By Sloane Ortel, Founder and Chief Investment Officer of Ethical Capital.

Larry Siegel recently put forward the argument that radically reducing carbon emissions is incompatible with civilization on a planet of eight billion people.

He goes on to argue:

A full energy transition from fossil fuels to renewables will not happen. We are going to continue to emit a significant amount of carbon dioxide into the atmosphere and, as the economist and blogger Tyler Cowen is reputed to have said, “Mostly we’re going to see how hot it gets.”

I have tremendous respect for Larry. His work as Director of Research at the CFA Institute Research Foundation was a big part of my life in the nine years I spent on staff at CFA Institute. But the dichotomy between sustainability and prosperity that he presents is false. And his logic is not just flawed, but also seductive and therefore dangerous.

With that said, it wouldn’t be particularly useful of me to simply say that I disagree. The investment community is rife with differences of opinion: they’re literally required in order for the market to function. So I see it as my responsibility to not only wade into this discussion, but to voice my dissent constructively.

The architecture of Larry’s argument is fairly straightforward:

- Access to energy is a necessary precondition for economic growth.

- Energy demand will increase as countries in the global south grow their economies.

- Meeting all this demand with current renewable energy technologies is not plausible.

- Fossil fuels are therefore the only way to meet the demand.

- Preventing climate change is impossible given all the fossil fuels we must burn, so all we can do is adapt to it.

Much of this is undeniable, but also incomplete.

The climate has already changed in ways that may be irreversible, so it’s impossible to disagree with Larry’s conclusion that we ought to focus on adapting to climate change instead of preventing it.

But after thoughtful consideration of what adaptation might actually cost and involve, it’s similarly impossible to conclude that blindly increasing our consumption of fossil fuels in a bid to boost growth is a sane path forward. The costs associated with Larry’s plan would be profound, the growth he claims it would unlock may never materialize, and the ethics of putting such a plan forward are immensely problematic.

Over the following paragraphs, we’ll take a deep look at what adapting to climate change actually means. Over the course of that exploration, it will become clear that the risks of acceding to this proposed future far outweigh the potential benefits.

We Can’t Know What Comes Next

I wish we could take it as a given that the global south will experience the economic growth it needs over the coming decade.

Unfortunately, a recent World Bank report makes this impossible. The authors examined the seventy-five countries eligible for loans and grants from the World Bank’s International Development Association (IDA), which are the poorest countries in the world by definition, and found some disquieting results.

The headline is stark: more than half of these countries are growing more slowly than the rich world. And fully one third of them are poorer today than they were at the onset of the COVID pandemic. This is a significant change from the past: We have to look back to the late 1990s in order to find a period where broadly increasing prosperity was this unusual.

I can’t tell you exactly why this is, but here’s one contributing factor: over the course of the last thirty years, jobs have reliably been created in lower cost economies as supply chains globalized in search of the most capital-efficient means of production. But after the frailties of this system were laid bare by the global pandemic, global companies began to “nearshore” or “friendshore” their operations in order to mitigate exposure to future shocks.

Firm-level benefits aside, further fragmentation of the previous world order is likely to have chilling effects on global economic growth.

A recent IMF working paper estimates a long-term global GDP loss of 4.5 percent if global economic integration reverts to its level in the year 2000, which was before China joined the World Trade Organization. Almost everyone would be worse off in this scenario, especially if tariffs and other barriers to trade were to be enacted as “corrective” measures.

And regrettably, some degree of such action is likely in the near future. To be clear: I am not predicting this. And I am certainly not rooting for it.

But the reality is simple: broader, more inclusive global growth is not a foregone conclusion under any circumstances. Trends in global trade patterns that made it seem that way may be reverting just as costly challenges are materializing.

Climate change is one of the most significant such challenges. Natural disasters already cost the average IDA country 1.3% of its GDP per year, and that has roughly doubled in recent decades. And though it’s difficult to know exactly what will happen as the climate changes, the consensus view is that these disasters will intensify.

Here in the intermountain west, it’s already obvious that a little bit of warming goes a long way. There is more than 300 million tons of dead wood in Colorado’s forests that’s rapidly drying into tinder for future wildfires.

This isn’t just nightmare fuel. It’s also the state’s fastest growing forest carbon pool.

New, healthy trees don’t automatically grow back in their place because the ecological niches these species have evolved to inhabit no longer exist.

