By Scott Maidel, CFA, Head of Business Development, and Steve Richey, co-CIO, Head of Convexity Alpha at QVR managing the QVR Market Neutral, Hedged Equity and Volatility Hedge strategies.

The marketing departments at banks and asset managers have conjured up some savvy descriptors for options strategies over the years. Portfolio Insurance, Option Overlay, Hedged Equity, Overwriting, Derivative Income, Defensive Equity, Structure Outcome, Enhanced Equity, and Buffer. As sales departments had success selling these types of products the assets under management (“AUM”) grew. Strategies using options are now commonplace in portfolios.

Investors will always look for ways to cheapen hedges but unless very closely understood, persistently capping the upside on your equity allocation is not the answer. Historical techniques such as collars and put-spread collars employed by some of the largest equity providers have become so overcrowded, that they will likely lead to nothing but extreme relative underperformance, simply value destruction. This statement is arguably also true for strategies now referred to as “Derivative Income” (aka call overwriting, defensive equity, covered call, etc.), which are all simply selling short calls against equity. Historically, the go-to benchmark here has been the Cboe BXM Index. An accurate description of benchmarks such as the Cboe BXM or similarly PUT indexes historically would be “Equitylike returns with lower volatility”, but today should be replaced with the statement, “Equity-like risk with lower returns”. These volatility selling strategies cap upside. An option selling strategy is not inherently risk-reducing: a covered call or a cash-secured put selling strategy has effectively the same exposure as outright equities in a sharp market selloff.

Various competitors in Hedged Equity such as JP Morgan1, SWAN2, Gateway3, Calamous4, Parametric5, and Innovator6 have had difficulty in recent years delivering their stated objectives. We believe their underperformance is the lack of price sensitivity on the options they use to deliver their stated investment mandate. These strategies have caused a combination of a simple imbalance of near-dated volatility supply and long-dated put demand. Over time, this has led to their products’ underperformance in both market rises and declines. Having simply overpaid for put exposure on the one side and having sold calls too cheap on average on the other side.

In the mid-1990s, the use of option strategies to enhance returns and/or provide downside protection was offered to institutional investors. Typically, institutions like hedge funds, insurance companies, pensions, and endowments had access to them. The amount of capital that was deployed was a fraction of the overall option volume. Newly offered structured product and derivative income categories collectively act as oversupply to Equity Hedge as an asset category.

JP Morgan Hedged Equity, for example, uses put spread collars (buying put spreads vs. selling calls) and is net short optionality, generating large relative losses in rallying markets. High returns from volatility selling attracted more money post-GFC, compressing volatility risk premium and lowering upside call strikes on popular “zero-cost” collars, which are certainly not “zero cost”. Pricing in the derivatives markets is simply the result of excess trade flow and with a decreased call premium received, all else equal to buy a put spread, the upside call strike decreases. These types of outcomes for large, disadvantaged hedged equity strategies have become more extreme and is reflected in the poor performance. This trade flow, without a doubt, is contributing to a large and growing structural dislocation that is not compensating “insurance sellers” (i.e. near near-dated call and put writers) and overcharging in implied volatility terms, buyers of insurance (i.e. long-dated puts).

So how do investors improve risk-adjusted performance in hedged equity? The answer is: Combine an alpha strategy that has negative correlation to broader equity. Moving alpha and porting that atop beta has been called portable alpha. Capturing positive returns in upside equity markets (positive up capture) and capturing positive performance or at least flattening downside beta returns in equity downside (flat to negative downside capture) is ideal. The vast majority of managers are upside down on up-down capture. Hedge funds and various alternative strategies with a negative up-down capture spread, rely on persistent positive equity upside for returns. In other words, this is typically achieved by underperforming funds through a combination of participating in less of the upside (bad) and more of the downside (bad) equating to a negative up-down capture.

