By Stephen L. Nesbitt – Chief Executive Officer, Chief Investment Officer of Cliffwater.

In the 1980s buyout critics railed on the risk to businesses from barbarians piling debt on companies to secure control. Abuses occurred but the buyout industry largely transformed to one where operating acumen replaced financial legerdemain. And for over two decades leverage ceased as major topic of discussion among private equity investors. That is changing. Newer forms of leverage are not at the portfolio company but at the fund level, introducing a third-party into the GP-LP relationship. Some are less concerning, like commitment lines that provide administrative convenience. But even these can be abused. Others are less understood and may not be desirable for all investors. Transparency and controls on these new forms of leverage are likely ahead, which may be a good thing.

Sources of Leverage

Historically, few private asset fund managers used fund-level leverage. Private asset strategies such as private credit utilize fund-level leverage but generally provide limited partners the option of a unlevered or levered structure. Over the past ten years, private equity and other private asset funds have introduced fund-level leverage with the use of capital call facilities or commitment credit lines. These facilities were typically used for a short-term period to bridge the period between closing a transaction and issuing a capital call to limited partners. In recent years, general partners have taken advantage of the low interest environment and lenders have expanded their business offerings for fund- level leverage. As a result of expansion of the fund-level leverage industry, the Institutional Limited Partners Association (“ILPA”) released guidelines in 2017 and 2020 regarding the use of such leverage and best practices for transparent reporting.

Types of fund-level leverage are as follows.

- Capital Call Facility. A term loan guaranteed by the aggregate fund commitments. The facility can be priced at approximately LIBOR plus 150 basis points and sized at a percentage of aggregate fund commitments. Some managers pay down the facility every six months while others leave it outstanding for two years or longer. The average time outstanding ranges from six months to one year. The capital call facility is typically put in place at a fund’s inception and utilized in the initial years of the fund.

- NAV-Linked Facility. Term loan secured by the underlying net asset value of the fund, excluding underperforming companies and impaired assets. A NAV-linked facility has been proposed in situations where a fund is past its investment period and has limited or no unfunded capital available to support active portfolio companies. The cost of NAV-linked leverage is higher than a capital call facility and the General Partner is incentivized to retire the facility as soon as possible given the higher cost.

- Distribution Facility. A term loan and sometimes paired with a delayed draw facility secured by the fund assets. The point of this fund-level leverage is to make a distribution of cash proceeds to limited partners and increase the fund IRR. Distribution facilities are higher cost than capital call facilities so the interest expense lowers the cash-on-cash return for limited partners. Fewer data points exist but the cost is in between a NAV-linked facility and a capital call facility.

Impact on Performance

The use of a fund subscription line enhances IRR performance at the expense of investors’ cash on cash return (TVPI or total value to paid-in capital). The negative impact on TVPI is amplified when a general partner earns its carried interest on a deal-by-deal basis and after meeting a stated preferred return because the subscription line allows the general partner to achieve the stated preferred return sooner.

While the cost of subscription lines is generally perceived to be low, the cost is not zero and limited partners are paying the expense. For tax-exempt investors, UBTI may be created when subscription lines are used for one year or longer. The following examples illustrate the impact of fund-level leverage.

Capital call facility

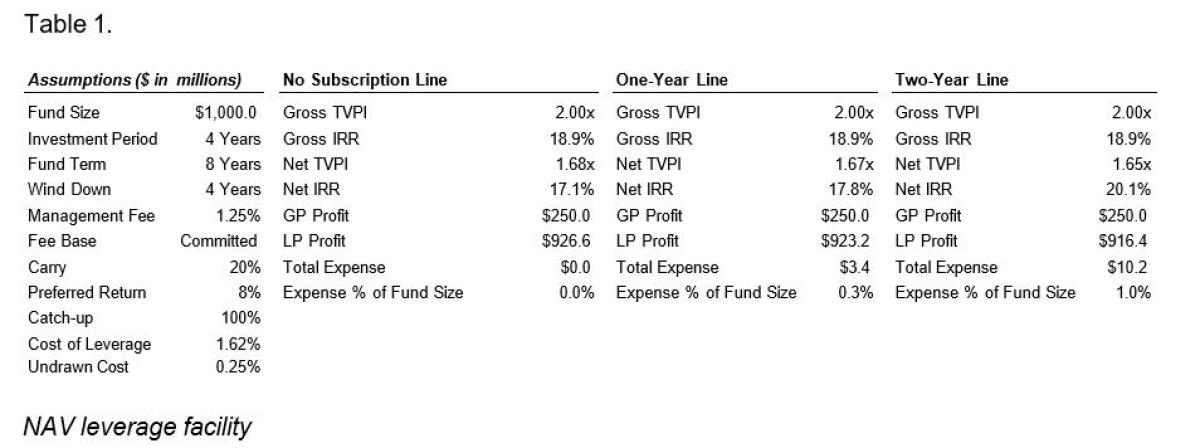

In Table 1, Cliffwater has modeled a sample capital call facility, which is utilized during the first few years of a fund’s life in order to maximize net IRR by delaying drawdowns. As shown below, utilization of the facility enhances fund net IRR; however, the cost of this performance enhancement is borne by limited partners and negatively impacts total LP profit. Leverage is relatively inexpensive for capital call facilities, given that these facilities are typically secured by future fund capital calls and benefit from the current low interest rate environment. These facilities tend to represent a much larger size relative to NAV leverage facilities and distribution facilities and are generally sized up to 25% of total fund commitments. In some cases, the facilities are larger, equal to 50% of aggregate fund commitments.

