By James Walton, Investment Director, River and Mercantile.

Plan sponsors embarking on an annuity purchase should understand the impact COVID-19 has had on the insurers participating in their transaction and what this means for their safety going forward. Despite the pandemic, 2020 was a robust year for transactions and insurer balance sheets have generally held up. However, awareness of market conditions and performing due diligence of insurance providers remains of critical importance.

Over the last decade, de-risking a pension plan through the use of an annuity buyout or buy-in has become prevalent. In 2014, total annuity risk transfer sales were under $10B; in 2020 they had skyrocketed to $27B (down from $30.5B in 2019). Pension plan sponsors that have offloaded liabilities to insurers through this strategy have saved on administrative costs and lowered funded status risk. In addition to buyouts as a de-risking strategy, there has also been continued growth in the number of plan terminations which ultimately end in a buyout contract and this trend will continue as plan funding levels continue to improve. It’s clear that annuity buyouts have served as a valuable strategy for pension plan sponsors.

Insurer solvency

Many insurers participating in the Pension Risk Transfer (“PRT”) arena saw a modest decline in solvency throughout 2020, although balance sheets remained strong at the end of the year. The specific drivers in 2020 which we will discuss in this article are:

- the impact of high death claims,

- the deterioration of investment portfolios in the weaker economic environment, and

- the impact of lower interest rates.

Impact of higher death rates has been manageable

Most PRT providers offer life insurance policies which have experienced higher payouts due to deaths associated with COVID-19. The good news here from the insurer’s perspective is that the number of deaths in the insured population, which is typically 35-65 year olds, has been manageable. As one PRT provider commented to us, “In terms of the financial impact, compared to the death scenarios we run, this isn’t a pandemic.”

80% of COVID-19 deaths have been in the 65 year old+ categories and these groups are not generally covered by life insurance policies.

There has been an approximate increase of ~10% in annualized death rates directly due to COVID-19. This generated some losses for life insurers but is materially below the severity that insurers reserve for – which tend to be more like multiples of the average death rate. Another consideration is that poorer socio-economic groups have seen significantly higher rates of COVID-19 deaths, yet life insurers have not been as exposed to claims here as these groups have smaller policies in force, if any life insurance at all. Insurers also re-insure pandemic risks away meaning that they will not experience the full force of any claims on their balance sheets beyond a certain level.

Finally, the virus has a higher mortality rate in old age so there may be, sadly, some benefit to insurers with large annuity books who no longer have to pay out annuities to these individuals.

The economic downturn has weakened investment portfolios

This is the area that potentially has the greatest negative impact to PRT providers. Over a year of restrictions have been in place which has placed stress on employment and the viability of many businesses and entire industries. However, economic activity is expected to return to normal over summer 2021 in developed countries and we are seeing a significant rebound in economic growth and an increase in inflation.

The majority of insurance company failures historically have arisen due to losses incurred on investment portfolios. Although the quality of insurers’ portfolios is high with relatively few equities, insurers are exposed to higher quality investment grade bonds being downgraded to sub-investment grade or ‘junk’ status. In addition, insurers hold loans secured on commercial property so we have focused our attention on any given insurer’s exposures to malls, offices, and hotels which are seeing lower demand. These trends could stretch well beyond 2021 as structural shifts in activities take place.

The reassuring news, in terms of the impact on investment portfolios, is that insurance companies can withstand a sizeable level of downgrades in their investment portfolios given their level of capitalization pre-COVID-19. In addition, the relatively worst hit sectors of the economy (airlines, hotels, restaurants, etc.) are not sectors that insurers are particularly exposed to. Commercial property portfolios at the PRT providers are typically not more than ~20% of total general account assets. Within these mortgage loan portfolios, insurers had generally been de-risking away from some riskier areas such as retail prior to 2020.