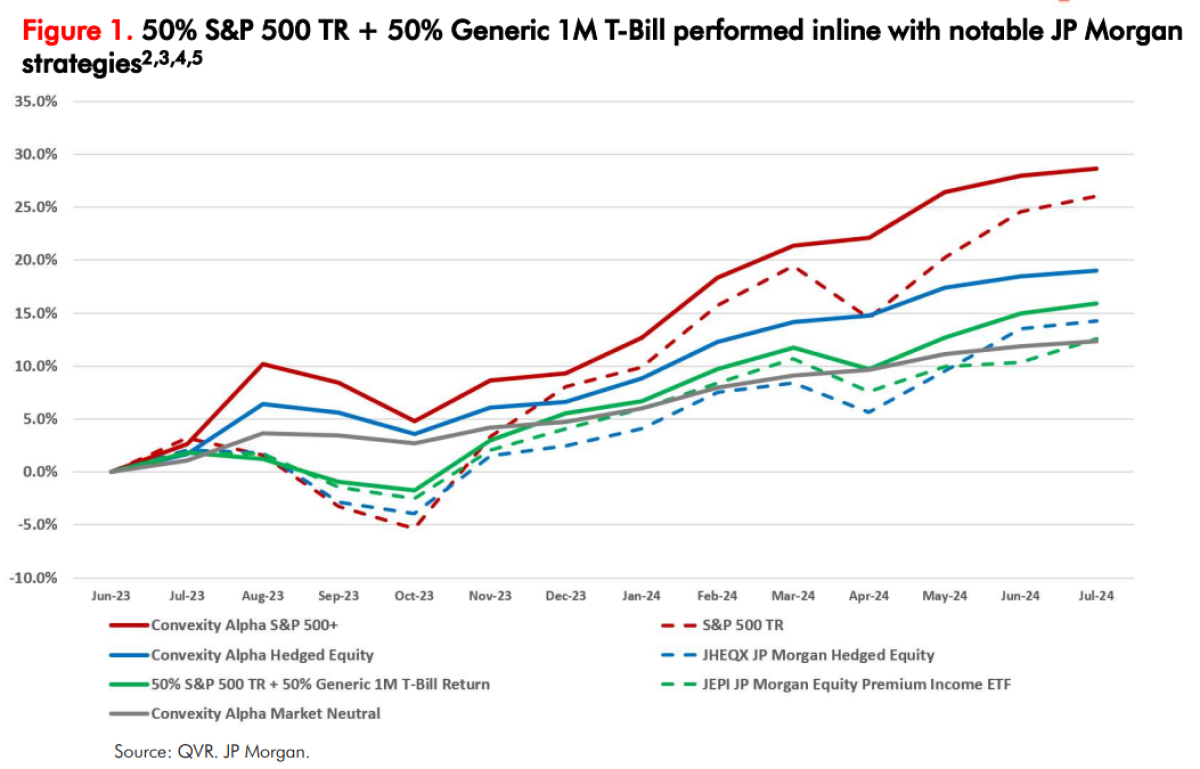

The term “outcome-oriented investing” started to be used many years ago, to allow managers to explain away poor performance relative to simple, suitable benchmarks and strategy substitutes. In Figure 1, we show how a simple strategy substitute of 50% S&P 500 TR + 50% Generic 1M T-Bill Return has recently outperformed notable JP Morgan strategies, tickers JHEQX, JP Morgan Hedged Equity and JEPI, JP Morgan Equity Premium Income ETF. Note the dashed blue and green lines underperforming the 50/50 strategy substitute.

