By Michael Green, Portfolio Manager and Chief Strategist at Simplify.

This note examines how passive investing has influenced short-selling dynamics, particularly highlighting unusual occurrences of stocks with over 100% short interest. Examples like Gamestop and Dillard’s are discussed, showing how passive funds’ activities and company buybacks impacted short sellers and stock prices.

Case Studies of Gamestop and Dillard's:

- Gamestop and Dillard's are used as case studies to illustrate the effects of passive investing and buybacks on stock prices. Both companies had significant share buybacks that led to passive funds like Vanguard and Blackrock becoming net sellers. This selling, combined with buybacks, created opportunities for significant price movements, as seen with Gamestop's short squeeze driven by retail investors.

- Reducing estimated float by passive ownership helps to understand the violence of the subsequent rallies.

The Main Event

Was Anyone Else Sad?

I have to confess that I tuned into Keith Gill … and waited 25 minutes for him to show up late to his own party. I briefly watched a few of his videos during the meme stock craze in 2020-2021. I concluded that his fundamental thesis on Gamestop (GME) was flawed, but this took a backseat to the dynamics highlighted on short selling in the presence of passive.

I’m going to split today’s note into three pieces. The first addresses the mechanics of how passive investing has changed the game for short sellers. The second (next week) attempts to address the reveal of the matrix that this episode entailed. Finally, part three attempts to integrate my emotional reaction to Keith Gill, the saddest newly minted centimillionaire I’ve ever seen.

Shorting in the Presence of Passive

The existence of a stock with greater than 100% short interest is unusual. The Managed Fund Association claims that this has only occurred 14 times in total since 2012, and notes that 8 of the 14 companies were very small. The remaining six examples they cite are interesting:

Four of the six were resolved with no adverse impact on short sellers. In fact, most instances of excessive shorting were in response to imminent share issuance and VERY brief in duration. Horizon Therapeutics is an example where serial share issuance during pharmaceutical product development “protected” the shorts:

This is the typical pattern where shorting is in response to a catalyst reasonably well-telegraphed by underlying fundamentals. In 2012, investors in the new secondary reduced their exposure and captured the new issue discount by shorting shares ahead of the offering.