This is far from an aesthetic consideration: these trees have historically provided a far-reaching suite of services to the surrounding ecosystems. And even if we had the data and audacity to claim that we fully understand these support structures, we won’t be able to replicate them without colossal, costly effort.

This single spillover effect from climate change has already turned the skies in New York City orange, caused more than half of the most dangerous air pollution in the American West, and left our ecosystems vulnerable to invasive species.

And this is ground truth, not a projection.

If we move towards the future on the path Larry proposes, we have no ready means of knowing what we will unleash.

The climate scientist slang for a future of fossil-fueled economic development is “taking the highway,” and the IPCC has a dedicated model to describe it. They refer to it as Shared Socioeconomic Pathway(SSP) 5-8.5.

It’s really quite a fascinating model, but it can be difficult to draw functional conclusions from without a bit of help. Fortunately, a new web app from spatial ecologist Matthew Fitzpatrick at the University of Maryland can help us imagine the disruptions that lurk down that path.

The app extends and updates a 2019 analysis published in Nature Communications to allow anyone to see how the climate is likely to change in 40,581 places and 5,323 cities around the world under SSP5-8.5.

Some of these allegories are dramatic: “If you happen to live in New York City, you would need to travel to northern Mississippi to experience what New York is expected to feel like by 2080. Say hello to hot, really humid summers and goodbye to snow in winter.”

But the profound danger of Larry’s plan becomes even clearer when we take a tour through the largest equatorial cities. By 2080, the climate in Lagos, Kinshasa, Bangkok, Ho Chi Minh City, Riyadh, Accra, Dar Es Salaam, and Manila will have changed so starkly that there is nowhere on earth we can look to as an analogy. And that’s not a complete list.

Taipei and Singapore will suffer the same fate, so in this future we can at least look forward to a tidy natural experiment that will demonstrate whether — and to what extent — wealth will work to shield us against an unearthly reality.

Not everything is bad and getting worse. The Great Barrier Reef in Australia is back to record coral cover, for instance. And though that should cheer us, it’s important to remember that these advances come after a $5 billion funding commitment from the government of Australia.

With that in mind, it’s reasonable to wonder what other costs would mount as the planet warms further. And remember that proceeding upon a development path that ignores those costs creates liabilities that will encumber future economic growth when they come due.

On this subject, my central insight is not that hard to grasp: it’s much simpler to avoid a mess than clean up after one. The interlinked ecological systems affected by the climate are profoundly complex and already struggling.

Investment professionals like Larry and me have a clear role to play in helping society navigate the implications of this, but we’ll need to look carefully at our professional ethics to do that effectively.

Capital Gains for Me, Ruin For Thee

My most profound misgiving about Larry’s line of argumentation is that he will not experience anything close to the worst outcomes of climate change.

As a fellow American and member of the investor class, both he and I are not just geographically remote from the worst of these outcomes, but will likely be able to afford whatever tech-enabled tools arise to mitigate the reality he advocates for.

Most folks in the global south would have no such succor, yet Larry would say he is writing out of concern for their prosperity. Underneath a chart that presents a clear linear relationship between energy use per capita and GDP per capita, he writes:

“Economic growth is pushing almost every country… toward prosperity. Pushing them back… would be the cruelest joke ever played on what Frantz Fanon called “the wretched of the Earth.”

I would hate to be involved in a cruel joke of any form, so let’s embrace the premise that there’s a straightforward path to sustained growth in any given country for a second. We’ll restrict our analysis to a single country – the Democratic Republic of the Congo – to keep things fairly tangible.

Imagine that after adopting our fossil fuel led development agenda, Congolese GDP grows constantly at the fastest clip observed in any single year since 1960 — 9.7% — for each of the fifty-five years between us and the year 2080. Assuming no change to population size, their GDP per capita would reach roughly the same level we enjoy today in the United States.

Would that be worth it?

From the narrow standpoint of global investors, maybe. Even just one growth story of that magnitude would unleash a bonanza for us capital markets types. And if we buy the premise that Larry’s plan would unlock growth of a similar magnitude across the global south, it gets very easy to anticipate describing our net worths with an extra comma or two.

But at what cost, and to whom?

After 5°C worth of global warming, any remaining Kinshasans would likely have to contend with fatal wet bulb temperatures throughout the rainy season. It’s possible that the mining industry would find ways to keep employees safe enough to keep the flow of critical minerals going, but that might involve wearing something akin to a space suit whenever they go outside. The agricultural sector — which currently employs about three-fourths of the country’s labor force — would be eviscerated.

