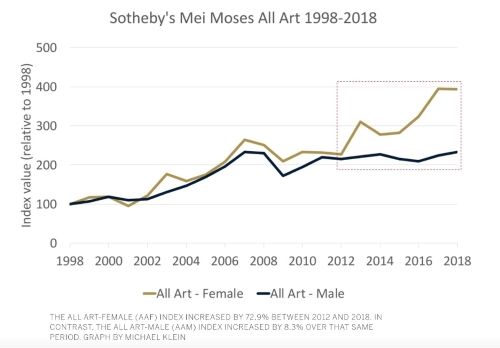

By Arthena's Art Market Research Team The effects of recessions on fine art prices are, without a doubt, the topic most-opined-about in our industry’s relatively small financial news echo chamber. Any hint of a market slowdown tends to flood our inboxes with an unyielding torrent of analysis, evidenced by the slew of articles in 2019 alone (a year many analysts feared might signal the start of a new recession before we realized how small ourproblems really were). On the one hand, we can prove, using historical data, the existence of opportunities for systematic investment strategies within the art market that yield returns uncorrelated with general market crashes. On the other hand, no amount of risk assessment has ever perfectly encapsulated future events, so there will always be contingencies and concerns to keep us hunched over the keyboard as we rifle anxiously through our digital feeds. Today, amidst the panic of the pandemic era, art investors face a difficult question in deciding which articles to believe and which sectors of the market to grant their attention. Unfortunately, much of the published advice on the subject of global market uncertainty can seem contradictory at first glance. Some articles, like Doug Woodham’s April 29th editorial for Artsy, advocate aggressive bargain hunting as prices collapse. Woodham advances the compelling argument that dealers will have to compromise on prices for all but their most premium works, signaling an opportunity for those few buyers who can afford to enter the market speculatively.1 Other industry voices fear a longer road to recovery, however, and Anny Shaw’s April 28th column for the Art Newspaper posits that the art market’s hopes rest not with individual investors but with a broader macroeconomic shift toward new centers of wealth in Asia.2 It can be tempting to latch onto one piece of concrete and simplifying advice as an anchor in stormy seas, but the truth of the matter is that market analysis becomes inherently more nuanced and more difficult to summarize when time-honored axioms begin to fail. For this reason, in an effort to provide a good-faith accounting of Arthena’s various investment considerations during the present market volatility, we’ve assembled a brief literature review below, accompanied by some of the most telling case studies from our historical data on repeat artwork sales that demonstrate the drivers of valuations over time.  Literature Review Last spring, Artnet News published the report, “Want to Be a Crash-Proof Collector? Here Are 3 Things to Do to Stay Ahead of the Art Market During a Recession.”3 Relying on aggregate auction data, this article highlighted a key concept that many observers might have guessed intuitively: “great works can still fetch great prices in downturns.”4 The core thesis of the article suggested that works of high quality are never truly at risk from flagging demand. The argument is a familiar one. Unlike lower-priced works, which can be understood as fair-weather purchases for aspirational market participants who turn away from the industry during times of economic stress, true masterpieces command the attention of wealthy consumers insulated from market shocks. In other words, blue chip works will always sell. As further evidence in support of top works’ persistent cachet, an enlightening 2019 article from Sotheby’s and Art Agency Partners’ joint advisory publication, In Other Words, described the important phenomena responsible for the rise of the market for female artists.5 Citing data from their Mei Moses indices, Sotheby’s explored trends around some of the public market’s top-performing artists, for whom demand almost always outstrips a strictly limited supply. In a bid to normalize valuations at the top of the market, the article contends, buyers must continuously re-contextualize their admiration for the cultural icons of art history by comparing their works to overlooked yet equally important contemporaries. As author Michael L. Klein puts it, “when the market runs out of art produced by its superstars, it tends to move onto related areas for supply.” Hence, the rise of female artists during the last decade, whose works’ latent value required only a small margin of breathing room to incite rightfully enthusiastic demand at the top of the public auction market. Judging by the appreciation in Sotheby’s Mei Moses All Art Female (AAF) index (below), there is certainly still untapped potential for strong returns in higher-valued masterpieces within new collecting categories.

