By Daniel Cruise, Deputy CEO, Tikehau Capital North America and Sharadiya Dasgupta, Founding Partner, Blue Dot Capital.

Driven by recent policy actions that include substantive onshoring provisions, the US decarbonization investment theme is poised for unprecedented growth. Technology maturation, favorable unit economics, rising demand, and public and private investment in the sector are creating in our view historical market opportunities across energy efficiency, low carbon mobility, and clean energy value chains.

The Inflation Reduction Act (IRA), signed into law last August, contains over $6 billion to onshore clean energy manufacturing[1]. In fact, the bill’s tax credit provisions will lead to much more spending to fight climate change with the Congressional Budget Office estimating the potential spend at $374 billion while recent market reports put the bill’s impact at closer to $800 billion[2]. Over the next decade, Credit Suisse puts climate spend in the US at $1.7 trillion while a Princeton University Zero Lab analysis puts the number at nearly $3.5 trillion[3].

Despite a looming economic downturn, this unprecedented coupling of demand and concerted public and private sector investment is set to transform the US investment landscape for years to come. Tikehau Capital’s long-standing decarbonization conviction will continue to guide our investment priorities as we explore these growing opportunities in the US market.

The increase in the adoption of renewables has been possible by a sustained reduction in their unit costs as well as the prices of batteries over the last 20 years.

Most notably, expressed in Levelized Cost of Energy (LCOE), globally, the price of solar and the price of onshore wind electricity declined by 89% and 70% respectively between 2009 and 2019[4]. Since 2012, the average total cost of an EV battery fell by more than 80%[5]. Technology available currently across the mission-critical sectors are ready for the influx of investment flows necessary for the world to meet its decarbonization milestones.

The United States, the second highest emitting economy in the world[6], has had a reinvigorated focus on comprehensive climate policy action since 2020 to build and expand the energy transition infrastructure needed to drive economic growth, mitigate climate change impact, and put the country on a path to achieve its stated 50-52% emissions reduction by 2030 goal (over 2005 level). Recent policy initiatives have enabled conditions to spur and sustain private investments in climate action themes.

The transportation sector accounts for 30% of greenhouse gas (GHG) emissions in developed countries, making EVs an important channel of the decarbonization matrix[7]. Within the mobility sector, road transportation is by far the biggest GHG emissions producer[8].

Even before the IRA, the number of EVs on US roads was projected to reach 26.4 million in 2030[9], building on a steady growth of 405% between 2015 and 2021[10].

The IRA contains significant provisions that would further accelerate the ongoing electrification of US transportation.

On the cost side, according to an analysis by McKinsey, in the Network for Greening the Financial System (NGFS) Net Zero 2050 scenario[11], after 2030 in the US, the total cost of ownership of passenger EVs would be lower than that of internal combustion engine (ICE) vehicles driven by maturation of technology and growing network effect.

In recent years, automakers have been ramping up their investments in electric vehicles and are directing billions into a scale-up of battery and auto manufacturing, charging infrastructure, and research and development.

The growing adoption and declining cost curves coupled with landmark policy incentives means that companies throughout the mobility ecosystem including suppliers to original equipment manufacturers (OEMs), plus manufacturers and operators of infrastructure are poised for growth and capital deployment opportunities.

Growth and onshoring of EV supply chain

Suppliers across the EV supply chain, from material processing to battery manufacturing to automotive assembly to battery recycling, have evolved to keep pace with the OEMs’ growing investments in electrification providing parts and solutions for batteries and the charging infrastructure.

