Authored by Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP

“I signed up for my 401k, but I don’t think I can run that far”

Including private assets in 401(k) plans has been an ongoing debate, one that heated up at beginning of the global pandemic in the United States after Pantheon and Partners Group co-authored an Information Letter to the Department of Labor in June 2020 arguing for private equity’s inclusion to fund lineups. Since then, the discussion around the suitability and challenges of integration of asset classes like private equity, credit, real estate, and infrastructure have brought strong proponents and detractors. Even today, strong opinions on including private markets still pop up, particularly negative (and, in my opinion, only partially correct) ones—see here and here.

In this edition of Chronicles of an Allocator, I will summarize some of the big arguments for and against including private investments in defined contribution schemes and finish with what I think is a path forward.

Just How Big is the 401(k) Space?

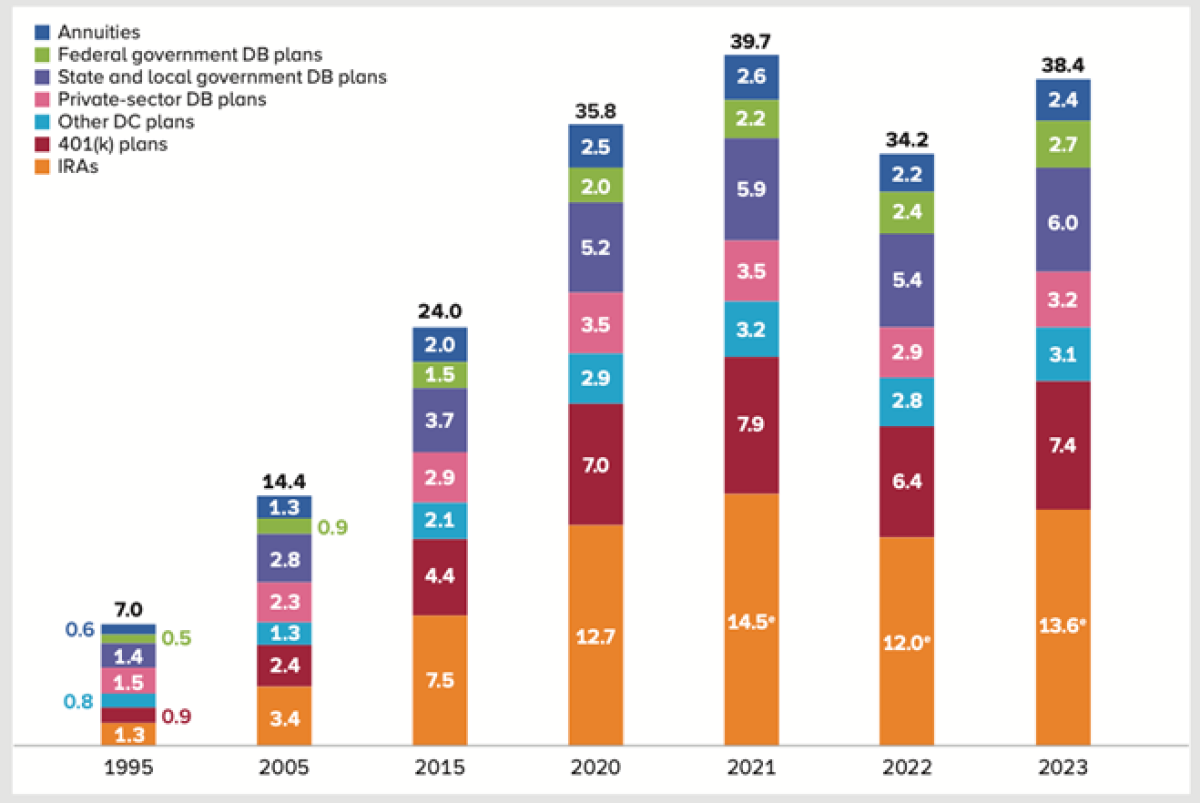

According to the Investment Company Institute (ICI), $38 trillion in assets is held in some form of a retirement plan in the United States as of 2023. Approximately two-thirds of these are held in 401(k), IRA, or other DC plan (see figure 1). Nearly $12 trillion of these retirement savings vehicles are dedicated to some form of an employer-sponsored retirement plan (401(k), 403(b), 457 Plans, TSPs, etc.).

Figure 1: Retirement Plan Assets in the United States

Source: Investment Company Institute

In This Corner … The Proponents.