Are the people of the Congo asking for this? Do they have the strong democratic institutions that would be necessary to grant their informed consent? We can certainly find individuals who align with Larry’s thinking, but that’s a long way away from a popular consensus.

The moral argument Larry makes is particularly seductive to Western ears. But I’d like to foreground something James Baldwin said in the 1970 documentary Meeting the Man: James Baldwin in Paris as we explore it.

Here’s the quote:

You, the English, you, the French, you, the West, you, the Christians. You can’t help but feel that there is something you can do for me. That you can save me. And you do not yet know that I have endured your salvation so long, I cannot afford it anymore.

The upshot here is straightforward: whatever their motivations, western interventions aimed at promoting prosperity are not necessarily welcomed by the folks they seek to support.

Think about how much would need to go right for future Congolese people to celebrate this plan retrospectively.

Growth would have to come fast, then last.

And even more unlikely: we must assume that both the political will to do something about all of the resulting negative externalities and the technology to actually get that done would arise at some point.

Why Are They Excited About This Again?

I don’t want to run the risk of mischaracterizing Larry or Mark Mills, the analyst he quotes extensively in his essay. So there’s a big quote from them coming soon. But because their argument talks a lot about GDP growth, I’ll first remind you that Simon Kuznets — the economist who came up with GDP — had the following to say about it:

GDP ‘measures neither our wit nor our courage, neither our wisdom nor our learning, neither our compassion nor our devotion to our country. It measures everything in short, except that which makes life worthwhile.

I hope having that handy makes the next few paragraphs a bit more fun for you:

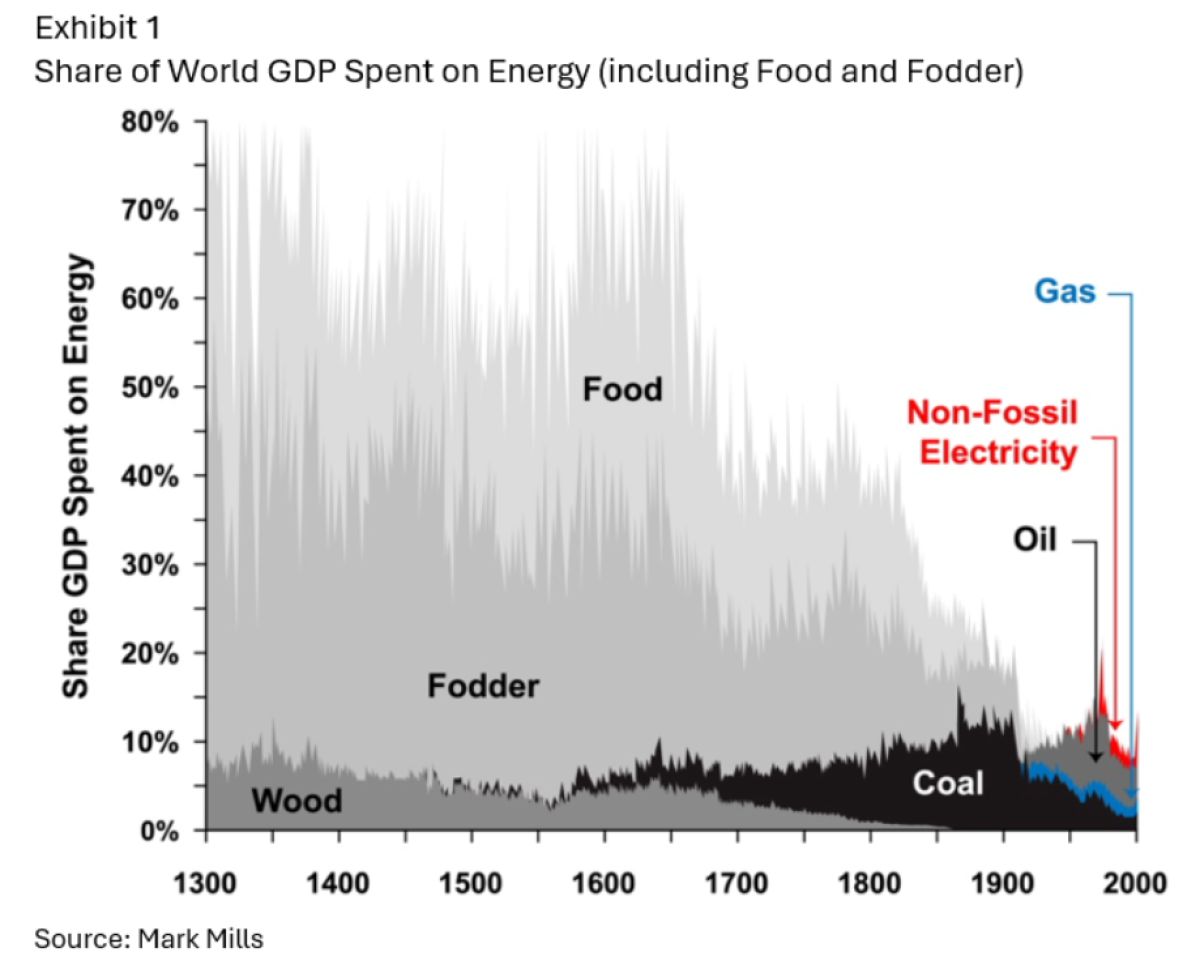

The proportion of the world’s GDP spent on energy-in-the-large, including food and animal feed, has decreased by an order of magnitude since the early modern era. A society that spends upwards of 70 percent of its income on food and fodder is poor indeed….

But energy costs as a share of GDP didn’t really fall off a cliff until the rapid industrialization of the nineteenth century, powered by coal and then oil and gas.

This may be counterintuitive: don’t heavy industries use a lot of energy? Yes, but an industrial economy is so much more productive than an agricultural and handcraft economy that the denominator – world GDP – grew massively.

Thus, the energy share fell even as the absolute consumption of energy soared. Interestingly, the energy share of GDP has remained about the same – around 10 percent –since the early 1900s.

This is not because energy use remained stable, but because energy use and economic output exploded upward roughly in tandem.

It’s interesting that Larry and Mark celebrate the role of technological development in producing this output explosion, but neglect to consider it in their analysis of renewable energy technologies. Their case that the energy needed to fuel growth must come from fossil fuels rests on the unstated assumption that renewables technology will not improve.

This is ahistorical.

The cost of building new wind and solar facilities has declined by orders of magnitude over the past twenty years while their efficiency has grown by leaps and bounds. And new battery chemistries are emerging based on plentiful, inexpensive minerals like sodium which may further reshape the energy landscape over coming decades.

In other words, today’s renewable energy technologies may not be able to fulfill global energy demand, but tomorrow’s might.

The 18th-century economist Thomas Malthus used similar logic to argue that the supply of food could not keep pace with the growth of the human population. But new developments in agricultural technology intervened and our planet is now home to roughly eight times as many humans who enjoy a much higher standard of living than our ancestors.

So as we consider the argument that fossil fuels are the only source capable of meeting our energy needs, let’s remember that things have a way of changing. The first patents for solar panels and wind turbines were only granted in the 1880s, and they’ve since evolved from novelties into economically viable alternatives.

This is particularly important because the path Larry and Mark propose has significant costs in addition to money. Average temperatures have already risen by .8°C relative to their average between 1961 and 1990, and it’s worth underlining that the order-of-magnitude increases in quality of living as measured by the cost of food and fodder had already materialized by 1900.

We have cell phones and the internet now, but also PFAS, and — according to a great report from the Republican side of Congress’ Joint Economic Committee — a level of mortality from deaths of despair like suicide, drug overdose, and alcohol-related liver disease that “surpasses anything seen in America since the dawn of the 20th century.”

There’s one thing we never had back then: plastic.

That’s not particularly interesting at first glance. Production volume in almost everything has grown by leaps and bounds in the postwar period. But there is one particularly pertinent thing to remember about plastics: they’re made of oil.

And demand for them is a huge part of global oil demand. To wit: the International Energy Agency’s latest medium-term oil outlook notes that Chinese imports of plastic polymers, synthetic fibers like polyester, and other intermediate petrochemicals produced roughly as much oil demand as the entire country of Germany in 2023.

The authors expect rising demand for petrochemicals (which, to be fair, is a much broader category than just plastics) to drive roughly three quarters of the increase in global oil demand between now and 2030.

And that’s worth remembering as you read the first sentence of Larry’s concluding section, which notes:

Some would say that it’s worth sacrificing almost everything we value in life to “save the planet.”

When the discussion is framed that way, it’s easy to overlook the many tangible steps that can be taken to mitigate the negative effects of fossil fuel consumption.

I doubt anyone would sign up to live in an unrecognizable world in order to preserve some semblance of normalcy. But that’s exactly the world that will result from Larry’s proposed path forward: just think about all of the cities with an unearthly future that we’ve talked about.