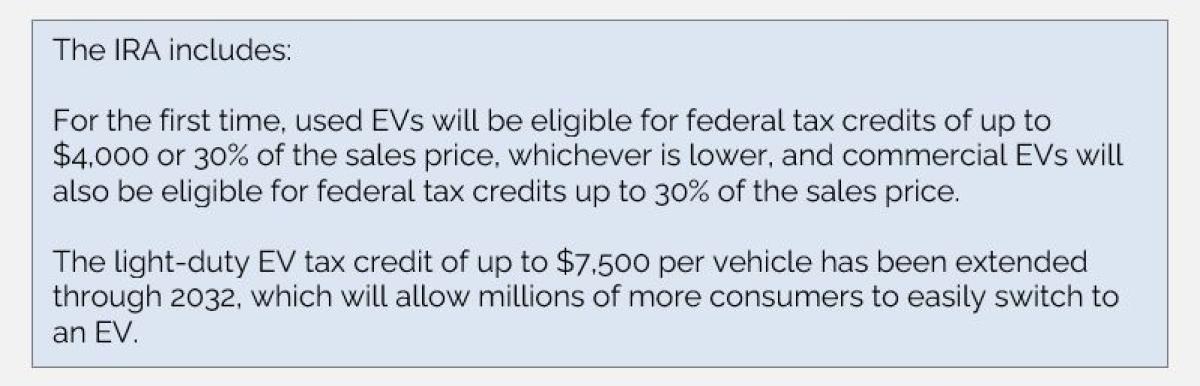

The $7,500 in tax credits for consumers who purchase EVs contained within the IRA only applies when final assembly of the vehicles occurs in North America. Another requirement: The components used in EV batteries must not have been “extracted, processed, or recycled by a foreign entity of concern,” which includes China and Russia. These requirements will provide additional impetus to the EV battery production capacity expansion in the US and the diversification away from China that is already underway.

The government approved close to $3 billion to boost production of advanced battery supply chains in February 2022 under the IIJA which included funding for upstream battery materials and refining as well as for production plants, battery cell and pack manufacturing facilities and recycling facilities. Car companies and suppliers such as LG Energy, SK Innovation, Panasonic, and Samsung are investing more than $38 billion through 2026 to boost battery production in the US, according to AlixPartners[12].

In response to the deepening investment opportunity set of the EV battery value chain, venture capital (VC) and growth equity funds have invested nearly $42 billion into battery technology startups across almost 1,700 deals, according to an analysis by PitchBook and TechCrunch[13]. What’s more, about 75% of the investments happened in the last two years alone.

Electricity is expected to play a prominent role in the future global energy mix. With a projected 60% growth in electricity demand by 2040, the power sector is expected to generate roughly half of all energy supply investments through 2040 (over $20tn in generation and transmission and distribution)[14].

Across countries, capacity is being ramped up and annual renewable capacity additions broke a new record in 2021, increasing 6% to almost 295 GW[15].

In the US, almost 5% of the energy consumed across sectors was from renewable sources in 2020[16]. Renewables made up 19.8% of electricity generation in 2020 and even without taking into account the IRA, the share was expected to rise to 35% by 2030, with most of the increase expected to come from wind and solar[17]. The provisions of the IRA are designed to drive growth at an even more rapid pace.

These historic investments will spur investor interest in products and services throughout the clean energy value chain including renewable equipment manufactures and renewable asset management service providers.

Catalyzing America-based clean energy value chains

Solar Energy Manufacturing for America Act

Baked into the IRA are provisions of the Solar Energy Manufacturing for America (SEMA) Act, which incentivizes US production throughout the solar value chain. The new tax credit is allowed for certain solar components, including photovoltaic cells and wafers, solar grade polysilicon, and a non-integrated solar module able to generate electricity when exposed to sunlight.

The US currently has capacity to produce metallurgical grade silicon, polysilicon, steel, aluminum, resins, racking and mountings and other key materials. The IRA includes a long-term extension of the solar investment tax credit which guarantees a solid demand outlook incentivizing investments to expand and improve the competitiveness of existing manufacturing capacity.

Source: In response to the passage of IRA and SEMA, the Solar Energy Industries Association (SEIA) released a white paper on August 16 with near- and long-term steps to drastically scale America’s solar manufacturing sector.

IRA extends tax credits for wind projects

A 10% production tax credit (PTC) adder applies for wind projects placed in service after Dec. 31, 2022, that satisfy a domestic-content requirement. To qualify for this new 10% bonus, it must be certified that any steel and iron, or any manufactured product that is a component of the facility, was produced in the US.