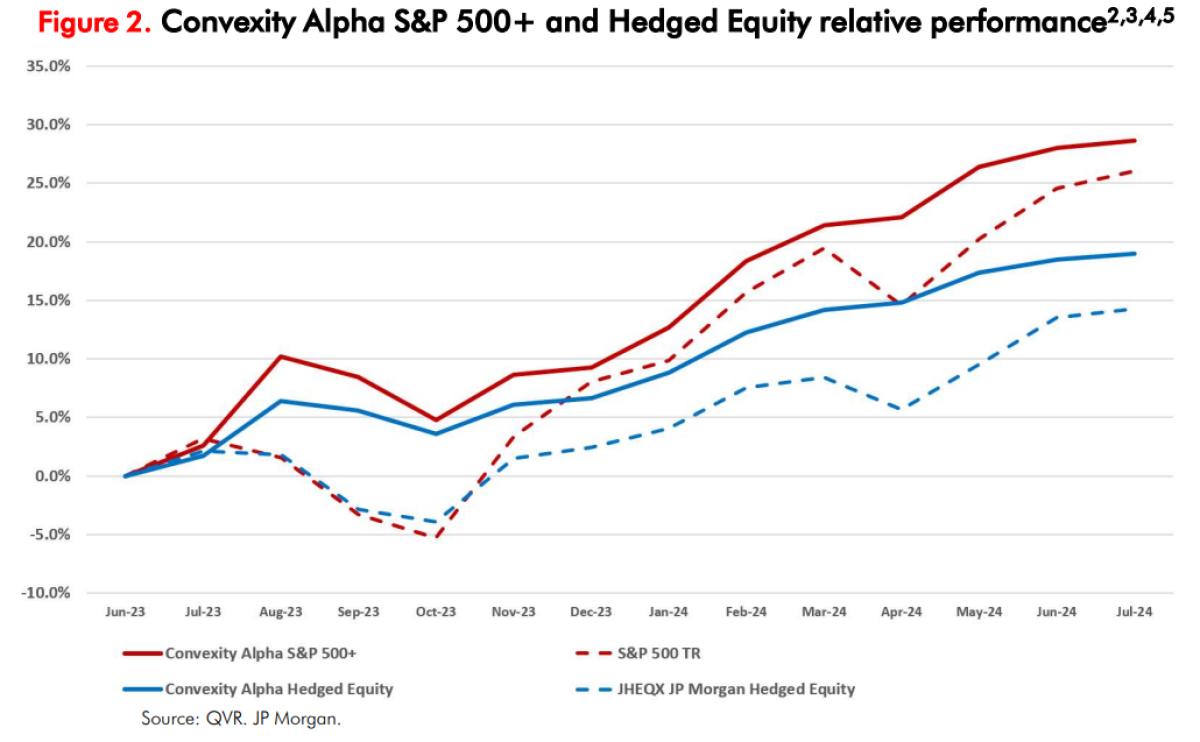

Figure 2 shows QVR Convexity Alpha S&P 500+ and Hedged Equity performance relative to suitable benchmarks. The program is designed to improve up-down capture by limiting losses in equity downside but also not “capping” upside potential such as with a put-spread collar (JHEQX) or covered call strategy (JEPI).

