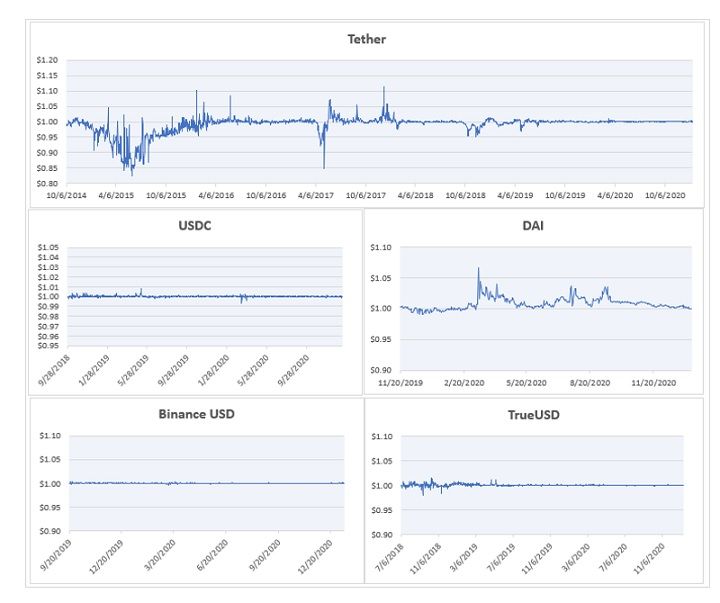

By Andrew Keenan, CAIA, CFA, CBP, Assistant Vice President at Credit Suisse INTRODUCTION The recent stratospheric rise of bitcoin and its compatriot altcoins has generated both intrigue and despair as a handful of big-name digital assets reached new apogees in 2021 with respect to price and market capitalization. In the case of intrigue, outperformance of and familiarity with bitcoin et al has led to fruitful discourse as well as interest by a plethora of Institutional Investors to start building allocations to digital assets (see the following CAIA infoseries for more on the discussion as to whether cryptoassets are indeed ready for Institutional Investors). Conversely, in the case of despair, the volatility of digital assets, regardless of how one measures it, has served as the proverbial “worst enemy” of cryptocurrencies and perhaps the most salient detractor for more widespread adoption. After all, it is hard to count on using an asset as a viable medium of exchange if its value or even a store of value if prices fluctuate wildly over a broad spectrum of time intervals and market conditions. Moreover, the parabolic rise of any asset tends to exacerbate the volatility problem by keeping traders consistently unsettled with one eye towards the metaphorical exit, trying to time their serendipitous withdrawal before the next drawdown. In the backdrop, however, is perhaps one of the key lynchpins to stymieing volatility and the despair that often accompanies it: stablecoins. The purpose of this research note, therefore, is to provide investment professionals a cursory understanding of a financial innovation within the cryptocurrency milieu that will likely receive more and more attention as investors of all stripes look for ways to garner digital asset exposure. OVERVIEW: WHAT IS A STABLECOIN? As the name implies, a stablecoin is a cryptocurrency whose price is stable—as in steady or fixed—and whose value is pegged to a secure asset such as a fiat currency (e.g. 1 unit of stablecoin is equal to 1 USD) or Commodity (e.g. 1 Unit of stablecoins is equal to the price of a gram of Gold) [1]. To achieve the said stability, different protocols or methodologies—discussed below in more detail—are utilized by issuers of stablecoins. To see just how “stable” relative to their espoused $1.00 peg stablecoins are, Exhibit 1 displays the price history of the top 5 stablecoins by market capitalization. [2] From an application standpoint, stablecoins aim to bridge the divide between the digital asset world and the fiat currency world by offering users and investors a way to have their proverbial cake and eat it too: curbed volatility coupled with the benefits provided by the decentralized, secure, transparent, and quasi-anonymous payment system afforded by blockchain technology and cryptocurrencies. At the time of this writing, the stablecoin market has grown precipitously since its genesis in ~2014 thanks to an increased number of offerings, regulation, and better supporting infrastructure. Albeit, far from the market capitalization of BTC and ETH, stablecoin’s market Capitalization has—notably--exceeded $33bn with Tether, a fiat-backed stable coin holding the third highest market capitalization across all cryptocurrencies, exceeding other big name cryptos such as LTC and Cardano. Exhibits 2 and 3 provide additional context on the composition of the Stablecoin Market as of 1/13/2021. [3] [4]  Exhibit 1: Price History of Current Top 5 Stablecoins by Market Capitalization relative to $1.00 peg Source: CoinMetrics

