By Ryan McGlothlin, Managing Director at River & Mercantile Group, PLC.

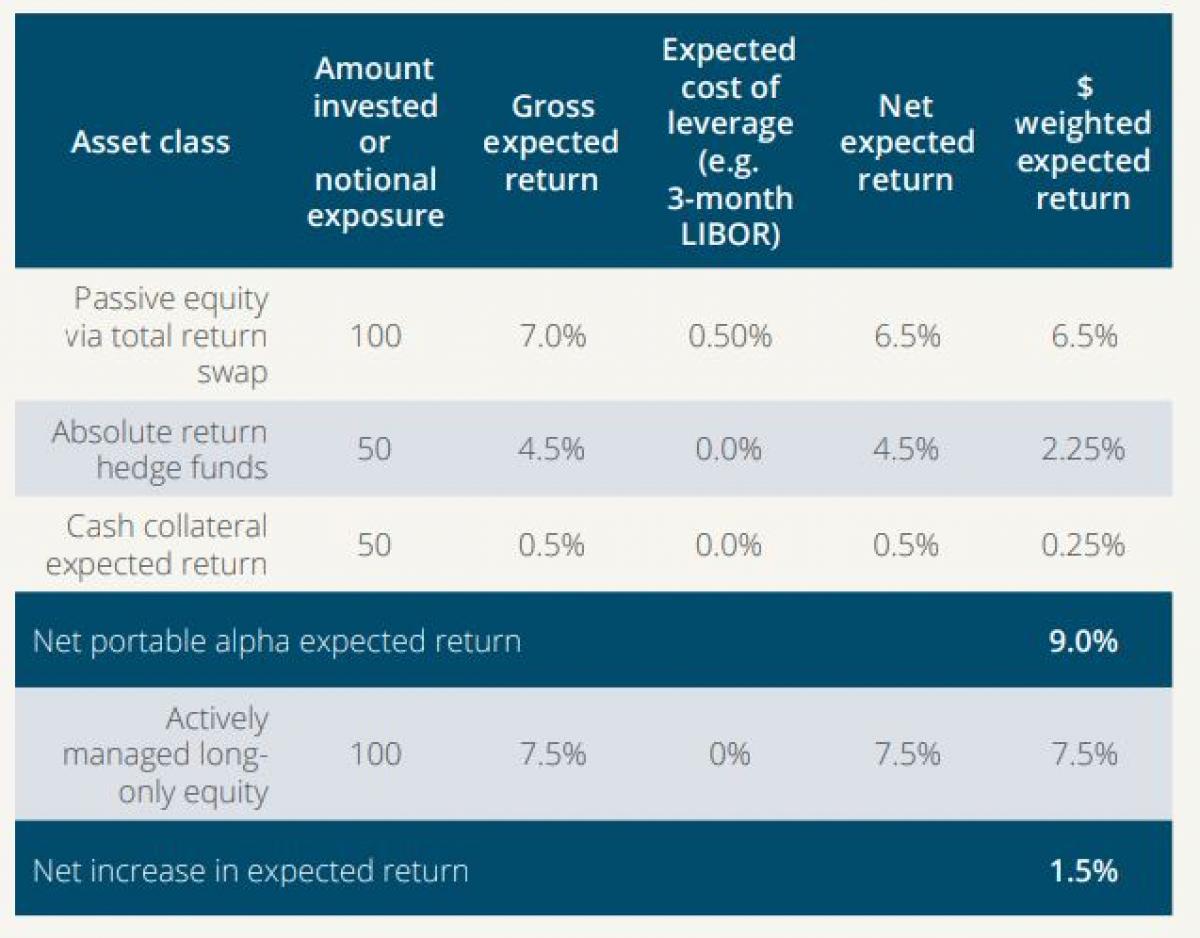

Portable alpha overview Portable alpha is often used as a replacement for traditional long-only active equity using the following typical assumptions:

In theory, holding hedge funds plus equity index total return swaps provides an expected return of 11.0% (Equity total return swap expected return + hedge fund expected return), versus 7.5% for traditional active equity. However, an investor must have collateral (cash or government bonds) to post against the equity total return swaps in case equity markets fall. Most portable alpha investors therefore maintain a collateral buffer of 30-50% for their program. This means that they could absorb an equity market drawdown of 30-50% before needing to obtain collateral from another portion of their portfolio or from selling assets. Assuming an investor has a $100m allocation to portable alpha, the improvement versus a traditional equity portfolio is calculated below:

So, even holding a relatively conservative collateral buffer of 50% improves expected returns by 1.5% versus traditional equity. This is obviously still very attractive. However, portable alpha involves the use of leverage and the addition of leverage introduces new risks that investors must mitigate and manage. A key risk is correlation between hedge fund and equity market returns as having both drop at the same time will exacerbate portfolio losses. However, it is liquidity risk that is the most important as being forced to sell assets to raise collateral against a swap position is an easy way to ruin long term returns. Having a 50% liquidity/collateral buffer is good, but investors should also have a liquidity management plan that informs what their response will be if equities fall significantly. For example, if equities fall by 35%, there will only be sufficient collateral remaining to absorb another ~23% fall from there. If a risk management policy is written such that a minimum amount of collateral buffer must be maintained, such as having enough to absorb an immediate 25% equity market fall, then a forced liquidation of assets to raise collateral could occur even though there is still headroom available from the original collateral buffer.