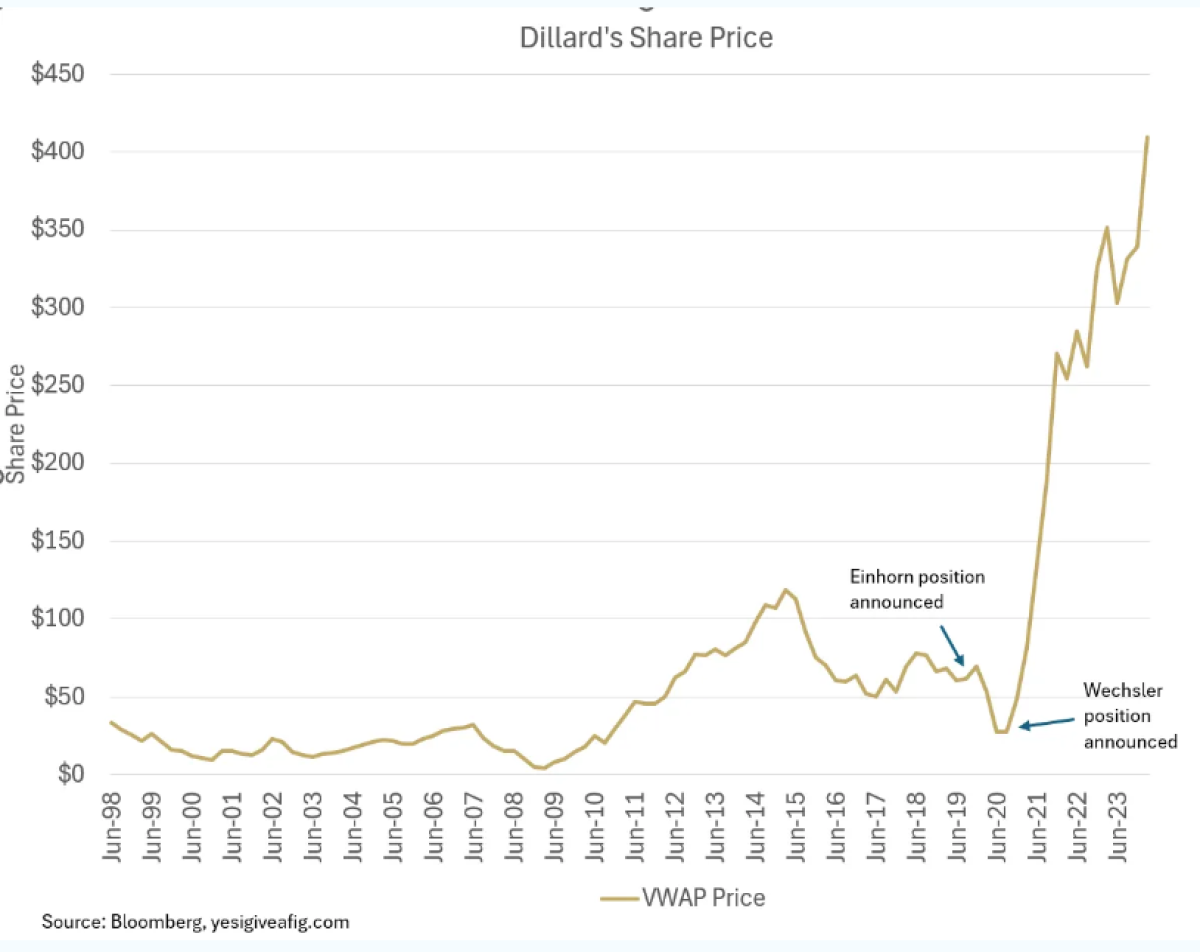

The last two, Gamestop and Dillard’s were obviously different, with both market caps among the largest and both shorted in expectation of likely bankruptcy filings due to a combination of failing business models and the impact of the pandemic. Gamestop’s business was extremely cash rich, but burning cash rapidly through a combination of share buybacks in 2019 (they repurchased 34% of shares outstanding) and losses in 2019, 2020 and 2021. Well, before the pandemic, these were businesses apparently in terminal decline.

Let’s hit Dillard’s first…

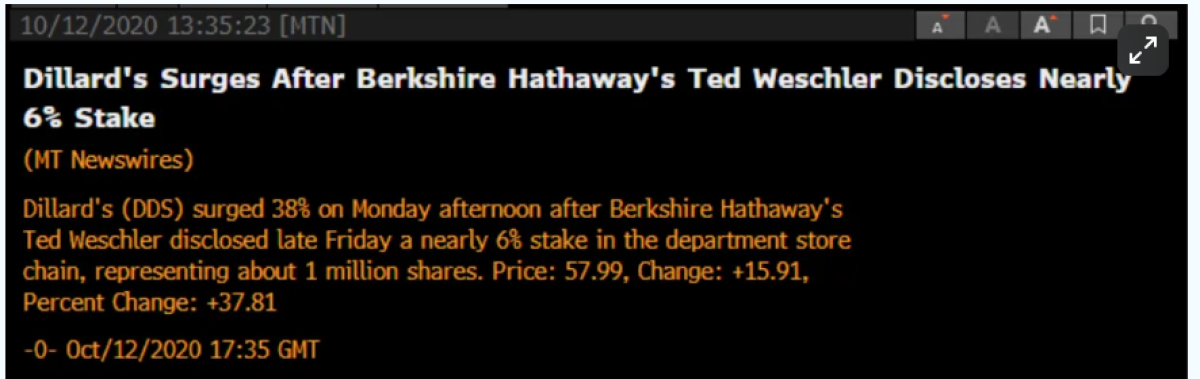

While it was relatively cash poor going into the pandemic, Dillard’s was well positioned to benefit from pandemic stimulus as competitors Sears and JC Penney had exited the business in Oct 2018 and May 2020 respectively. As customers returned to stores and online purchases, the company restructured its logistics chains, converting retail stores to “ship from store” locations and began to benefit from a rebound as early as Q4-2020. Ahead of these events, however, a savvy buyer stepped in:

And while Ted’s prescient purchase was the spark, the real fuel for the fire was created by an unprecedented improvement in margins as Dillard’s responded to inventory shortages by reducing discounting.