Literature Review Last spring, Artnet News published the report, “Want to Be a Crash-Proof Collector? Here Are 3 Things to Do to Stay Ahead of the Art Market During a Recession.”3 Relying on aggregate auction data, this article highlighted a key concept that many observers might have guessed intuitively: “great works can still fetch great prices in downturns.”4 The core thesis of the article suggested that works of high quality are never truly at risk from flagging demand. The argument is a familiar one. Unlike lower-priced works, which can be understood as fair-weather purchases for aspirational market participants who turn away from the industry during times of economic stress, true masterpieces command the attention of wealthy consumers insulated from market shocks. In other words, blue chip works will always sell. As further evidence in support of top works’ persistent cachet, an enlightening 2019 article from Sotheby’s and Art Agency Partners’ joint advisory publication, In Other Words, described the important phenomena responsible for the rise of the market for female artists.5 Citing data from their Mei Moses indices, Sotheby’s explored trends around some of the public market’s top-performing artists, for whom demand almost always outstrips a strictly limited supply. In a bid to normalize valuations at the top of the market, the article contends, buyers must continuously re-contextualize their admiration for the cultural icons of art history by comparing their works to overlooked yet equally important contemporaries. As author Michael L. Klein puts it, “when the market runs out of art produced by its superstars, it tends to move onto related areas for supply.” Hence, the rise of female artists during the last decade, whose works’ latent value required only a small margin of breathing room to incite rightfully enthusiastic demand at the top of the public auction market. Judging by the appreciation in Sotheby’s Mei Moses All Art Female (AAF) index (below), there is certainly still untapped potential for strong returns in higher-valued masterpieces within new collecting categories.  Crucially, however, Artnet’s 2019 article qualified the assertion that expensive works are good investments by acknowledging key disparities in price volatility for different estimate brackets and geographies, picking out a “sweet-spot” for price stability. According to Artnet, the most consistent stores of value were found in works by recognizable artists estimated between $100K and $1M in major auction markets like New York and London. Beyond these boundaries, Artnet admitted, especially in the truly exceptional $10 M+ range, prices become so large and sales so infrequent that volatility proves inevitable. As if to emphasize the importance of this last caveat, Artnet Executive Editor, Julia Halperin, recently published a March 2020 auction review demonstrating that lower-priced works are, in fact, responsible for the bulk of the auction market’s resilience this spring, as sellers collectively pull back on the rates at which they typically consign masterpieces.6 It would seem, therefore, that both low-priced and high-priced works present their own sets of risks and opportunities.

Crucially, however, Artnet’s 2019 article qualified the assertion that expensive works are good investments by acknowledging key disparities in price volatility for different estimate brackets and geographies, picking out a “sweet-spot” for price stability. According to Artnet, the most consistent stores of value were found in works by recognizable artists estimated between $100K and $1M in major auction markets like New York and London. Beyond these boundaries, Artnet admitted, especially in the truly exceptional $10 M+ range, prices become so large and sales so infrequent that volatility proves inevitable. As if to emphasize the importance of this last caveat, Artnet Executive Editor, Julia Halperin, recently published a March 2020 auction review demonstrating that lower-priced works are, in fact, responsible for the bulk of the auction market’s resilience this spring, as sellers collectively pull back on the rates at which they typically consign masterpieces.6 It would seem, therefore, that both low-priced and high-priced works present their own sets of risks and opportunities.  The principle whereby extremely low-priced and extremely high-priced works suffer during downturns is no new insight. In numerous articles dating back to the ‘08-’09 Great Recession, including Artprice’s 2008 annual trends report and the New York Times’ 2009 special report, “An Investors' Guide to Art Market Pain and Opportunity,” pessimistic observers have variously classified fine art either as a discretionary expenditure, which declines when wages fall, or as a rampant bubble economy, inflated by enormous valuations at the high end.7 Logically, however, these two critiques cannot simultaneously characterize the entire market, since they imply that the art market is both highly sensitive to, and largely independent from, consumer demand. In the gray area between these two criticisms, therefore, there must be room for a segment of the art market with a devoted clientele that is nonetheless too conservatively regulated to allow prices to boom and bust with passing trends. If there is a kernel of truth in each of these bearish assessments, then there is also necessarily some middle ground where the market behaves more logically. Unfortunately, the narrative bias of each reporting source generally determines whether this stable middle ground is portrayed as a narrow crag or a wide-open field. Art sellers, like auction houses, are incentivized to exaggerate the stability of the middle market to promote their business. News outlets and analytical subscription services, by contrast, maintain a vested interest in emphasizing the risk and difficulty in navigating all sectors of the art market in order to sell more content. In an effort to sidestep hypocrisy, therefore, we present below some of the historical repeat sales that encapsulate our perspective on pricing volatility, without overstating the broader applicability of our conclusions.

