By Fritz Louw and Niel Harmse

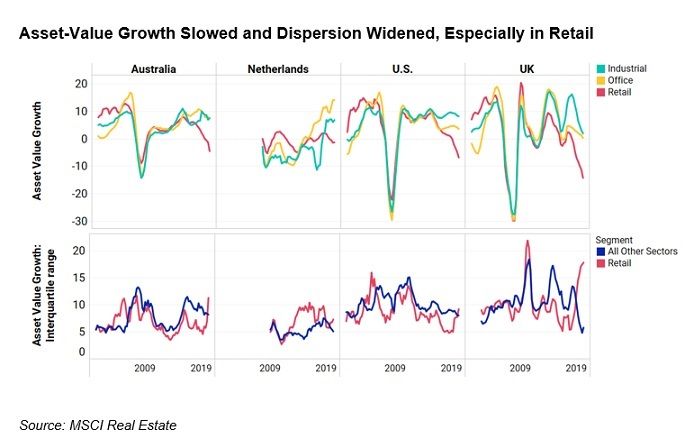

- The recent market turmoil has resembled the global financial crisis and other volatile periods, in that we have observed a widening of the dispersion of returns across real estate assets.

- This widening spread has been most pronounced in retail property — a sector that was under pressure long before the COVID-19 pandemic — particularly in the U.K.

- Given the increased dispersion of returns, institutional investors may wish to pay closer attention to asset selection and conduct more granular performance analysis.

As the old adage goes, economic expansions don’t die of old age. This expansion is no different. Many real estate markets were showing signs of a slowdown before anyone had heard of social distancing. But the COVID-19 crisis seems to have been this cycle’s grim reaper. Has this correction been similar to previous ones? The global financial crisis (GFC) is an obvious comparison due to its global nature. The GFC was marked by synchronized declines across real estate sectors. That decline stands in stark contrast to today’s performance landscape, where long-running structural changes to the use of retail and industrial space have caused very different investment outcomes over recent years. The more recent impact of COVID-19 has merely accelerated these trends. What remains similar, though, is that the dispersion of returns within underperforming sectors, such as retail, is widening. This cross-sectional dispersion of returns highlights the importance of asset selection and taking a more granular analysis of performance within segments and sectors. This way, real estate investors can better understand potential drivers of returns. To illustrate, we looked at data from four markets in different global regions: the U.S., U.K., Netherlands and Australia. COVID-19: A Secular or Pervasive Crisis for Real Estate? Real estate returns began declining more sharply when COVID-19 started affecting global markets. As we’ve noted, its real estate impact has been more localized, unlike during the GFC. The key difference: The drop in asset-value growth and widening performance dispersion have so far been more sector-specific, with retail the hardest hit, as can be seen in the exhibit below. A combination of reduced overall consumer spending, mandatory lockdowns in scores of countries and significant uncertainty about the future of the sector weighed heavily on retail-property valuations. The interquartile range[1] in the charts below highlights how periods of high uncertainty may be reflected in increased dispersion of returns, whether with broad co-movement of sectors and geographies, as we saw during the GFC, or on a localized basis. (For example, the U.K. experienced a wider returns dispersion after the Brexit referendum in June 2016). The current widening of the interquartile range echoes the GFC insofar as that such wide dispersions, even limited to certain sectors or geographies, have been uncommon outside periods of significant market volatility. And it reminds us that, on an asset level, real estate performance can be highly varied during periods of heightened uncertainty.  It is important to note that the weakness in retail real estate predates the COVID-19 crisis. In all four markets we examined, asset-value growth in retail either peaked before the GFC or briefly surged during the subsequent recovery (in the U.K.) before embarking on its secular decline. In recent years we’ve seen that the interquartile range of asset-value growth tends to spike when that growth reaches a turning point or approaches zero. This seems relatively more pronounced for the retail sector. The relative weakness of retail versus other sectors is common across all four markets — and has been for quite some time. The Devil Is in the Dispersion We are still in the early days of seeing how COVID-19 may play out for real estate. The data we used in this analysis was limited to the end of first quarter of 2020. Many lockdowns didn’t start until March, and it remains to be seen how variants of continued lockdown across the globe impacted each of the property sectors. What is, however, clear is that COVID-19 has already had an unequal impact on asset classes, geographies and sectors. If the individual assets or property types (e.g., shopping malls in retail) were more uniform within a given sector, one might expect that sector’s overall returns to vary over time; but one would not expect dramatic shifts in the dispersion of returns, as we have seen during uncertain times. In reality, we know that individual assets vary along many dimensions (income duration, exposure to tenant industries and their credit strength, to name just a few). Each of these characteristics may determine how quickly and to what extent the assets’ returns are impacted by broader market movements like those created by COVID-19. A widening performance dispersion within real estate sectors and geographies reminds us that not all assets are created equal within these broader classifications. In particular, it is a reminder that asset selection has long played an important role in the real estate investment process — and that an in-depth analysis of more granular data, at the sub-sector or even asset level, can help investors understand the factors that really drove performance. Further reading: Real Estate Asset Selection Mattered — Especially in a Crisis Private real estate: From asset class to asset How COVID-19 could impact private real estate values Real estate is about more than location during uncertain times [1] Interquartile range is the difference between the 75th and 25th percentiles of a distribution.

It is important to note that the weakness in retail real estate predates the COVID-19 crisis. In all four markets we examined, asset-value growth in retail either peaked before the GFC or briefly surged during the subsequent recovery (in the U.K.) before embarking on its secular decline. In recent years we’ve seen that the interquartile range of asset-value growth tends to spike when that growth reaches a turning point or approaches zero. This seems relatively more pronounced for the retail sector. The relative weakness of retail versus other sectors is common across all four markets — and has been for quite some time. The Devil Is in the Dispersion We are still in the early days of seeing how COVID-19 may play out for real estate. The data we used in this analysis was limited to the end of first quarter of 2020. Many lockdowns didn’t start until March, and it remains to be seen how variants of continued lockdown across the globe impacted each of the property sectors. What is, however, clear is that COVID-19 has already had an unequal impact on asset classes, geographies and sectors. If the individual assets or property types (e.g., shopping malls in retail) were more uniform within a given sector, one might expect that sector’s overall returns to vary over time; but one would not expect dramatic shifts in the dispersion of returns, as we have seen during uncertain times. In reality, we know that individual assets vary along many dimensions (income duration, exposure to tenant industries and their credit strength, to name just a few). Each of these characteristics may determine how quickly and to what extent the assets’ returns are impacted by broader market movements like those created by COVID-19. A widening performance dispersion within real estate sectors and geographies reminds us that not all assets are created equal within these broader classifications. In particular, it is a reminder that asset selection has long played an important role in the real estate investment process — and that an in-depth analysis of more granular data, at the sub-sector or even asset level, can help investors understand the factors that really drove performance. Further reading: Real Estate Asset Selection Mattered — Especially in a Crisis Private real estate: From asset class to asset How COVID-19 could impact private real estate values Real estate is about more than location during uncertain times [1] Interquartile range is the difference between the 75th and 25th percentiles of a distribution.

Interested in contributing to Portfolio for the Future? Drop us a line at content@caia.org