By Aaron Vale, CAIA, CFA, MFin, Global Managing Director, Mexico Infrastructure Partners

In recent years, owning a natural gas power plant in the U.S. felt tenuous. Today, it can be among the most coveted assets in private infrastructure portfolios. Investors who recognized this shift early have been rewarded. Understanding what changed, and what it means for investors, requires tracing an arc from boom to bust, and back again.

From Boom to Bust

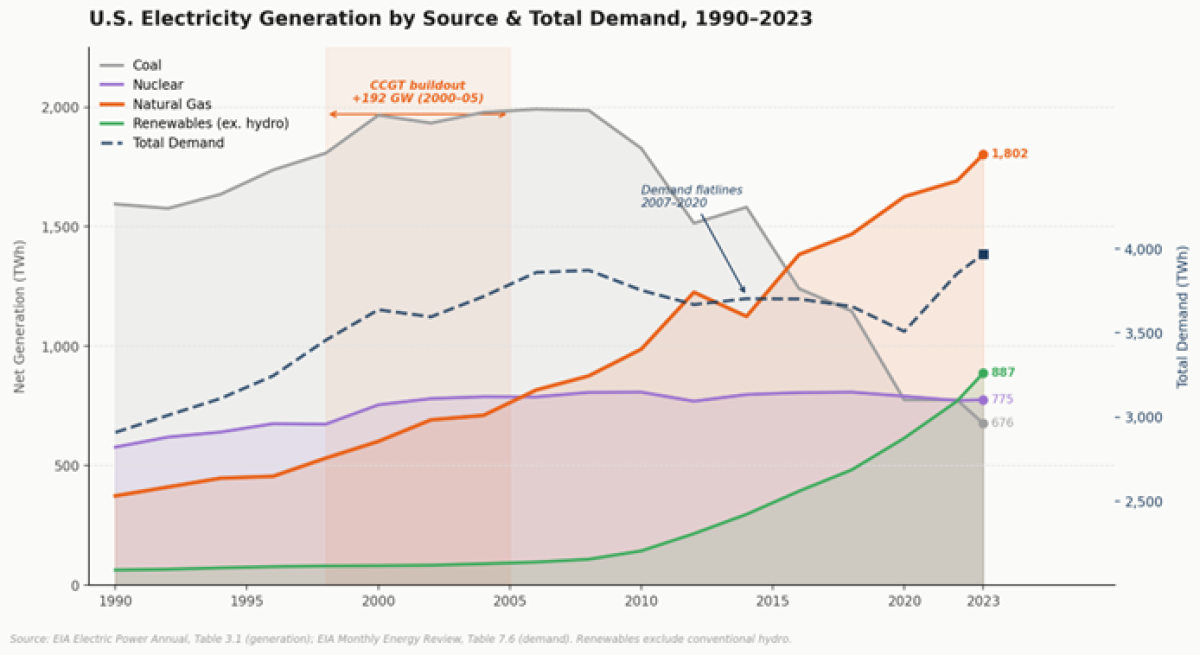

The U.S. natural gas power sector had a golden era in the late 1990s and early 2000s that set up a period of generation expansion. Deregulated electricity markets, cheaper gas, and growing power demand sparked a buildout of combined cycle gas turbines (CCGTs). These highly efficient plants became essential to the American power grid. Independent power producers and infrastructure sponsors raised billions to build and operate these power plants.

Right around 2007, things started changing. Electricity demand flatlined. Renewable energy, turbocharged by tax credits and rapidly falling installation costs, dominated investor flows as coal energy declined precipitously. Despite these changes, gas generation kept growing and became the dominant source of U.S. electricity generation.

