By Christie Townsend, Director, Content and Research, CAIA Association.

My brilliant friend and colleague Steve recently wrote a blog post that made the case for private market investors holding onto assets for longer. Steve made an impactful case—particularly relevant to professionals who manage perpetual pools of capital—to consider a more thoughtful and nuanced approach to the idea of demanding liquidity events for the sake of liquidity itself. I agree with Steve in principle but think it important to play devil’s advocate to his devil’s advocate and outline some of the pitfalls of accepting a longer holding period than expected.

First, our significant points of agreement:

1. Demanding unnecessary liquidity from healthy companies with a strong GP and management team is often counterproductive.

Not to mention, forcing liquidity at inopportune times can be economically devasting, as those of us who navigated COVID, the GFC, and other crises understand.

2. Deference to the status quo when it comes to fund life, terms, structure, and liquidity expectations in a dynamic market is untenable.

3. GPs are in a better position to make informed judgements regarding buy/sell decisions.

After all, their expertise, experience, and developed trust are all reasons you committed capital in the first place.

4. The best investors are forward thinking when evaluating actual portfolio needs, as well as navigating both the current environment and opportunities.

Sound investment decision making should not be based solely on backward-looking risk/return data.

It’s clear the argument for increasing private equity holding periods until exit markets rebound contains a lot of wisdom to appreciate. However, there are also counterpoints that are important to keep in mind.

First off, while private equity portfolio company exits are the primary avenue to liquidity and thus fund distributions, exit markets provide a rich set of indicators to assess: the health of the economy, the appetite for corporate acquisitions, and even the efficacy of GP and management teams, among other data points.

Rising rates and other economic factors have weighed more heavily on exit markets recently, and I get the sense that many private equity investors may be over-indexed to the narrative that a rebound and more supportive exit pricing environment is right around the corner. This may be true, but that story sounds vaguely reminiscent of similar thinking that occurs in public market meme culture: bagholding.