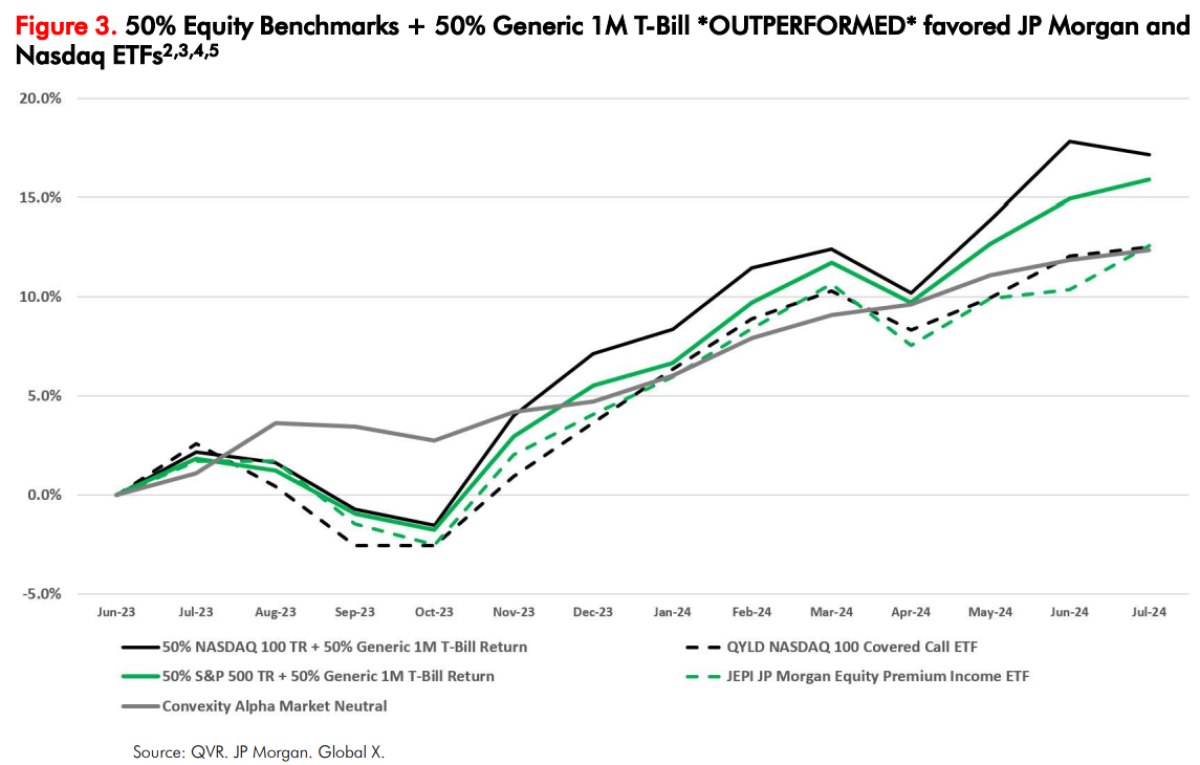

Figure 3 shows QVR Convexity Alpha Market Neutral performance relative to two similarly split 50% equity +50% Generic 1M T-Bill benchmarks. We made the point above, that investors may be better off with a 50% S&P500 TR + 50% Generic 1M T-Bill Return versus notable JP Morgan strategies, tickers JHEQX, JP MorganHedged Equity and JEPI, JP Morgan Equity Premium Income ETF. We also now add the QYLD, GLOBAL X NASDAQ 100 Covered Call ETF. The utterly dismal performance of these strategies relative to standard benchmarks such as the S&P 500 TR and NASDAQ 100 TR we’ve handicapped to the 50/50 benchmark and JEPI and QYLD still underperform. The market through option pricing is punishing investors of these products and giving opportunity for more skilled traders to achieve true alpha for investment programs.

As a reminder, in decades past these types of strategies *had* the potential to outperform generic equity benchmarks. Today, however, not even a reduced benchmark hurdle of a 50/50 benchmark seems to be easily outperformed. The massive trade flow, supporting hundreds of billions in AUM growth without a doubt, is contributing to a large and still growing structural dislocation in options markets.

UP-DOWN CAPTURE

Consider up-down capture which we already addressed in a recent research piece, see OPTION SELLING HASBECOME CONSENSUS: ITS IMPACTS Q1 2024. Up capture measures return capture as a percent of monthly upside. A positive capture is ideal in upside (ie SPX +1%, strategy +0.5%, equates to a +50% up capture). Down capture measures return capture as a percent of monthly downside. A positive capture figure is aligned with the direction of asset downside (ie SPX -1%, strategy -0.5%, equates to a +50% downcapture). A negative capture however is ideal in downside (ie SPX –1%, strategy +0.5%, equates to -50%down capture). Up minus down spread is indicative of manager skill and future returns. Over time, we have seen a degradation of up-down capture for investable strategies such as the Cboe BXM and investable indexes such as the HFRXEH index. The oversupply of option-selling strategies has changed the game for many prevalent funds. This is a major problem for many investment managers. These product-based price insensitive strategies have a material effect on implied volatility and therefore the pricing of options. These end-users are contributing to a large structural dislocation. This is unequivocally bad news for managers employing these types of strategies.

