By Phil Huber, CFA, CFP, Managing Director and Head of Portfolio Solutions at Cliffwater.

As the private equity industry has matured, two distinct yet related trends have emerged: the rise of the secondary market and the emergence of innovative evergreen structures designed for individual investors.

A symbiotic relationship exists between these trends, with secondaries uniquely suited for asset managers seeking to launch, deploy, and scale perpetual private capital funds.

In this paper, we explore the evolution of the secondary markets, the portfolio benefits of secondaries, the appeal of specialist secondary managers, and the necessary (but insufficient) role secondaries play in evergreen strategies.

The private equity (PE) secondary market has evolved significantly since its inception, tracing its roots back to the early 1980s when pioneering firms like the Venture Capital Fund of America (today VCFA Group)1 began facilitating the trading of limited partnership interests. Initially, secondary transactions were primarily driven by distressed sellers looking to exit their investments prematurely. However, the secondary market has matured over the last several decades into a robust and dynamic ecosystem fueled by growing investor demand for liquidity, portfolio optimization, and strategic capital deployment.

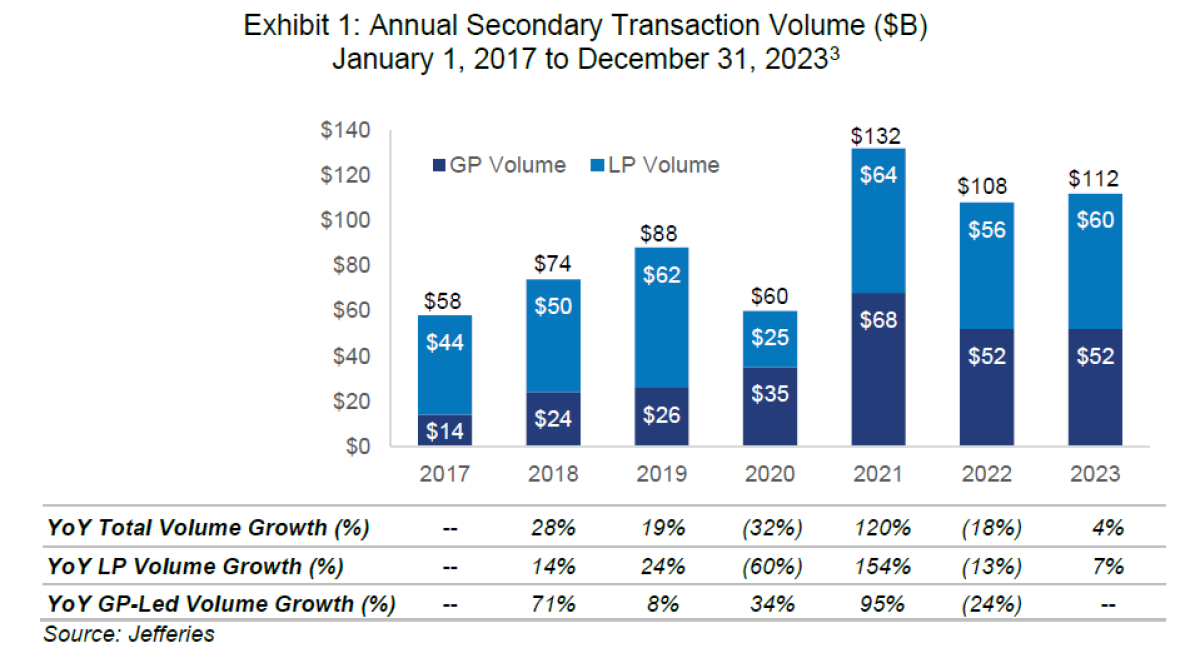

Global transaction volumes by secondary funds clocked in at $112 billion in 2023, more than triple the volume of $37 billion in 20162, underscoring the increased importance of secondary transactions in the private equity landscape. Much has changed since the secondary market’s infancy, having now witnessed the emergence of dedicated secondary funds, the expansion of the buyer universe to include both institutional investors and high-net-worth individual investors, and the development of sophisticated pricing models and due diligence processes. Secondary-focused managers have become increasingly specialized, like private equity itself, with funds specific to investment strategy, security, geography, and company stage.