Energy efficiency in buildings and industrial end markets is a key decarbonization lever and a mature industry with long-running efficiency standards and labelling programs. Energy efficiency has large, near-term impact: An analysis of nine large countries and regions, including the US, the EU, and China showed that efficiency standards helped save about 1,500 TWh of electricity per year in 2018, equivalent to that year’s total generation from wind and solar in those countries[18].

The growing adoption has now received a further boost from the IRA. By targeting both retrofits and new buildings, the IRA provides substantive opportunities to scale the market for US building electrification.

The growing acknowledgement of decarbonization as a secular trend and the large-scale, whole-of-country, multi-sectoral policy initiatives have created a once-in-a-generation opportunity for businesses and investors across the energy efficiency, low carbon mobility, and clean energy sectors.

At Tikehau, we are committed to investing in proven US decarbonization-aligned businesses and technologies that are facing demand and supply side tailwinds.

Through future content and convening efforts, we will continue to explore the evolving growth dynamics of the US decarbonization ecosystem as it enhances capacity to cater to growing demand and materially reduce emissions.

Footnotes:

[2] https://www.theatlantic.com/science/archive/2022/10/inflation-reduction-act-climate-economy/671659/

[4] https://ourworldindata.org/cheap-renewables-growth

[6] https://worldpopulationreview.com/country-rankings/carbon-footprint-by-country

[7] https://www.un.org/sites/un2.un.org/files/media_gstc/FACT_SHEET_Climate_Change.pdf

[8] https://climate.ec.europa.eu/eu-action/transport-emissions_en

[9] Edison Electric Institute - Electric Vehicle Sales and the Charging Infrastructure Required Through 2030 (This This consensus forecast is based on four independent forecasts done by Boston Consulting Group, Deloitte, Guidehouse, and Wood Mackenzie, as well as analysis from the National Renewable Energy Lab)

[10] IEA Global EV Outlook 2022 and IEA Global EV Data Explorer

[11] Network for Greening the Financial System (NGFS), a consortium of central banks and financial supervisors, designed a Net Zero 2050 scenario that provides an even chance of keeping postindustrial warming below 1.5°C by the end of the century. McKinsey’s analysis focuses on opportunities and risks associated with the transportation sector’s decarbonization trajectory in line with NGFS Net Zero 2050 scenario.

[12] TechCrunch – Battery Investment Moves Onshore to Kickstart US EV Production, August 2022

[13] TechCrunch - Batteries Have Become VC And PE’s Most Electric Investment Opportunity, May 2022

[14] Based on IEA data from World Energy Outlook © OECD/IEA 2019, www.iea.org/statistics, License: www.iea.org/t&c; as modified by Tikehau IM

[15] IEA – Renewable Energy Market Update, May 2022

[16] EIA - Primary Energy Consumption by Source

[17] EIA – Annual Energy Outlook, March 2022

[18] IEA - Energy Efficiency 2021, November 2021

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Authors:

Daniel Cruise joined Tikehau Capital in 2020 and serves as Deputy Head of Tikehau Capital North America. Tikehau Capital is a global alternative asset management group with €37.5 billion of assets under management (as of 30 September 2022).

Daniel is a member of the leadership of Tikehau’s North America Private Equity Climate Practice and sits on its investment advisory committee. Previously, Daniel led several corporate functions and regions for Alcoa (AA) and Arconic (ARNC). He served on the Executive Committee of both companies. Prior to this, Daniel was assistant Press Secretary at the White House and part of the staff of the National Security Council.

Education: University of Cambridge, Brown University

Sharadiya Dasgupta, Founding Partner, Blue Dot Capital

Sharadiya is the founding partner of Blue Dot Capital, a sustainable finance consultancy. Blue Dot partners with financial services firms to support the end-to-end development and execution of ESG and impact investing programs, capabilities, and products. Blue Dot’s clients and partners include traditional and alternative investment managers, family offices, and data providers.

Sharadiya leads Blue Dot’s strategy, partnerships, and industry engagement and advises CEOs, CIOs, Heads of ESG, and family office principals. She is also the lead champion of Blue Dot’s “commitment-to-constant-learning” policy.

Education: Columbia University, Indian School of Business