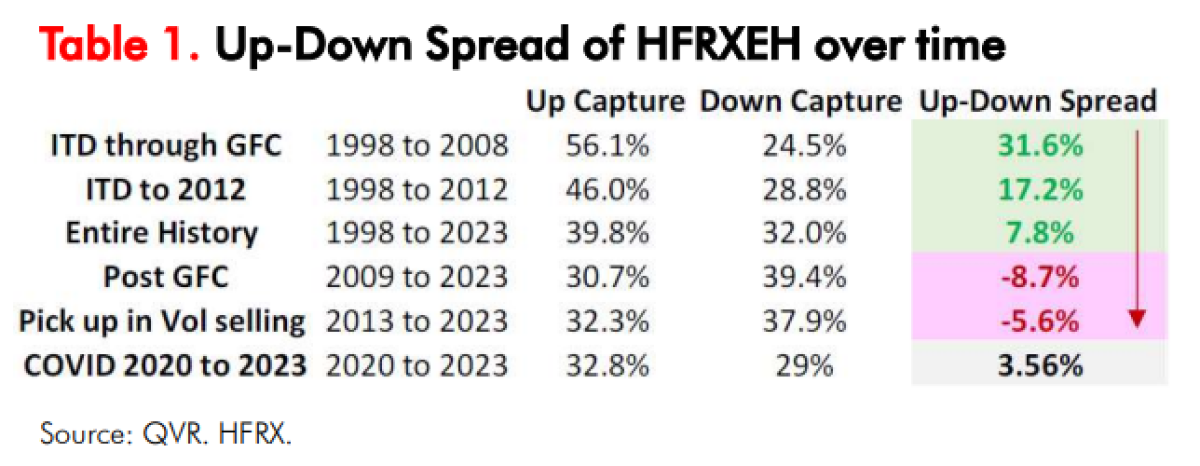

As with all risk premiums, the attractiveness ebbs and flows. Pre-GFC, short-term options tended to be expensive. As a result, harvesting a volatility risk premium and hedged equity strategies were attractive and backtested well pre-Global Financial Crisis (“GFC”). Post-GFC, both retail and institutional demand for option-selling strategies and hedged equity started to grow rapidly. Large groups of investors are now viewing both as an “evergreen” asset class for income generation (“Derivative Income”) or a liquid alternative (“HedgedEquity”). Or at least that’s what we see marketed everywhere. Table 1 shows the degradation of the up-downcapture for the HFRX Equity Hedge Index, +31.6% (excellent) ITD through GFC versus -8.7% Post GFC (bad).

Call and put write strategies have roughly the same downside risk (down capture) as underlying equity market risk, with much less positive return in up markets. In a portfolio context, adding negative convexity strategies with low returns to the upside and high correlation to risk assets to the downside is not additive to portfolio performance. An investor should always think about the portfolio context and the opportunity cost of capital, the value potential.

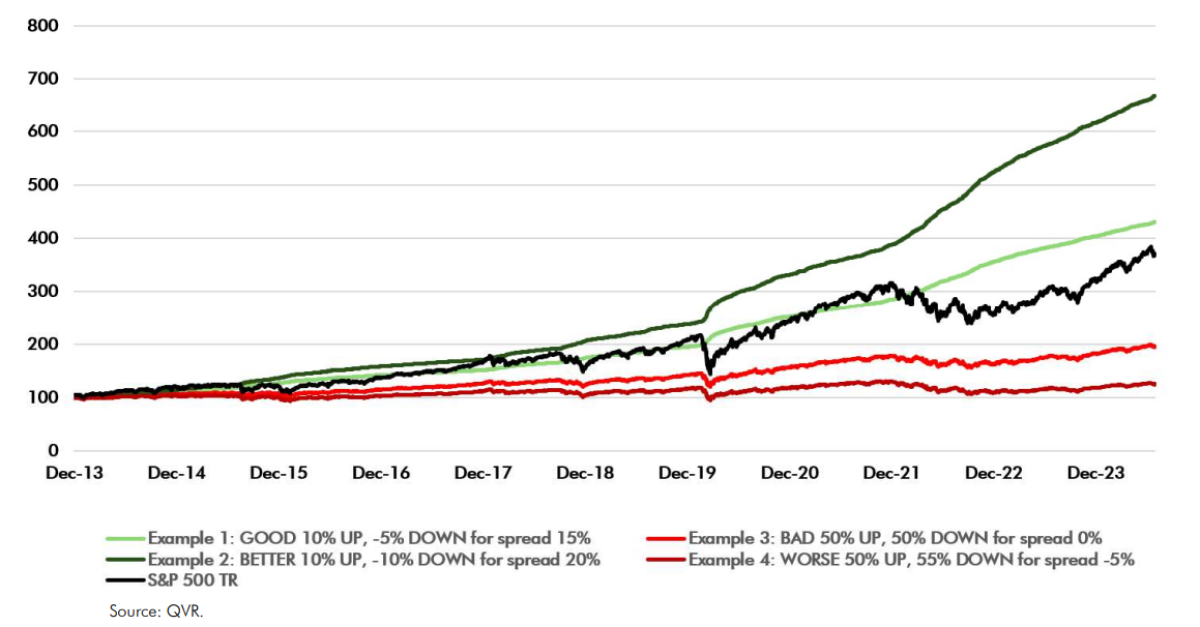

Up-down capture is important, not to only produce superior performance but to have any potential to outperform relevant benchmarks. Or said differently, knowing your manager is not destroying value potential. Historically, a strategy that could provide a +10%, +15% or a very good +20% up-down spreadcapture or better would be considered very attractive and had the potential to handsomely outperform the S&P 500 (Figure 4) or various benchmarks such as the HFRXEH over time. An up-down capture in the +30% or +40%range would be considered elite.

