By Joe Elmlinger, Head of Client Solutions, and Alex DeFeo, Senior Portfolio Manager at Lake Hill.

The market can crash or decline sharply at any time. Portfolio managers who simply buy index puts (or a strip of index puts) to hedge their downside are likely to be severely disappointed if either the hedge doesn’t pay off when expected or the costs of the hedging program pile up over time.

This paper focuses on the correct way to hedge an equity portfolio by purchasing put options within a defined annual budget of total option premium spend.

Many articles have been written either supporting or refuting the idea of buying puts to hedge a portfolio. The position of this paper is that purchasing defensive puts within a budgeted framework is a viable hedging strategy for certain investors under certain circumstances, but the strategy must be executed properly to deliver the highest probability of success and ensure its longevity.

The Lake Hill mantra is that to succeed with options, investors must be both disciplined and patient. Successful options strategies are those that, over time, take advantage of the odds by buying and selling options with positive expected value. To achieve that, you also need a lot of sophisticated technology.

Purchasing put options within a defined budget is a straightforward proposition, and it is largely for this reason that many investors find the strategy attractive, but there are some important limitations:

Put options are a form of insurance. Investors should not expect to be able to buy insurance in a deep liquid market and consistently earn more than the premium they pay to the insurance sellers. It cannot be done in the property or life insurance markets, nor can it consistently be done in the equity options market. However, investors who buy put options can significantly reduce the costs and increase the odds of a payout if the option portfolio is managed correctly. Simplistically buying a strip of out-of-the-money puts spread over various expiration dates and waiting for something to happen is not the correct way to go about it.

Put buying strategies are tail hedge strategies. At-the-money puts cost more than out-of-the-money puts. Therefore, when you’re on a budget, you buy far out-of-the-money options. The further away from the money the option is, the less likely it is to pay off. Far out-of-the-money options are, therefore, tail hedge instruments. Put-buying strategies must be distinguished from risk-mitigation strategies such as put spreads or put spread collars in which the short options play an important role – those strategies are not discussed in this paper.

Investors are impatient. Most investors simply don’t have the stomach to tolerate continued losses (expenditures) month after month or year after year as they wait for the rare market catastrophe to happen. The purchased put portfolio will consist of relatively far out-of-the-money options that statistically have a low likelihood of paying off. This means that a long time will likely pass before any of the puts yield their intended benefit. Whatever the CIO or investment committee may say today about their willingness to spend money to protect against a market crash will almost certainly be “re-evaluated” after a short number of years of continued drain.

Many put buying strategies are designed to spend no more than about 50-100 bps per year of portfolio NAV (e.g., in protecting a $1 billion equity portfolio, don’t spend more than $5-10 million per year buying put options). A strategy with such a modest annual budget will have a certain risk profile due to those limitations. The hedging portfolio must be constructed based on certain parameters that determine the mix of strike prices and maturities as well as how they are actively rebalanced over time.

Most of the anti-put buying pundits point to the track record of simplistic strategies that hold until to expiration (e.g., the CBOE PPUT Index). They claim that since these simple approaches invariably show losses historically, they should not be used. Conversely, many put buying supporters demonstrate the benefits of “tail hedges” by simulating what might happen in the event the market instantly drops by 10%, 20%, or more. Because such dramatic instantaneous market shocks really don’t happen, they won’t be found in backtests, so they must be simulated to show a potential “what if” benefit.[i]

We believe both sides are missing critical points: 1) Put buying strategies don’t have to be uber-simplistic, and 2) Sharp market declines can occur over time and are often devastating.

It is relatively easy to buy a strip of three-, six- and/or twelve-month out-of-the-money options and roll those options before they expire. The difficult things include:

- Keeping the annual option purchasing budget steady while still covering the entire portfolio NAV.

- Establishing a process for monetizing the put options.

- Determining the optimal way to roll the positions so that the hedging program stays within the risk parameters at all times. That means choosing the best strike prices and maturities and re-evaluating the hedge portfolio as the market moves.

- Estimating the hedging program’s likely performance for a variety of scenarios across price movements and time.

Most put-buying programs that we have seen do not have access to the technology that allows for numerous strikes and positions to be rolled, added or removed daily, while maintaining risk parameters within a tight tolerance.

