Natixis Global Asset Management has released the results of a survey of 500 institutional investors, asking them their views on prospects for 2017.

The surveyed institutions expect that political and economic developments could cause an increase in volatility in the year to come, and active managers have to reset their portfolios with that thought in mind.

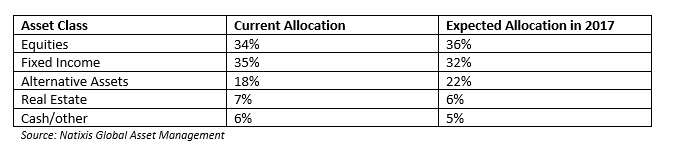

As the table indicates, portfolio shuffling will work send more assets to alternatives managers, and to equities, at the expense of other asset classes.

Part of that re-setting involves a greater emphasis on the emerging market nations, and especially on equity there. Among stocks, 37% of those surveyed said EM equities will be the biggest gainers of 2017.

Cumming and Zhang

This summer, two scholars associated with York University in the UK posted online two fascinating discussions of “alternative investments in emerging markets,” that expand upon Natixis’ point.

Actually, what Douglas J. Cumming and Yelin Zhang were engaged in one of these articles was meta-scholarship, rather than the first-order thing. It was a review of recent works on AI in EM, highlighting the trends.

There are five big themes in recent scholarship on the subject, they find: the importance of information asymmetries (investors acquiring alpha by virtue of local knowledge otherwise unexploited); the importance of due diligence and governance; the diversification benefit of both AI and EM is intensified when one considers the benefit of AI in EM; the pronounced role of country-specific conditions such as culture or politics, and lastly; the lack of data representativeness across studies, or in other words the extreme segmentation of this body of scholarship.

Cumming and Zhang focus a good deal of attention on crowdfunding as a way of facilitating investment in emerging markets; they call this “one of the fasted growing research areas in recent years. “ This is one example of a field where cross-study comparability is very important, yet very challenging, because the phenomena in any one country will depends quite heavily on that country’s legal system and cultural idiosyncrasies. They suggest that future researchers might want to compare the growth of equity crowdfunding to initial public offerings.

Hedge Funds

Around the turn of the millennium, Cumming and Zhang say, scholars started noticing that hedge funds could do quite well in emerging markets if they had a local presence, which presumably assists in taking advantage of local knowledge and thus of an asymmetry thereof.

More recently, scholarship has turned to the ways local regulations affect the performance of hedge funds, so that for example a study in 2013 showed that “restrictions on location of key service providers and wrapper distributions tend to be associated with worse performance, lower fund flows, less sensitive fund flows relative to past performance, and more frequent misreporting of monthly returns.”

Angel Investors

In another of their collaborations this summer, Cumming and Zhang took off the “meta” gloves and engaged in their own first-order study of emerging markets, in a piece entitled “Angel Investors Around the World.” Angel investors, as they define the term, are distinct from both PE and VC funds. Angels are high-net worth individuals who invest their own money in small high-growth entrepreneurial firms in exchange for equity, without institutional intervention.

Unfortunately, there are great gaps in the availability of data on the outcomes of this practice. Angels are not subject to the reporting requirements of venture capital or private equity firms, and though they do form associations, those associations don’t have traditions of systemic data collection. Pitchbook has a lot of data, but it wasn’t culled in a way designed to assist comparisons across countries.

But the data so far as it goes tends to show that the institutions that mediate investment capital justify their existence. Firms financed by angels are less likely to find a successful ‘exit’ either via an IPO or via a merger than are firms funded by PE or VC operations.