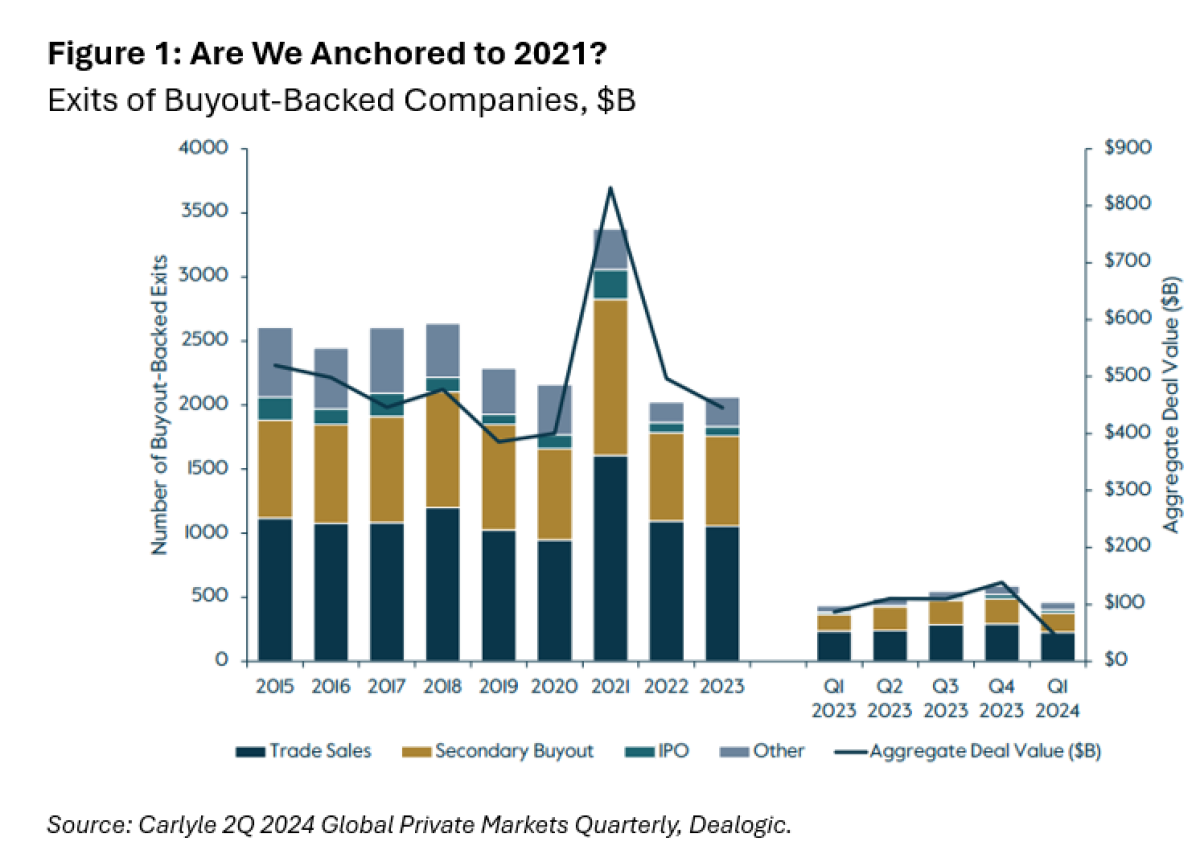

The 10%-20% pullback in exits is certainly meaningful; however, given trade sales and other channels have remained somewhat resilient, it’s important for investors to assess if current market dynamics support a longer holding period. Are the assets truly well-managed or are we anchored to a monetary regime and set of outcomes (figure 1) that may or may not ever rematerialize given Fed expectations and other unique factors (e.g., the drop off in non-traditional, late-round investors in VC, etc.)

Additionally, I would also consider the impact of holding these assets for longer…how will that filter through the broader PE landscape and impact other areas like fundraising, &etc.

Second, particularly when evaluating continuation funds, it’s important to consider the management strategies employed to date and the intermediate- to long-term effect of those decisions, a practice that requires evaluating fund assets at the company level. Some ways to tell if an LP’s expected outcome matches the reality of the situation:

- Is the asset truly being managed for growth or just to pad valuation metrics?

- Are there aggressive cost cutting measures or cash runway issues that could cripple future growth prospects?

- Does the holding period align with the expected management strategy?

- Is the problem truly the exit environment or is it holding out hope for the greater fool?

For my last, and possibly most obvious point, I once again invoke the investing genius of the Wu-Tang Clan: cash rules everything around me. Do you need liquidity now? Maybe or maybe not, but as investors we are constrained by our biases and what often amounts to a lack of creativity in terms of managing risk. Remember years ago, when reaching for yield during the low-rate environment was a thing? Don’t you wish you had a dollar for every time you heard the troupe “I’m more worried about deflation vs. inflation” during that time?

Beyond that cash distributions offer flexibility and help facilitate dynamic portfolio management. Distributions equal optionality, and surprisingly, cash even has yield right now. While it may make sense to hold out for longer, there is also nothing wrong with tapping out of a fund at the end of the legally agreed-upon time period stated in the documents your organization signed 12-20 years ago. This is true even if you have high conviction in the opportunity; if nothing else, that cash may be better used to invest in opportunities that better align with your portfolio needs over the next 20 years.

Additional Guidance/Takeaways

- When evaluating continuation and other funds, flex your rusty excel skills and model out the cash flows, fees, and other expectations in different multiple and rate regimes.

- If you expect the trend in fund length to continue, consider evergreen funds where the terms, fund structure, and alignment is often better suited to managing a pool of private capital.

- The risk-free rate still rules everything around you. Whether you decide to hold the assets longer or take the cash, do so with your eyes open, forward looking! 😉

About the Author:

Ms. Townsend oversees the organization’s thought leadership and external research efforts. Christie brings over 16 years of experience as a practitioner, having built bespoke investment programs on behalf of a variety of institutional investors. She is an outspoken advocate for accessible investment education, fiduciary responsibility, governance, long-termism, diversity, stakeholder management, and transparency.