By Jose R. Michaelraj, CAIA, CIPM, is a Senior Consultant at Meradia.

Despite the enormous growth in alternative investments, performance measurement practices in this space continue to be rough around the edges. There’s more to this than simply adding a couple of terms to the numerator or denominator of a traditional performance calculation to make it ‘alternative ready’. Unique characteristics (leverage, risk, long-short strategies, and benchmarking, in particular) underlying alternative investments pose a unique set of challenges because leverage can create negative denominators in the return calculation.

‘Performance Measurement for Alternative Investments’ by Timothy Peterson, CFA, CAIA is an in-depth exploration into this complex, interesting area. The terms ‘Investment Performance’ and ‘Alternatives’ intersect a wide variety of concepts, and this book adds to the body of knowledge rather than simply commenting on existing material. Written by an accountant, the book addresses a plethora of terminologies common to traditional and alternative investments.

Mixing valuations that come from the accounting arena with multi-period returns that originate and reside in performance has given rise to a new field (i.e. not a pure intersection alone) with its own unique measurement approaches and calculation frameworks. Adding to the confusion and challenge is the varying ways in which alternative investments can be defined. At times, they are categorized by the nature of asset classes (for example, Real Estate and Infrastructure). In other instances, the investment vehicle i.e. the approach through which investments are made define alternatives (for example, long short funds). Regulations also play a role. Traditional investment vehicles i.e. mutual funds, have thresholds defined for derivatives and alternative assets. Breaching those thresholds sends the vehicle into the realms of alternatives.

A defining feature of the book is its tendency to describe several approaches along with practical implications. The book is a how-to manual, providing a first-of-its-kind hierarchy that addresses all the various fee and expense treatments associated with alternative investment vehicles. Concepts are provided with specialized context so practitioners can address selective scenarios; for example, how to calculate and report returns on derivatives and other assets that use notional values.

The book is divided into 2 parts, consists of 15 chapters and two appendices. It covers four significant knowledge areas:

Alternative investment strategies/products: Answers to the following key questions are presented - a) What are the characteristics of alternative investment strategies. b) How do they stand in comparison with traditional investments c) What are the types of alternative investment strategies (public, private, and crossover) d) How is a hedge fund different from a private fund? e) How to value and handle real estate that often has a combination of debt, private and public equity characteristics?

Basic return measurement approaches: The differences between time-weighted return and money-weighted returns have been well documented in the industry. The author provides a quick overview, discusses arithmetic, geometric and most importantly the lognormal approach that is perhaps the only method allowing us to sum returns down and across. Pertinent points regarding continuous compounding which has close semblance to the real world and comparison with time-weighted/money-weighted approaches that utilize discrete methods are well made.

Three return calculation methods (accounting, notional & comparative portfolio value) are provided for forwards, futures and options. All of them would yield similar results, with the accounting method providing componentized numbers. Options with delta adjusted notional value calculations could have provided more enrichment to this section. The ‘currency surprise’ return portion in currency overlays is illustrated well with a worked-out example.

Other calculations and benchmarking approaches: Debt-related adjustments add another flavor to return calculations done for real estate. Moreover, the return measurement could be done at several levels – property, investment, fund and composite. Not all alternatives utilize the same return formulas. Private Equity has a handful of ratios that provide insight into how much returns have been earned over the life of the fund. They are sometimes known as multiples (TVPI, DPI, etc.).

A holistic framework provided for the treatment of fees (not just alternatives) is an interesting section of this book. It suggests a fee hierarchy i.e. pure gross, gross, net, net-net & pure net and how insights are obtained at each return level. After discussing how conventional properties of a valid benchmark are not suitable for alternatives, the book discusses ICM-PME & Kaplan-Scholar methodology PME with detailed examples.

Regulatory Considerations: An extremely important and often overlooked area is the regulatory space. It assumes greater significance in alternatives as a firm would have to comply with several regulators based on the invested asset types. Regulations often tend to define what should be done (core rules), what need not be done conditionally (exemptions) and what might be best practice (recommended). The book covers a wide gamut of regulations including SEC, NFA, CFTC, NCREIF and INREV to name a few.

Timothy Peterson’s book is at times defining, debating and theorizing, ultimately creating a useful and unique perspective for analysts and practitioners alike.

Here’s a short Q&A with the author, Timothy Peterson:

Jose Ranjit Michaelraj: What prompted you to write this book and can you describe the journey from spark to draft?

Timothy Peterson: In my career and had worked in a performance measurement function, but also spent considerable time outside performance in some alternative asset firms. After consulting to alternative firms and speaking at conferences for about ten years, I realize I had accumulated enough material to write a book.

The guidance on this topic coming from the standard-setting community was rather academic and generic. I looked at things from a practitioner’s point of view: real assets, real clients, and real problems that needed to be solved. I wanted to write a “how-to” book.

The book was mostly written in the middle of the night during bouts of insomnia. I sent a draft to Carl Bacon who gave positive feedback but suggested the publisher would want to see twice as much material. I spent almost another year writing after that. I learned that writing a book was like building your own house: it’s never complete, and you’re never really happy with it. I would go to FedEx Office and have them print and bind a double-sided copy (300+ pages) for me to proofread. I had a stack of 9 drafts, each as thick as a bible, before I even sent it to a publisher. By the end of the process, I was exhausted and felt no joy in it. I swore I’d never write another book.

Currently, I’m writing 3 books: a bitcoin investment thesis, one on digital asset investment, and another on network effects.

Jose Ranjit Michaelraj: Can you pick out the most interesting example so we can share a lesson?