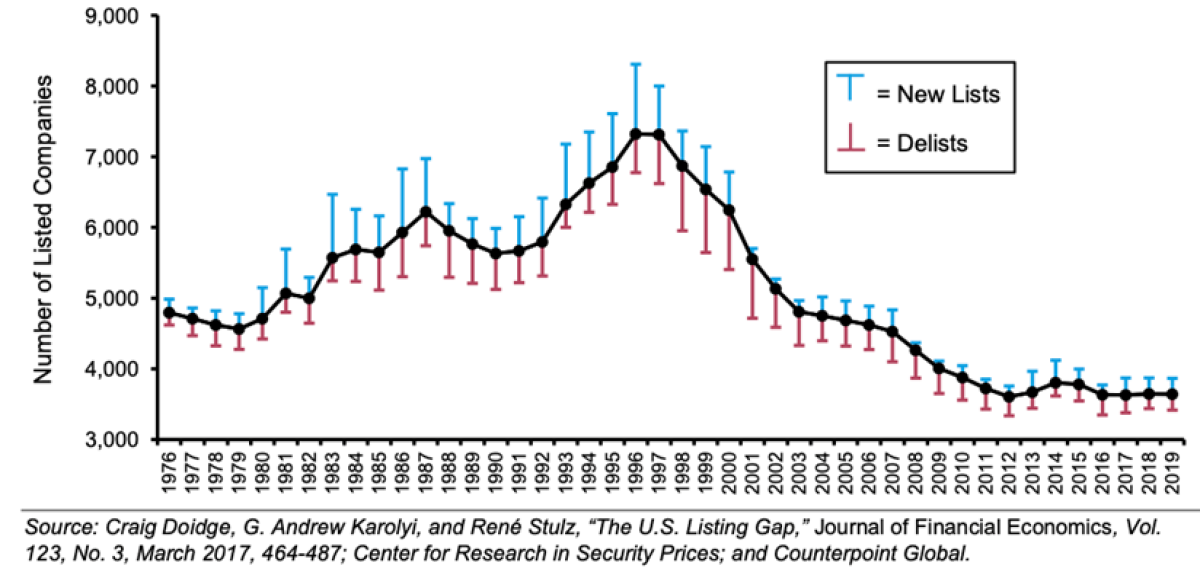

The first argument for including alternative investments, in particular private assets, in these plans is that it better allows everyday retirement savers to access the increasingly significant parts of the economy that are not accessible through the public stock market. The chart from Counterpoint Global (figure 2) illustrates the decline in publicly-traded companies in the United States since the mid-70s. As shown, after a peak in the mid-90s and the burst of the tech bubble, the number of publicly traded stocks declined significantly.

Figure 2: Additions and Subtractions to U.S. Listed Companies, 1976-2019

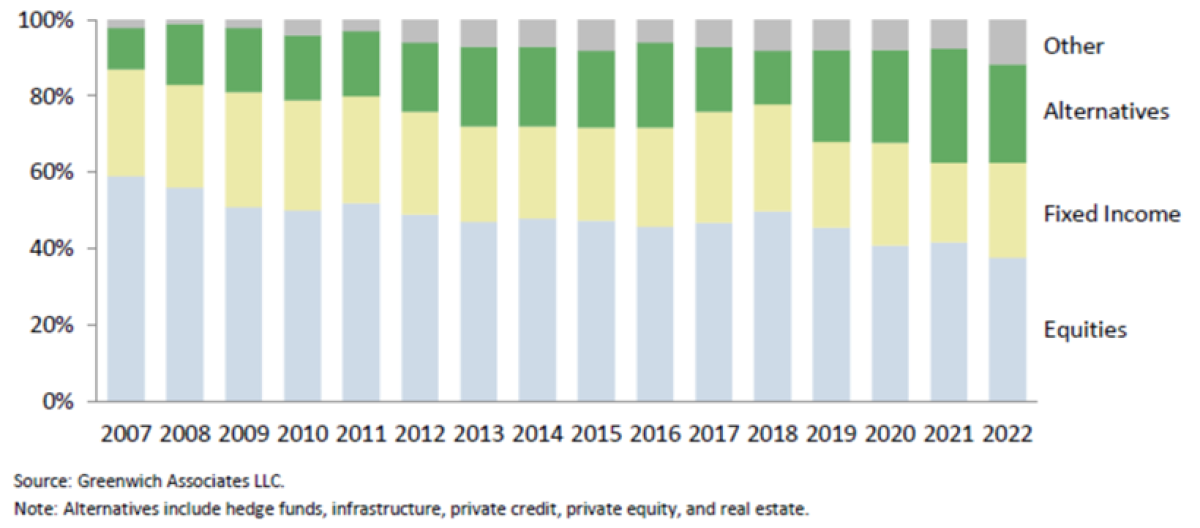

For defined benefit plans, shifts in capital formation are important but less of an issue given their access to a broader opportunity set. Further, many DB plans were forced to diversify as interest rates hit record lows throughout the 2010s (see figure 3). However, defined contribution plan participants have experienced these same shifts with little changes in their investment universe. In other words, participants are “product-takers,” and the products are no longer comprehensive! Another checkmark in the pro-alts column!