Reduced inventory was part of the dynamic, but a June 2022 article from the Northwest Arkansas Democrat Gazette (don’t you love the internet?) tells the real story:

Warren Stephens, chief executive of family owned financial services firm Stephens Inc. and a member of Dillard's board of directors, said at a recent meeting of Rotary Club 99 in Little Rock that one factor is that the company is benefiting from the purchase of many competitors by private-equity firms.

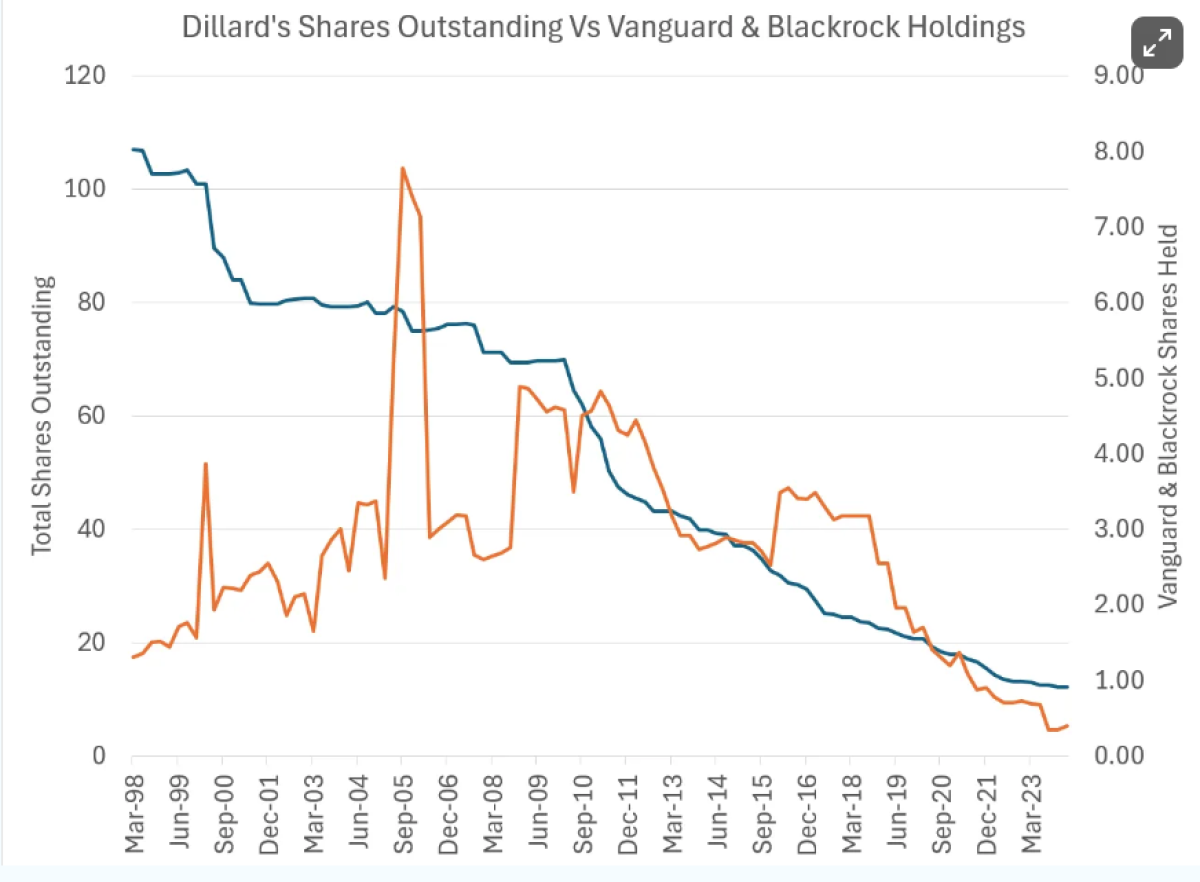

Once again, we see reduced competition at work to benefit capital. On the same level of sales from 2019, Dillard’s now generates 33% more gross profit and 300% more operating profit. The company has continued to buy back shares at a furious pace. Unsurprisingly, my friend David was all over this one, although he bought it a bit earlier than Ted. Bravo to both.