The nearly equal mix of LP-led ($60B) and GP-led ($52B) deals in 2023 demonstrates the breadth of factors supporting the substantial growth of the secondary market. With more capital being called than distributed in the current economic environment, LPs are increasingly tapping the secondary market to generate liquidity, fund their commitments, and rebalance their portfolios. GPs, on the other hand, are increasingly transferring assets from older funds to new entities, often with the aim of securing additional time and capital to support their portfolio companies’ growth or to manage a structured exit. This approach can apply to single or multiple assets and is a strategic move to prolong the GPs value-add period, particularly during a climate of muted M&A and IPO activity.

Secondary Benefits

Now that we know the dual benefits that secondaries can offer LPs and GPs alike, let’s turn our attention to the question that really matters: what’s in it for investors? The investment merits of secondaries can be summarized as follows:

▪ Immediate Diversification: The expedited capital deployment of traditional, LP-focused secondary funds allows investors to diversify broadly by vintage years, geographies, industries, and asset classes in a timely manner.

▪ Shorter Duration: Investors in secondary funds may benefit from shorter investment holding periods and more consistent cash yields than primary investments as they acquire existing stakes with underlying assets closer to maturity.

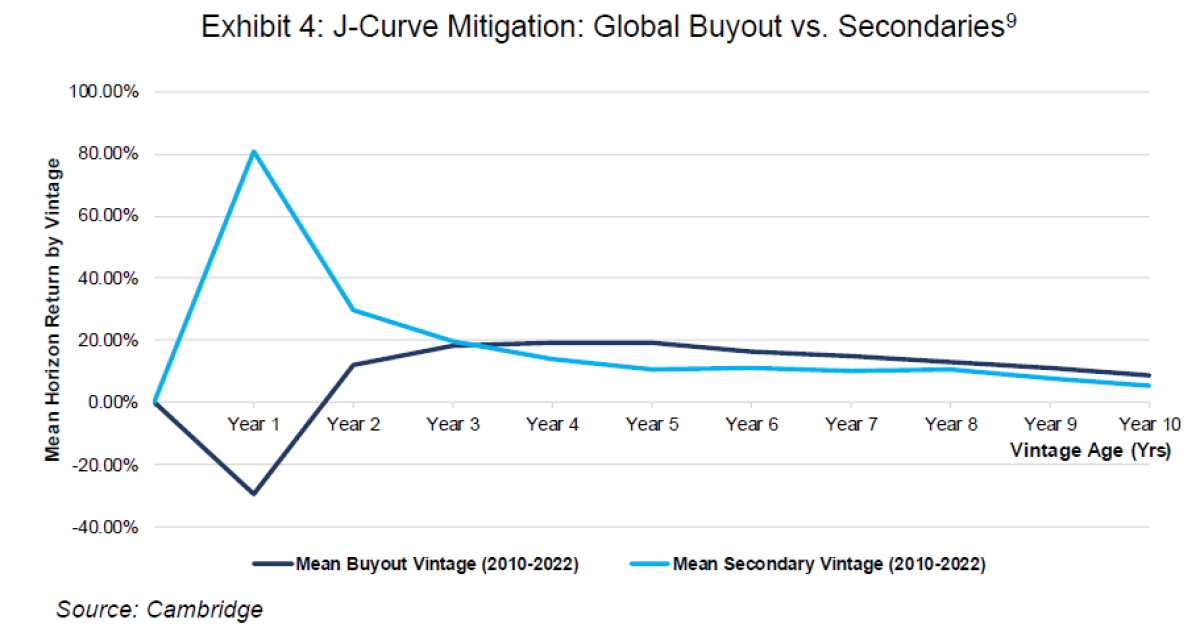

▪ J-Curve Mitigation: Secondary investments can help mitigate the J-curve effect commonly associated with primary private equity investments, as they often involve acquiring seasoned assets with established track records, the potential for more immediate cash flows, and less of a drag (relative to primary funds) from fees levied on committed capital.

▪ Potential for Attractive Pricing: Secondary investments may offer pricing advantages compared to primary investments, as they often involve acquiring assets at discounts to net asset value (NAV), providing opportunities for attractive risk-adjusted returns. After all, who is more likely to command a premium – the investor in need of liquidity or the one providing it? These initial discounts can vary in magnitude but typically result in strong interim performance from the immediate write-ups of new

investments.