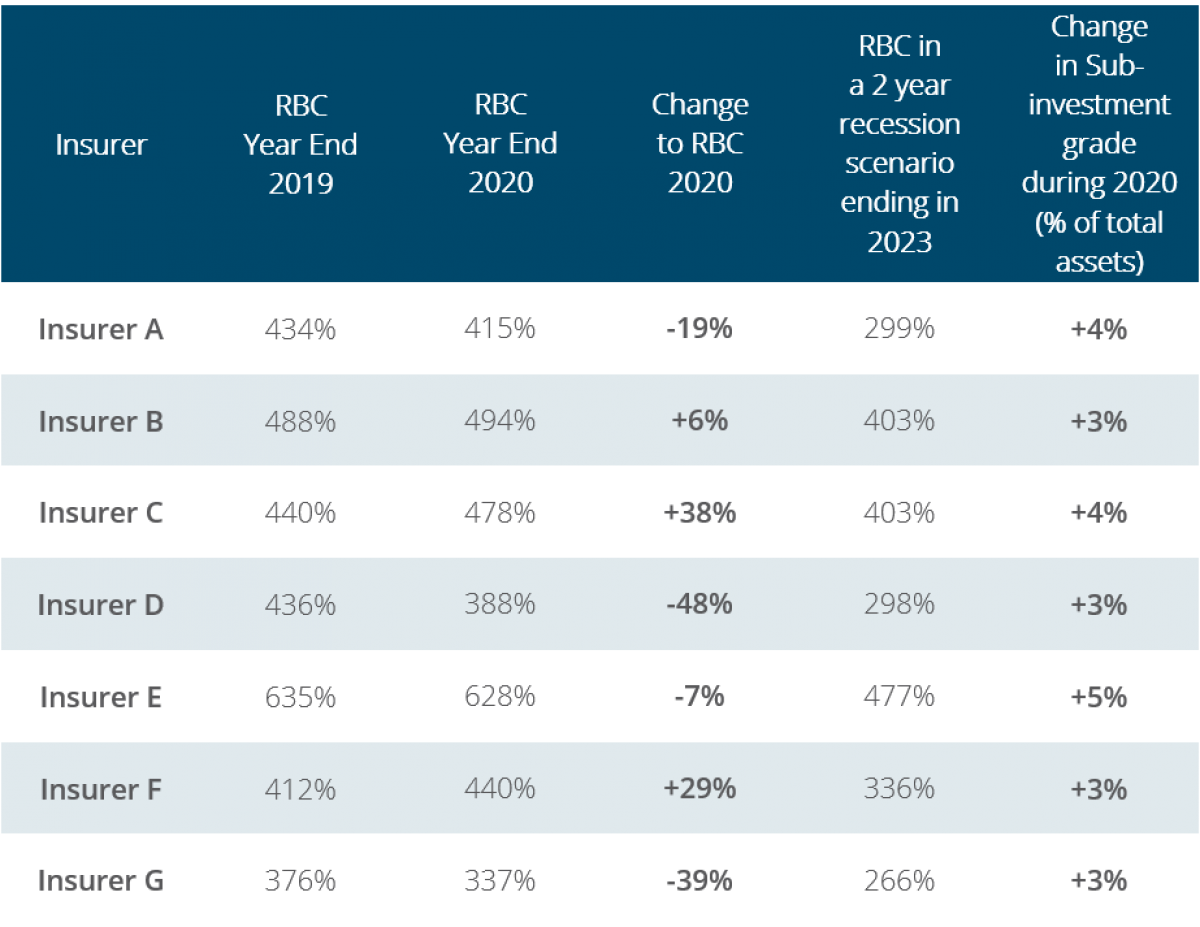

The chart below shows the change in the level of sub-investment grade rated assets for a number of sample insurers, the Risk Based Capital (“RBC”) ratio in 2019 and 2020, and the RBC in a 2 year recessionary scenario assumed to end in 2023. Although our expectation is a continued economic recovery from here, we have stressed insurers’ balance sheets to understand what happens if a more severe scenario than expected occurs.

The RBC ratio coverage is the amount of excess capital insurers hold vs a minimum level, set by regulators, with regards to the size of the company and the risks being run. A higher number indicates greater financial strength all else being equal, and the PRT industry average was approximately ~400% prior to COVID-19.

Calculations assume that in a 2 year period starting end 2020, portfolios experience a similar level of defaults and downgrades as experienced in the US from the end of March 2008 to the end March 2009. Calculations assume no action is taken to rebalance investment portfolios, and that there are no other changes to capital requirements due to other risks. 30% of the C1 capital charge increase is assumed to apply to the total capital requirement.

To summarize the above:

There has been a deterioration in the credit quality of investment portfolios. The proportion of assets rated sub-investment grade typically increased by 2-5% of total assets.

The impact on capital coverage levels was mixed with some insurers improving, and others deteriorating. The PRT industry average was slightly negative. In cases where capital improved we often observed insurers had taken actions throughout 2020 supportive to capital, such as injecting cash from outside the insurance company entity. With the benefit of hindsight allowing for the recovery we have seen in 2021, some of these actions now appear overkill. Therefore, a few insurers are now actually in a stronger capital position going forward than they were pre-COVID-19.

Low interest rates have weighed on profitability

Following the onset COVID-19, the Federal Reserve cut interest rates to near zero and long dated interest rates also fell significantly. 2021 has seen a reversal of this effect with long term interest rates increasing at least partly due to rising inflation expectations.

A persistently low interest rate environment is bad for life insurance companies. Although the PRT providers hedge interest rates much more tightly than a typical pension plan, falling interest rates generally do increase reserve requirements and weaken capital levels, particularly where insurers offer products with minimum investment return. Lower absolute levels of rates also reduce the profit margins on many products insurers sell. We observed earnings of many PRT providers fall in 2020, with low interest rates often cited as the major driver.

We regard the low interest rate environment as less of a solvency concern for the PRT providers, and more of headwind for future profitability going forward - which is more of an issue for stock holders of these insurance companies.