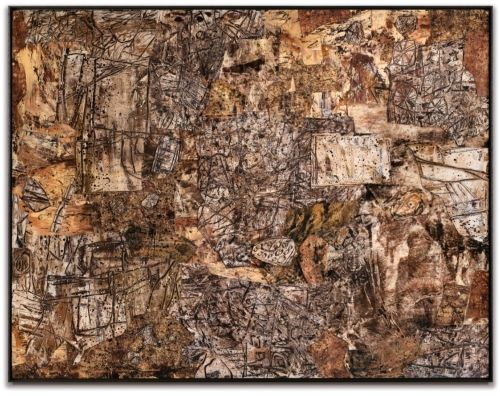

The principle whereby extremely low-priced and extremely high-priced works suffer during downturns is no new insight. In numerous articles dating back to the ‘08-’09 Great Recession, including Artprice’s 2008 annual trends report and the New York Times’ 2009 special report, “An Investors' Guide to Art Market Pain and Opportunity,” pessimistic observers have variously classified fine art either as a discretionary expenditure, which declines when wages fall, or as a rampant bubble economy, inflated by enormous valuations at the high end.7 Logically, however, these two critiques cannot simultaneously characterize the entire market, since they imply that the art market is both highly sensitive to, and largely independent from, consumer demand. In the gray area between these two criticisms, therefore, there must be room for a segment of the art market with a devoted clientele that is nonetheless too conservatively regulated to allow prices to boom and bust with passing trends. If there is a kernel of truth in each of these bearish assessments, then there is also necessarily some middle ground where the market behaves more logically. Unfortunately, the narrative bias of each reporting source generally determines whether this stable middle ground is portrayed as a narrow crag or a wide-open field. Art sellers, like auction houses, are incentivized to exaggerate the stability of the middle market to promote their business. News outlets and analytical subscription services, by contrast, maintain a vested interest in emphasizing the risk and difficulty in navigating all sectors of the art market in order to sell more content. In an effort to sidestep hypocrisy, therefore, we present below some of the historical repeat sales that encapsulate our perspective on pricing volatility, without overstating the broader applicability of our conclusions.  Case Studies Anecdotally, the idea that certain types of artworks occupy a “stable middle ground” finds confirmation among many of the most successful repeat sales in Arthena’s database. For example, the 1957 painting Célébration du Sol, by Jean Dubuffet, closely matches Artnet’s ideal parameters, consisting of a classic composition by a renowned and recognizable artist with a sales history limited to major international markets. This particular work, moreover, has never been overburdened by unwieldy low-estimates in excess of the million-dollar mark, suggesting its suitability as a safe investment.