▪ Reduced Blind Pool Risk: Unlike primary investments in blind pool funds, where investors commit capital without knowledge of the specific assets, secondary investments allow investors to assess the performance and composition of existing portfolios, reducing the risk associated with investing in unknown assets.

Secondary Shapes and Sizes

There is no one-size-fits-all approach to investing in secondaries. Managers of secondary-focused funds run the gamut, with a high degree of variation across:

▪ Fund Size (Large vs. Small)

▪ Asset Class (Buyout vs. VC/Growth vs. Real Estate/Real Assets vs. Distressed/Credit)

▪ Strategy (LP-Led vs. GP-Led4 vs. Hybrid)

▪ Asset Type (Single-Asset vs. Multi-Asset/Multi-Fund)

▪ Maturity (Tail-End vs. Inflection Point vs. Seasoned Primary)

▪ Geography (North America vs. Europe/ROW)

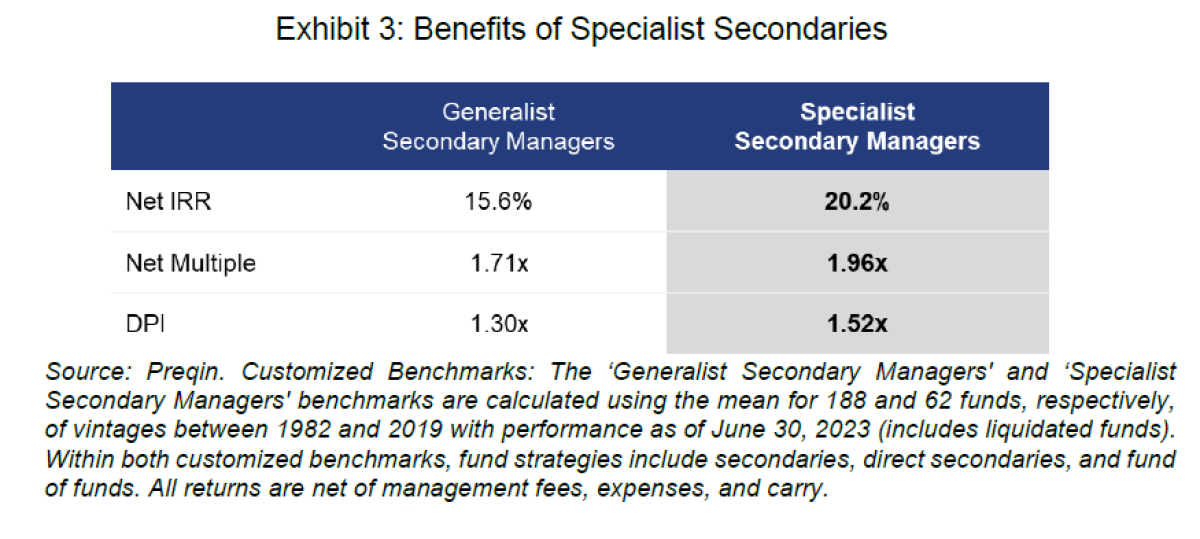

One way to simplify the degrees of diversity above is to narrow the universe of secondary managers into two camps: generalists and specialists.

Our research supports the notion that specialist secondary managers maintain several key advantages over their more generalist counterparts:

▪ Higher Underwriting Standards: Specialists focus on quality, not quantity, and do not rely on leverage and deal structure to manufacture returns.

▪ Smaller Transaction Size: Specialists operate in less efficient markets where sellers are motivated by factors other than price. With smaller transaction sizes, specialists can originate unique transactions and obtain attractive discounts.

▪ Origination Advantage: With greater focus, specialists have an advantage in originating and underwriting LP and GP secondaries within specific strategies, end markets, and geographies.

The specialized knowledge and market focus of secondary specialists allow them to discover and capitalize on opportunities that more generalist managers may overlook. According to our analysis, these structural advantages have translated into a better return experience for investors in specialist secondary funds.

An Evergreen Future

As we have documented recently, perpetual (or “evergreen”) funds are quickly becoming the vehicle of choice among wealth management allocators seeking exposure to private markets.6 These structures that are perpetual by design are quickly replacing traditional private funds due to their enhanced investor protections, administrative convenience, immediate investment, and periodic liquidity. Examples include SEC-registered private BDCs, private REITs, interval funds, and tender funds, each with important differences but collectively offering high-net-worth investors a more convenient path to accessing

alternative investments.