But I’d note that something else was going on… due to the large buybacks, both Vanguard and Blackrock were actually net SELLERS of Dillard’s. Needless to say, this is unusual. While I can’t definitively conclude that this selling contributed to the remarkably low prices for Dillard’s in late 2020, I can confidently suggest it certainly didn’t help the price. So, in this case, passive likely helped create the opportunity:

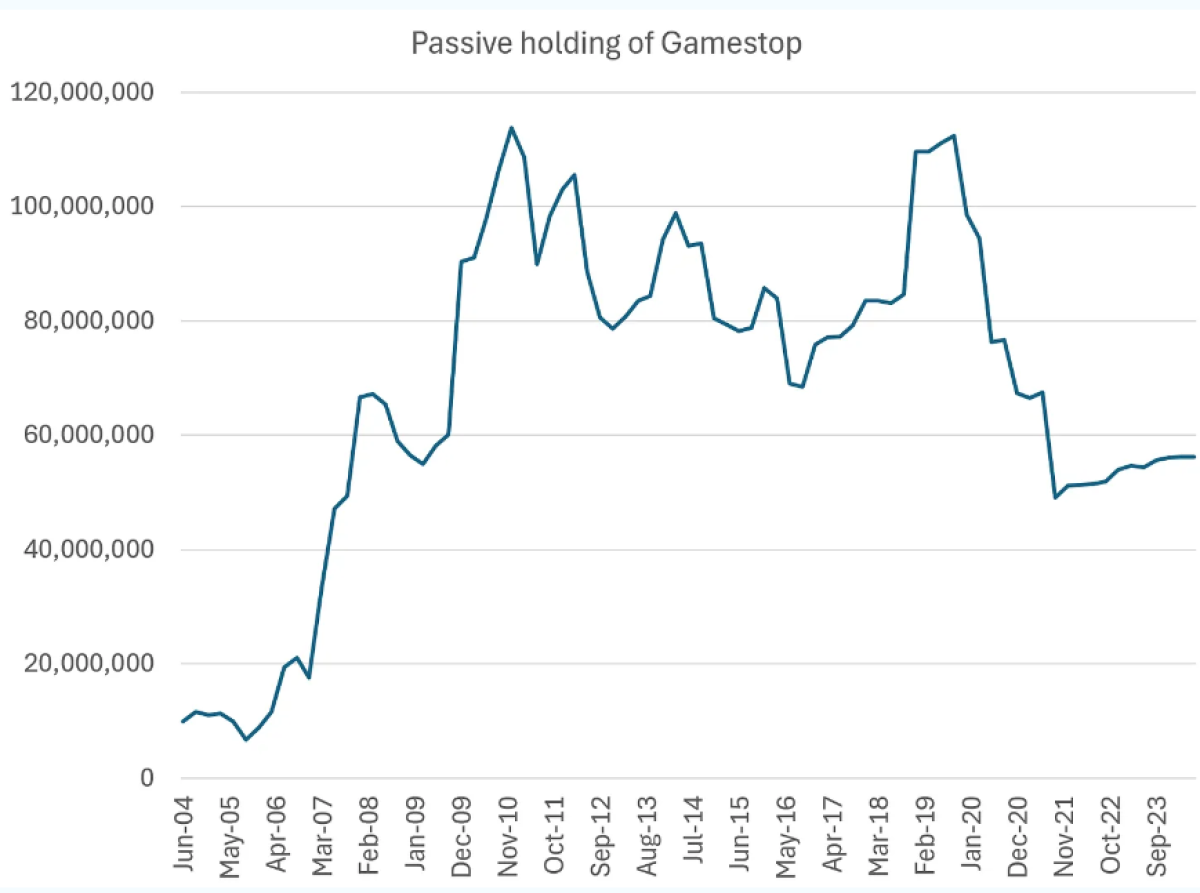

Interestingly enough, Gamestop had a very similar trajectory. As the company aggressively bought back shares under the insistence of Michael Burry in Q3 &Q4-2019, Vanguard and Blackrock became net sellers:

Into this selling, stepped Ryan Cohen…

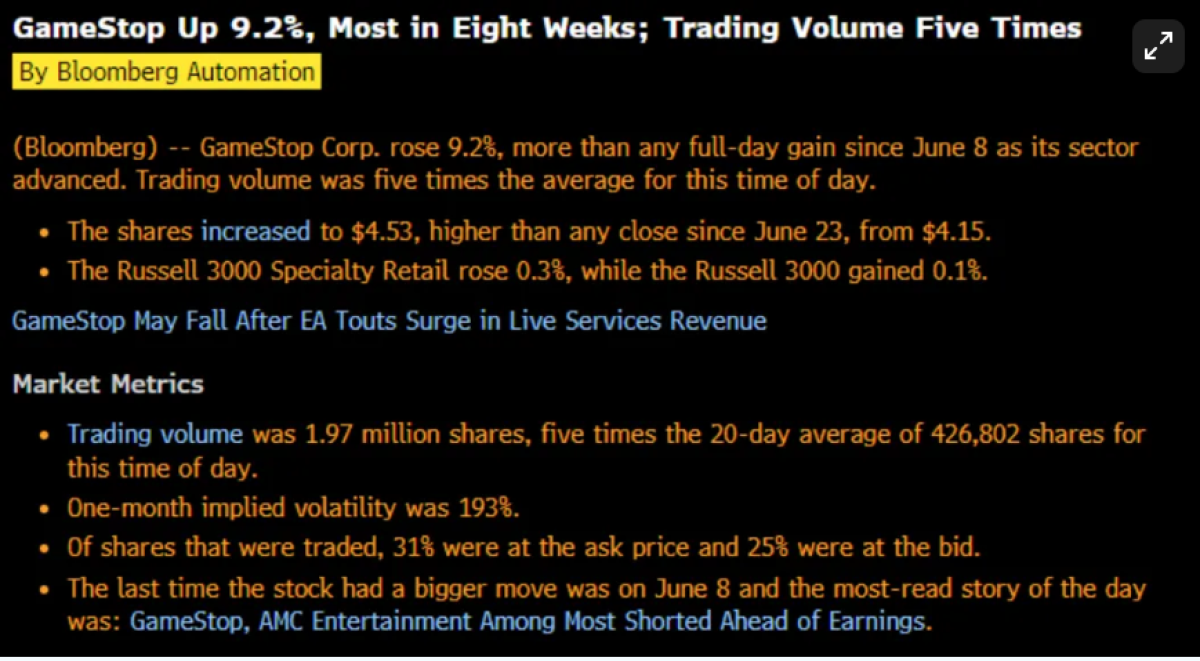

Predictably the share price began to respond to the headlines, with “apes” emboldened and shorts running for the hills. Notice that once Gamestop STOPPED buying back shares, passive began to add. And the share price went bananas:

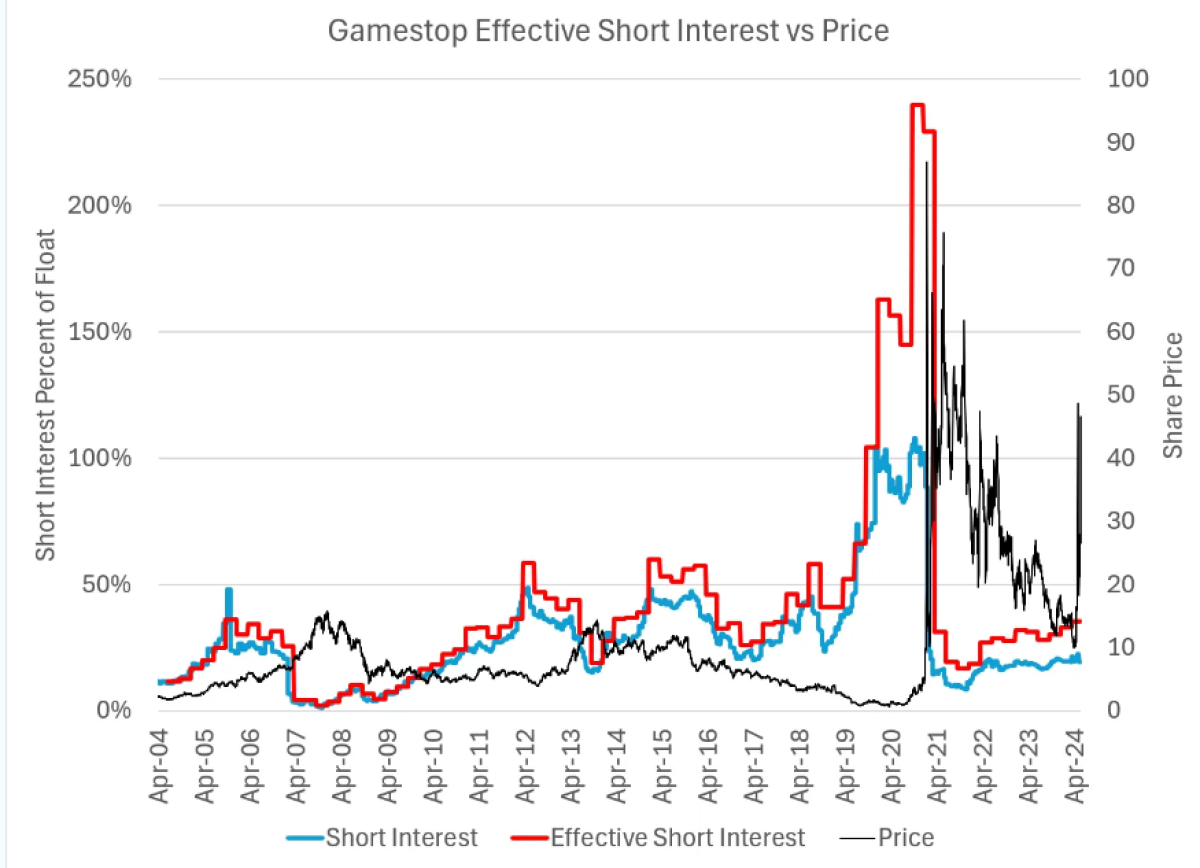

If we acknowledge that passive is simply another "insider” with no intention to sell unless the company reduces shares (or redemptions emerge), then the free float shrinks and we see just how exposed the shorts really were with nearly 250% of the effective float short. Note the strongly inverse effect as shorts added and covered in Gamestop over time. When they were forced to cover from 245%, all hell broke loose:

So Roaring Kitty was right about his short squeeze thesis. And he became very rich.

On the other side of the table, the shorts were demolished with losses estimated at $20B for short funds. RK’s fundamental thesis was dead wrong. Gamestop has continued to lose money and market share as videogames transitioned from physical media to streamed content. Walled “playstores” prevented a digital-based strategy. But regardless, the shorts have been wounded. I have been unable to update this chart for some reason, but the net effect is that short interest has collapsed. Bloomberg notes that short interest in the S&P is even lower at only 1.7%, just above the lows from 2001.

Headlines proclaim the death of shorts:

And it certainly does feel that way. As one of my readers noted last week:

Genuine question - if your theories are suggesting up... why not be long? You seem to have such a solid thesis on passive which suggests markets continue to grind higher -- but simultaneously believe markets shouldn't go up based on fundamentals? Aren't those two views inconsistent?

This is a great question and as I noted previously, “I wish I had listened to myself.”

The answer, of course, is I continue to believe that a reversal in flows is at hand. So far, through May 2024, it appears that flows have slowed and possibly reversed. Importantly, we do not have Vanguard mutual fund flows for June until later this month. We are still operating off of May data. And while there was a modest rebound in mutual fund shares in May, that was offset by ETF share declines (suggests tax trading). On net, May was down:

As a result, I continue to believe that a reversal is ahead with economic weakening. But if this proves wrong, then I will be wrong. Which is great place to pause for this note.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Michael Green, CFA, has been a student of markets and market structure, for nearly 30 years. His proprietary research into the shift from actively managed portfolios and investment funds to systematic passive investment strategies has been presented to the Federal Reserve, the BIS, the IMF and numerous other industry groups and associations.

Michael joined Simplify in April 2021 after serving as Chief Strategist and Portfolio Manager for Logica Capital Advisers, LLC. Prior to Logica, Michael managed macro strategies at Thiel Macro, LLC, an investment firm that manages the personal capital of Peter Thiel. Prior to Thiel, Michael founded Ice Farm Capital, a discretionary global macro hedge fund seeded by Soros Fund Management. From 2006-2014, Michael founded and managed the New York office of Canyon Capital Advisors, a $23B multi-strategy hedge fund based in Los Angeles, CA, where he established their global macro strategies, managing in excess of $5B of exposure across equity, credit, FX, commodity and derivative markets.

In addition to his work as a market theorist and portfolio manager, Michael has been noted for his work as a public speaker and financial media participant. He is a graduate of the Wharton School at the University of Pennsylvania and a CFA holder.