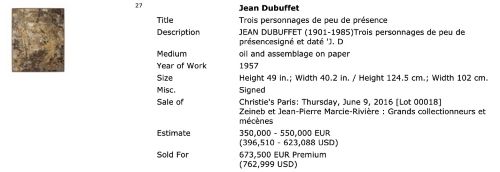

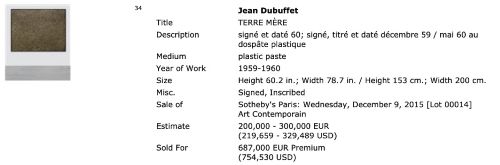

Case Studies Anecdotally, the idea that certain types of artworks occupy a “stable middle ground” finds confirmation among many of the most successful repeat sales in Arthena’s database. For example, the 1957 painting Célébration du Sol, by Jean Dubuffet, closely matches Artnet’s ideal parameters, consisting of a classic composition by a renowned and recognizable artist with a sales history limited to major international markets. This particular work, moreover, has never been overburdened by unwieldy low-estimates in excess of the million-dollar mark, suggesting its suitability as a safe investment.  Indeed, after a relatively quiet yet distinguished provenance and private transaction history, including early patronage by famed gallerist Paul Facchetti, this Dubuffet painting came to auction for the first time at Sotheby’s Paris in 2011 during the height of the art world’s post-recession recovery. Offered at a reasonable price, the lot’s performance was still modest, perhaps because its uniformly brown and understated composition hadn’t inspired the same fervor that surrounded Dubuffet’s more figurative works. The painting barely managed to sell for its low-estimate of €300,000. Subsequently, however, 2014 and 2015 proved to be excellent years for the art market before a correction and moderate volatility somewhat reset expectations in 2016. In late 2017, however, Célébration du Sol’s new owner brought it back to auction, again in Paris, where its new estimates reflected the presumed appreciation for Dubuffet’s market. By this time, several high-profile sales had clearly demonstrated that large-scale Dubuffet abstractions were in vogue with the European post-war art collectors. In 2015 and 2016, for example, two directly comparable, monochrome, abstract pieces, Trois personnages de peu de présence (1957) and Terre Mère (1959-1960), had both beaten their high estimates in Paris, each selling for almost €700,000.

Indeed, after a relatively quiet yet distinguished provenance and private transaction history, including early patronage by famed gallerist Paul Facchetti, this Dubuffet painting came to auction for the first time at Sotheby’s Paris in 2011 during the height of the art world’s post-recession recovery. Offered at a reasonable price, the lot’s performance was still modest, perhaps because its uniformly brown and understated composition hadn’t inspired the same fervor that surrounded Dubuffet’s more figurative works. The painting barely managed to sell for its low-estimate of €300,000. Subsequently, however, 2014 and 2015 proved to be excellent years for the art market before a correction and moderate volatility somewhat reset expectations in 2016. In late 2017, however, Célébration du Sol’s new owner brought it back to auction, again in Paris, where its new estimates reflected the presumed appreciation for Dubuffet’s market. By this time, several high-profile sales had clearly demonstrated that large-scale Dubuffet abstractions were in vogue with the European post-war art collectors. In 2015 and 2016, for example, two directly comparable, monochrome, abstract pieces, Trois personnages de peu de présence (1957) and Terre Mère (1959-1960), had both beaten their high estimates in Paris, each selling for almost €700,000.

In light of these points of comparison, the 2017 auction for Célébration du Sol featured an optimistic, revised low-estimate of €700,000, hopeful to make good on the artist’s rising market despite 2016’s lackluster performance. Ultimately, however, this seemingly ambitious estimate was still perhaps not high enough, and Célébration du Sol hammered for €1,200,000, finally establishing the rightful market position for this style of abstract monochrome painting among Dubuffet’s oeuvre. The collector, whose initial purchase of €360,750 had appreciated to €1,449,000 with premium, realized a net CAGR for his investment of over 22%. The initial 2011 purchase had, in fact, been a bargain. Naturally, works purchased for truly exceptional bargain prices are liable to increase in value over time, almost irrespective of volatility. but how do artworks fare when they are subjected to awkward and sub-optimal market conditions or poor transaction timing?