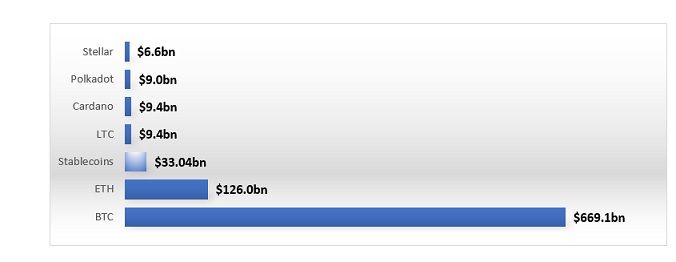

Exhibit 1: Price History of Current Top 5 Stablecoins by Market Capitalization relative to $1.00 peg Source: CoinMetrics  Exhibit 2: Size Comparison of Various Top Cryptos by Market Cap vs. Stablecoins as of 1/13/2021 Source: Coinmarketcap and Cryptoslate

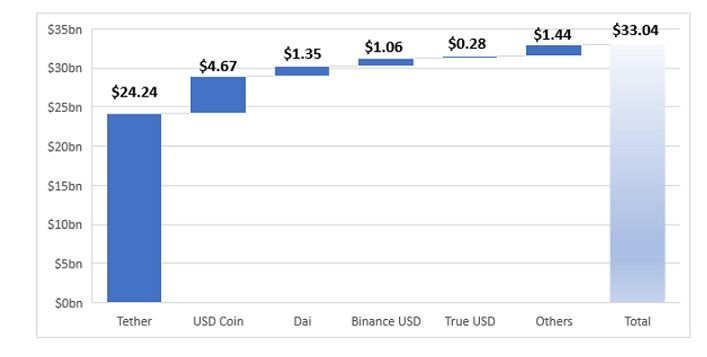

Exhibit 2: Size Comparison of Various Top Cryptos by Market Cap vs. Stablecoins as of 1/13/2021 Source: Coinmarketcap and Cryptoslate  Exhibit 3: Stablecoin Market Composition (in billions of $s) as of 1/13/2021 Source: Cyrptoslate HOW THEY WORK: PEGGING METHODS There are 3 primary pegging models in the stablecoin ecosystem. These models and how they work at a high-level are as follows (note: these are attempted generalizations; the specifics may vary by stablecoin).

Exhibit 3: Stablecoin Market Composition (in billions of $s) as of 1/13/2021 Source: Cyrptoslate HOW THEY WORK: PEGGING METHODS There are 3 primary pegging models in the stablecoin ecosystem. These models and how they work at a high-level are as follows (note: these are attempted generalizations; the specifics may vary by stablecoin).

- Algorithmic Pegging - this approach leverages smart contracts and are technically non-collateralized though some issuers may have a war chest in reserve just in case. A crude but practical way to understand the mechanics of the smart contract is as follows:

- If the price of a given stablecoin is greater than $1.00, then issue more coins (increase the supply) until the price has reverted to $1.00.

- If the price of a given stablecoin is less than $1.00, then purchase more coins (reduce the supply) until the price has reverted to $1.00.

- If the price of a given stablecoin is equal to $1.00, then no action is needed.

- Fiat Pegging - this approach leverages fiat currency as a source of collateral in a fixed ratio (e.g. 1:1) and is, at the time of this writing, the most common stablecoin pegging methodology. A practical way to understand the mechanics is as follows:

- An issuer holds $1,000,000 as collateral in a bank account, safe, or trust and issues stablecoins in a 1:1 ratio that represent that collateral.

- Users of the fiat backed stablecoin thus have 1,000,000 units approximately equivalent to 1 USD to trade in the open market.

- To increase the supply the issuer would need to house additional USD before issuing more stablecoins and vice versa if the issuer wanted to reduce the supply.

