By Marc Dummer, CAIA, CIMA® - Managing Director & Client Portfolio Manager; May Tong, CFA, Managing Director and Portfolio Manager, Asset Allocation; Jessica Bush, CFA, Portfolio Manager, and Ben Rotenberg, CFA, CAIA, Portfolio Manager at Principal Asset Management.

Key takeaways:

-

The markets have been so fixated on forecasting a recession and ensuing rate cuts that they have ignored an abundance of data pointing to the early stages of a manufacturing-led expansion.

-

It appears the market may have been mispriced amid the Federal Reserve (Fed) emphasizing price stability, a resilient U.S. economy, and rates staying higher for longer.

-

Regardless of inflation’s path in 2023, we anticipate a mean reversion of returns between real assets and nominal equities, whereby the former outperforms, and the latter gives up its gains.

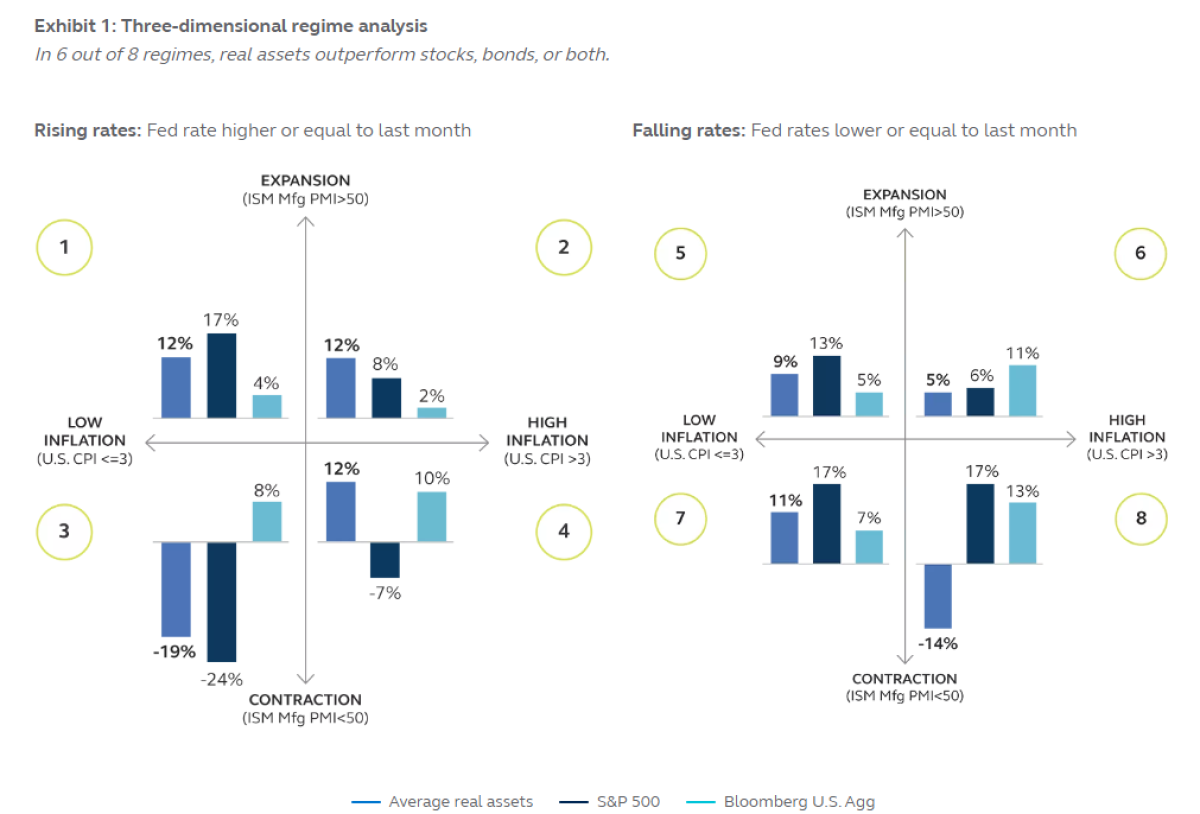

Real assets vs. nominal assets: Assessed through a three-dimensional lens

Economic growth, inflation, and interest rates are key factors in assessing the performance of real vs. nominal assets. Isolating merely one of the three variables fails to acknowledge their interplay in influencing investment returns between asset classes. As a guide for forward-looking returns, we defined eight regimes (numbered on exhibit 1) across the three variables (growth, inflation, and rates) and assessed their historical returns.