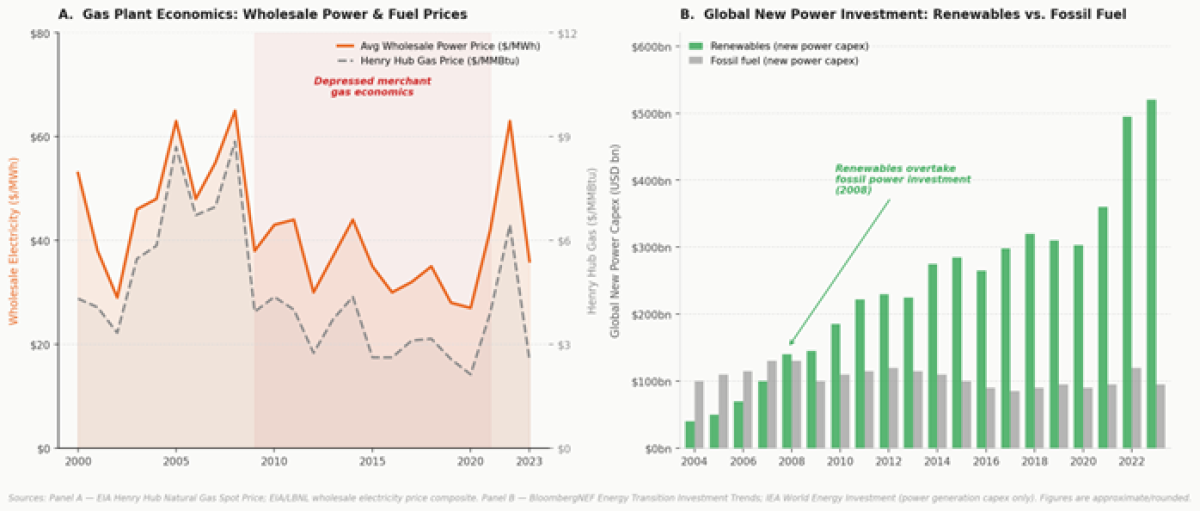

By the early 2020s, merchant gas plants (i.e. those selling power without long-term contracts) saw their cash flows eroded after a decade of low prices. Bankruptcies and distressed sales followed as certain projects couldn't keep up with their debt payments. Infrastructure investors had voted with their wallets: gas was yesterday's story; renewables were the present and future.

The Demand Shock

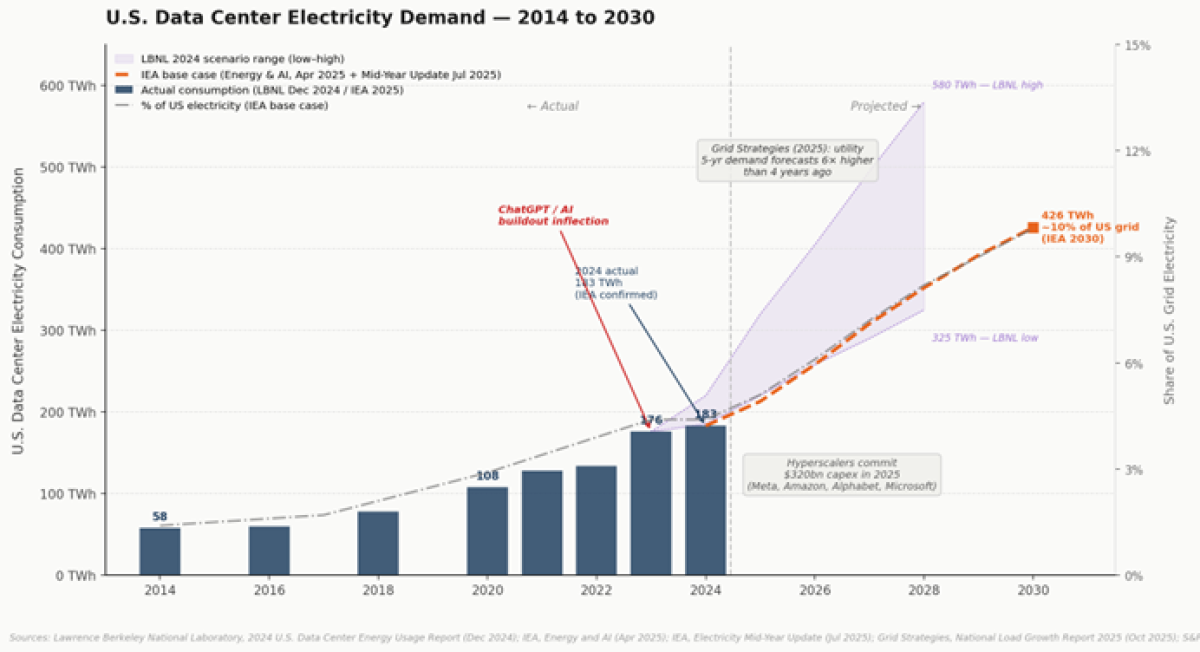

A strong reversal began in 2023 with the emergence of artificial intelligence. Data centers consumed roughly 4% of total U.S. electricity in 2023 but that share is projected to reach 10-12% by 2028 as hyperscalers race to build out compute capacity for training and inference workloads. The power requirements of large language models are orders of magnitude greater than traditional enterprise computing, and that demand is accelerating, not decelerating.

Data centers are only part of the picture. The electrification of transportation, industrial processes, and domestic manufacturing reshoring are simultaneously straining the grid, stacking new load onto a system that, in many regions, has seen little net dispatchable capacity added in a decade. Grid operators are now projecting sustained reserve margin tightening that they have not seen in a generation.

Growth in renewable energy cannot solve this by itself. Wind and solar remain intermittent; battery storage currently provides hours of backup, not continuous reliability. When the grid needs power, a gas plant is what gets called. That operational reality, somewhat minimized in policy discussions, is now impossible to ignore.