A Better Way

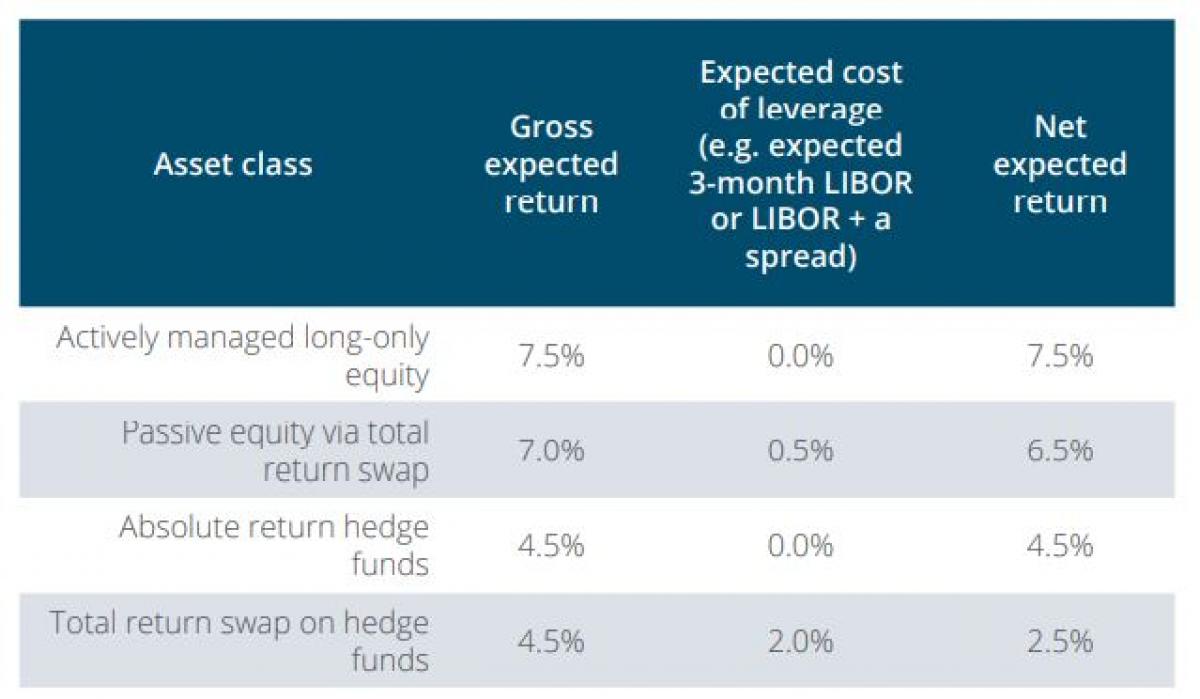

The return enhancement potential of portable alpha is compelling, especially in a world of reduced expected returns. But this potential comes with unfamiliar risks, such as stress scenario liquidity management, that many investors may not be comfortable with. The return potential of portable alpha can be maintained while better managing the key liquidity risk. There are two ways this can be accomplished: 1. Using the hedge fund portfolio itself as collateral for the equity total return swaps; or 2. Obtaining both equity and hedge fund exposure via swaps Either of these methods can dramatically reduce liquidity risk while increasing expected returns versus a more traditional portable alpha program by 1.0% p.a. or more. The availability of financing against hedge funds, whether a revolving credit facility or a swap, has increased significantly due to relaxation in the bank regulatory environment. To make a comparison we use the following assumptions.