Variables

- Economic growth is measured by the ISM Manufacturing Index, also known as the Purchasing Managers’ Index (PMI).

- Expansion = PMI > 50

- Contraction = PMI <= 50

- Inflation is measured by the core U.S. Consumer Price Index (CPI).

- High inflation = CPI > 3%

- Low inflation = CPI < =3%

- Rates are measured by the Federal Funds Rate (FFR).

- Rising rates = FFR >= previous month

- Falling rates = FFR <= previous month

Source: As of December 31, 2022. Data since 1971. Source: Principal Global Investors. ISM Mfg PMI: Institute for Supply Management Manufacturing Purchasing Managers’ Index; an index of the prevailing direction of economic trends in manufacturing sectors consisting of a diffusion index that summarizes with a number from 0 to 100, whether market conditions, as viewed by purchasing managers, are expanding (>50), staying the same (=50), or contracting (<50). CPI: Consumer price index. Average real assets: An equal-weighted version of the S&P Global Infrastructure Index NTR (11/30/2001-12/31/2022), FTSE EPRA/NAREIT Developed Index NTR (12/31/1971-12/31/2022), Bloomberg U.S. Treasury TIPS Index (3/31/1997-12/31/2022), 15% Bloomberg Commodity Index (01/31/1971–12/31/2022), and S&P Global Natural Resources Index NTR (11/30/2002–12/31/2022). S&P 500 Index: market capitalization weighted index of 500 widely held stocks often used as a proxy for the stock market (stocks). Bloomberg U.S. Aggregate Bond Index: an unmanaged index of domestic, taxable, fixed-income securities (bonds).

Where are we now?

In 2022, markets appeared rational, having priced in the appropriate regime (rising rates, contraction, high inflation—regime four), with real assets outperforming nominal assets over the year. For much of 2023, however, markets have been pricing in a late stagflation regime (falling rates, contraction, high inflation—regime eight). In this regime, nominal assets have outpaced real assets on expectations that the Fed would cut rates, thereby leading to an outperformance of growth stocks, particularly among a narrow band of large-cap technology stocks. Amid the Fed consistently emphasizing price stability, a resilient U.S. economy, and rates staying higher for longer, has the market mispriced the likely market outlook? It is looking likely.

Where are we headed?

