By Stephen L. Nesbitt – Chief Executive Officer, Chief Investment Officer of Cliffwater.

Industry data suggests that investor concern over an excess inflow of capital targeting private debt is unnecessary, and to the contrary shows that the growing supply of private debt capital over the past decade (the majority consisting of direct lending) has been consistent with the financing needs of a growing US buyout market. This finding is also consistent with the persistence of significant yield spreads in private direct middle market loans, the ultimate arbiter of supply and demand for financing.

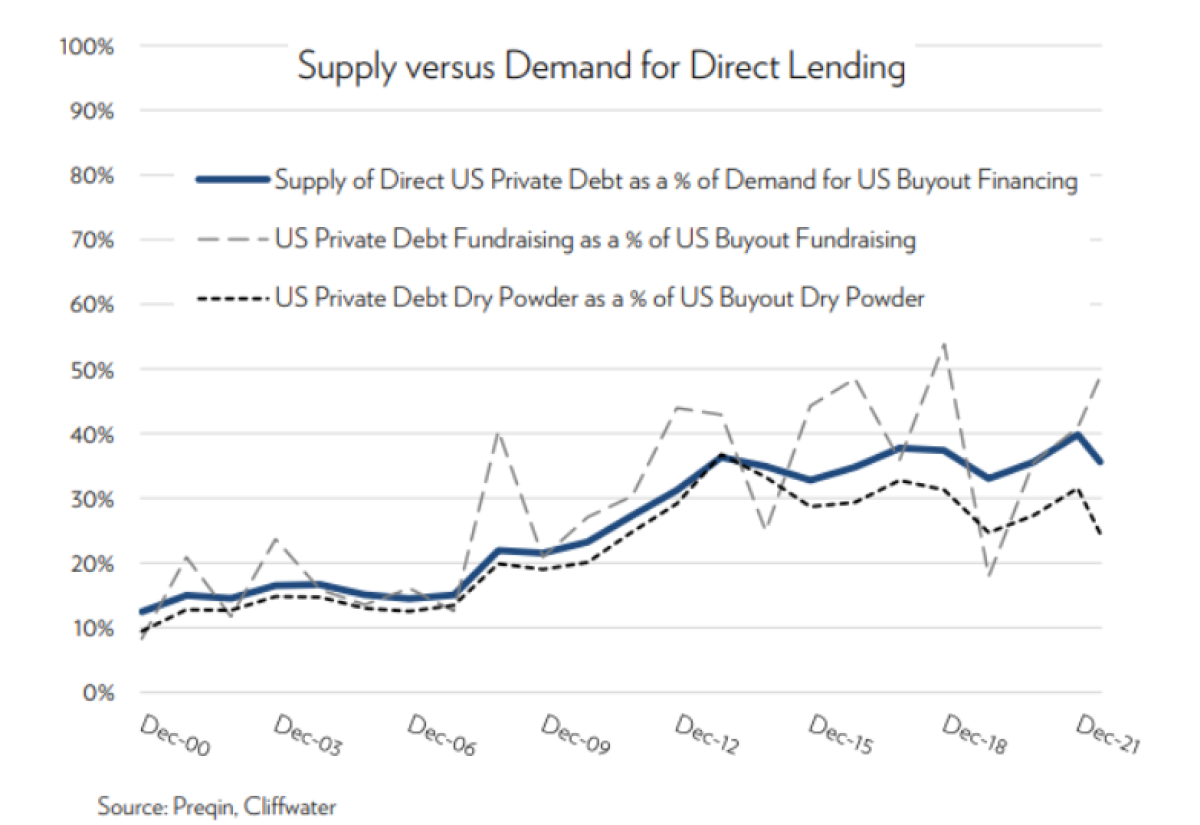

The chart below provides three related metrics that put the growth of performing private debt in the context of a broader US private market ecosystem that has been growing at three times the rate of the public markets over the last 20 years. The three metrics are fundraising, dry powder, and total supply/demand.

All three metrics express private debt as a percent of US buyouts, the segment of private equity that most utilizes private debt for financing. Since approximately 50% of US buyouts is debt financed, US private debt would equal approximately 100% of US buyout equity capital if it was the only source of financing. However, as the chart shows, US private debt, represented by the Preqin database consisting primarily of institutional private debt capital, represents approximately one-third of the financing needs of US buyout firms. Importantly, private direct debt doubled as a percent of US buyout equity needs after the 2008 Financial Crisis, as bank lending retreated, but has remained a consistent percentage over the last decade. If there was too much new institutional supply, which includes public and private BDCs, market penetration would be increasing, pushing out other suppliers of buyout financing like banks, insurance companies, non-bank finance companies, and hedge funds. Instead, the level market share for US private debt suggests that the “too much money” condition is not present.

About the Author:

Steve Nesbitt is Chief Executive Officer and Chief Investment Officer of Cliffwater, and is primarily responsible for the day-to-day management of Cliffwater Corporate Lending Fund (CCLFX) and the Cliffwater Enhanced Lending Fund (CELFX), an SEC-registered credit interval fund focused on the US corporate middle market.

Steve is recognized for a broad range of investment research. His papers have appeared in the Financial Analysts Journal, The Journal of Portfolio Management, The Journal of Applied Corporate Finance, and The Journal of Alternative Investments. His private debt research led to the creation of the Cliffwater BDC Index, measuring historical BDC performance, and the Cliffwater Direct Lending Index, measuring historical performance for direct middle market loans. Steve authored the book, Private Debt: Opportunities in Corporate Direct Lending, Wiley Finance (2019) which provides the analytical and empirical underpinnings of the private debt market.