Designing the Strategy

Designing a put-buying strategy within a budget quickly raises issues. Since market conditions change all the time, it is impossible to know exactly how much protective puts will cost in the future. One can either set a fixed budget for the premium expenditure and modify the notional amount of the portfolio protection (how much of the NAV will be protected) or fix the notional amount of protection and consistently purchase puts such that the budget becomes uncertain.

The Simplistic Strategy

A simplistic strategy (that is not likely to perform as anticipated) might use 30% out of the money put options. The sample portfolio buys half the puts that expire in 3-months and the other half with puts that expire in 6 months. This means that every 90 days - as the nearby option is expiring - a new 6-month out-of-the-money option is purchased in a notional amount equal to half the portfolio size. Looking at such a hedging portfolio since 2005 reveals some significant issues regarding both the degree of expected portfolio protection and the annual cost of the program.

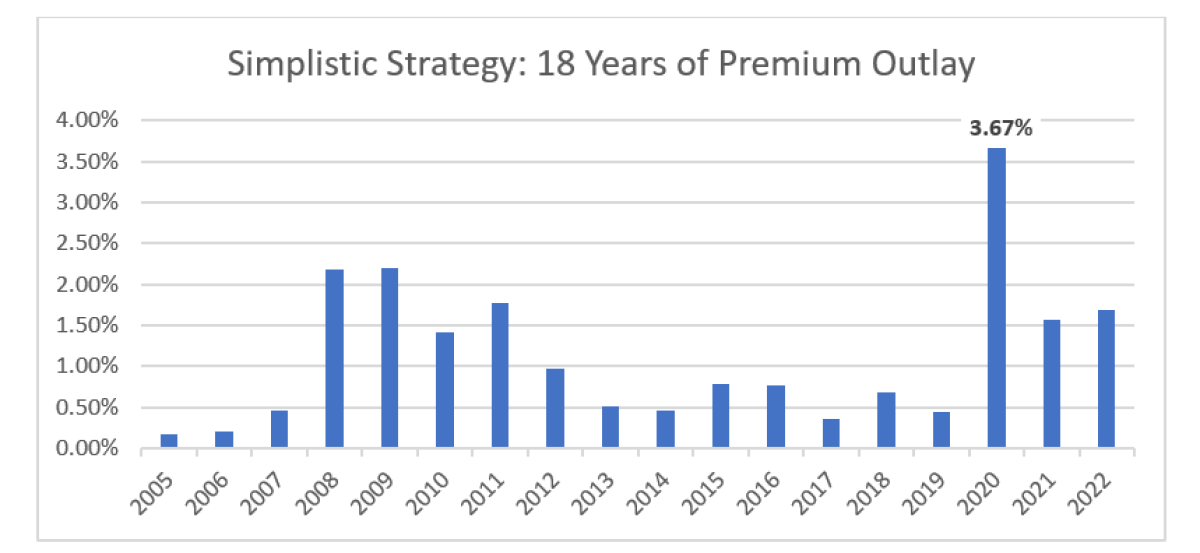

Simplistic Strategy: Annual Premium Expenditures Since 2005

Even when using quite far out-of-the-money strike prices, keeping the annual expenditure within tight bounds becomes extremely challenging if the notional amount of portfolio protection is held constant. The annual expenditures for protective puts in this backtest fluctuate widely from 17 bps to over 367 bps per year. The average annual premium outlay over the entire 18-year period is 113 bps per annum. Note that this is the sum total of the premium expenditures in each calendar year, not the profit/loss of the option portfolio in a given year (which is discussed later).

The Lake Hill Approach

Lake Hill’s technology can greatly reduce the uncertainty of the annual program cost and the wild fluctuations in the amount of expected portfolio protection. Lake Hill’s daily optimization routine attempts to both lower the average annual cost of the program and maintain consistency in the level of portfolio protection (as measured by numerous metrics not detailed in this paper).

Lake Hill Approach: Annual Net Cost since 2005

Using the optimization process means that the put option portfolio can potentially change as frequently as daily. Therefore, assessing the cost of the program requires looking at the profit and loss over time, not simply the actual premium outlay.