Why the U.S. Has a Structural Edge

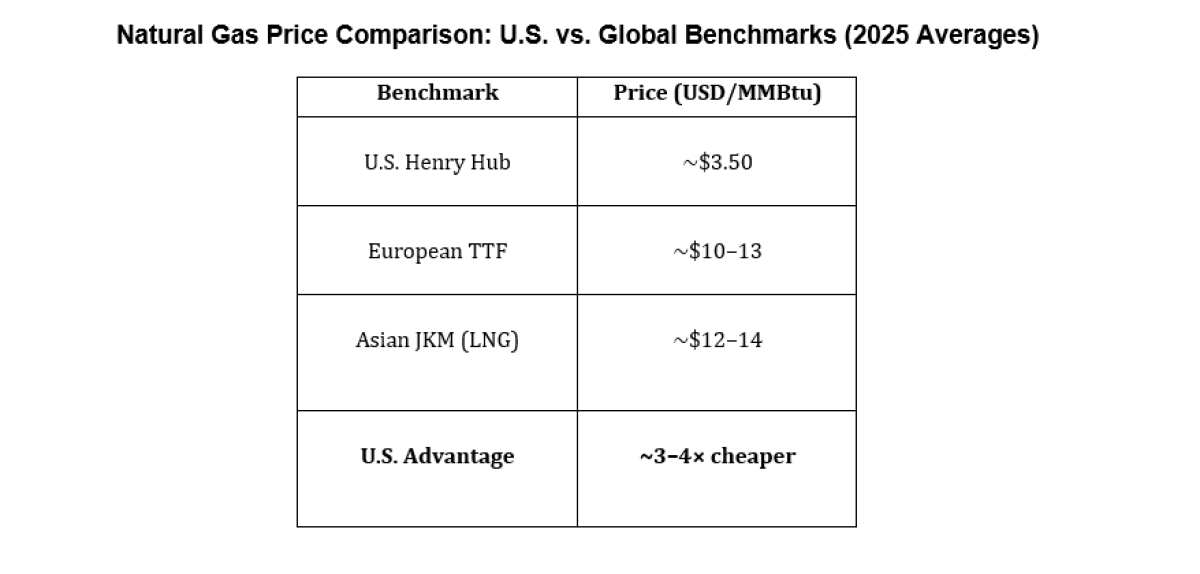

A key feature of this moment is the cost advantage of American natural gas. Domestic production is forecast to reach record highs of 120–122 billion cubic feet per day through 2026–2027, keeping U.S. gas prices structurally below European and Asian import benchmarks. For gas-fired generators, feedstock cost is the primary variable expense; a well-positioned U.S. plant benefits from proximity to abundant, low-cost supply. This advantage has been reinforced by recent conflicts in the Ukraine and the Middle East, which puts further pressure on global import prices.

How Capital Markets Have Responded

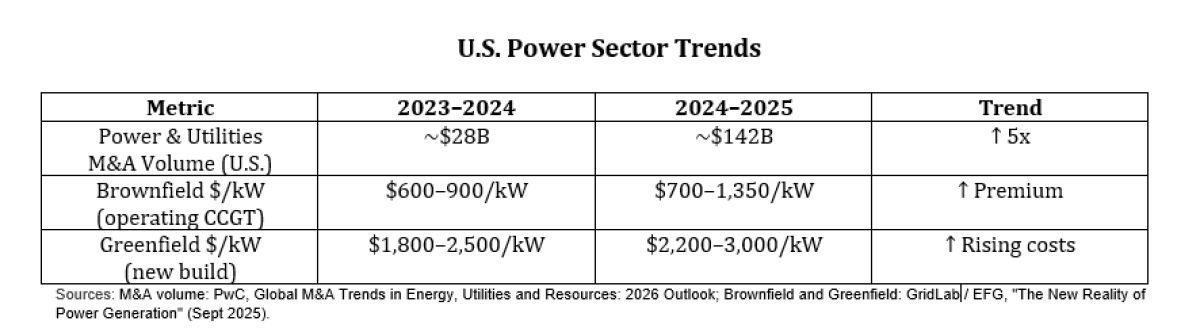

Investors have moved fast. Energy sector M&A activity totaled nearly $142 billion in the twelve months ending November 2025, up from under $28 billion in the prior year. Deal multiples have expanded sharply, with recent private market transactions clearing at 7–8+x EV/EBITDA. The Constellation acquisition of Calpine, at $26.6 billion total, is the largest private power transaction in U.S. history.

Yet valuations remain below replacement costs. New greenfield CCGT construction runs $2,200–$3,000 per kilowatt while operating brownfield assets are trading at $700–$1,350 per kilowatt. That discount provides meaningful margin of safety and reflects a hard structural reality: there is no rapid fix through new construction given interconnection backlogs, permitting timelines that stretch years, and gas turbine delivery queues extending to 2030.

Different Risk Profiles

For investors, the choice between acquiring operating plants and building new ones represents a risk question.

Brownfield acquisitions dominate deal activity for good reasons. Operating plants generate cashflows from day one, carry established grid connections, and offer operating histories that support rigorous underwriting. Key risks such as future power prices and exposure to regulatory changes are analytically forecastable, even if uncertain.

Greenfield development is more complex: multi-year permitting, interconnection delays, and equipment scarcity compound execution risk. What can make this opportunity more compelling is when developers can pre-sell capacity under long-term contracts before starting construction. A leading opportunity in this vein is data center co-location, where new generation is built adjacent to a hyperscaler's facility and contracted directly to provide dedicated, behind-the-meter power.

The Opportunity

For institutional allocators, this moment offers a large, liquid sector which offers differing risk profiles and has been repricing in real time. The question is not whether gas generation is attractive in principle, as its supply / demand / pricing fundamentals appear durable. U.S. gas generation has gone from boom, to bust, now back to boom. The Thermal Renaissance is here.

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/