By Michael Edesess, Ph.D, Managing Partner / Special Advisor at M1K LLC.

Readers may recall that in 2014, a weighty (700-page) and abstruse book, Capital in the Twenty-First Century, written by French economist Thomas Piketty, became a surprise best-seller, reaching number one on The New York Times best-seller list for hard-cover nonfiction. The book had been published a year earlier in French to little fanfare, but sold well in foreign languages after its English translation achieved best-seller status.

My review of the book for Advisor Perspectives was published on May 6 of that year. It was titled, “The Book that will Reshape the Study of Economics.” In the review I wrote, “The book uses data to develop a framework for its analysis that will embed it firmly in the intellectual history of the coming decades, if not the coming centuries.” I further wrote, “It will be Piketty’s data and framework, not his conclusions or policy recommendations, that propel his book to the center of discussion and debate about economics and our economic future.”

It is too soon to tell if these predictions will prove accurate. But much discussion of economics since the book’s publication has indeed been influenced by Piketty’s data and analytic framework.

The data contained in two of his graphs has entered the general consciousness about economics and its history. The information it reveals was not unknown prior to Piketty’s book, but because it became a best seller it became widespread knowledge. In particular, the data in Figures 1 and 2 below have become more widely known than they would have been otherwise.

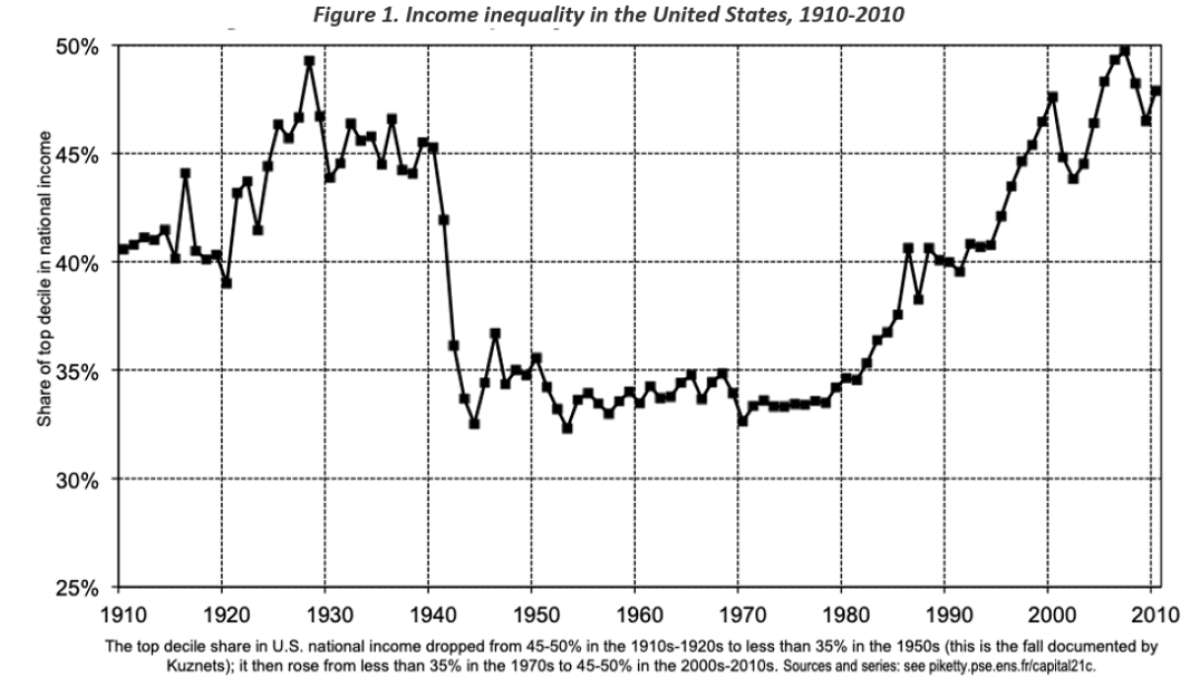

Figure 1 shows that income inequality was high in the early 20th century (as it was also in the late 19th), then low in the decades following the Second World War, and then trending high again after 1980, reaching heights in the 21st century equivalent to those of the high points in the early 20th.

