By Randy I. Anderson, Ph.D., CRE Chief Executive Officer Griffin Capital Asset Management Company, LLC/Apollo.

What Is an Interval Fund?

Interval funds are professionally managed, pooled investment vehicles that combine attractive features of both closed-end funds and traditional open-end funds.

Open-end funds pool money from many investors and invest in a portfolio of securities, such as stocks and bonds, that is designed for a specific investment objective. Ownership of the portfolio is available to the public through shares that can be purchased or sold, hence the name “open-end.”

Closed-end funds also pool money, however, they do not typically redeem shares at the option of the shareholder. Rather, closed-end fund shares usually trade on the secondary market. This structure provides asset managers with a stable amount of capital to invest in less liquid markets, such as real estate, venture capital, and structured credit.

Interval funds share characteristics of both closed-end and open-end funds. They offer limited liquidity to shareholders by offering to

repurchase a limited amount of the shares at certain “intervals,” typically every three months. Investors can purchase shares at any time, though, just like they would in an open-end fund.

Interval Funds Offer Access

Interval funds provide individual investors access to a diversified portfolio of public and private securities. While interval funds offer many of the benefits of an open-end fund, the benefit that sets them apart is the ability to allocate more than 15% of their portfolio to private securities—a strategy institutional investors have utilized for years to:

- Help reduce volatility.

- Potentially increase income.

- Lower correlation to the public markets.

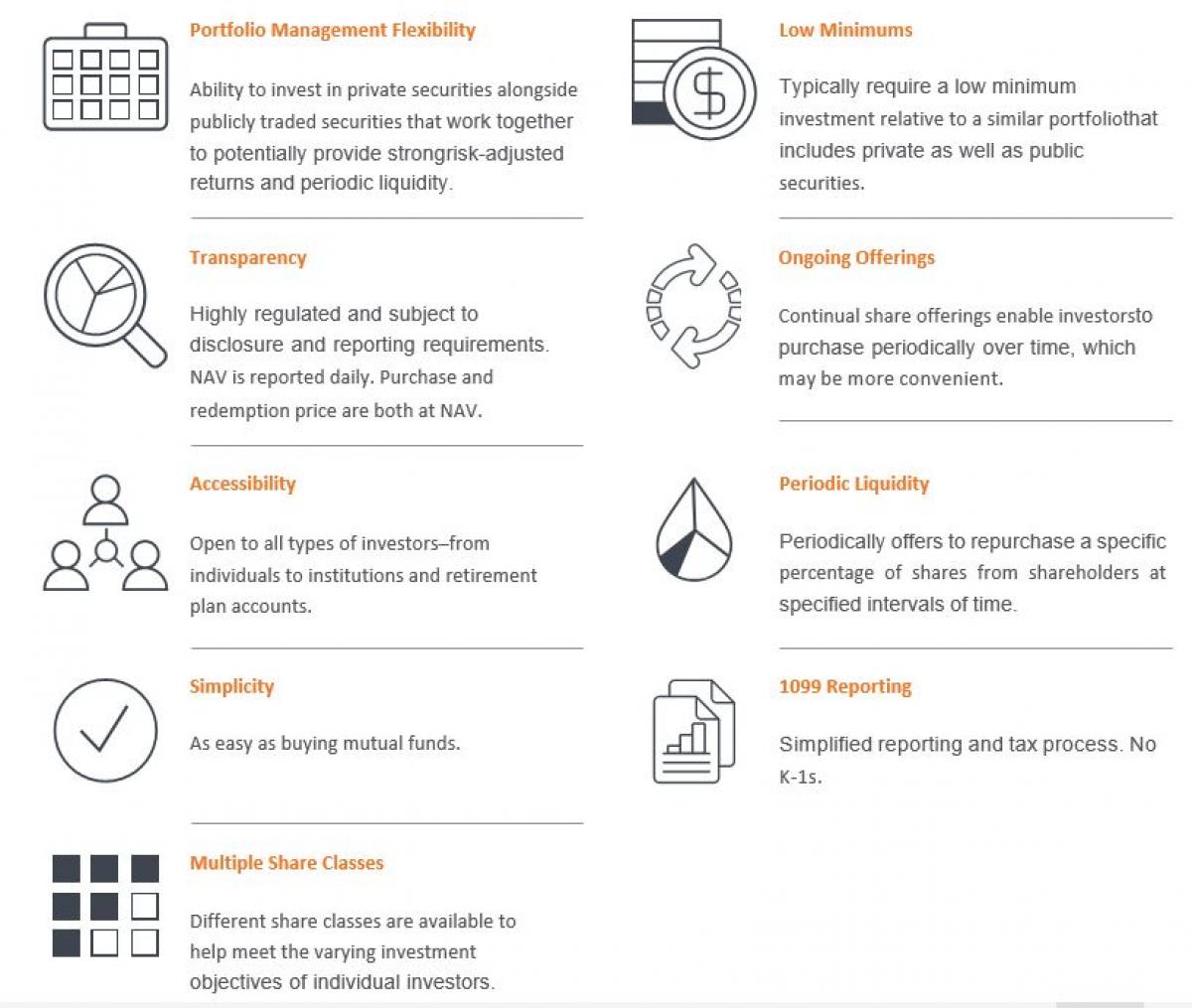

Attractive Features of Interval Funds

Interval funds provide many of the key features of both closed-end funds and open-end funds including:

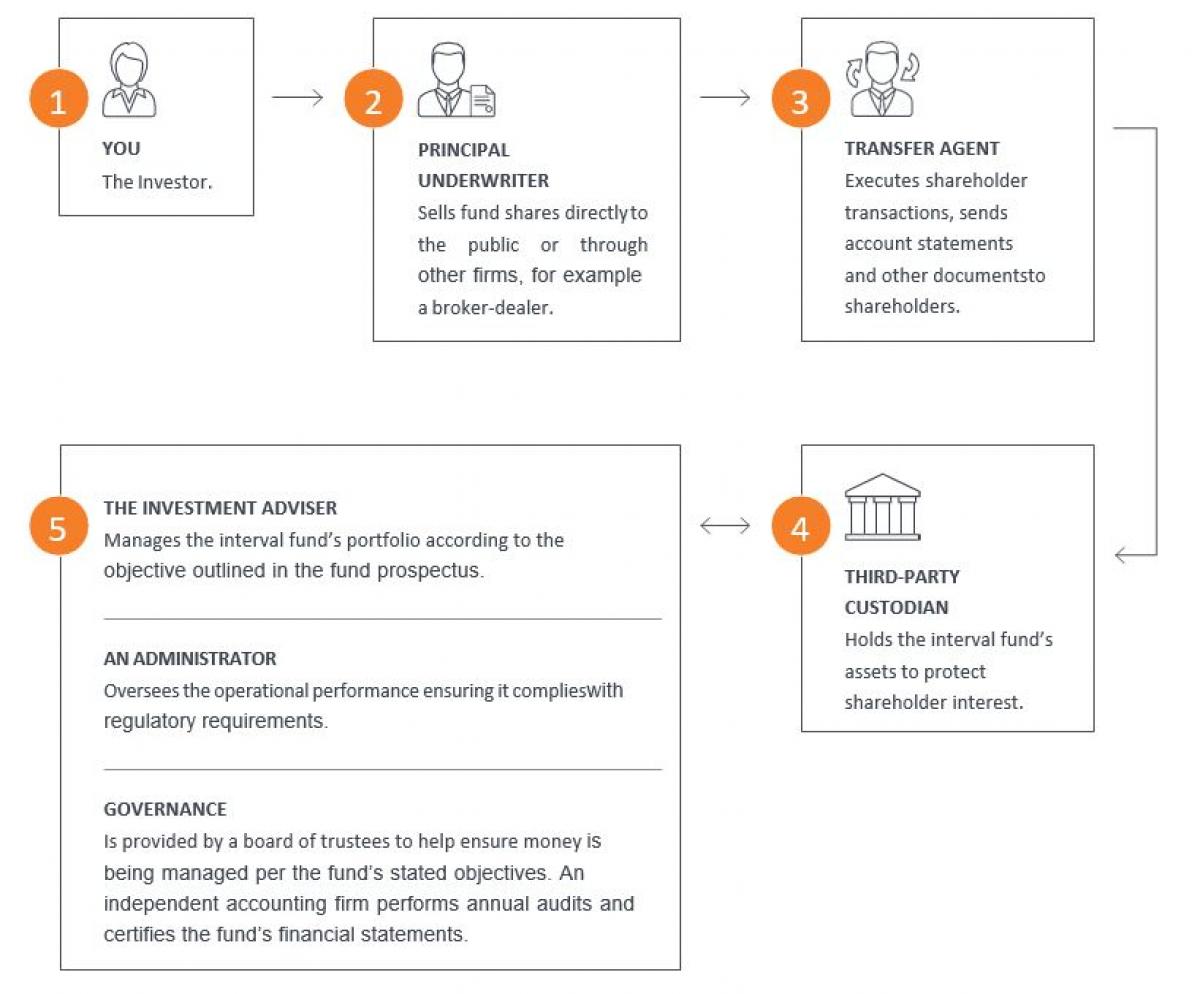

How Interval Funds Operate

![]() The Securities and Exchange Commission (SEC) is the primary regulator of investment companies, including interval funds. Interval funds are regulated by the SEC mainly pursuant to the rules adopted under the Investment Company Act of 1940, as amended.

The Securities and Exchange Commission (SEC) is the primary regulator of investment companies, including interval funds. Interval funds are regulated by the SEC mainly pursuant to the rules adopted under the Investment Company Act of 1940, as amended.

Although all interval funds share this basic framework, not all interval funds are created equal. Different funds may have different investment objectives and underlying securities. Some key items to consider include:

STRENGTH OF THE INVESTMENT ADVISER

Research the fund’s investment adviser to determine their strength and reputation. It may be helpful to consider assets they have under management (AUM), experience in the interval funds market, and the overall performance of the interval fund.

