By Stephen L. Nesbitt – Chief Executive Officer, Chief Investment Officer of Cliffwater.

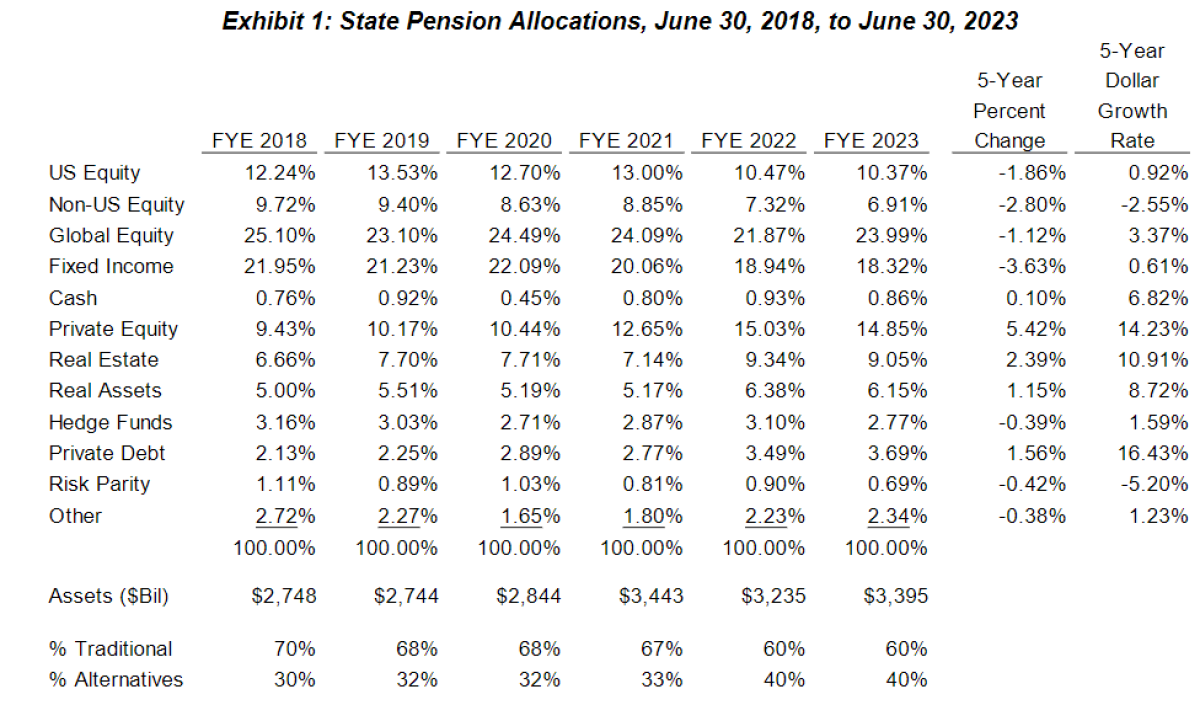

Allocations to alternatives reached 40% of state pension assets in 2022 and remained at that level in 2023.1 While private equity allocations saw the greatest percentage point change (+5.42%), private debt experienced the highest annual growth rate in assets

(+16.43%). However, the current 3.69% allocation to private debt remains well below the 14.85% allocation to private equity, perhaps quieting the “too much money” crowd.

Exhibit 1 details asset-weighted allocations across a closed group of 65 state pension plans with June 30 fiscal years.2 Together, these state pensions represented $3.4 trillion in assets on June 30, 2023.

Key takeaways are:

1. Alternatives grew from 30% to 40% of total assets over the last five years.3

2. Private equity has grown the most, from 9.43% of total assets to 14.85%.

3. Funding for alternatives has come pro rata from public stocks and bonds.

4. Private alternatives are increasingly favored over liquid alternatives, with declining allocations to

hedge funds and risk parity.

5. Alternative allocations may be reaching peak levels for state pensions, with likely future alternative

growth coming from the high-net-worth channel and non-US investors.

6. Recent performance data and allocator capital market expectations suggest that alternative

allocations are likely to remix further, with private equity and private debt growing at the expense

of real estate and liquid alternatives.4

We have shown elsewhere that the growth in alternatives has been materially accretive to state pension

returns, and lowering risk as well.5 We expect allocations to private debt to increase further, either as part

of higher overall alternative allocations or a remix.

Footnotes:

1 The increase in alternatives in 2022 to 40% of assets could have resulted from the “denominator effect” in that fiscal

year. Its sustained level in 2023 suggests a permanent higher allocation to alternatives.

2 This study uses the same group of state pension plans found in annual Cliffwater state pension performance studies.

3 The “Other” category covers allocations to “strategic,” “opportunistic,” and “multi-asset” investments that employ

alternative asset classes or alternative strategies.

4 See Cliffwater Research, Why Private Debt, January 2023 for survey of allocator capital market assumptions.

5 Cliffwater Research, State Pension Performance, 2000-2022 and Private Equity.

About the Author:

Steve Nesbitt is the Chief Executive Officer and Chief Investment Officer of Cliffwater, and is primarily responsible for the day-to-day management of Cliffwater Corporate Lending Fund (CCLFX) and the Cliffwater Enhanced Lending Fund (CELFX), an SEC registered credit interval fund focused on the US corporate middle market.

Steve is recognized for a broad range of investment research. His papers have appeared in the Financial Analysts Journal, The Journal of Portfolio Management, The Journal of Applied Corporate Finance, and The Journal of Alternative Investments. His private debt research led to the creation of the Cliffwater BDC Index, measuring historical BDC performance, and the Cliffwater Direct Lending Index, measuring historical performance for direct middle market loans. Steve authored the book, Private Debt: Opportunities in Corporate Direct Lending, Wiley Finance (2019) which provides the analytical and empirical underpinnings of the private debt market.

Stephen L. Nesbitt snesbitt@cliffwater.com

The views expressed herein are the views of Cliffwater LLC (“Cliffwater”) only through the date of this report and are subject to change based on market or other conditions. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Cliffwater has not conducted an independent verification of the information. The information herein may include inaccuracies or typographical errors. Due to various factors, including the inherent possibility of human or mechanical error, the accuracy, completeness, timeliness and correct sequencing of such information and the results obtained from its use are not guaranteed by Cliffwater. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this report. This report is not an advertisement, is being distributed for informational purposes only and should not be considered investment advice, nor shall it be construed as an offer or solicitation of an offer for the purchase or sale of any security. The information we provide does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Cliffwater shall not be responsible for investment decisions, damages, or other losses resulting from the use of the information. Past performance does not guarantee future performance. Future returns are not guaranteed, and a loss of principal may occur. Statements that are nonfactual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Cliffwater is a service mark of Cliffwater LLC.