By Andrew Smith, CAIA

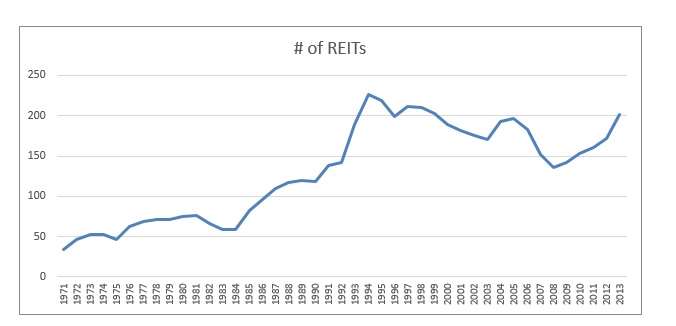

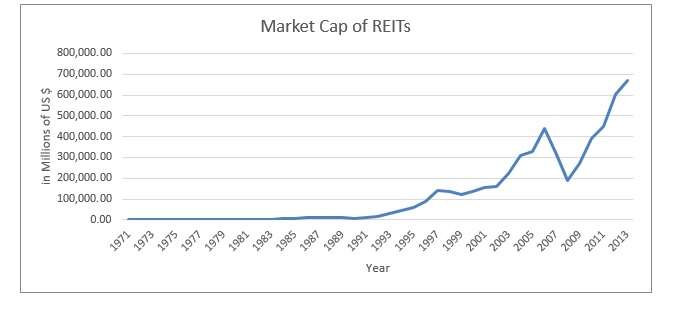

Liquid alternative investments have exploded over the past decade. Post 2007-2009 financial crisis individual investors, their advisors, and institutional investors alike sought investment opportunities to provide risk diversification, return enhancement and inflation hedging characteristics without sacrificing liquidity or transparency. Many investors, both professional and individual, believe that liquid alternatives are a new commodity; however they have been around for quite some time. It is true that the explosive growth in alternative mutual and exchange traded funds has largely taken place over the past half-decade or so, but the liquid alternative market, as a whole, is much broader than simply alternative mutual and exchange traded funds. Liquid alternatives, by definition, are any investment funds that are tradable, on a daily or intraday basis, that provide investors’ exposure to assets that fall outside the traditional “box” of stocks, bonds & cash. When past generations wanted to make investments, they had very few options. Publicly listed stocks or bonds, bank products such as CDs, cash like investments such as money market funds, and private investment opportunities. The final being high risk, typically carrying no liquidity, no transparency, and the need for expertise in the sector. Over the past 4 decades there have been vast strides made to bring alternative investments such as real estate, commodities, active investment funds, private equity funds, and non-traditional real estate holdings such as oil & gas properties, farmland, timberland, etc. to the mainstream public, in a liquid, regulated, transparent package. While the investment company act of 1940 has long allowed for the creation, operation, marketing and thus investment in mutual funds that provide alternative asset exposure, the first Liquid Alternative Funds to gain traction were Publicly Listed Real Estate Investment Trusts, or REITs. REITs began being offered at the end of the 1950s, however they were widely unknown investment opportunities. In 1971 there were only 34 REITs in total, carrying assets under management, as measured by market capitalization, of $1.494 Billion. Since the 1970s, the REIT market has grown 60-fold in AUM to over $670 billion in total AUM, and 6-fold in number of REITs offered to 202 in 2013, according to NAREIT. Other real estate opportunities have gained popularity as well, such as Timberland Investment Management Organizations (TIMOs), though not nearly the popularity of REITs. Below are two charts, first showing the growth in the number of listed REITs, followed by one showing growth in AUM of REITs.

