The Deutsche Börse Group and Eurex Clearing have together issued a white paper on “How central counter-parties strengthen the safety and integrity of financial markets.”

The Deutsche Börse Group and Eurex Clearing have together issued a white paper on “How central counter-parties strengthen the safety and integrity of financial markets.”

The paper makes some now familiar arguments, though it makes them more thoroughly than is usually the case. Let’s work through them and learn what we can.

In the Beginning

The argument begins with the annus horribilis, 2008. There were three reasons why that year was so horrible, according to the authors of this paper: excessive risk taking, the interconnectedness of the market participants, and insufficient collateralization. The essential argument of the paper is that CCPs render unlikely a repeat performance, because CCPs serve as transparent and independent risk managers.

The paper “also stresses the pre-requisites for CCPs to perform their important function,” such as the highest quality standards for their own operations and governance, as set out in EMIR.

Regulatory Initiatives

In the first chapter, the authors outline the regulatory initiatives that have made the world – and will continue to make the world – a place rather different from what it was in 2008-09.

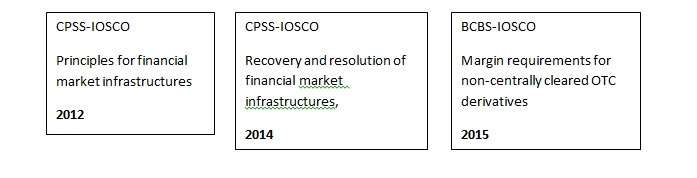

With regard to IOSCO-related regulations/principles alone there are three boxes. In timeline order from left to right they are:

[The above boxes are adapted from the white paper’s Exhibit 1.]

To decode the acronyms quickly: IOSCO, International Organization of Securities Commissions; CPSS, Committee on Payment and Settlement Systems; BCBS, Basel Committee on Banking Supervision.

Moving to a national/regional level: the U.S. Congress passed the Dodd-Frank Act in 2010, creating a clearing obligation for standardized OTC derivatives. This Act bifurcated regulatory responsibility between the Securities and Exchange Commission on the one hand and the Commodity Futures Trading Commission on the other. The bifurcation is from a high altitude a simple one. The CFTC is to regulate swaps, swap dealers and major swap dealers insofar as they are not securities-based: the SEC takes over insofar as they are.

In 2012, a new regulation of the European Parliament came into force. Known as the European Market Infrastructure Regulation (EMIR), its provisions depended on the development of regulatory technical standards and implementing technical standards, and these RTS/ITS’ took some time to come online. Certain of them that came into force in March 2013 related to the clearing obligation, risk mitigation techniques, and registration of trade repositories.

The clearing obligation of standardized ORC derivatives will in turn come into force via EMIR next year, 2015.

Later still, in 2017, MiFID II and MiFIR will require higher transparency of the OTC derivatives market.

Enthusiasm and Memory

The authors, enthusiasts for the benefits of central clearing, invoke the failure of AIG in particular as an object lesson.

“Due to diverging incentives,” they write, “AIG suffered from a lack of risk management skills. In August 2007, Joseph J. Cassano, Head of AIG Financial Products Division, stated that ‘it is hard for us, without being flippant, to even see a scenario within any kind of realm of reason that would see us losing one dollar in any of these transactions’” [i.e. a derivatives portfolio in the FP Division with a notional value of $2.7 trillion.]

They do not believe, though, that the excessive risk of that portfolio, especially the credit default swap portion thereof, can be attributed solely to the failure of internal risk management. The context was one of bilateral counterparties who “did not require appropriate collateralization of CDS transactions, given AIG’s AAA credit rating.” That is precisely what a CCP would add.

But by the third chapter the white paper raises a critical question: won’t the CCP’s themselves in a not-distant scenario simply become in turn the “too big to fail” institutions that could come under stress. Are they all that different from the AIGs or Bear Stearns’ of the world?

The authors don’t take any such parallel very seriously. After all, a CCP “does not take on proprietary risk and reflects the risk exposure by neutral valuation and prudent collateralization.” And there is always the calming prospect of multilateral netting.

One related question that these enthusiasts don’t seem to have addressed adequately, though, is the matter of collateral shock. If everyone needs to post the same assets as collateral with the same CCPs, then isn’t it clear that the market value of those assets will be arbitrarily inflated, with a range of distortive consequences?