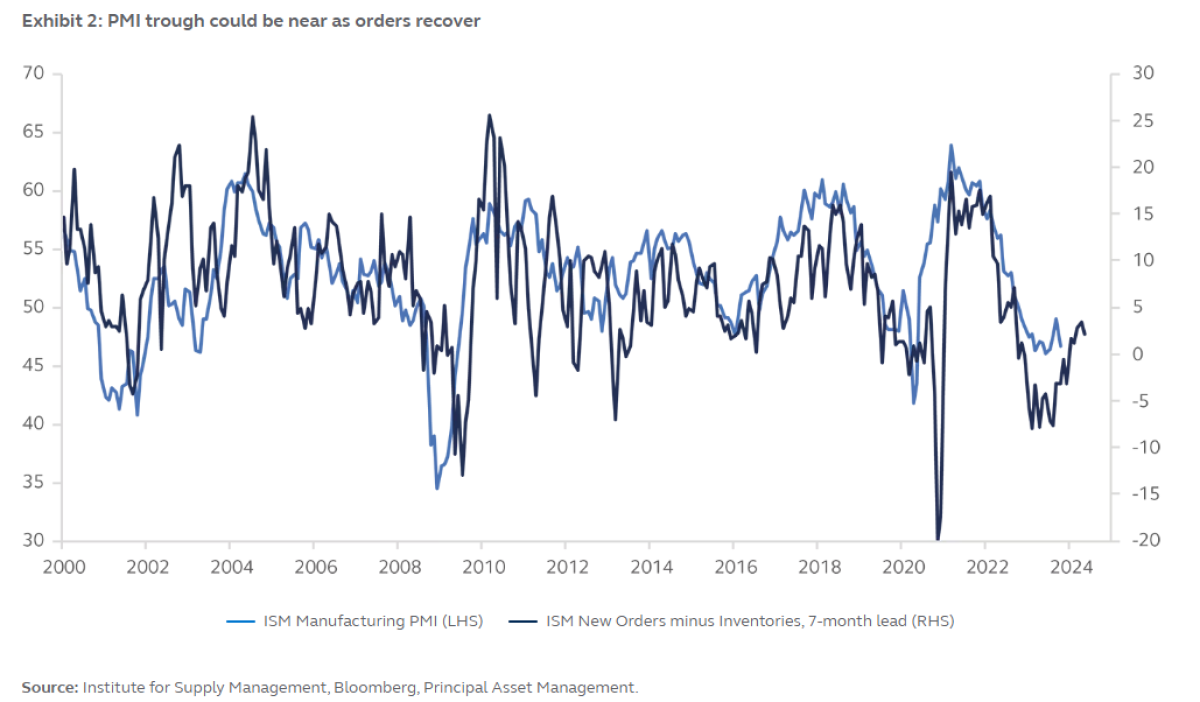

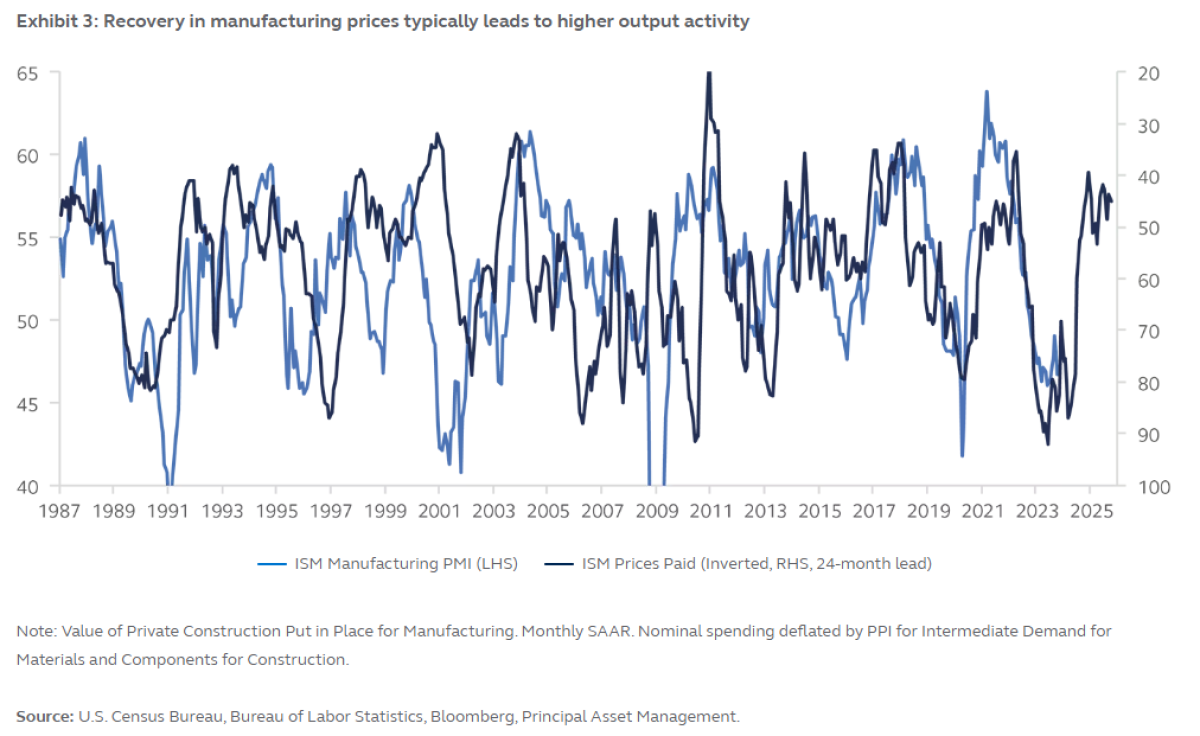

The markets have been so fixated on forecasting a recession and ensuing rate cuts that they have ignored the abundance of data pointing to the early stages of a manufacturing-led expansion. Inventory levels and manufacturing prices are two leading indicators that support this thesis (see exhibits 2 and 3).

After a buildup during COVID-19, inventory levels have been drawn down and may need replenishment. The ISM Manufacturing PMI has been hovering just below expansion territory, defined as a reading at or above 49, and could be close to a trough. This belief is supported by a notable surge in the ISM Prices Paid Index, which could lead the ISM Manufacturing PMI to above 50 in the near term.