Figure 3: Alternative Allocations Across US Public Plans, 2007 - 2022

The other common argument in favor of integrating alternative investments into defined contribution plans is the benefits they bring to the overall portfolio. Once again, this argument isn’t specific to the DC space, but it’s seemingly fallen on deaf ears at the plan sponsor and regulatory level.

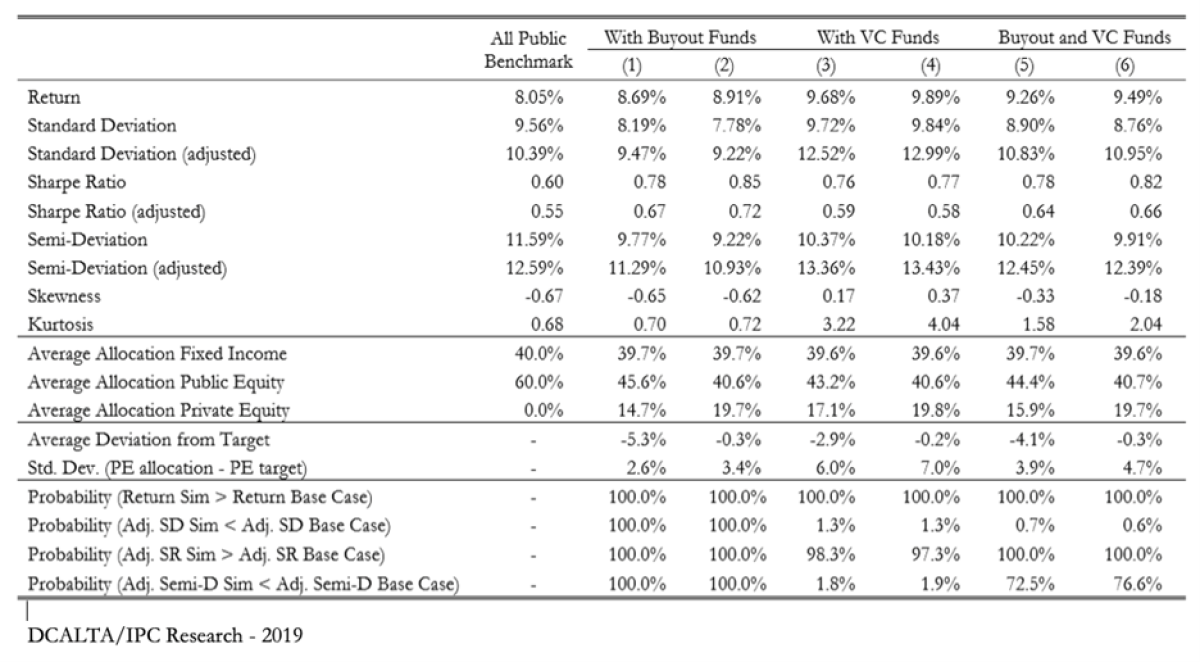

The big difference between the DC space and institutional, or even individual investors, is that participants have varying degrees of sophistication. Further, plan sponsors are not typically investment professionals—so selecting the right funds is a challenge. However, a few years ago, a joint paper between the Institute for Private Capital (IPC) and Defined Contribution Alternatives Association (DCALTA) took on the challenge of determining the viability of integrating private markets (i.e., PE and VC) into a public-only portfolio, incorporating the reality that dispersion exists. The point was to show the likelihood of positive incremental performance, using simulations that randomly selected groups of funds. An excerpt from their results are shown in figure 4:

Figure 4: Asset Allocations with and without Alternative Investments

“…we calculate[d] the percentage of the private fund portfolio simulations that are better than the public-only benchmark… In 100% of simulations, the returns with private funds outperform the public-only benchmark. This suggest that despite the wide dispersion of returns in private funds, the ability to diversify by investing in multiple funds is sufficient to have nearly guaranteed superior returns historically.”

Of course, we want to be better than random, which I’ll address below.

And In this Corner … The Detractors.