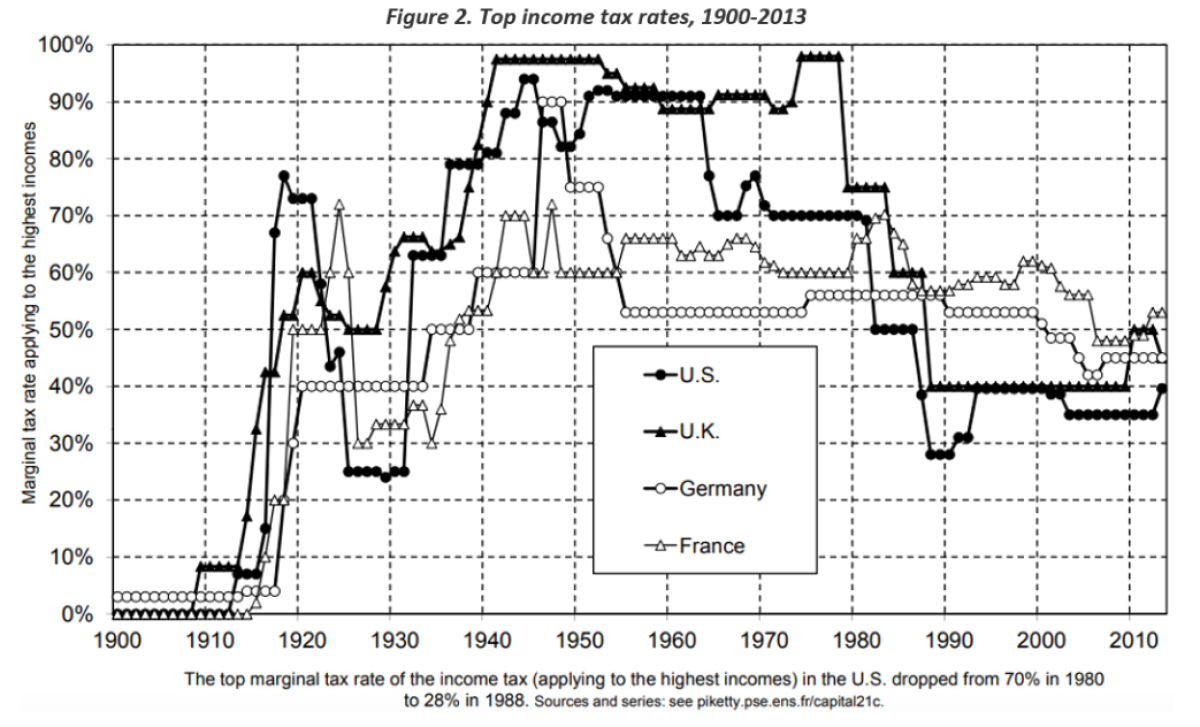

Figure 2 shows that top income tax rates were very high during the decades following the Second World War – at times exceeding 90% – a period when income inequality was at its lowest.

Also important is Piketty’s speculative formula r>g, where r is the rate of return on capital and g is the rate of growth of national income. If this formula holds true, then the rate of growth of returns to capital will exceed the growth of returns to labor. Continuation of this relationship will make inequality greater, as will the gulf between those who invest capital and those whose incomes derive from their labor.

Mordecai Kurz’s contribution to the debate

Mordecai Kurz, an 89-year-old Stanford professor emeritus with an impressive résumé of research and accomplishments in the field of economics, published earlier this year a book that has received much attention, The Market Power of Technology: Understanding the Second Gilded Age.

Kurz’s very subtitle reflects the dialogue that has been inseminated by Piketty.

As Piketty’s data in Figure 1 shows, income inequality in the United States reached peaks in the early 20th century (and late 19th) – the First Gilded Age – and in the 21st century, the Second Gilded Age. Between these Gilded Ages, following the end of World War II, there were approximately 30 years of strong economic growth in the United States and Europe – what the French call “Les Trente Glorieuses” (the 30 glorious years). These 30 glorious years of strong economic growth coincided, surprisingly, with the highest levels of top-income tax rates.

Also, in those years of moderation and high economic growth in the middle of the 20th century, as Kurz notes, the shares of labor and capital were relatively stable; r>g did not hold. But they diverged after the 1970s.

The imperfect state of economics

Kurz presents a detailed theory about why these patterns occurred over time. He draws the conclusion that a continuation of present trends will be dangerous for democracy. He then proposes policies that he believes will remediate those trends.

Like so much of latter-day economic concepts, Kurz’s theory finds gaping holes in the idealized bedrock of classical economics. The classical theory depended on the assumptions of perfect information and perfect competition among a large number of small firms or consumers who individually have little or no market power to affect prices.

Much of the more recent history of economics Nobel prizes has been for works that poke holes in these assumptions. George Akerlof, a recipient of one of those prizes, wrote in his seminal paper “The Market for Lemons” that access to information is not perfect but is asymmetrical between buyers and sellers. For example, the seller of a used car has much more information about the condition of that car than a potential buyer.

Elinor Ostrom won a Nobel prize for identifying the gray areas between the presumed perfect “invisible hand” of the market, and market failures like “the tragedy of the commons” in which rather than allocating resources as perfectly as possible, competition among “rational egotists” results in depleting resources unsustainably. In both extremes – the perfect “invisible hand” and the disastrous “tragedy of the commons” – the assumption is that economic actors act independently and selfishly and without coordination, sometimes with superior results, and sometimes the opposite. Ostrom showed that in many cases, neither occurs; rather, a combination of individually minded rational egotists and community-minded “norm users” work together to bring about pragmatic solutions.

