billion portfolio. Previously, he was responsible for a $2 billion global equity sector portfolio at the Dutch pension fund APG as well as $2.5 billion US equity portfolio manager at a Dutch insurer. David holds a bachelor’s degree in Economics from Boston College, Massachusetts and an MBA, Finance from the Isenberg School of Management at the University of Massachusetts Amherst.