SELECTION OF SUB-ADVISERS

Investment advisers that manage interval funds may engage sub-advisers to assist in managing the portfolio. Sub-advisers may provide additional investment expertise as it relates to the interval fund’s portfolio.

Review the selection of sub-advisers the same way you would the strength of the investment adviser. Highly reputable sub-advisers add value that may potentially allow for strong risk-adjusted returns.

QUALITY OF INVESTMENTS AND STRATEGIES

Some interval funds take an institutional approach to portfolio management and adapt it for the unique needs of the individual investor. This approach helps ensure access to higher-quality assets with skilled managers, who have the expertise to select effective investments and implement a cohesive strategy.

VIDEO: https://www.griffincapital.com/investor-education/understanding-interval-funds-video/

Key Terms for Performance Measurement

The following terms may be helpful when gauging the performance of an interval fund.

| Alpha | Alpha is a measure of risk-adjusted return implying how much a fund/manager outperformed its benchmark, given its risk profile. |

| Annualized Return | Annualized return is calculated by annualizing a fund’s cumulative return (i.e., adjusting it for a period of one year). The annualized return includes capital appreciation and assumes reinvestment of dividends and distributions. |

| Beta | Beta is a measure of systematic risk (volatility), or the sensitivity of a fund to movements in a benchmark. A beta of 1 implies that you can expect the movement of a fund’s return series to match that of the benchmark used to measure beta. A value of less than 1.0 implies that the fund is less volatile than the benchmark, and a value greater than 1.0 implies that the fund is more volatile than the benchmark. |

| Correlation | A statistical measure of how two securities move in relation to each other. A correlation ranges from -1 to 1. A positive correlation close to 1 implies that as one security moves, either up or down, the other security will move in “lockstep,” in the same direction. A negative correlation close to -1 indicates that the securities have moved in the opposite direction. If the correlation is 0, the movements of the securities are said to have no correlation; they are completely random. |

| Cumulative Return | Cumulative return is the compound return of an investment. It includes capital appreciation and assumes reinvestment of dividends and distributions. |

| Sharpe Ratio | The Sharpe ratio measures risk-adjusted returns by calculating the excess return (above the risk-free rate) per unit of risk (standard deviation). The higher the ratio, the better the risk-adjusted returns. |

| Standard Deviation | Standard deviation measures the average deviations of a return series from its mean, and is often used as a measure of volatility/risk. A large standard deviation implies that there have been large swings in the return series of the manager. |

| Total Return | When measuring performance, the actual rate of return of an investment or a pool of investments over a given evaluation period. Total return includes interest, capital gains, dividends, and distributions realized over a given period of time. |

| Yield | The income return on investment. This refers to the interest or dividends received from a security and is usually expressed as an annualized percentage based on the investment’s price. |

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Dr. Anderson serves as Chief Executive Officer of Griffin Capital Asset Management Company and Chief Economist of Griffin Capital Company, LLC/Apollo.

Previously, Dr. Anderson held several senior executive positions at Bluerock Real Estate LLC, including founding partner of the Bluerock Total Income + Real Estate Fund where he was the Portfolio Manager. Prior to Bluerock, Dr. Anderson was a founding partner of Franklin Square Capital Partners, the firm that pioneered the non-traded Business Development Company. Dr. Anderson also served as the Chief Economist and a Division President for CNL Real Estate Advisors, as the Chief Economist and Director of Research for the Marcus and Millichap Company where he served on the Investment Committee, and as Vice President of Research at Prudential Real Estate Advisors. Dr. Anderson also served as the Howard Phillips Eminent Scholar Chair and Professor of Real Estate at the University of Central Florida where he directed the research and education institute.

Dr. Anderson was the former editor of the Journal of Real Estate Portfolio Management; was awarded the Counselors of Real Estate designation, named a Kinnard Young Scholar by the American Real Estate Society, and named both a NAIOP Research Foundation Distinguished Fellow and a Homer Hoyt Institute Fellow. Dr. Anderson is also known for sharing his macroeconomic insights at investment industry events and in the media. He has provided economic commentary for prominent financial news outlets, most notably Bloomberg Radio, CNBC, TheStreet, and Fox Business News. Dr. Anderson has also been quoted in articles featured in Financial Advisor Magazine, GlobeSt. com, and National Real Estate Investor.

THIS IS NEITHER AN OFFER TO SELL NOR A SOLICITATION OF AN OFFER TO BUY ANY SECURITIES. AN OFFERING IS MADE ONLY BY A PROSPECTUS. THIS LITERATURE MUST BE READ IN CONJUNCTION WITH A PROSPECTUS IN ORDER TO UNDERSTAND FULLY ALL OF THE IMPLICATIONS AND RISKS OF SECURITIES TO WHICH IT RELATES. A COPY OF A PROSPECTUS MUST BE MADE AVAILABLE TO YOU IN CONNECTION WITH AN OFFERING.