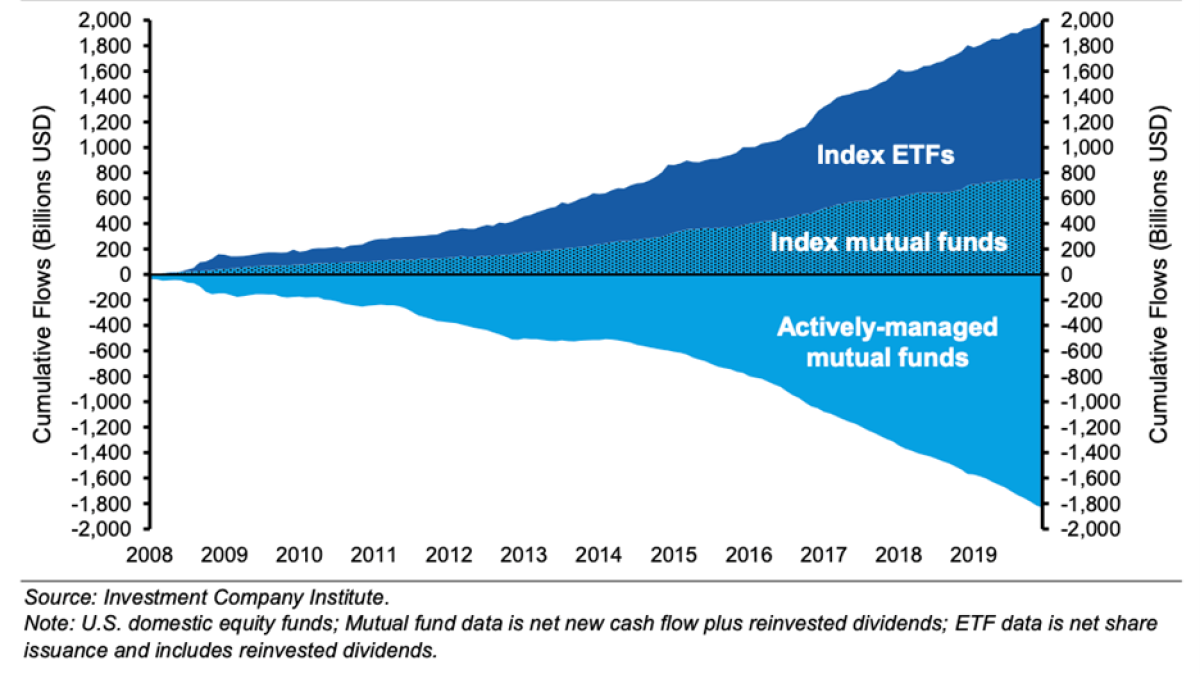

One of the biggest detractors of alternative investments relative to traditional investments are the fees being charged. While all investors are generally fee-sensitive, plan sponsors in the defined contribution space are even more fee-sensitive. In fact, according to ICI, the asset-weighted average expense ratio for equity mutual funds in 401(k) plans was 0.77% in 2000 ... twenty years later, that same average dropped to 0.39%, which falls even below the broader industry asset-weighted average of 0.52%.

Figure 5: Cumulative Flows from U.S. Active to Passive Funds, 2008 - 2019

What’s driving fee compression? Growth of assets, economies of scale, and industry-wide competitive pressures as assets move into index funds. Not to mention a strong fiduciary culture (or a fear of being sued) that’s driven by the Department of Labor. So, it’s no wonder that detractors balk at the traditional 2-and-20 model.

The second argument against integrating alternatives into 401(k) plans is that participants are not sophisticated investors and therefore may not make prudent investment decisions on their own. After all, alternative investments are complex and have historically been hired by professional investors at the institutional level. Putting aside the fact that performance dispersion is far wider in alts than in traditional markets, a common worry is that participants may not fully understand the risks and other considerations, like illiquidity.

The third argument, and one that is highly correlated to the previous two, are legal concerns. There’s a long history of class action lawsuits against plan sponsors as the 401(k) market has grown, particularly focused on fees—in fact, over 50% of plans with assets over $1 billion have been sued for “excessive fees” alone. By introducing higher-cost funds with a higher probability of disappointing returns, sponsors have a strong case against inclusion, simply by pulling the litigation card given legal precedent now demands prioritizing lowest fee options

In my opinion …

From my perspective, plan sponsors are between a rock and a hard place. There’s so much red tape and regulation around the delivery of qualified defined contribution plans, that I understand why there’s hesitancy to buck the trend of low-cost, indexed, public market products on the plan menu. All else equal, lower fees are better for the participant, of course, but there’s a lot of work to be done on re-orienting sponsors (and lawyers) around “net of fee” returns. On the other hand, I think there’s a lot of truth and merit to the access and investment cases presented by proponents. The reality is these are not markets you can ignore, and we should be finding a way to give individuals better access to all parts of the economy.