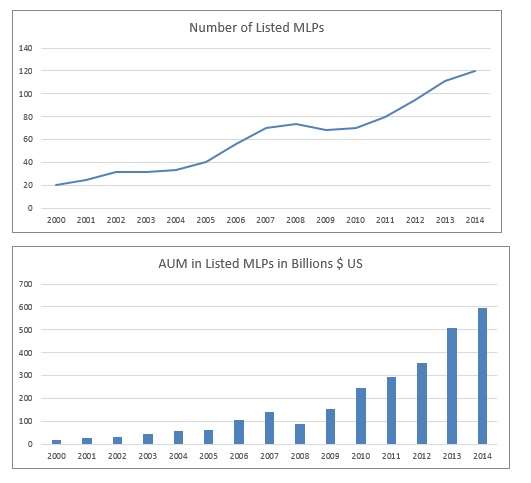

Listed REITs offer investors exposure to the vast, global, real estate market, with intraday tradability. Listed REITs also offer investors, who seek real estate exposure, professional asset management. The demand for liquid real estate exposure was, and remains elevated, particularly after the lack of liquidity and lumpiness of private real estate ownership burned a large number of real estate investors in the 2007-2009 financial crises. As mentioned earlier, other investment opportunities in real estate, or real assets for a broader definition, have long existed, only recently to garner popularity in a liquid, transparent, regulated and accessible package. Oil and gas opportunities have always intrigued investors, as the demand, globally, for energy commodities have, and will continue to increase as the world develops. Dependency on fossil fuels creates an opportunity to generate healthy returns, with inflation hedging characteristics. Publicly listed Master Limited Partnerships (MLPs) have made these opportunities accessible to all investors. The Listed MLP market has exploded over the past 2 decades, and particularly since the financial crisis of 2007-2009. In 2000, there were only 20 listed MLPs, with a total AUM, measured by market capitalization, of $16billion. At the beginning of 2014, that market had grown to over 120 MLPs with over $590 Billion in AUM. Since 2008, AUM in MLPs, which bottomed at $89billion, has grown more than 6-fold and the number of funds has increased by over 75%, from 68 at the end of 2008, to current levels.

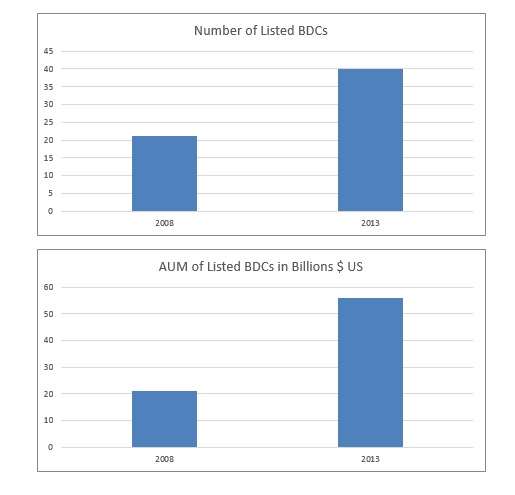

There are a number of reasons for the explosive growth in this market, however the two most compelling are the inflation hedging benefits and the tax-advantaged status of the MLP vehicle. Listed MLPs are one of the best inflation hedges, providing investors both an infrastructure and commodity exposure. Listed MLPs distribute a lot of cash, as a mandate of their existence, providing investors a stable income investment opportunity, but they also carry significant tax advantages, and with the majority of current US investors entering, or getting close to their retirement tax advantaged income is in high demand. Factors, such as diversification, liquidity and transparency in a market that previously had little opportunity to diversify due to very few funds with high minimum investments, no liquidity, and a significant lack of transparency add to the appeal of listed MLPs, and have drawn individual investors, investment advisors, and institutional investors to increase their allocations to listed MLPs. The charts above highlight this demand in a visual format. Liquid alternative investment opportunities are not confined to the real estate/real asset sectors. The private equity market, a traditionally highly complex and non-transparent asset class with virtually no liquidity, has begun its shift into the liquid alternative space with the listing, increased awareness towards, and growing popularity of Business Development Companies (BDCs). Listed BDCs are the first publicly listed private equity funds, accessible by individual and institutional investors alike. While not all BDCs are listed, many more are choosing a public stock exchange as an outlet to not only raise capital and garner a public valuation, but offer investors liquidity and transparency. BDCs are not as broad of a private equity exposure as many investors would like, focusing mostly on middle market growth companies that are preparing for strategic sale of public offering, however it is an exposure to private equity, particularly for those investors that have been shunned from the market due to high minimum investments and investor qualification rules. The listed BDC market is young, and still growing, but just since 2008, the number of listed BDCs has nearly doubled, and the assets under management in the listed BDCs has nearly tripled. BDCs are the liquid alternative to private structure private equity funds, and are a liquid alternative investment, offering liquid exposure to private equity through public stock exchanges. Below are two charts, the first shows the growth in the number of listed BDCs in 2008 and again in 2013, the second highlights the growth in listed BDC assets under management.