In Table 2, Cliffwater has modeled a sample NAV-based leverage facility, which may be utilized by a general partner that is seeking to invest further capital into a portfolio without the use of capital calls. Facilities such as the one described are often utilized by funds that lack adequate reserves, as well as funds that are later in their fund life and are seeking to invest further capital in the portfolio without the use of capital calls. NAV leverage facilities typically utilize more expensive leverage and have a higher degree of variability in debt pricing given that these facilities are loans secured by the unrealized portfolio of a fund, or a portion of the unrealized portfolio of a fund. These facilities are typically smaller in size relative to capital call facilities given that they are often used to support add-on acquisitions and capital deployment for a fund rather than to complete new platform investments. These NAV leverage facilities typically utilize a low LTV in order to limit the pricing of fund-level leverage. Unlike a capital call facility described above, NAV leverage facilities are not primarily utilized to enhance net IRR, but rather, to substitute capital calls or further equity injections. The expenses borne by limited partners will vary based upon the size of the facility utilized and the pricing of leverage.

Table 2.

In Table 3 below, Cliffwater has modeled a sample NAV-based leverage facility, which may be utilized by a general partner to provide distributions to limited partners prior to actual fund realizations. These facilities have been less commonly utilized relative to the two facilities described in Table 1 and Table

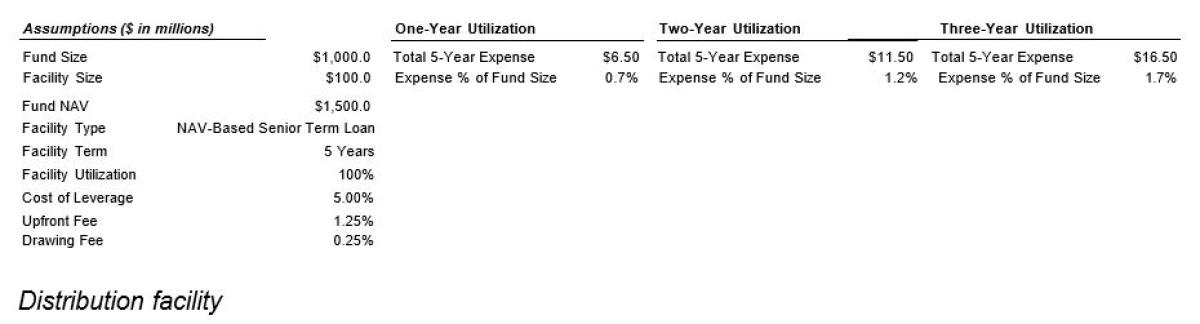

2. A distribution facility is typically utilized by a general partner to provide limited partners with liquidity in market environments of relatively inexpensive leverage. A distribution facility is very similar to an NAV-leverage facility described in Table 2 and will often be structured as an NAV-based term loan; however, the proceeds of capital will be utilized to distribute capital immediately to limited partners, rather than utilized for portfolio investment. Pricing for a distribution facility varies more widely than a traditional capital call facility, and will depend upon the structure of the loan, if the loan is secured by any uncalled capital from the fund, and the quality and health of the active portfolio. A distribution facility is primarily utilized to enhance DPI and will typically have a more modest impact on net IRR relative to a capital call facility given the timing of the utilization of the facility. A distribution facility adds greater risk as the general partner may ultimately need to sell assets at a sub-optimal time or draw down unfunded commitments to pay back the leverage facility. Cliffwater strongly discourages managers from utilizing fund-level leverage to make cash distributions to limited partners.

Table 3.

Transparency

Managers should increase transparency to limited partners by providing greater notice of upcoming capital calls. Cliffwater recommends that general partners take advantage of the opportunity to provide limited partners with a capital call schedule if a leveraged facility is being used to aggregate capital calls. The following information should be disclosed in quarterly reporting to limited partners:

- disclosure of the balance and percent of total outstanding uncalled capital,

- the number of days outstanding of each drawdown,

- the use of proceeds from fund-level leverage facilities,

- the levered and unlevered net IRR,

- the terms of the leverage facility and costs to the fund (interest and fees).

Cliffwater supports the ILPA recommendations, which include guidance as to how general partners should incorporate detailed information in quarterly and annual reporting and that the size of a capital call facility be capped at an amount equal to 25% of aggregate fund commitments.