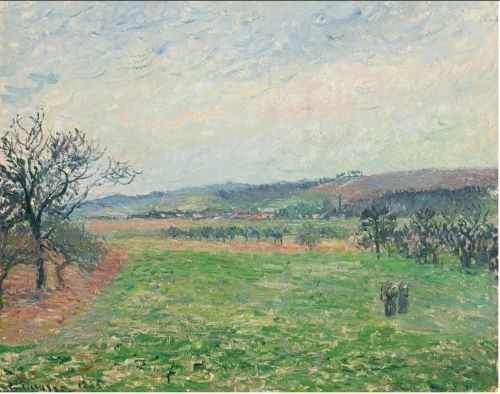

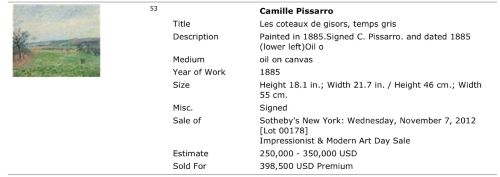

In light of these points of comparison, the 2017 auction for Célébration du Sol featured an optimistic, revised low-estimate of €700,000, hopeful to make good on the artist’s rising market despite 2016’s lackluster performance. Ultimately, however, this seemingly ambitious estimate was still perhaps not high enough, and Célébration du Sol hammered for €1,200,000, finally establishing the rightful market position for this style of abstract monochrome painting among Dubuffet’s oeuvre. The collector, whose initial purchase of €360,750 had appreciated to €1,449,000 with premium, realized a net CAGR for his investment of over 22%. The initial 2011 purchase had, in fact, been a bargain. Naturally, works purchased for truly exceptional bargain prices are liable to increase in value over time, almost irrespective of volatility. but how do artworks fare when they are subjected to awkward and sub-optimal market conditions or poor transaction timing?  Camille Pissarro (1830–1903) Les Coteaux de Gisors, Temps Gris (1885) Oil on canvas, 46 x 55 cm;18.1 x 21.7 in. The Camille Pissarro oil painting Les Coteaux de Gisors, Temps Gris (above) may represent an enlightening example of a blue-chip lot exposed to complex and challenging market forces. Auctioned at Sotheby’s in New York during the height of 2012’s bull run, Les Coteaux fetched a sale price of $398,500 with premium ($330,000 hammer). At face value, one might argue the painting sold well, almost surpassing its high estimate. Unfortunately, however, this very same work had previously failed to sell during the 2009 recession when Doyle offered it for the ambitious low estimate of $600,000. We may conjecture that the seller perhaps felt mounting pressure to liquidate this painting at the first hint of a broader market recovery, and in approaching a smaller auction house with less bargaining power, could have demanded a higher estimate than perhaps the work truly merited. In any case, the work went unsold. As auction insiders well know, a volatile transaction history tends to dissuade some collectors from betting on a work’s future value, and the Pissarro’s unsuccessful showing in 2009 might easily have earned it the notoriety of a “burned” lot. Nonetheless, three years later, with a much lower estimate and a macroeconomic tailwind, the painting’s new buyer had been willing to bid up to the newly adjusted high estimate for the work, perhaps viewing its recent history and discounted estimates as signs of a good deal.