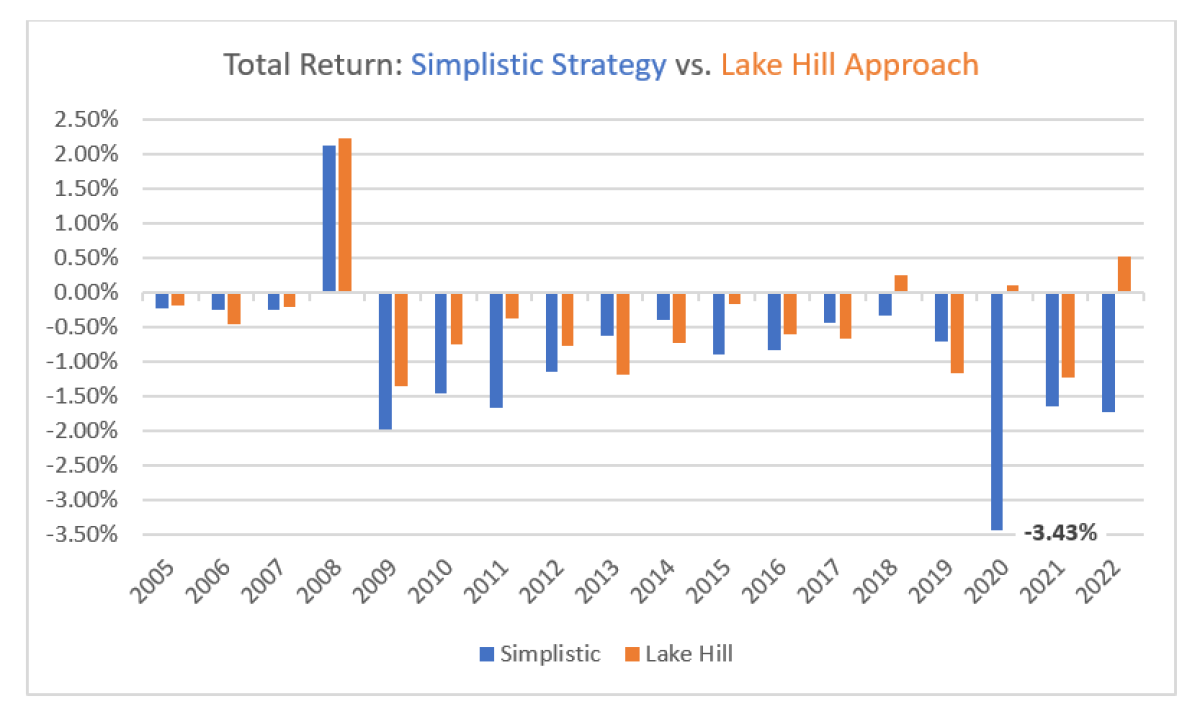

A side-by-side comparison of the profit and loss of each strategy shows the efficiency and consistency of the Lake Hill Approach:[ii]

Comparing the Two Strategies

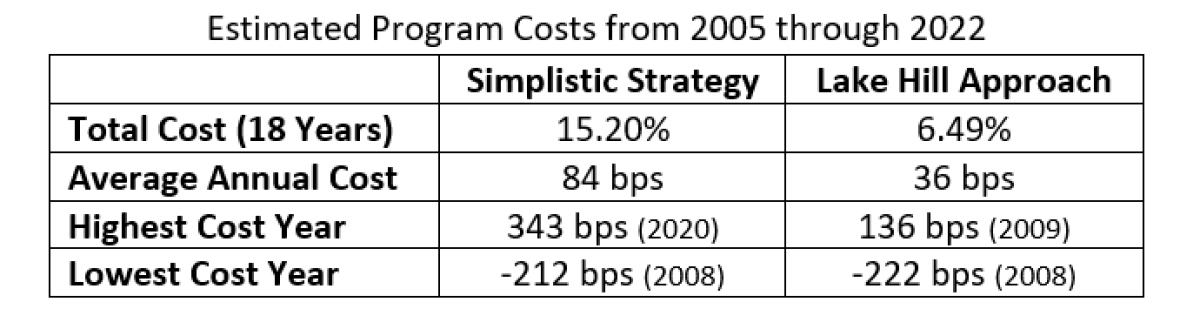

The differences are remarkable. The backtest covering the period Jan2005 thru Dec2022 shows the theoretical cost would have been less than half of those of the simplistic strategy. All while providing protection when needed most. (i.e. 2008, 2022 etc.)