By contrast, a future with less plentiful polymers is a lot easier to stomach. Wouldn’t you be willing to give up plastic bottles and polyester for a chance at a more sustainable future? Wading into trade-offs like this is at the heart of effective adaptation to climate change, which Larry and I agree is absolutely essential.

So what does it look like to take that challenge seriously?

Arise, Acolytes of Adaptation!

We won’t make progress on anything without a cogent and comprehensive definition of the problem we’re dealing with.

When we talk about climate change, we’re often referring to a more complex set of changes linked to the consequences of human activity on the surrounding environment.

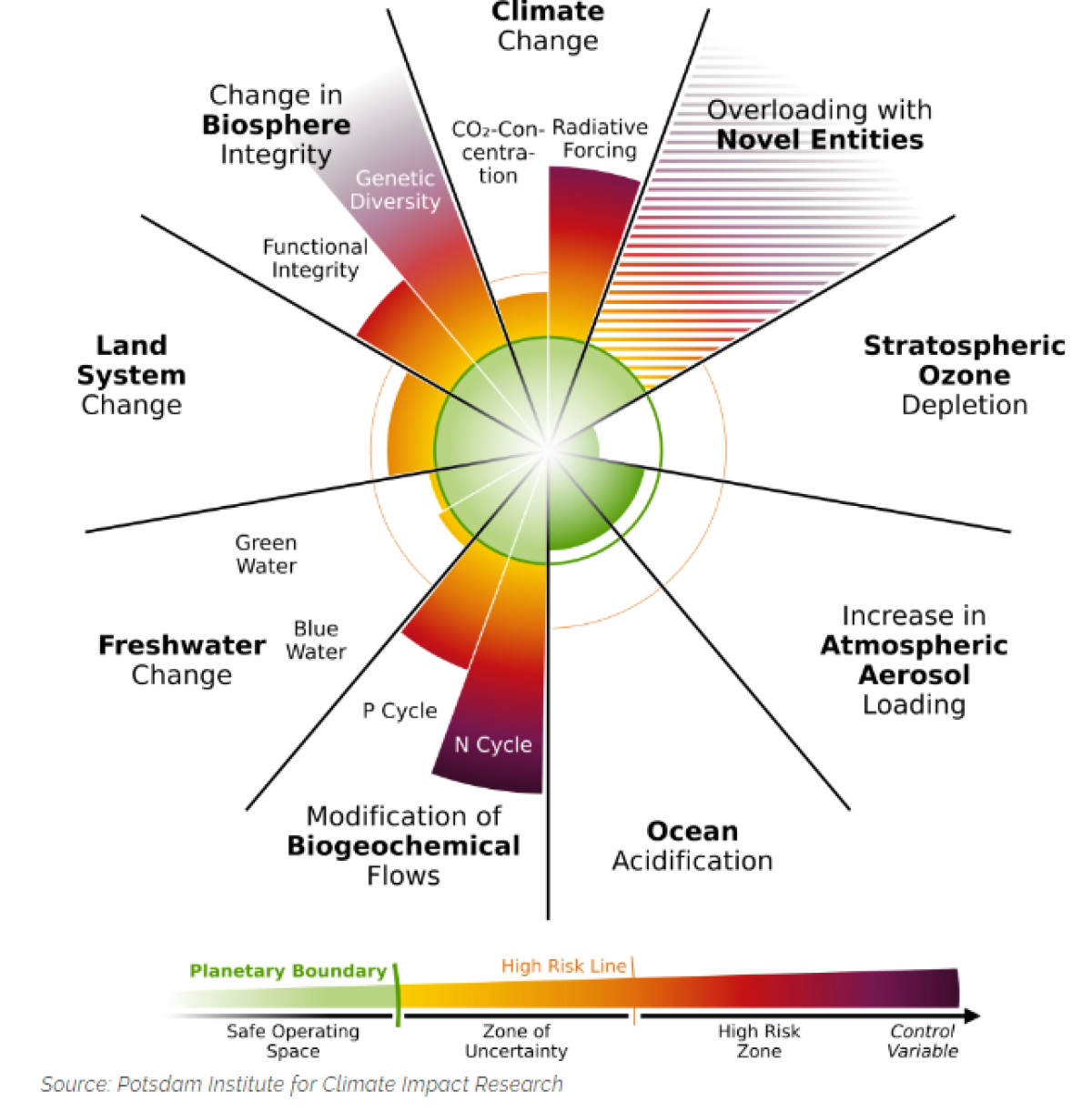

A team of researchers has helpfully enumerated each of the nine planetary processes that are essential for maintaining the stability and resilience of the earth as a whole. The extra large illustration below shows those nine systems, as well as the riskiness of their current state.