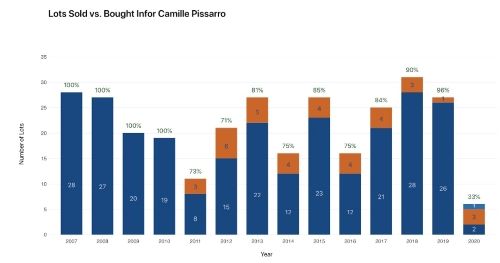

Camille Pissarro (1830–1903) Les Coteaux de Gisors, Temps Gris (1885) Oil on canvas, 46 x 55 cm;18.1 x 21.7 in. The Camille Pissarro oil painting Les Coteaux de Gisors, Temps Gris (above) may represent an enlightening example of a blue-chip lot exposed to complex and challenging market forces. Auctioned at Sotheby’s in New York during the height of 2012’s bull run, Les Coteaux fetched a sale price of $398,500 with premium ($330,000 hammer). At face value, one might argue the painting sold well, almost surpassing its high estimate. Unfortunately, however, this very same work had previously failed to sell during the 2009 recession when Doyle offered it for the ambitious low estimate of $600,000. We may conjecture that the seller perhaps felt mounting pressure to liquidate this painting at the first hint of a broader market recovery, and in approaching a smaller auction house with less bargaining power, could have demanded a higher estimate than perhaps the work truly merited. In any case, the work went unsold. As auction insiders well know, a volatile transaction history tends to dissuade some collectors from betting on a work’s future value, and the Pissarro’s unsuccessful showing in 2009 might easily have earned it the notoriety of a “burned” lot. Nonetheless, three years later, with a much lower estimate and a macroeconomic tailwind, the painting’s new buyer had been willing to bid up to the newly adjusted high estimate for the work, perhaps viewing its recent history and discounted estimates as signs of a good deal.  Over the course of the following five years, despite generally favorable conditions in the art world, Pissarro’s market performed uncharacteristically falteringly, with relatively disappointing sell-through rates (represented in the chart below). The 2012 buyer ultimately chose to consign his Pissarro back to Sotheby’s in 2017. Detractors armed with conventional auction wisdom might have called this strategy a glaring mistake, avoidable if the buyer had only paid more heed to a shaky sale record. And yet, despite buying a burned lot during a market high and selling after a disappointing year, the Pissarro’s owner was still able to muster an impressive $531,000 sale total for Les Coteaux’s next sale, against all odds. This seemingly bold strategy ultimately preserved the value of the buyer’s investment, and his work’s realized price actually grew by a fair margin despite 2016’s market dip.

Over the course of the following five years, despite generally favorable conditions in the art world, Pissarro’s market performed uncharacteristically falteringly, with relatively disappointing sell-through rates (represented in the chart below). The 2012 buyer ultimately chose to consign his Pissarro back to Sotheby’s in 2017. Detractors armed with conventional auction wisdom might have called this strategy a glaring mistake, avoidable if the buyer had only paid more heed to a shaky sale record. And yet, despite buying a burned lot during a market high and selling after a disappointing year, the Pissarro’s owner was still able to muster an impressive $531,000 sale total for Les Coteaux’s next sale, against all odds. This seemingly bold strategy ultimately preserved the value of the buyer’s investment, and his work’s realized price actually grew by a fair margin despite 2016’s market dip.  Did Les Coteaux’s intrinsic qualities account for its steady performance, as Artnet analysis might suggest? Certainly, the historical cachet of the artist name, Pissarro, carried significant weight and ensured a fair consideration for the work’s quality despite some poor sales metrics. The market for Pisarro had indeed been somewhat slower between 2012 and 2016 than in prior years, but unlike other lesser-known painters, the famous impressionist’s market never completely faded. By the time November’s New York auctions returned in 2017, other Pissarro landscapes, such as Verger a? Saint-Ouen-l'Aumo?ne en hiver, were again selling close to their high estimates, and Les Coteaux’s value held steady. Unfortunately, what had appeared to be a bargain price in 2012 was simply a fair correction. For an art purchase to qualify as a good investment, there must be sufficient evidence to uphold the conviction that an artist’s market will hold steady, but there must also be probable cause to suggest that the purchase price is a good deal. Nonetheless, in spite of challenging sales circumstances, the sales history for Les Coteaux de Gisors, Temps Gris serves to illustrate the idea that high quality art assets are surprisingly resilient to market disruptions and volatility. Conclusion When we consider any investment at Arthena, we attempt to look beyond generalizations and sparse, volatile estimates. To the best of our ability, often by relying on high-dimensional data correlations more abstract than humans can readily discern, we attempt to judge art based on its underlying value relative to its price, keeping in mind the macroeconomic factors that can cause an artist’s market to move. We believe that the basis for good art investing consists of a solid understanding of individual works’ fair market values–metrics which can be easily misrepresented or disguised by “hype,” “sentiment,” and even well-intentioned market analysis when taken out of context. During periods of widespread volatility, it becomes more critical than ever to adhere to fundamentally sound investment principles because radical shifts in methodology motivated by abstract fears and recession-specific hypotheses tend to distract us from the underlying value in art and often result in the volatile returns we would seek to avoid. All these considerations aside, however, we feel grateful to participate in a marketplace characterized by overall strong resilience to economic shocks, with physical assets anchored in an indelible history of cultural and aesthetic value. Arthena is a venture-backed financial technology company which has pioneered quantitative strategies for art asset acquisition. If you are an accredited investor or institutional investor interested in learning about current opportunities, please contact info@arthena.com or visit Arthena’s website or Instagram. Footnotes 1. https://www.artsy.net/article/artsy-editorial-advice-collectors-navigating-art-market-amid-covid-19 2. https://www.theartnewspaper.com/analysis/great-depression-of-the-21st-century-looms 3. https://news.artnet.com/market/crash-proof-three-tips-selling-art-next-market-downturn-1510171 4. https://news.artnet.com/market/art-market-recession-tips-1656103 5. https://www.sothebys.com/en/articles/where-women-outpace-men-in-the-market 6. https://news.artnet.com/market/art-market-auction-analysis-march-2020-1848597 7. https://imgpublic.artprice.com/pdf/trends2008_en.pdf https://www.nytimes.com/2009/06/10/arts/10iht-rcartus.html