ARE YOU BEING MISLED?

So are you being misled, with all the marketing spin? Maybe. This is a market after all and we do encourage different points of view. So here is ours.

COVERED CALLS ARE NOT A FIXED-INCOME ALTERNATIVE

Perhaps the most egregious and certainly misleading statement we’ve seen lately has been, “Considering a fixed income alternative? Explore how the Global X Nasdaq 100 Covered Call ETF QYLD could add a new dimension to your portfolio.” Nearly all the downside of the Nasdaq 100 is certainly not a fixed income alternative.

COVERED CALL AND PUT WRITE STRATEGIES ARE NOT DEFENSIVE EQUITY OR HEDGED EQUITY

Consider this statement, “We construct a lower-volatility portfolio by reducing equity beta and systematically selling fully collateralized equity index options to enhance returns.” On various medium and long-term defensible time periods (i.e. 5-year, Annualized ITD), this same provider's marketing material makes our point and shows that a 50% S&P 500TR and 50% T-Bill mix outperforms. Alternatively, consider this simple point: a covered call or cash-secured put (or 50/50 mix of both) always has near 100% beta and downside volatility to equity market in the downside limit, even if an out-of-the-money put strike might provide a bit of “buffering” for small moves.

THE VOLATILITY RISK PREMIUM IS NOT PERSISTENTLY POSITIVE OR ATTRACTIVE

Consider this statement, “Our options-based strategies benefit from a persistent implied volatility risk premium, which can support cash flow generation and reduce risk.. . . able to be employed in a variety of portfolio applications and may potentially enhance an equity portfolio, diversify fixed income allocations, or offer a liquid and transparent component to an alternative program”. The relative performance has underperformed so much in recent time post-GFC from changing dynamics, that this and many other providers compare an equity strategy to a fixed-income alternative. Furthermore, sloppy statements around persistently positive volatility risk premium (“VRP”), to the unsuspecting reader, may sound attractive. In practice, the underlying strategy uses different tenor combinations of options that have no relevance to viewing the Cboe VIX index to current or subsequent 1-month SPX realized volatility to create a nice-looking chart. BEWARE OF THE TERM “DERIVATIVE INCOME”, NEW MARKETING SPIN

This is highly misleading. Using the term “income” was even too much for Morningstar historically, which felt to comment on it in 2013 given the slew of option-selling mutual funds hitting the market. They have however given way to the option selling tsunami and created a Derivative Income category. We are aware they noticed our prior statements about this article and furthermore, it has been removed:(https://www.morningstar.com/articles/612677/option-selling-is-not-income). Business is business, softening the tone. A more recent article can be found here: https://www.morningstar.com/funds/options-income-like-jepi-isnt-everyone

Beware these investments may not rot your teeth but maybe your portfolio. See here: https://www.morningstar.com/columns/rekenthaler-report/boomer-candy-sweet-treats-or-investment-toothache

And we like the WSJ-coined-term,' boomer candy', here: https://www.wsj.com/finance/investing/retireesboomer-candy-investing-fu…;

We also as Morningstar don’t understand why investors have become so fond of derivative-income funds. After all, these funds do not receive something for nothing. See here: https://www.morningstar.com/columns/rekenthaler-report/covered-call-funds-mystery-wrapped-anenigma.

High yield, low risk, enhancement?

Absolutely not. Opportunity for skilled traders? Unequivocally, yes. And that is the point of this analysis, creating better Hedged Equity and S&P 500 outperformance.