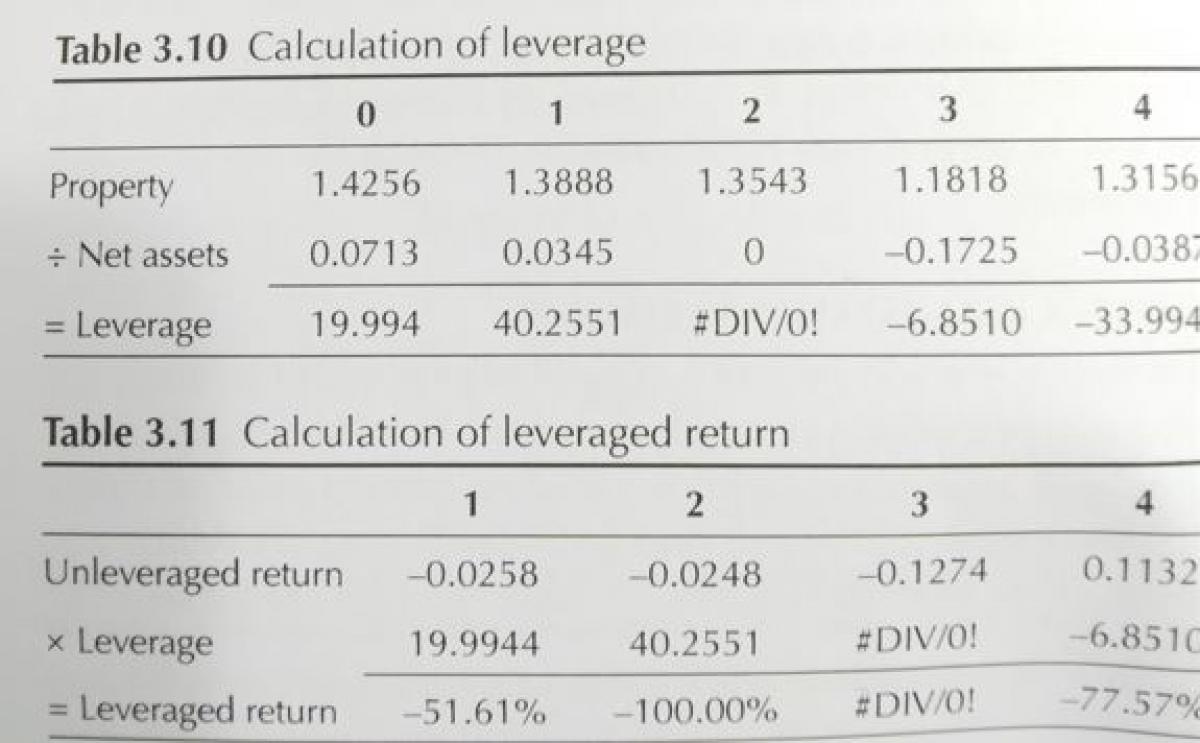

Timothy Peterson: The main theme of the book is that there are always two returns in a portfolio: a leveraged return (ROE) and an unleveraged return (ROA). ROA = ROE in the special case where there is no leverage. However, leverage is a defining characteristic of alternative investments. So much of the confusion in performance reporting and evaluation can be traced to the treatment of leverage.

Shortly after the GFC, real estate was being written down and prices declined. One firm I knew was writing down the fair value of the property to equal the value of the loan. This resulted in a portfolio equity of zero, which meant the denominator of the performance calculation was zero. What to do?

To solve this problem one must calculate three numbers a return on assets, a return on equity, and a leverage ratio. It should always be possible to calculate a return on assets. The remainder of the solution relies on disclosure, not calculation. This example is shown on Page 76 in tables 3.9-3.11.

Jose Ranjit Michaelraj: What area(s) within performance measurement for alternatives do you think deserves more attention by the industry?

Timothy Peterson: By far, I think more needs to be done regarding the calculation and disclosure of leverage (to include short positions and derivatives). Leverage can take an ordinary expected loss and turn it into a catastrophic loss from which there is no recovery.

Most alternative strategies are directed at institutional, qualified, and accredited investors. This class of investors is assumed to have sufficient knowledge and sophistication to evaluate risk. But how can the risk be evaluated if it is not properly measured and disclosed? Simply disclosing return and variance is not enough.

Most risk disclosures are legal boilerplate. There is a big difference between disclosing that the “portfolio may lose value” versus disclosing that the portfolio has routinely been exposed to 20x leverage.

In my career, I have watched LTCM, Lehman, and Archegos all blow-up, and all due to leverage. They were all supposedly run by “the best of the best.” Archegos was a multi-billion-dollar New York money manager that ticked all the “right” boxes: Ivy League employees, huge assets, and track record experience that grew from the most prestigious Wall Street firms and hedge funds. Lehman was a 158-year Wall Street giant with $600 billion in assets. LTCM’s board boasted two Nobel Laureates. It managed $1 trillion, nearly 5% of the global bond market. Yet each of these companies was completely destroyed. These were not black swan events, each was completely preventable.

About the Author:

Jose R. Michaelraj, CAIA, CIPM, is a Senior Consultant at Meradia who plays a central role in the Performance, Risk & Analytics practice. He brings more than 15 years of progressive, varied investment services experience; establishing performance system architectures being one of them.

For the global risk solutions group of an asset servicing client, Jose redesigned important aspects of investment performance systems, established best practices for the information delivery framework and standardized performance validation procedures across the US, Europe, and India. He has been involved in the strategic assessment of performance vendor products and led some of them. His strong domain, functional and technical skills combined with end-to-end process knowledge, data management expertise and project leadership mostly result in effective solutions. Leveraging his strengths from traditional performance, he is curious about bringing efficiencies into the alternatives space. Daytime professional and nocturnal seeker of truth.