Did Les Coteaux’s intrinsic qualities account for its steady performance, as Artnet analysis might suggest? Certainly, the historical cachet of the artist name, Pissarro, carried significant weight and ensured a fair consideration for the work’s quality despite some poor sales metrics. The market for Pisarro had indeed been somewhat slower between 2012 and 2016 than in prior years, but unlike other lesser-known painters, the famous impressionist’s market never completely faded. By the time November’s New York auctions returned in 2017, other Pissarro landscapes, such as Verger a? Saint-Ouen-l'Aumo?ne en hiver, were again selling close to their high estimates, and Les Coteaux’s value held steady. Unfortunately, what had appeared to be a bargain price in 2012 was simply a fair correction. For an art purchase to qualify as a good investment, there must be sufficient evidence to uphold the conviction that an artist’s market will hold steady, but there must also be probable cause to suggest that the purchase price is a good deal. Nonetheless, in spite of challenging sales circumstances, the sales history for Les Coteaux de Gisors, Temps Gris serves to illustrate the idea that high quality art assets are surprisingly resilient to market disruptions and volatility. Conclusion When we consider any investment at Arthena, we attempt to look beyond generalizations and sparse, volatile estimates. To the best of our ability, often by relying on high-dimensional data correlations more abstract than humans can readily discern, we attempt to judge art based on its underlying value relative to its price, keeping in mind the macroeconomic factors that can cause an artist’s market to move. We believe that the basis for good art investing consists of a solid understanding of individual works’ fair market values–metrics which can be easily misrepresented or disguised by “hype,” “sentiment,” and even well-intentioned market analysis when taken out of context. During periods of widespread volatility, it becomes more critical than ever to adhere to fundamentally sound investment principles because radical shifts in methodology motivated by abstract fears and recession-specific hypotheses tend to distract us from the underlying value in art and often result in the volatile returns we would seek to avoid. All these considerations aside, however, we feel grateful to participate in a marketplace characterized by overall strong resilience to economic shocks, with physical assets anchored in an indelible history of cultural and aesthetic value. Arthena is a venture-backed financial technology company which has pioneered quantitative strategies for art asset acquisition. If you are an accredited investor or institutional investor interested in learning about current opportunities, please contact info@arthena.com or visit Arthena’s website or Instagram. Footnotes 1. https://www.artsy.net/article/artsy-editorial-advice-collectors-navigating-art-market-amid-covid-19 2. https://www.theartnewspaper.com/analysis/great-depression-of-the-21st-century-looms 3. https://news.artnet.com/market/crash-proof-three-tips-selling-art-next-market-downturn-1510171 4. https://news.artnet.com/market/art-market-recession-tips-1656103 5. https://www.sothebys.com/en/articles/where-women-outpace-men-in-the-market 6. https://news.artnet.com/market/art-market-auction-analysis-march-2020-1848597 7. https://imgpublic.artprice.com/pdf/trends2008_en.pdf https://www.nytimes.com/2009/06/10/arts/10iht-rcartus.html

Interested in contributing to Portfolio for the Future? Drop us a line at content@caia.org