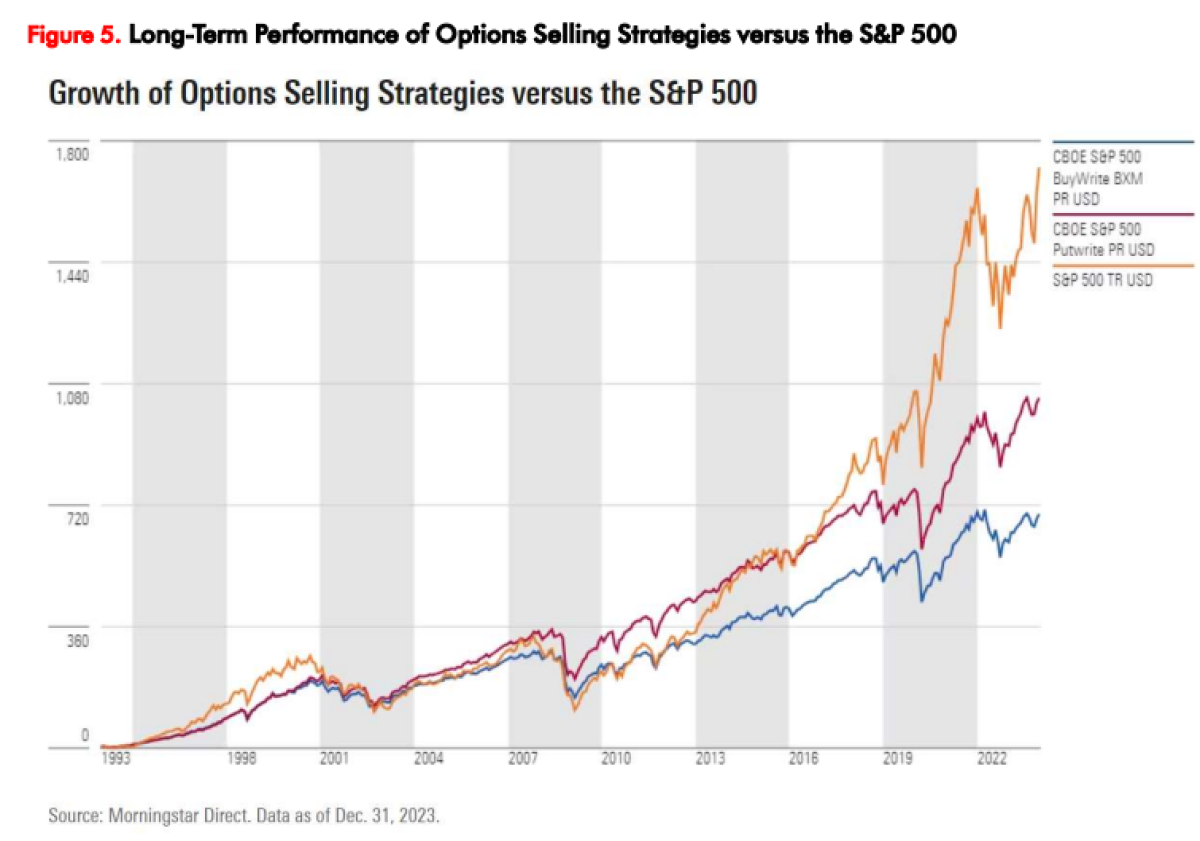

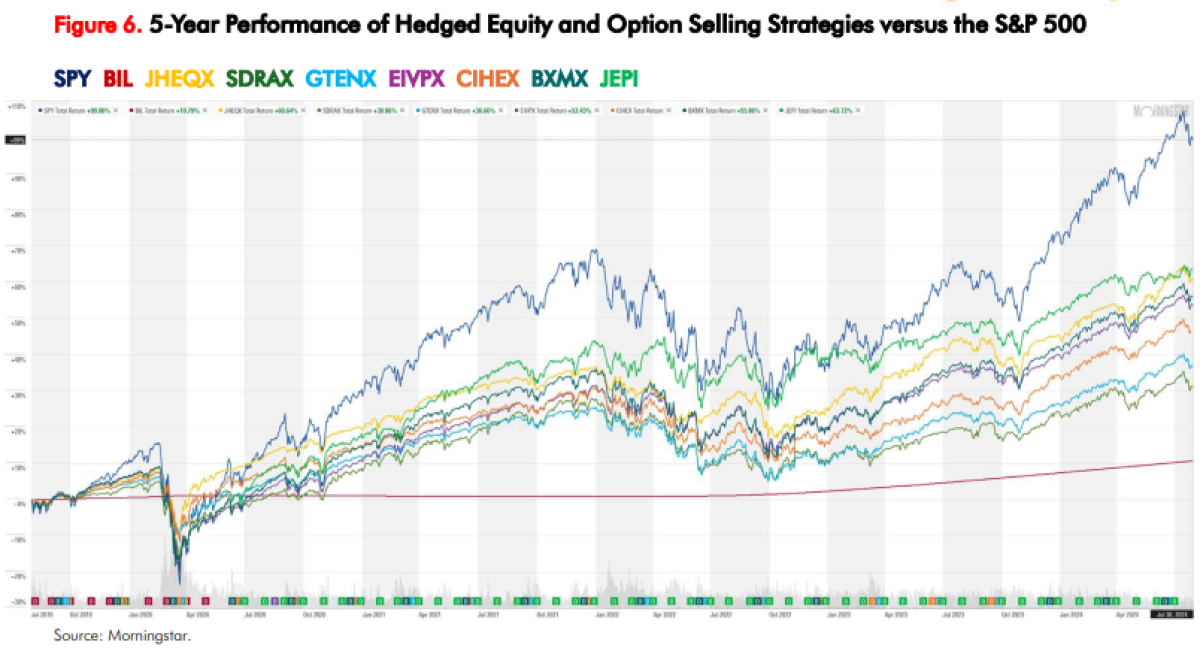

Shown are a select few of the prevalent retail and institutional investment vehicles in the hedged equity and option selling space. Figure 5 shows a simple view of underperformance picking up steam post-GFC and particularly in 2013 onward as public mutual funds and ETF’s launched. Figure 6 shows various total returns for institutional and retail traded traditional hedged equity and derivative income tickers: JHEQX, SDRAX, GTENX, EIVPX, CIHEX, BXMX, and JEPI. Given the deteriorated opportunity set for legacy firms and legacy strategies, we still don’t believe many will course correct. Most are too entrenched in existing programs for their business operations.

ALPHA MATTERS

We are undeterred that, finding repeatable sources of alpha, attractive risk-adjusted return is best found by providing liquidity to price-insensitive end users of derivatives. This is a core belief of any skilled trader and a good starting point for any long-term investment strategy, so should come as no surprise. Provide liquidity to price-insensitive options trading programs and own mispriced gamma adapting to the opportunity set.

CONCLUSION

The poor performance of short-term option selling strategies over the last 10-15 years stems from their incredible AUM growth from successful marketing spin. Given the deteriorated opportunity set for legacy firms and legacy strategies, we still don’t believe many, if any, have the skill to pivot. These traditional approaches are simple and pursued by too many players, degrading returns and impacting implied volatility. This persistent demand for risk mitigating and income strategies has led to a structural shift in risk pricing in S&P 500 options. We seek to provide liquidity to price-insensitive options trading programs and own mispriced gamma adapting to the opportunity set.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Authors:

Scott Maidel joined QVR from Gladius Capital Management where he was most recently a Director of Institutional Solutions. He was previously Senior Portfolio Manager, Equity Derivatives at Russell Investments and Associate Director, Global Trading and Trade Research at First Quadrant. Scott has over 15 years of trading and portfolio management experience with global derivatives.

Scott holds a B.Sc. in Investments and Financial Markets from the University of Southern California, an MBA from Pepperdine University and is a Harvard Business School alumni of the Program for Leadership Development (PLD). Scott is a CFA charter holder and Financial Risk Manager (FRM) certified.

Steve Richey is co-CIO, Head of Convexity Alpha at QVR managing the QVR Market Neutral, Hedged Equity and Volatility Hedge strategies. Steve has long career success generating alpha from dislocations in S&P 500 option markets. Steve has spent over 25 years researching and refining S&P 500 trading strategy both professionally and personally. Steve started his trading career at First Quadrant and in his 11 years there, he attained the position of Partner and Director of Trading and Global Options Strategies where he oversaw a $3+ Billion systematic volatility program at its peak. Steve more recently was a PM at Capstone and Parallax. Steve holds a B.Sc. And MBA from Hawaii Pacific University and is a CFA Charterholder.