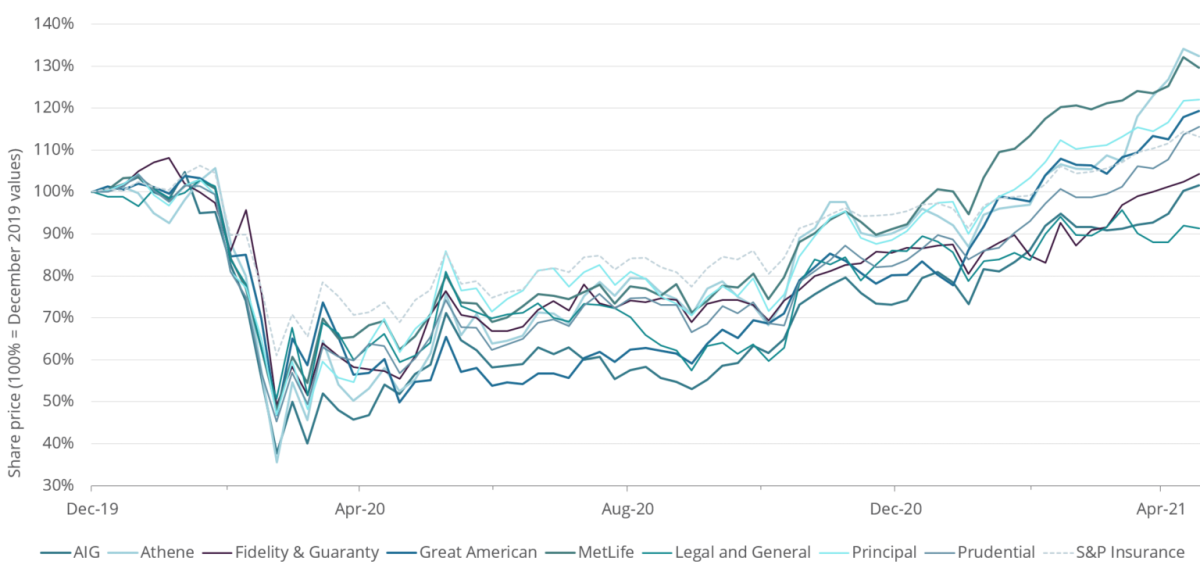

A higher inflationary environment combined with higher interest rates is, all else being equal, a positive for insurance companies’ profitability in the long term. Insurance company share price has seen a substantial recovery in 2020 into 2021 as economic expectations have improved:

What does this mean for plan sponsors?

Sponsors undertaking an annuity transaction can take heart in the fact that all insurers active in the PRT market, at the time of this writing, are still very likely to remain solvent and meet their obligations to make payments. The security of participant benefits is still likely to remain higher in an insurance company, with associated guarantees, than it is in any private pension plan.

In the current uncertain environment, it is critical that plan fiduciaries are aware of the risks and undertake due diligence on insurance companies. Fiduciaries are encouraged by Department of Labor Bulletin 95-1 to select the “safest annuity available” and to “conduct an objective, thorough, and analytical search.“ They are encouraged to hire an “Independent Expert” if they are unable to do this themselves. In the cases we have been involved with, special attention has been given to how a particular insurer has adjusted to the various effects of COVID-19.

Insurance companies report results periodically, with some mutual companies only releasing detailed data annually. Therefore, to be comfortable with an insurer at the point of an annuity placement, it is essential for your annuity placement provider or independent expert to have a deep understanding of how the insurers are likely to be affected in the current environment. Going beyond standard credit due diligence, for example, assessing insurers’ ability to service participants off site in a disaster environment, also takes on particular importance in these times.

Conclusion

Given the current market environment, plan sponsors need to have an annuity placement specialist that can form an opinion on the credit worthiness of participating insurers and provide fiduciary cover under DOL 95-1. Because insurer solvency concerns are in a state of flux, the right specialist will have a rigorous process for looking at how the markets are affecting the insurers and their ability to provide the safest available annuity. For our annuity placement clients, we have included additional documentation related to the impact of COVID-19 to give plan fiduciaries piece of mind in making their selection of an annuity provider.

About the Author

James Walton is an Investment Director in River and Mercantile’s Boston office. James works with clients on financial risk management, develops investment strategies and derivative solutions. He also leads the due diligence of annuity providers and is a member of the US Investment Committee. James joined River and Mercantile in May 2016 from Legal and General, a UK based insurance group. He performed a number of investment management roles relating to the retirement business. This included ALM, credit strategy, illiquid assets and responsibility for the investment strategy of the US Pension Risk Transfer business. James started his career at Aon as an ALM consultant to defined benefit pension plans where he also developed Aon’s LDI, strategic asset allocation processes and analytics. James is a qualified actuary and holds a Masters degree in Physics (Summa Cum Laude) from The University of Oxford.

INVESTMENT ADVISOR: Investment advisory services are provided by River and Mercantile LLC, an investment advisor registered with the US Securities and Exchange Commission and the National Futures Association.

PAST PERFORMANCE IS NOT AN INDICATION OF FUTURE RESULTS.