This manufacturing activity suggests we are in the early stages of a potentially enduring manufacturing renaissance in the U.S. that will be driven by ongoing deglobalization trends (onshoring, near-shoring) and economic incentives such as the CHIPS and Science Act and the Infrastructure Investment and Jobs Act. These incentives have catalyzed investments into U.S. manufacturing, with robust spending growing at a year-over-year pace not seen in the last two decades. Since CHIPS was signed, companies have announced more than $166B in plans for new U.S. manufacturing facilities for semiconductors and electronics.1 Along with the deglobalization tailwinds supporting manufacturing and decarbonization initiatives—such as those supported by the Inflation Reduction Act—have provided incentives for U.S. manufacturers to invest and build new clean energy facilities to produce solar panels, wind turbines, battery storage technologies, and other green energy projects. Exhibit 4 highlights the significant boost in manufacturing construction spending that the policies have triggered.

Investment takeaway

As the manufacturing renaissance takes hold, we believe we may be entering the early stages of a higher growth and elevated rates backdrop. Whether inflation reverts to the Fed’s target of 2% or remains structurally higher, we anticipate a mean reversion of returns between real assets and nominal equities, whereby the former outperforms, and the latter gives up its gains.

Footnotes:

1 FACT SHEET: One Year after the CHIPS and Science Act, Biden-Harris Administration Marks Historic Progress in Bringing Semiconductor Supply Chains Home, Supporting Innovation, and Protecting National Security, 2023.

More from the Principal Group: 2024 Hubrus Unlikely to Gain Wins

About the Authors:

May Tong is a Managing Director and Portfolio Manager for Principal Asset Allocation. She is responsible for managing the Dynamic Outcomes suites of strategies which provides outcome-oriented solutions to global clients.

Prior to joining Principal in 2021, May was SVP and Senior Portfolio Manager with Franklin Templeton’s Investment Solutions group developing and managing multi-asset strategies and solutions including target-date, target risk, 529 plans, retirement income and model portfolios. Previously, she was also a Portfolio Manager and Head of Portfolio Implementation & Management with Voya’s Multi-Asset Solutions group. May started off her career with Merrill Lynch Investment Management and subsequently joined ING Investment Management (now Voya IM) whereby she managed quantitative equity and index equity portfolios.

May has an MBA from Columbia University, a bachelor’s degree in finance and accounting from Boston College, and has earned the right to use the Chartered Financial Analyst designation. She currently sits on the board of Literacy Trust which focuses early childhood literacy intervention.

Ben Rotenberg is a Portfolio Manager for Principal Asset Allocation. He is responsible for co-managing our dynamic outcome suite of strategies. This includes all portfolio construction, asset allocation and manager optimization decisions relating to this suite of strategies. He joined Principal in 2014 and has been in the investment industry since 1993. Previously, he was a Managing Director with Cliffwater LLC, and was responsible for investment manager due diligence and assisting clients with asset allocation, manager selection, and portfolio construction. Ben was also a member of Cliffwater’s Investment Oversight and Risk Committee Prior to joining Cliffwater, Ben was Director of Research with National Fiduciary Advisors, an investment consulting firm based in Los Angeles, where he was responsible for conducting investment manager due diligence across multiple asset classes. Ben began his investment career at Wilshire Associates providing services to investment consultants in Wilshire’s Cooperative Universe Service division. He received a Bachelor of Arts from Pomona College. Ben has earned the right to use the Chartered Financial Analyst and Chartered Alternative Investment Analyst designations and is a member of the CFA Society of North Carolina.

Jessica Bush is a Portfolio Manager for Principal Asset Allocation. She is responsible for co-managing our dynamic outcome suite of strategies. This includes all portfolio construction, asset allocation and manager optimization decisions relating to this suite of strategies. Jessica joined Principal in 2006 and has been in the investment industry since 2002. Previously, she served as a Senior Research Analyst on the Manager Research team responsible for the evaluation and monitoring of the sub-advisors under the due diligence program used by Principal Funds. Prior to joining Principal, she was a Senior Portfolio Analyst on the fixed-income team at Putnam Investments. Jessica earned a bachelor’s degree in business administration from the University of Michigan. She has earned the right to use the Chartered Financial Analyst designation.

Marc Drummer is a Managing Director and Client Portfolio Manager for Principal Asset Allocation. He is responsible for managing the client solutions team and representing Principal Asset Allocation’s strategies to their largest and most sophisticated institutional and retail clients, including multi-asset strategies that span the equity, real estate, fixed income, and commodity asset classes. Previously, Marc was responsible for co-managing our dynamic outcome suite of strategies. He joined Principal in 2003 and has been in the investment industry since 1996. Prior to joining Principal, he co-managed fixed-income general account assets for a group of privately held insurance companies. Marc received an M.B.A. and a bachelor’s degree in finance from the University of Utah. Marc has earned the right to use the Certified Investment Management Analyst and Chartered Alternative Investment Analyst designations.