Climate change is just one of these nine processes, and CO2 concentration is not even its most acutely stressed facet at the moment. That distinction belongs to radiative forcing, which is what happens when the amount of energy entering earth’s atmosphere is greater than the amount that leaves it.

This framework invites us to think about the sustainability of activities in a fuller context. Take cutting down a forest for example: it has carbon implications to be sure, but also can lead the earth to absorb more solar radiation if the ground is darker than the forest that used to cover it.

Such activity also removes habitat, which can lead to the endangerment and extinction of species and a loss of genetic diversity in the biosphere. If the forest were to be replaced with farmland, there would likely also be increases in biogeochemical flows from the introduction of nitrogen and phosphorus fertilizers. Pesticides and other chemicals would likely come alongside them, introducing novel entities into the environment. And the farm would also have to be irrigated, which presages changes in freshwater use.

These connections are straightforward once they’ve been illuminated, but will likely be new to most readers. If nothing else, they highlight how intricately linked these systems are and allow us to imagine the non-monetary costs associated with upsetting them further.

But that’s not all: they are also confounding for ideologues, who often put forward one big solution for all of the planet’s woes.

Take electrification for example. The quote below that Larry shares from Mark Mills is undeniably true today:

The world already digs up an amount of earth equal to 7000 Great Pyramids per year to shift from gas, oil, and coal to the minerals required for the energy transition. These include nickel, cadmium, tellurium, obviously lithium, and cobalt among other minerals. You would have to dig up 50,000 Pyramids’ worth of the Earth each year to get [enough of] those minerals [to complete the transition].

All of that mining already has drastic consequences for the biosphere. To keep this essay readable, I’ll refrain from enumerating all of them.

But readers rooting for the immediate and wholesale replacement of fossil fuels should be aware that they’re advocating for something with profound spillover effects.

So where does that leave us?

The messy gray area where progress actually happens.

In a perfect world, we could rely on a combination of environmental markets and regulations to accurately price the external costs associated with all human activities.

That world sounds nice, but we don’t live there.

So as we think about how to reduce the harm associated with human activity, we need to resist one size fits all solutions and seek instead to understand the checkerboard of local realities that create the global energy picture. And the reality is that burning oil or natural gas would be a huge improvement in some places, since it would replace dirtier energy sources like coal.

For as long as the world remains imperfect, it’s incumbent upon analysts like me and Larry to embrace the reality that many things can be true at once. There is no “magic bullet” solution waiting in the wings to relieve our planet’s many stresses, nor a simple tradeoff between economic growth and sustainability.

We live in a world with finite resources but infinite desires. And over the past century, we’ve allowed those desires to set the economic agenda without much interference.

None of us can put forward a complete solution to solve the climate crisis while preserving our economic prosperity, and we should acknowledge that at every opportunity. After all, we are in the business of making decisions amid conditions of uncertainty. And people often think that means we know much more than we actually do.

That’s why, as we close this exploration, it feels important to draw attention to the malignant overconfidence with which us finance types can sometimes trod through thorny ethical terrain.

If we come to believe that we can speak with certitude on behalf of people we have never met about their own best interest, we imperil our ability to serve our social function, weaken our standing as a profession, and diminish ourselves individually in the process.

The only thing we can know about the future is that it’s coming. The fuel that powers it, the technology that shapes it, and the people we’ll share it with are yet to be determined. But it’s likely that the world will stay an inherently subtle place no matter what happens, and I hope me and my colleagues at Ethical Capital will be here to help you embrace that nuance.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Sloane Ortel is a dynamic and passionate speaker that brings a wealth of experience, practical insight, and warmth to every interaction.

As the Chief Investment Officer of Ethical Capital and architect of its investment process, she is known for managing long-term investment portfolios with industry-leading moral and material rigor.

Prior to starting her own firm, she spent close to nine years on staff at CFA Institute where she published hundreds of essays on investment topics and created educational materials aimed at advancing the craft of investment management. Prior to CFA Institute, she managed investment portfolios at Oppenheimer & Co in New York and a Bangalore-based family office.

Sloane is a graduate of Fordham University and a member of both CFA Institute and CFA Society Salt Lake.