To avoid cherry-picking, we looked at the 10 years between 2010 and 2019 when the market rose steadily and owning far out-of-the-money puts resulted in few, if any, mark-to-market gains. Over that period, the simplistic strategy cost 824 bps in total (82 bps p.a. average) while the Lake Hill approach was significantly less costly 596 bps (60 bps p.a. average).

Conclusion

There are over 10,000 differing strikes on the Index options complex available to trade on any given day, thousands of which are out-of-the-money puts. Premiums go up and down every day. There are potentially millions of options combinations one should analyze in real time. Even restricting the universe to single options and a few expirations requires accurate real-time monitoring of the entire spectrum of premiums and a disciplined process to evaluate changes in price, skew, term structure, bid-offer spread, liquidity, and other volatility surface dynamics. In short, massively increasing the odds of success of a “simple” put buying strategy requires the ability to run a large-scale optimization that takes all the pricing and risk metrics into account and reacts to market conditions instantly. Success also depends on the ability to execute option trades as efficiently as the leading market-makers, high-frequency brokers, and proprietary options trading shops, who are likely the ones taking the other side.

We believe that simplistic put buying strategies typically underperform not because they are inherently bad or inexorably doomed to fail, but rather because of the investment manager’s lack of advanced technology and process discipline.

A simple put protection program with a defined annual budget may be easy to understand and explain but not so simple to implement. The benefits may quickly be lost if the costs mount, the catastrophic event does not happen, or even worse - if the payoff doesn’t happen when the event occurs. By adding sophisticated technology and a disciplined process, a put buying program can be made far more efficient, consistent, and predictable.

Footnotes:

[i] Hypothetical shock payoff “what if” estimates raise many issues as assumptions must be made about other factors such as how implied volatilities will change if the market quickly moves sharply in ways that may have never happened before. Shock payoff “what-ifs” also reveal a typical limitation of commercially available options software: Modeling multi-period drawdowns (over days or weeks), anticipating monetization and/or rolling actions, and/or incorporating delta hedging steps is far more complicated.

[ii] The Total Return includes the effect of any mark-to-market gains or losses on the option portfolio in a given calendar year (each year begins and ends with open option positions) while the Annual Premium Outlay is only the actual amount spent purchasing options in a given calendar year. For the simplistic strategy, the premium expenditure in 2020 was 367 bps but the total return was a loss of only 343 bps due to 24 bps of unrealized profit.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Authors:

Joe Elmlinger is Head of Client Solutions at Lake Hill. For over thirty years, Joe has been a pioneer in derivatives sales and is recognized as a leader in equity derivatives, structured products, and customized financial engineering for clients.

Previously Mr. Elmlinger was Head of Sales for Equities & Derivatives at Société Générale. Mr. Elmlinger spent the majority of his career at Citigroup and its predecessor, Salomon Brothers, as Global Head of Equity Derivatives. He has also held senior roles at Bankers Trust Company, Merrill Lynch, the Board of Directors of ISDA and The Options Clearing Corporation.

He has a B.A. from the University of Vermont and an M.B.A. from Stanford University.

Alex DeFeo is a Senior Portfolio Manager at Lake Hill with a finance career spanning more than two decades. Prior to joining Lake Hill, he was a Senior Portfolio Manager at Goldman Sachs where he focused on Alternative Risk Premia and Volatility Strategies. He has also held senior positions at Credit Suisse, where he served as the Head Trader and Portfolio Manager for the Alternative Beta Strategies group and at Bank of America.

Alex has been a guest lecturer at the London School of Economics and an instructor at UC Berkeley. Some of his research has been funded by the US Army, the Department of Defense, and the National Science Foundation.

Alex earned an M.S. in Mechanical Engineering from the University of California, Berkeley, and a B.S. in Mechanical Engineering from the Massachusetts Institute of Technology.