Legal Considerations

In addition to the legal risks inherent in taking on fund-level leverage, the lender’s consent may be required for certain amendments to a fund’s limited partnership agreement. This required consent introduces a third party into the general partner / limited partner relationship and therefore, may reduce the flexibility of the general partner and limited partners in structuring the fund. Lenders may also require limited partners to waive their rights in the event of a limited partner bankruptcy. Lender influence has been less of an issue during the current market environment where leverage is plentiful, however lenders have greater negotiating strength when a fund has underperformed or when a General Partner requires additional capital (beyond fund commitments) to support its portfolio. The potential for lender involvement is greater when the general partner employs a NAV-based facility or a leverage facility to make a cash distribution without selling any companies or assets.

When negotiating a limited partnership agreement for a new private asset vehicle, it is best practice to prohibit a NAV-based leverage facility and loans solely to create cash distributions. Limited partners should advocate for greater notice for capital calls when a fund-level leverage facility is in place as well as stipulate the metrics that managers report with respect to fund-level leverage.

Cash Flow Dynamics

Managers can provide capital call forecasts to limited partners when investing off of a fund-level facility, particularly in the initial years of a fund investment period. As experienced in the second quarter of 2020, a downturn in the capital markets often results in larger capital calls for limited partners. While some private asset fund managers have done a better job of communicating the timing and quantum of future capital calls, there is no market standard. A minority of general partners have utilized fund-level leverage to draw down as much as 50% of limited partner capital commitments without any advance communication.

Cliffwater believes there is room for managers to improve communication to limited partners about how the capital call facility is being used and the implication for future capital calls. At minimum, general partners can provide limited partners with 30 days of notice for a future capital call.

ILPA Guidelines

ILPA published guidelines in 2017 and in 2020. The 2017 guidelines focused on the importance of disclosure to limited partners, appropriate sizing of the facility compared to fund size, and only using a facility so there can be benefits to limited partners (not utilizing leverage facilities to make distributions. Below is a summary of the ILPA guidelines:

- LPAs should include reasonable use thresholds for subscription lines such as maximum use at 15-25% of uncalled capital.

- LPAs should include reasonable term thresholds for subscription lines such as 180 days.

- Quarterly reporting of items such as the size and balance of the facility, impact on LP funded ratio, and impact on performance.

- Annual reporting of items such as counterparty, average maturity, collateral, and financing costs.

- Additional notice time and disclosure of larger than normal capital calls as a result of repaying the subscription line.

Cliffwater concurs with the ILPA guidelines as the transparency and reporting are paramount to understanding how leverage is being employed at the fund level.

Recommendations

- Limited partners evaluate general partner performance on an unlevered basis and encourage transparent quarterly reporting from general partners with appropriate language in the limited partnership agreement.

- General partners should not use subscription lines for more than 180 days and should not use them to make distributions in lieu of selling companies or assets. General Partners should make money the “old-fashioned way” by selling companies and assets.

- Subscription lines should not be used to pay management fees.

- Leverage facilities should only be used during a fund’s investment or commitment period.

Conclusion

In principle, limited partners should have the option of whether to invest in a levered fund vehicle and accept the “extra layer of leverage.” Fund-level credit facilities should be utilized mainly to aggregate capital calls early in a fund’s life. NAV-based leverage facilities can be considered when capital is needed to support the portfolio and undrawn capital commitments are not sufficient. Greater transparency and advance notice of capital calls should be a benefit of fund-level leverage for limited partners.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Steve Nesbitt is the Chief Executive Officer and Chief Investment Officer of Cliffwater, and is primarily responsible for the day-to-day management of Cliffwater Corporate Lending Fund (CCLFX) and the Cliffwater Enhanced Lending Fund (CELFX), an SEC registered credit interval fund focused on the US corporate middle market.

Steve is recognized for a broad range of investment research. His papers have appeared in the Financial Analysts Journal, The Journal of Portfolio Management, The Journal of Applied Corporate Finance, and The Journal of Alternative Investments. His private debt research led to the creation of the Cliffwater BDC Index, measuring historical BDC performance, and the Cliffwater Direct Lending Index, measuring historical performance for direct middle market loans. Steve authored the book, Private Debt: Opportunities in Corporate Direct Lending, Wiley Finance (2019) which provides the analytical and empirical underpinnings of the private debt market.

Stephen L. Nesbitt snesbitt@cliffwater.com

The views expressed herein are the views of Cliffwater LLC (“Cliffwater”) only through the date of this report and are subject to change based on market or other conditions. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Cliffwater has not conducted an independent verification of the information. The information herein may include inaccuracies or typographical errors. Due to various factors, including the inherent possibility of human or mechanical error, the accuracy, completeness, timeliness and correct sequencing of such information and the results obtained from its use are not guaranteed by Cliffwater. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this report. This report is not an advertisement, is being distributed for informational purposes only and should not be considered investment advice, nor shall it be construed as an offer or solicitation of an offer for the purchase or sale of any security. The information we provide does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Cliffwater shall not be responsible for investment decisions, damages, or other losses resulting from the use of the information. Past performance does not guarantee future performance. Future returns are not guaranteed, and a loss of principal may occur. Statements that are nonfactual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Cliffwater is a service mark of Cliffwater LLC.