In addition to offering investors a “one-stop shop” for diversified exposure to private capital, semi-liquid perpetual funds provide allocators more flexibility in adjusting their overall asset allocations based on market conditions, rebalancing preferences, or client-specific needs.

According to a recent survey from Coller Capital7, roughly one-third of LP respondents believe that private wealth/retail capital will eventually reach institutional levels of PE exposure. Thus far, private wealth investors have not allocated as significantly to PE as they have to private debt and real estate. Of the $184 billion in perpetual funds as of September 2023, only $19 billion was in PE-focused strategies. To be fair, the PE category has seen consistent growth. There is just more runway left for PE to grow relative to other private market asset classes.

From Liftoff to Cruising Altitude

Speaking of runways, a common thread among recent evergreen PE fund launches has been significant exposure to secondaries during the initial takeoff and climb phases of a new fund’s ascent. Several asset managers have tactically overweighted secondaries relative to their stated strategic targets early in a fund’s life.

There are several reasons why a semi-liquid evergreen fund might overemphasize secondaries in the first couple of years post-inception. First, semi-liquid funds must strike a delicate balance between the duration of their holdings and the frequency/magnitude of the liquidity they offer investors. Secondaries can help in this regard. Second, because capital inflows into a perpetual fund are typically deployed all at once, it is crucial that investors step into a highly diversified portfolio with minimal cash drag on day one. Third, and perhaps most obvious when evaluating these funds’ return patterns, is the outsized interim returns that can help a new fund gain traction via the immediate markup to NAV of assets purchased at a discount.

Earlier in this paper, we mentioned J-curve mitigation as one of the key benefits of secondaries. Not only do secondaries largely bypass the J-curve, but they also often exhibit a distinct curve of their own. Ares8 describes this as the n-curve:

“The phenomenon where a secondary fund purchases assets at a discount to NAV, and therefore shows a strongly positive early interim IRR. This discount amortizes over the holding period of the investment, which can lead to a declining IRR as the secondary fund matures. This results in an IRR-over-time profile distinct from traditional primary funds, where interim IRR tends to start out negative as a result of fee drag and later increases as underlying assets appreciate (sometimes referred to as the J-curve). That secondary funds purchase primary fund interests after the latter’s early high fee scrape period also contributes to the ncurve.”

The chart below visually depicts the n-curve relative to the J-curve.