- Crypto Pegging – this approach leverages smart contracts as well as cryptocurrencies as a source of collateral in usually what tends to be an over-collateralized manner. The reason for this over-collateralization is that the collateral, which is protocol specific but is often Ether, BTC, or a basket of cryptocurrencies, used to maintain the peg is inherently volatile and therefore over-collateralization serves as a stability mechanism. A pragmatic way to understand the mechanics is as follows:

- Users will make a loan with a smart contract by putting up the specified collateral forming what is known as a Collateralized Debt Position.

- Via this Collateralized Debt Position, crypto-backed stablecoins, pegged to a specified asset such as USD, enter circulation. The user may need to conduct maintenance (akin to margin calls in the futures space) to ensure that the collateral ratio does not fall under a certain threshold (e.g. 2:1 or 200%).

- To close out the position, the user will pay back their debt to the smart contract and retrieve their collateral in exchange for the stablecoin previously generated.

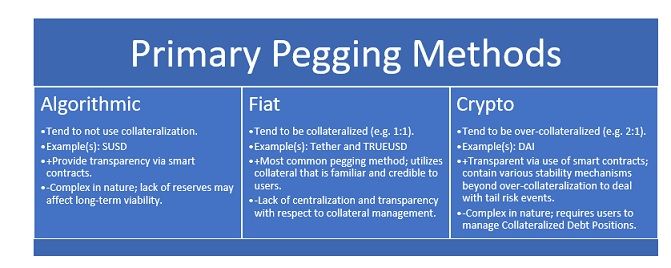

The Pegging Methods outlined and expatiated upon above [5] each come with a unique set of tradeoffs that are worth understanding in additional detail. WHAT ARE SOME DRAWBACKS TO BE AWARE OF? No system is perfect and each of the above-mentioned pegging methods is not without its own unique drawbacks, or tradeoffs to be put more euphemistically. For instance, Algorithmic pegging system’s lack of substantive reserves or collateral undergirding the stablecoin may serve as a source of apprehension for the risk averse, especially with respect to its long-term viability. In addition, adding to the already intricate nature of the pegging methodology, Blockchain data feeds that that the system rely on may be subject to inaccuracies or price manipulation, undermining trust in the pegging method that supports the associated stablecoins. [6] Fiat pegging systems face two crucial issues: centralization and transparency. With regards to centralization, unless an issuer maintains collateral in a decentralized manner (e.g. across multiple banks or financial institutions), this pegging system essentially jettisons one of the key hallmarks of blockchain technology. Concerning transparency, if the issuing entity does not have sufficient reserves in place as advertised, then a redemption may go awry if many take place contemporaneously. Consequently, users must trust that the issuing entity and, by extension, the assigned custodian indeed have the corresponding collateral required to back the stablecoin properly. [7] Crypto pegging systems also tend to be esoteric in nature and, like their algorithmic-backed counterparts, can be riddled with complexity and hard to follow dynamics that may deter users from feeling comfortable that their stablecoins are indeed stable even if the corresponding smart contracts are publicly viewable. While over-collateralization and other stability mechanisms can help deal with tail events, purchasing the collateral for and managing a Collateralized Debt Position may be a hard sell for new adopters. For the reader’s convenience, a summary of these pegging methods can be found in Exhibit 4 below. [8]  Exhibit 4 – Summary of Primary Pegging Methods PERSPECTIVE: HOW ARE STABLECOINS SUPPOSED TO MAKE AN IMPACT? The oft-cited answer to this question is that stablecoins will reduce the volatility that has plagued digital assets since their inception. But how exactly? While the true answer may be layered, technical, and nuanced, taking an Ockham’s razor approach that the “simplest answer is the best answer” is, in this author’s opinion, the way to go. As Bill Barhydt, the founder and CEO of Abra, points out that only a “massive amount of liquidity” and “a significant amount of time” will smoothen out the volatility of crypto markets [9]. He also aptly states: “Instead, stablecoins will have a role to play in broadening cryptocurrency markets. In my mind, the most promising and often overlooked application for stablecoins is their utility