By Sean Castillo of Cliffwater.

Continuation funds provide an opportunity for limited partners to remain invested in high performing portfolio companies, post-sale, through a minority stake with the general partner. The attractiveness of these novel funds balances potential further growth at lower fees, on the one hand, with material conflicts vis-à-vis the GP and non- participating LPs and added governance risks associated with being a minority investor.

Background

A continuation fund is created by a general partner for the purpose of acquiring minority equity interests in multiple companies or assets alongside a third-party acquirer. Continuation funds, previously used to provide support equity to poor performing investments, have been repurposed as GPs seek to retain an ownership interest in high performing assets while also providing liquidity to existing fund investors within the construct of a ten-year fund term. Typically, potential LP investors are asked to make a blind pool commitment to a continuation fund.

Potential conflicts of interest

A primary consideration is whether the GP has a strong rationale for pursuing a continuation fund with the ability to address conflicts of interests.

Clear parameters for investment criteria: The general partner should provide clear parameters for continuation fund investments. Investment selection based on specific returns generated by the main fund (e.g., deal must generate above a 2.5x return), strategy (e.g., deal must not be turnaround focused or defensive) or sector (e.g., deal must target software investments) can be effective.

Institutional decision-making process: The general partner should have a formal re-underwriting and investment committee process for investments into the continuation vehicle, particularly given investments are often minority equity interests at market price entry multiples.

Risk of selection bias: There is a potential risk that the general partner may offer inferior opportunities to investors of the continuation vehicle. This is mitigated in part by the GP commitment and carried interest terms of the continuation vehicle. Acquirer deal dynamics could also negatively impact the quality of opportunities available. Acquirers may demand a larger share of equity capital in high conviction investments or seek the continuation vehicle’s investment on deals that are not high conviction.

Key due diligence questions

Investors should factor in due diligence considerations specific to the continuation vehicle model.

Is the general partner maximizing value for its selling buyout fund(s)?

GPs should run a competitive sales process for every exit. Independent third-party buyers or financial intermediaries should set the price independent of the general partner, typically becoming majority investor and negotiating the terms of the transaction.

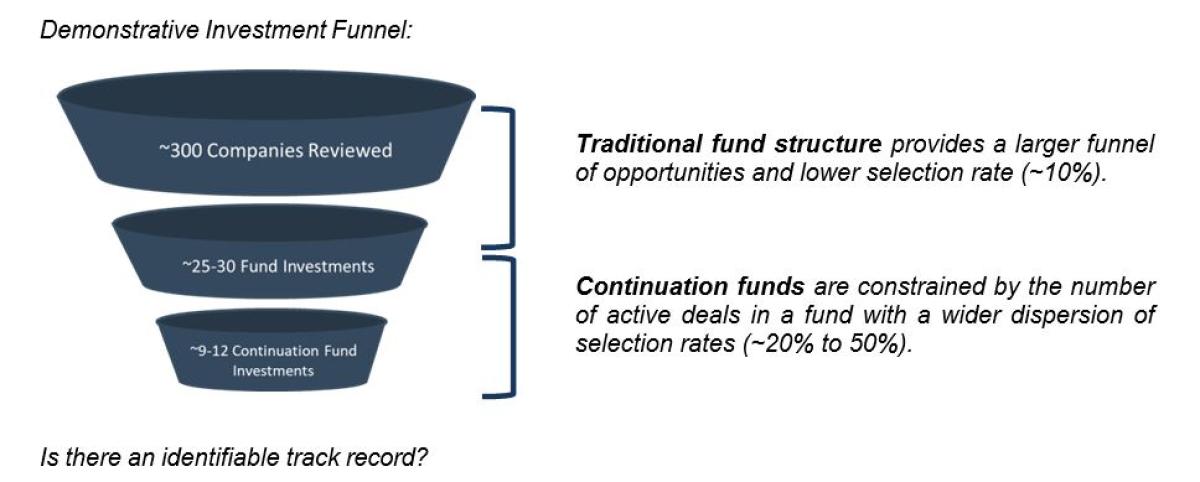

How robust is the opportunity set?

The continuation fund will generally be constrained to invest across active holdings of the GP’s flagship funds. The breadth and quality of the opportunity set can vary across GPs.

The graph below illustrates the opportunity set of deals available to traditional private equity relative to the same GP raising a continuation fund:

Is there an identifiable track record?

The GP should be able to point to a track record of recapitalizations, minority ownership, and/or successful outcomes for third-party buyers that have acquired the firm’s portfolio companies in the past. The firm should demonstrate a history of being able to support company and asset investments from a minority ownership position.

What is the fundamental performance of portfolio companies?

GPs should demonstrate revenue and EBITDA growth as well as other positive key performance metrics during the ownership period. The go-forward investment thesis should include strategic initiatives and/or operational improvements that will enable the next owner to capitalize on future growth.

Does the same investment rationale for a continuation fund exist in a “down” market?

Private equity firms have generated record returns in the past nine months with inexpensive leverage supporting sponsor acquisition activity and robust public equity markets enabling strategic acquisitions, public offerings, and SPAC mergers. With multiple avenues to achieve an exit, negotiating the right to re-invest alongside a third-party buyer and obtaining a high value is achievable. If the market environment changes and it becomes more difficult to sell investments, continuation vehicles will have less of an opportunity.

What are the legal and economic terms of the continuation fund?

A general partner that is managing two different funds on either side of a transaction will be conflicted. As such, it is important that the general partner have a clear allocation policy at the firm level, have a meaningful economic commitment to both fund vehicles, and be a “term taker” in its continuation fund that is re-investing in a business alongside a third-party buyer. Given the general partner is not leading investments in its continuation fund, it should offer the product to investors for a lower fee rate or no management fee compared to its core investment fund. To further mitigate conflicts, the general partner should only admit limited partners that are invested in its core (selling) buyout funds to its continuation vehicle.

Conclusion

Investors should be aware of the potential shortcomings of the private equity continuation vehicle structure and assess whether general partner has a strong rationale for raising a continuation vehicle. If structured appropriately, these vehicles offer another avenue for investors to deploy more capital with high performing managers in some of their best performing investments.