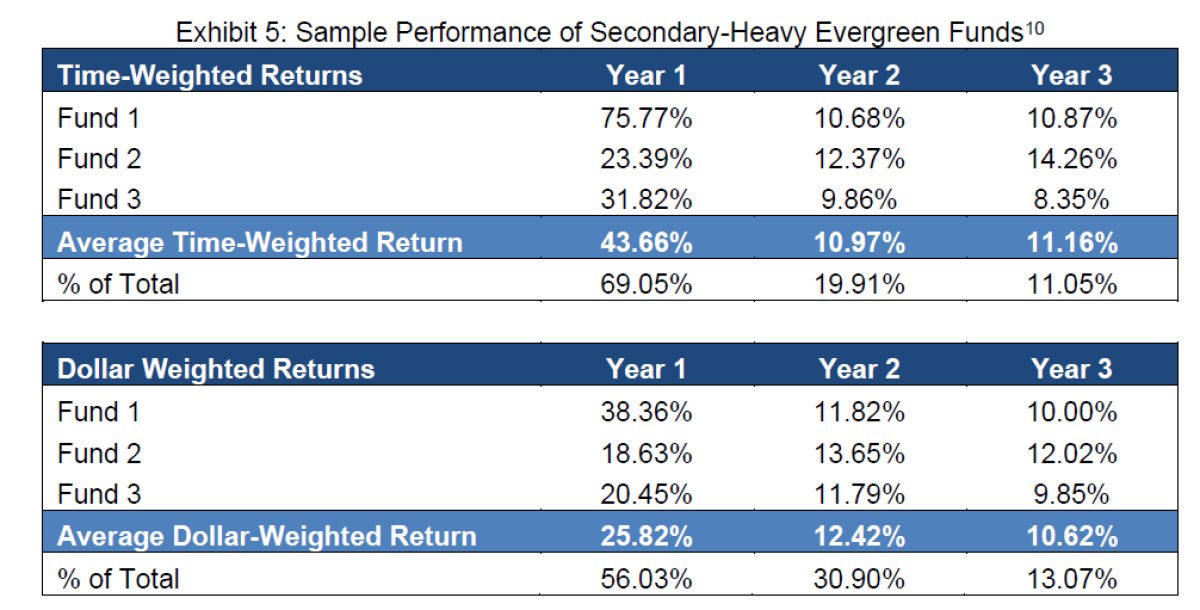

We have seen this concept play out in real-world results. We analyzed the first twelve months of performance for all ‘40 Act evergreen PE funds launched since 2020 with observable data to their investment type. Of the eleven funds in the sample, we found that:

▪ Funds that were ≥ 50% invested in secondaries returned ~33% on average in their first year, and

▪ Funds that were < 50% invested in secondaries returned ~11% on average in their first year.

We then homed in on a narrower subset of these funds, subject to certain AUM, track-record length, and secondary weight parameters. The remaining three funds, whose names we have omitted, were then reviewed to see if anything of note stood out. While admittedly a small sample size, we did notice a consistent pattern where year-one performance is substantially larger than performance in years two and three. This illustrates the n-curve idea in practice and supports the perception that early adopters of evergreen PE funds with material secondary exposure have benefited relative to investors coming in later.

Once the desired cruising altitude is reached during a flight, the aircraft levels off, and the engines adjust to maintain a steady speed and altitude. This marks the beginning of the cruise phase, where the plane covers the majority of its journey at a consistent altitude and speed. Asset managers should take note as they consider the evergreen model's objective of perpetual capital deployment, liquidity management, and durable long-term excess returns.

When an evergreen fund reaches its desired “altitude” of portfolio diversification and scale, it makes sense to scale back the reliance on secondary investments in favor of co-investments and/or primary fund investments. By diversifying the investment approach beyond secondaries, evergreen PE funds can capitalize on a broader range of opportunities and market dynamics.

Secondaries: Invest Early and Often, But Not Only and Always

We’ve all heard the expression, "If all you have is a hammer, everything looks like a nail." Similarly, if all we have are secondaries, everything might start looking like a discount-to-NAV arbitrage. The problem with an “all secondaries” approach is that it favors instant gratification at the expense of delayed, sustainable gratification.

It’s important to remember that the initial markup to NAV does not ensure a positive long-term return or exit. A discount to current NAV is different than a discount to future intrinsic value, or IV. Successful secondary outcomes require more than one way to win – healthy discounts combined with fundamental value creation. If executed properly, the benefits from underwriting the quality of the underlying asset(s) should outweigh any entry discount.

Direct co-investments and, to a lesser degree, primary fund commitments should also play a role in an evergreen private equity program. Co-investments offer greater control over investment selection, lower fees, and potentially higher returns. However, a diversified co-investment book simply takes time to build.

Modest and judicious primary commitments, while introducing J-curve dynamics into the equation, can be a great lever to pull when building relationships with hard-to-access GPs and entering their co-investment deal flow orbit.

In short, the Goldilocks principle applies to the use of secondaries in a diversified private equity portfolio – not too hot, not too cold, but just right.

Closing Thoughts

The secondary market in private equity has become a strategic necessity due to shifts in global investment paradigms. As investors become more sophisticated and require greater liquidity and flexibility in private markets, the secondary market has evolved from being a niche play to a vibrant ecosystem. Unlike in the past, when secondary transactions were mainly driven by the need to manage illiquid assets in constrained market conditions, today's secondary market offers a diverse range of solutions to both GPs and LPs. Innovative structures such as GP-led restructurings and specialized secondary funds have transformed the market into a critical tool for active portfolio management.

As we look to the future, the secondary market is poised to play an even more important role in the private equity industry writ large. Continued innovation in transaction structures, combined with technological advancements, will enhance market efficiency and transparency. This will enable the secondary market to provide tailored solutions that meet the changing needs of investors, thereby solidifying its position as an indispensable component of the private equity landscape.

Asset managers developing evergreen private capital solutions for individual investor consumption can and should use secondaries deliberately, strategically, and opportunistically. But, they should not become a crutch. Rather, they should be leveraged as one of many tools in the toolbox to obtain comprehensive exposure to private markets and achieve desired investor outcomes.