as on-ramps for assets moving from traditional financial markets into crypto.” [10] To that end, stablecoins are akin to dipping your toe into the pool before diving straight in. They offer potential investors a gateway into cryptocurrency markets, a realm where adoption rates and liquidity are arguably the most critical factors for the said market’s long-term success. stablecoins help alleviate the conventional fear of loss of initial capital invested because, via many current offerings, they are pegged to fiat currencies or Commodities that consumers are intimately familiar with in their daily lives. Once a new user “makes the plunge” into crypto assets via a stablecoin, they should, in most cases, expect a virtually unmoved account balance (sans transaction fees and, with some minor exceptions, subtle price movements toward or away from the peg). A first-time investment in BTC or ETH will probably not yield that same experience. Awaiting new users, regardless of motive, is the groundbreaking blockchain technologies that has been the mainstay of digital assets: an immutable, decentralized, and transparent ledger that provides a borderless payment system with no single point of failure or a robust offering of audited, publicly viewable smart contracts. Once you are in the pool, you are more likely to venture off and explore other areas of it, including the deep end! Presumably, with stablecoins comes comfort and credibility. With comfort and credibility come adoption rates. With adoption rates comes liquidity. And with liquidity comes reduced volatility. CONCLUDING THOUGHTS This research note only scratched the surface of the technicalities involved with this inchoate financial innovation and provided investment professionals with introductory definitions, mechanics, drawbacks and a perspective of how stablecoins will continue to impact the world of digital assets. On one hand, stablecoins may be the lynchpin that launch digital assets into the mainstream as they provide a bona fide manner for the next wave of adopters to test drive crypto assets without being hampered by the salient volatility. On the other hand, they are not without their own drawbacks and tradeoffs as described above such as complexity, transparency, and possible lack of centralization. Further, stablecoin’s role in the digital asset world may become moot if volatility settles on its own by other external factors. [11] Regardless, investor education is a desideratum in this rapidly changing milieu and taking the time to build an understanding of stablecoins is certainly a worthy endeavor. Andrew Keenan, CAIA, CFA, CBP is an AVP at Credit Suisse. Contact E-mail: andrew.keenan@credit-suisse.com REFERENCES [1] Shaginyan, Artem. “What Is a Stablecoin? Everything You Need to Know.” TechRadar, TechRadar Pro, 22 Dec. 2020, http://www.techradar.com/news/what-is-a-stablecoin-everything-you-need-…. [2] https://coinmetrics.io/community-network-data [3] https://cryptoslate.com/cryptos/stablecoin [4] https://coinmarketcap.com [5] CementDAO. “Stablecoin Market Problems.” Medium, CementDAO, 24 Sept. 2020, medium.com/cementdao/stablecoin-market-problems-c188dfbc04da. [6] Ibid. CementDAO. “Stablecoin Market Problems.” Medium, CementDAO, 24 Sept. 2020, medium.com/cementdao/stablecoin-market-problems-c188dfbc04da. [7] Becky. “What Is a Fiat-Backed Stablecoin? - Coininsider.” Coin Insider, 30 Oct. 2020, http://www.coininsider.com/what-is-a-fiat-backed-stablecoin/. [8] Becky. “What Is Cryptocurrency-Backed Stablecoin? - Coininsider.” Coin Insider, 30 Oct. 2020, http://www.coininsider.com/what-is-a-crypto-backed-stablecoin/. [9] Barhydt, Bill. “Stablecoins Will Do More Than Just Reduce Crypto Price Volatility.” CoinDesk, CoinDesk, 20 July 2018, http://www.coindesk.com/stablecoins-will-do-more-than-just-reduce-crypt…. [10] Ibid. Barhydt, Bill. “Stablecoins Will Do More Than Just Reduce Crypto Price Volatility.” CoinDesk, CoinDesk, 20 July 2018, www.coindesk.com/stablecoins-will-do-more-than-just-reduce-crypto-price…. [11] Beigel, Ofir. The Complete Beginner’s Guide to Stablecoins. 23 Oct. 2020, 99bitcoins.com/what-are-stablecoins/.