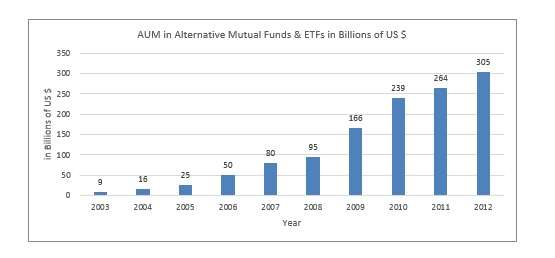

As can clearly be seen, the number of, the popularity of and the awareness towards listed BDCs as a liquid private equity fund has grown significantly, and likely will continue to, as institutional investors intend to increase their private equity allocations to nearly double their current level by 2030, according to Preqin. Liquid alternatives serve a useful purpose in both the individual and institutional portfolio. As discussed in this posting, Real Estate, Real Assets & Private Equity has become significantly more accessible with the listing of REITs, MLPs and BDCs, however, most non-institutional investors have also suffered from a lack of exposure to actively managed alternative investment funds that employ sophisticated trading strategies, developed and operated by “Wall Street” professionals with significant knowledge. These funds, commonly known as hedge funds, have always lacked accessibility, carried high minimum investments, complex fee structures, and only provided liquidity when the manager of said funds was willing. Both Pre & Post financial crisis, investors in hedge funds sought better alternatives, the alternative mutual and exchange traded fund business exploded. Alternative mutual & exchange traded funds offer investors exposure in actively managed, long/short commodity, equities, & fixed income strategies, domestically, region specific and/or globally. There is a broad range of various strategies, whether simply value oriented and actively managed, or focused on a specific situation such as merger arbitrage, or some other specialty. In 2003 there was only $9billion in AUM in alternative mutual funds & ETFs, by 2008 it had grown 10 fold, at the end of 2012, total AUM in alternative mutual funds & ETFs reached over $300billion. This chart demonstrates the enormous growth in popularity of these liquid alternative funds.  As has been detailed throughout this post, investors today have the ability to build a truly diversified portfolio, gaining exposure to asset classes such as real estate, real assets (oil & gas land, timberland, commodities, infrastructure), private equity & hedge funds, without sacrificing the liquidity of their portfolio. Capital markets today are far more competitive than they were when our parents and grandparents were building their wealth through investing. For generations, the only investment options were stocks, bonds, bank products, cash-like investments such as money market funds, and private investment deals. This presented a massive challenge to the average investors attempting to build a diversified, long-term portfolio, particularly maintaining a high level of liquidity. Today, there is no excuse, whether you’re an individual investor, retail advisor, or institutional investor, for maintaining a portfolio that lacks asset or strategy diversification. There are many options that provide investors the ability to expose their portfolio to a broad spectrum of both traditional and alternative assets, as well as traditional and alternative strategies. Here in the new millennium, capital markets have evolved, and the inclusion of liquid alternative strategies allow investors of all size and sophistication to take a long-term diversified asset allocation approach, building a stable portfolio focused on delivering returns, minimizing risk, and meeting the goals of the portfolio. The evolution of the liquid alternatives market has been significant, beginning in the late 1950s, investors have seen the continuous addition of new opportunities that provide new asset and strategy exposure, and have, for the most part, taken advantage of such opportunities. Investors that have not yet participated in these new opportunities have not missed out. It is not too late for investors of all sizes to take advantage of liquid alternatives. It would be prudent of all investors to seek advice from a professional, or conduct adequate research to determine the best way to include liquid alternative opportunities in their portfolio. The growth in this market is expected to continue and new products seemingly emerge every month. While traditional investments still serve their purpose within the portfolio, it will become increasingly important, as markets become increasingly efficient from an information standpoint, to utilize alternatives if seeking to outperform or stabilize returns when investing. Liquid alternatives will likely become the preferred option for all investors, as they have already for so many. It is likely that liquid alternatives will replace the private structure funds of old, if not entirely, significantly, due to the increase in transparency and the ability to redeem funds quickly and easily, as needed.

As has been detailed throughout this post, investors today have the ability to build a truly diversified portfolio, gaining exposure to asset classes such as real estate, real assets (oil & gas land, timberland, commodities, infrastructure), private equity & hedge funds, without sacrificing the liquidity of their portfolio. Capital markets today are far more competitive than they were when our parents and grandparents were building their wealth through investing. For generations, the only investment options were stocks, bonds, bank products, cash-like investments such as money market funds, and private investment deals. This presented a massive challenge to the average investors attempting to build a diversified, long-term portfolio, particularly maintaining a high level of liquidity. Today, there is no excuse, whether you’re an individual investor, retail advisor, or institutional investor, for maintaining a portfolio that lacks asset or strategy diversification. There are many options that provide investors the ability to expose their portfolio to a broad spectrum of both traditional and alternative assets, as well as traditional and alternative strategies. Here in the new millennium, capital markets have evolved, and the inclusion of liquid alternative strategies allow investors of all size and sophistication to take a long-term diversified asset allocation approach, building a stable portfolio focused on delivering returns, minimizing risk, and meeting the goals of the portfolio. The evolution of the liquid alternatives market has been significant, beginning in the late 1950s, investors have seen the continuous addition of new opportunities that provide new asset and strategy exposure, and have, for the most part, taken advantage of such opportunities. Investors that have not yet participated in these new opportunities have not missed out. It is not too late for investors of all sizes to take advantage of liquid alternatives. It would be prudent of all investors to seek advice from a professional, or conduct adequate research to determine the best way to include liquid alternative opportunities in their portfolio. The growth in this market is expected to continue and new products seemingly emerge every month. While traditional investments still serve their purpose within the portfolio, it will become increasingly important, as markets become increasingly efficient from an information standpoint, to utilize alternatives if seeking to outperform or stabilize returns when investing. Liquid alternatives will likely become the preferred option for all investors, as they have already for so many. It is likely that liquid alternatives will replace the private structure funds of old, if not entirely, significantly, due to the increase in transparency and the ability to redeem funds quickly and easily, as needed.

Andrew N. Smith, CAIA is a Co-Founder and Chief Product Strategist for OWLshares and serves as the chairperson of the Steering Committee for the Los Angeles Chapter of the CAIA Association.