For their investment merits, there’s a lot to like about secondaries. But, they are not a panacea. The strengths of secondaries can help offset the drawbacks of primary fund commitments and co-investments in perpetual fund vehicles, and vice versa. Instead of either/or, they should all work in harmony.

Private equity’s second act is being defined by the parallel trends of evolving secondary markets and the accelerating adoption of semi-liquid evergreen funds. We suspect this will ultimately lead to Act III: A more inclusive and secure future for individual investors where private markets are a staple of

well-diversified portfolios.

Footnotes:

1 VCFA Group founder Dayton Carr is believed to be the mastermind behind the earliest private equity secondary transaction.

2 Source: Jefferies, “Global Secondary Market Review, January 2024”.

3 Percentages indicate year-over-year growth in total volume, LP volume, and GP-led volume. The figures and percentages provided are based on publicly available information and may be subject to revision or update. Readers should exercise caution when interpreting the data and consider additional factors that may impact secondary market trends.

4 For a detailed review of GP-Led Secondaries, see Cliffwater research paper, “The Prevalence and Impact of GP-Led Secondary

Transactions (October 2021).”

5 For illustrative purposes only and are not necessarily representative of all Cliffwater relationships. There is no assurance that similar investments will be made.

6 Source: Cliffwater, “Perpetuals Gaining Traction Again, Despite Real Estate Headwinds,” December 2023.

7 Source: Coller Capital, “Global Private Equity Barometer, Winter 2023-24”.

8 Source: Ares, “Navigating Secondaries: A Guide to Changing Currents, April 2022”.

9 The analysis was conducted internally by Cliffwater. The sample size consisted of '40 Act evergreen private equity funds launched since 2020, with observable data regarding their investment type. Performance figures are based on internal calculations and may differ from publicly reported figures. The results may not be indicative of future performance and should be interpreted with caution due to the limited sample size and other factors. Additionally, the omission of fund names is intended to preserve confidentiality and should not be construed as a reflection of the performance or characteristics of any specific fund.

10 Specific fund names have been excluded. Inclusion is based on SEC-registered private equity-focused funds using interval fund and tender fund structures that were launched in 2020 or later, with at least a 3-year track record, at least 30% of their portfolio in secondaries, and with net assets greater than $250 million. Data on performance metrics was collected on a semi-annual basis using SEC filing reports, including Certified Shareholder Reports (Semi-Annual and Annual), all of which were obtained from the SEC database.

About the Author:

Phil Huber is the Head of Portfolio Solutions for Cliffwater, a leading alternative investment adviser and fund manager. Prior to joining Cliffwater in 2024, Phil was the Chief Investment Officer for Savant Wealth Management, a multi-billion dollar wealth management firm. Phil has been involved in the financial services industry since 2007. He earned a bachelor’s degree in finance from the Kelley School of Business at Indiana University. He is a member of the CFA Society of Chicago.

He is the author of The Allocator’s Edge: A Modern Guide to Alternative Investments and the Future of Diversification.

Phil has been featured by a number of media outlets, including The Wall Street Journal, The New York Times, InvestmentNews, CityWire RIA Magazine, and Bloomberg TV.

Phil and his wife Christie live in the northwest suburbs of Chicago where they enjoy reading, yoga, and spending time with their daughter Hannah. He is also a lifelong, die hard professional wrestling fan.

The views expressed herein are the views of Cliffwater LLC (“Cliffwater”) only through the date of this report and are subject to change based on market or other conditions. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Cliffwater has not conducted an independent verification of the information. The information herein may include inaccuracies or typographical errors. Due to various factors, including the inherent possibility of human or mechanical error, the accuracy, completeness, timeliness and correct sequencing of such information and the results obtained from its use are not guaranteed by Cliffwater. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this report. This report is not an advertisement, is being distributed for informational purposes only and should not be considered investment advice, nor shall it be construed as an offer or solicitation of an offer for the purchase or sale of any security. The information we provide does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Cliffwater shall not be responsible for investment decisions, damages, or other losses resulting from the use of the information. Past performance does not guarantee future performance. Future returns are not guaranteed, and a loss of principal may occur. Statements that are nonfactual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Cliffwater is a service mark of Cliffwater LLC.