Exhibit 4 – Summary of Primary Pegging Methods PERSPECTIVE: HOW ARE STABLECOINS SUPPOSED TO MAKE AN IMPACT? The oft-cited answer to this question is that stablecoins will reduce the volatility that has plagued digital assets since their inception. But how exactly? While the true answer may be layered, technical, and nuanced, taking an Ockham’s razor approach that the “simplest answer is the best answer” is, in this author’s opinion, the way to go. As Bill Barhydt, the founder and CEO of Abra, points out that only a “massive amount of liquidity” and “a significant amount of time” will smoothen out the volatility of crypto markets [9]. He also aptly states: “Instead, stablecoins will have a role to play in broadening cryptocurrency markets. In my mind, the most promising and often overlooked application for stablecoins is their utility as on-ramps for assets moving from traditional financial markets into crypto.” [10] To that end, stablecoins are akin to dipping your toe into the pool before diving straight in. They offer potential investors a gateway into cryptocurrency markets, a realm where adoption rates and liquidity are arguably the most critical factors for the said market’s long-term success. stablecoins help alleviate the conventional fear of loss of initial capital invested because, via many current offerings, they are pegged to fiat currencies or Commodities that consumers are intimately familiar with in their daily lives. Once a new user “makes the plunge” into crypto assets via a stablecoin, they should, in most cases, expect a virtually unmoved account balance (sans transaction fees and, with some minor exceptions, subtle price movements toward or away from the peg). A first-time investment in BTC or ETH will probably not yield that same experience. Awaiting new users, regardless of motive, is the groundbreaking blockchain technologies that has been the mainstay of digital assets: an immutable, decentralized, and transparent ledger that provides a borderless payment system with no single point of failure or a robust offering of audited, publicly viewable smart contracts. Once you are in the pool, you are more likely to venture off and explore other areas of it, including the deep end! Presumably, with stablecoins comes comfort and credibility. With comfort and credibility come adoption rates. With adoption rates comes liquidity. And with liquidity comes reduced volatility. CONCLUDING THOUGHTS This research note only scratched the surface of the technicalities involved with this inchoate financial innovation and provided investment professionals with introductory definitions, mechanics, drawbacks and a perspective of how stablecoins will continue to impact the world of digital assets. On one hand, stablecoins may be the lynchpin that launch digital assets into the mainstream as they provide a bona fide manner for the next wave of adopters to test drive crypto assets without being hampered by the salient volatility. On the other hand, they are not without their own drawbacks and tradeoffs as described above such as complexity, transparency, and possible lack of centralization. Further, stablecoin’s role in the digital asset world may become moot if volatility settles on its own by other external factors. [11] Regardless, investor education is a desideratum in this rapidly changing milieu and taking the time to build an understanding of stablecoins is certainly a worthy endeavor. Andrew Keenan, CAIA, CFA, CBP is an AVP at Credit Suisse. Contact E-mail: andrew.keenan@credit-suisse.com REFERENCES [1] Shaginyan, Artem. “What Is a Stablecoin? Everything You Need to Know.” TechRadar, TechRadar Pro, 22 Dec. 2020, http://www.techradar.com/news/what-is-a-stablecoin-everything-you-need-…. [2] https://coinmetrics.io/community-network-data [3] https://cryptoslate.com/cryptos/stablecoin [4] https://coinmarketcap.com [5] CementDAO. “Stablecoin Market Problems.” Medium, CementDAO, 24 Sept. 2020, medium.com/cementdao/stablecoin-market-problems-c188dfbc04da. [6] Ibid. CementDAO. “Stablecoin Market Problems.” Medium, CementDAO, 24 Sept. 2020, medium.com/cementdao/stablecoin-market-problems-c188dfbc04da. [7] Becky. “What Is a Fiat-Backed Stablecoin? - Coininsider.” Coin Insider, 30 Oct. 2020, http://www.coininsider.com/what-is-a-fiat-backed-stablecoin/. [8] Becky. “What Is Cryptocurrency-Backed Stablecoin? - Coininsider.” Coin Insider, 30 Oct. 2020, http://www.coininsider.com/what-is-a-crypto-backed-stablecoin/. [9] Barhydt, Bill. “Stablecoins Will Do More Than Just Reduce Crypto Price Volatility.” CoinDesk, CoinDesk, 20 July 2018, http://www.coindesk.com/stablecoins-will-do-more-than-just-reduce-crypt…. [10] Ibid. Barhydt, Bill. “Stablecoins Will Do More Than Just Reduce Crypto Price Volatility.” CoinDesk, CoinDesk, 20 July 2018, www.coindesk.com/stablecoins-will-do-more-than-just-reduce-crypto-price…. [11] Beigel, Ofir. The Complete Beginner’s Guide to Stablecoins. 23 Oct. 2020, 99bitcoins.com/what-are-stablecoins/.