Market power

Kurz’s exception to the idealistic classical theory is on a different track. He argues that companies that are technological innovators develop long-term “market power” that is difficult for competitors to overcome. This market power stems initially from legally sanctioned patents or know-how that is kept private, but it continues for a long time because of first-mover advantages, network effects, and numerous other advantages that are acquired by the first movers in a technology – even if the technology is not superior to those of competitors – making it difficult for “creative destruction” by competitors to overcome those advantages.

Kurz presents much evidence for this argument. It is an argument that is easy to accept, when so many (or rather so few) companies like the “Magnificent Seven” exhibit a “winner takes all” dominance in their markets.

The core of Kurz’s analysis is a new, or reorganized, approach to corporate accounting. Says Kurz, “Economists often divide income into labor and capital, lumping profits with capital income, and this practice omits important information about profits and market power.”

Instead, Kurz divides the income created by a firm or an economy into “three compensations: labor compensation, capital compensation, and profits brought about by market power or monopoly profits.”

In chapter 3, “Monopoly Wealth and Intangible Capital,” Kurz presents a detailed technical exposition of his method of accounting and its differences with conventional accounting practices, focusing especially on the concept of “goodwill.” I am no accountant, and I have never taken an accounting course (or for that matter any course having to do with money in either undergraduate or graduate school) and I find this chapter difficult. But Kurz’s general idea is easy to understand.

Some of a corporation’s revenues go to pay labor. Some go to support capital assets, by paying investors who put up the funding to provide those assets a reasonable interest on their investment. If there is more revenue than enough to cover these costs, that excess revenue is profit.

If the classical concept of an ideal market with perfect competition held true, there would be no further revenue, only enough to cover those costs, and therefore no profit. If there were more revenue than that, competitors would provide the same good at reduced prices until the price had been driven down to equal the costs.

Therefore, if a company does realize a profit, it must be because the ideal of perfect competition in its product does not hold true. In other words, the company must have monopoly power.

Therefore, Kurz calls the remaining component of revenue after labor costs and capital costs “monopoly profits,” and its present value “monopoly wealth.”

Kurz says that contrary to the classical economic theory, firms that create technological innovations will naturally accumulate monopoly profits and monopoly wealth. Beyond the profit protection provided by patents and private know-how, which expire after a number of years, these firms will have longer-lasting monopolistic characteristics. They will have loyal customers, deep information derived from their long-standing relationships with their customers, possibly network effects due to customers and suppliers wanting to use the same service that others use, and many other advantages over potential competitors. Therefore, the assumption that continued “creative destruction” will destroy monopolies, according to Kurz, is untrue.

Implications and correctives

This creation of monopoly profits by technological innovators, Kurz believes, leads to increasing levels of inequality, which eventually become a threat to democracy. This is a bit of a leap to a conclusion, but it can be provisionally accepted, at least to see what further implications Kurz draws.

Kurz also argues from classical economic concepts that these monopoly profits will reduce economic productivity and growth. This is because excess monopoly profits obviously mean higher prices for the monopolist’s products, and therefore lower demand and production than there would be otherwise. This strikes me as an argument requiring the usual ceteris paribus assumptions of economic theorizing, but the ceteris are never actually paribus in the real world (all other things are never equal). But if Kurz’s argument holds true, it could be a contributing factor to the higher economic growth of the Trente Glorieuses, when monopolistic practices were more held in check by anti-trust policies and unions.

Kurz believes that remedies must be found to cut monopoly profits to reasonable levels – such as those that can be accumulated solely due to patent protection, for example, which was its original purpose, i.e., to incentivize technology innovators and reward them for their initial investments of research and time by enabling them to amass monopoly profits for a limited time. Kurz believes that monopolistic profits should be held only to that, and even then he believes that too many patents are awarded, and that “The number of patents issued should be reduced by raising the degree of novelty required for a patent.”

Original Article as posted on Advisor Perspectives/VettaFi

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Michael Edesess, Ph.D is an accomplished mathematician and economist with a Ph.D. in pure mathematics in stochastic processes and expertise in the finance, energy, and sustainable development fields. He is an adjunct associate professor in the Division of Environment and Sustainability at The Hong Kong University of Science and Technology, managing partner / special advisor at M1K LLC, and a research associate of the EDHEC-Risk Institute. He is author or coauthor of two books and numerous articles published in Advisor Perspectives, MarketWatch, The Wall Street Journal, Financial Times, South China Morning Post, Bloomberg, Nikkei Asian Review, Technology Review, and other publications, and was previously a co-founder and chief economist of a financial company that was sold to BNY-Mellon. He has chaired the boards of three major nonprofit organizations in the fields of energy, environment, and international development.