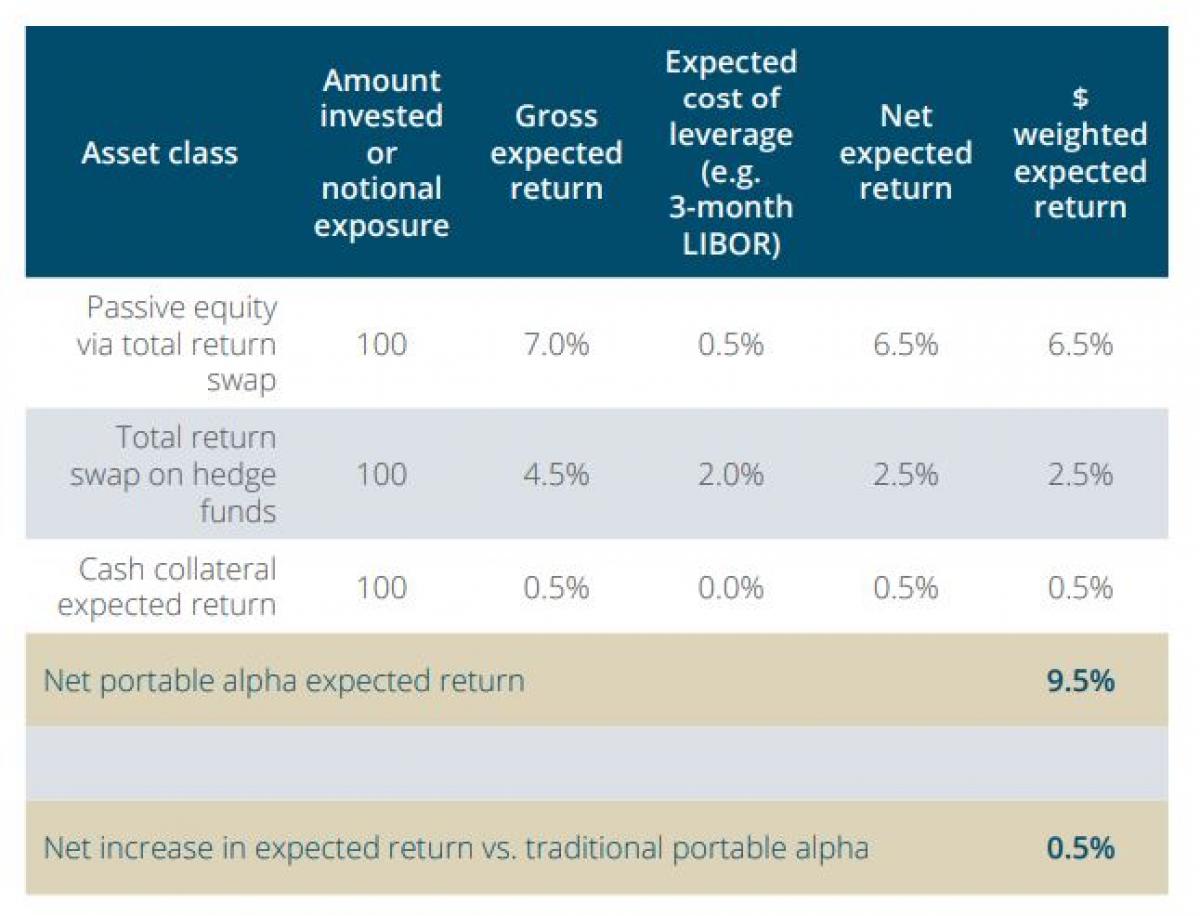

Using these assumptions, we can take the same $100m portable alpha portfolio and restructure it using total return swaps on hedge funds. The following example is perhaps the most conservative approach to improving returns. This approach increases the gross exposure to hedge funds from $50m to $100m, so investment risk is increased. However, if the selection of the hedge funds has been done well and their return correlation to equities is very low, then this may be a risk well worth taking. In addition, liquidity risk has been dramatically reduced, again assuming that the hedge fund portfolio does not have material, highly correlated, downside risk alongside equities. The new portfolio can now withstand an almost unlimited equity market drawdown with no need to worry about where collateral will come from as the equity swaps are backed 1:1 with cash. The strategy will fail if the combined losses of equities and hedge funds are $100m, but this an exceptionally extreme outcome, and a traditional portable alpha investment is likely to have failed as well.

Returns can be enhanced by more than the 0.5% shown above if alternative hedge fund financing strategies are able to be used. Such strategies include the utilization of the hedge fund investments as collateral for the swaps and the use of non-recourse revolving credit facilities written against the value of the hedge funds. Different investors will have different accounting, legal and regulatory constraints that make each of these potential solutions more or less attractive or viable. But each of these can materially reduce the cost of implementing portable alpha, with that reduced cost showing up as a material increase in expected returns - in some cases another 0.5% - 1.0% p.a. In addition, good derivatives and collateral management can add additional returns. For example, a strong derivatives manager can add value by varying the maturity tenor and instrument used to obtain passive equity exposure. A manager can also manage government bonds, as opposed to just cash, to generate better yields from the collateral pool. But the potential improvements from these areas are dwarfed by the potential improvement from changing the way that the portable alpha program is structured.

Conclusion

We believe that institutional investors should strongly consider portable alpha as a tool to enhance risk adjusted returns. But there are different ways to implement a portable alpha program and the differences in risk and expected returns between these can be significant. Investors would be well-served to work with a derivatives manager that has developed innovative ways to significantly enhance portable alpha program returns while dramatically reducing liquidity risk.

About the Author

Ryan McGlothlin is a Managing Director in River and Mercantile’s Boston office. He is the portfolio manager for the firm’s Active Structured Equity strategies and is on the Macro investment team. He works with all types of institutional investors on customized investment and risk management strategies. Ryan joined River and Mercantile in 2007 to found its US business. Prior to that, he worked for Barclays Capital in London, helping to implement some of the first interest rate, inflation and equity risk management solutions using derivatives for UK pension schemes. He began his career as a natural resources industry investment banker in Houston and London. He holds an M.B.A. from the University of Chicago Booth School of Business and a B.A. (Honors) from the University of Texas at Austin.