Further, the structure of the defined contribution plan is probably one of the best mechanisms to utilize longer-dated, more illiquid investments. Young participants have multiple decades before they’ll ever touch their hard-earned savings, and participants across all ages are typically “set it and forget it” investors. Target date funds represent about 60% of 401(k) assets and anecdotal and empirical evidence shows that these types of investors hardly ever touch their portfolio!

Speaking of target date funds, this is the opportunity. I agree with those who say that everyday DC-style plan participants are not sophisticated enough to select these funds on their own. When it comes to alts integration, I don’t believe we should start with the “do it yourselfers.” Instead, focus on building up capabilities in target date funds—they’re managed by sophisticated firms that have access and scale, and the majority of plan participants are already in them!

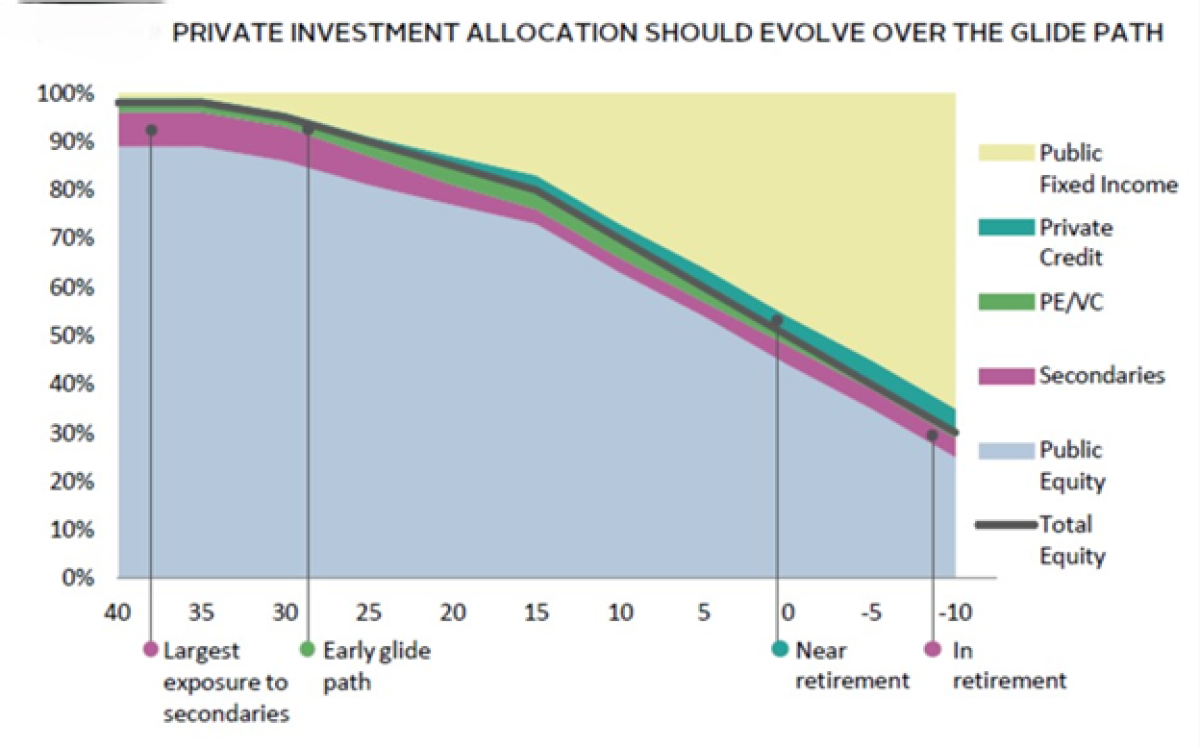

Figure 6: Private Investment Allocation Should Evolve Over the Glidepath (Hypothetical)

Source: Cambridge Associates

Cambridge Associates goes a step further (figure 6) and provides a hypothetical glidepath for a target fund that includes private investments, arguing that these funds should utilize secondaries funds for buyout and venture exposure and private credit funds on the fixed income side. This approach, in their view, would balance illiquidity with additive performance.

Ultimately, we really need a Superannuation Fund and all of our problems would be solved … right?

If you find this topic interesting, check out the following:

Capital Decanted: The Democratization of Alternative Investments

PGIM: The Evolving Defined Contribution Landscape Series

MIT: How Target Date Funds Impact Investor Behavior